- Healthcare Services

- Aerospace Medicine Market

Aerospace Medicine Market Size, Share, and Growth Forecast, 2025 - 2032

Aerospace Medicine Market By Service Type (Military, Operational, Others), Application (Prevention, Diagnosis, Others), End-use, and Regional Analysis for 2025 – 2032

Aerospace Medicine Market Size and Trends Analysis

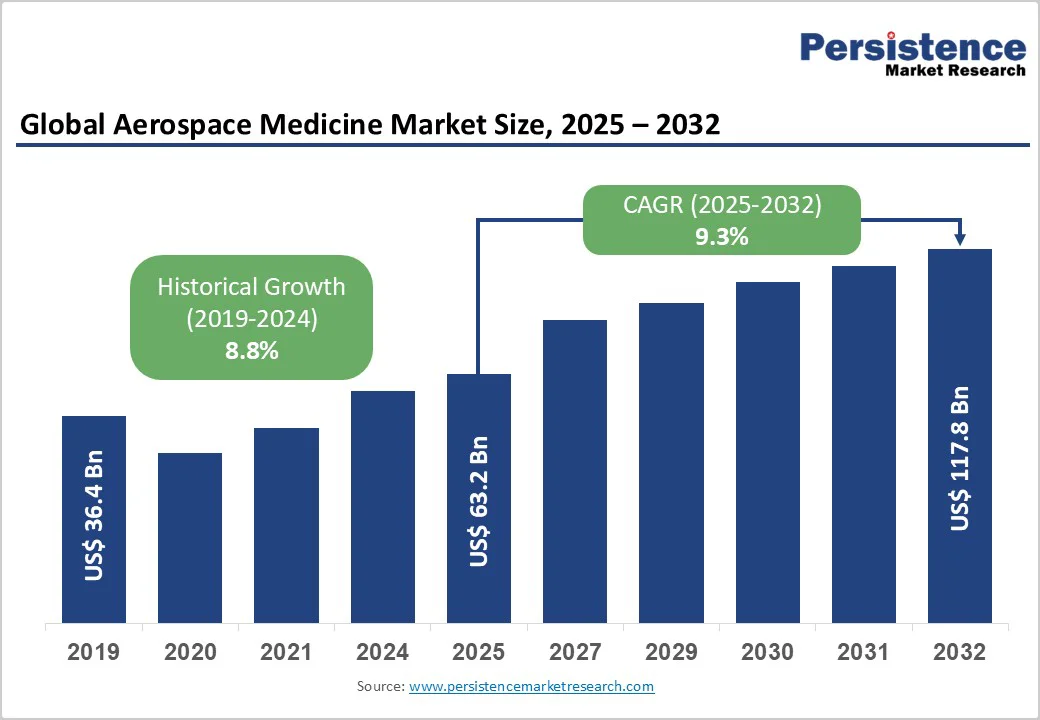

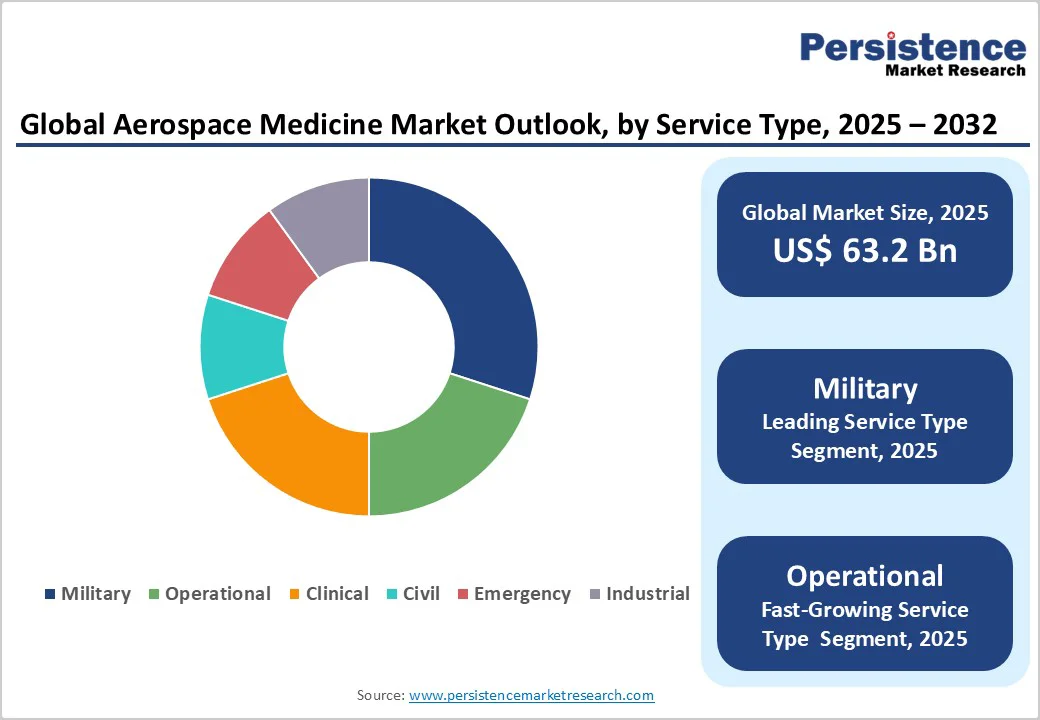

The global aerospace medicine market size is likely to be valued US$63.2 Billion in 2025, anticipated to reach US$117.8 Billion by 2032 at a CAGR of 9.3% during the forecast period from 2025 to 2032 driven by the increasing number of space exploration missions, rising commercial space tourism, and advancements in human spaceflight health management.

The market is further propelled by innovations in telemedicine for space and AI-driven diagnostic tools, catering to preferences for preventive care and recovery in extreme environments.

The growing acceptance of aerospace medicine as essential for safe human spaceflight, especially with private sector involvement, is a key growth factor.

Key Industry Highlights:

- Leading Region: North America, commanding a 35% market share in 2025, driven by NASA's investments and private space initiatives in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by expanding space programs in China and India, and rising commercial aviation health needs.

- Dominant Service Type: Military, holding approximately 30% of the market share, due to defense requirements for aviator fitness and mission safety.

- Leading Application: Prevention, accounting for over 40% of market revenue, driven by pre-flight assessments and training protocols.

- Leading End-use: Space Agencies, contributing nearly 25% of market revenue, owing to human spaceflight health monitoring.

- Key Market Driver: Expanding government and private space missions, including long-duration flights and space tourism, increase demand for specialized astronaut health services.

- Growth Opportunity: Advancements in AI for real-time diagnostics, enabling telemedicine in long-duration spaceflights.

| Key Insights | Details |

|---|---|

| Aerospace Medicine Market Size (2025E) | US$63.2 Bn |

| Market Value Forecast (2032F) | US$117.8 Bn |

| Projected Growth (CAGR 2025 to 2032) | 9.3% |

| Historical Market Growth (CAGR 2019 to 2024) | 8.8% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Space Exploration and Commercial Aviation Demands

The global aerospace medicine market is being significantly driven by increasing space exploration and growing commercial aviation demands. Expanding government-funded space programs and private space ventures, including companies such as NASA, SpaceX, Blue Origin, and Virgin Galactic, are pushing the boundaries of human spaceflight. Long-duration missions, deep-space exploration, and emerging space tourism initiatives require specialized medical services to ensure astronaut and passenger safety, monitor physiological changes, and provide effective countermeasures for microgravity, radiation exposure, cardiovascular strain, and psychological stress. These developments create a sustained need for operational, preventive, and treatment-focused aerospace medicine solutions.

The commercial aviation sector is experiencing growth due to rising passenger traffic, especially in long-haul and international flights. Airlines are increasingly adopting aerospace medical protocols to address in-flight health challenges, including fatigue management, cardiovascular monitoring, and infectious disease prevention.

High Costs and Regulatory Hurdles

The sector faces significant challenges due to high costs and stringent regulatory hurdles, which can limit market growth and slow adoption of new technologies. Developing specialized medical protocols, equipment, and monitoring systems for aviation and space environments requires substantial investment in research and development. Costs associated with advanced health monitoring devices, telemedicine platforms, and training programs for pilots, astronauts, and crew are often prohibitive, particularly for emerging companies and smaller private space ventures. Additionally, the high expense of testing, certification, and implementing medical solutions in extreme environments further increases operational costs.

Regulatory hurdles add another layer of complexity. Aerospace medicine is subject to strict guidelines from national and international agencies, such as the FAA, ESA, NASA, and other aviation and space authorities. Compliance with safety standards, medical certifications, and reporting requirements is mandatory, and failure to meet these regulations can result in operational delays or financial penalties.

Expansion in Space Tourism and Telemedicine

The aerospace medicine market is witnessing significant opportunities through the expansion of space tourism and the adoption of telemedicine technologies. The emergence of private space travel ventures, including companies such as SpaceX, Blue Origin, and Virgin Galactic, has created a demand for specialized medical services that ensure the health and safety of tourists during suborbital and orbital flights. Space tourists face unique physiological challenges, including exposure to microgravity, rapid acceleration, radiation, and psychological stress. Aerospace medicine providers are developing pre-flight assessments, in-flight monitoring, emergency protocols, and post-flight rehabilitation programs to mitigate these risks, ensuring a safe and comfortable travel experience.

Telemedicine is transforming aerospace medical services by enabling real-time health monitoring and remote diagnostics. Wearable devices, AI-driven diagnostic tools, and satellite communication systems allow medical teams to track vital signs, detect early symptoms, and provide guidance to pilots, crew, and astronauts even in remote or extreme environments.

Category-wise Analysis

Service Type Insights

Military dominates the market, account 30% of the share in 2025. Its leadership is driven by aviator fitness programs, health monitoring, and specialized medical support to maintain combat readiness. These measures are essential for defense operations, ensuring pilots and aircrew can safely perform under high-stress conditions, extreme environments, and prolonged missions.

Operational is the fastest-growing segment, driven by the rise of commercial spaceflight. It focuses on mission planning, in-flight health monitoring, and risk management, supporting safe and efficient space tourism. Rapid adoption by private aerospace ventures highlights its critical role in ensuring crew and passenger health during commercial missions and emerging space travel activities.

Application Insights

Prevention leads with 40% share, driven by comprehensive pre-flight health assessments, training, and risk mitigation strategies. These measures help identify potential medical issues, prepare astronauts and aircrew for physiological and psychological challenges, and reduce the likelihood of in-flight complications, ensuring safety and optimal performance during space missions and aviation operations.

Treatment is the fastest-growing, driven by the need for effective recovery protocols for space-related injuries and health conditions. Longer-duration missions expose astronauts to muscle atrophy, bone density loss, and cardiovascular strain, necessitating advanced medical interventions, rehabilitation programs, and innovative therapies to ensure safe recovery and maintain crew performance during and after spaceflight.

End-use Insights

Space Agencies hold 25% share, focusing on astronaut health during deep space missions. They develop specialized medical protocols, countermeasures for microgravity and radiation exposure, and monitoring systems to ensure physical and psychological well-being. These initiatives are critical for long-duration missions and the safety and performance of space crews.

Commercial Aviation is the fastest-growing, driven by increasing focus on passenger wellness during long-haul flights. Airlines are adopting preventive health measures, fatigue management protocols, and in-flight medical monitoring to ensure passenger safety and comfort. Rising health awareness and regulatory requirements further accelerate demand for specialized medical services in the commercial aviation sector.

Regional Insights

North America Aerospace Medicine Market Trends

North America accounts for 35% in 2025, driven by significant investments in space exploration and aviation health initiatives, particularly through NASA, which maintains a multi-billion-dollar budget dedicated to space research, astronaut health, and technological innovations. Concurrently, private aerospace companies such as SpaceX are expanding crewed space missions, creating increased demand for specialized operational medicine and in-flight healthcare solutions. Trends in the region emphasize the integration of artificial intelligence (AI) and machine learning for diagnostics, health monitoring, and predictive medical interventions, improving safety and efficiency for both astronauts and aviation personnel.

The U.K. market falls under Europe, it mirrors North American developments, supported by funding from the UK Space Agency and growing interest in commercial space travel. Health monitoring systems, preventive care programs, and telemedicine platforms are being increasingly adopted to meet the medical needs of pilots, astronauts, and space tourists.

Europe Aerospace Medicine Market Trends

Europe holds about 25% market share, led by Germany and France emerging as leading contributors. The region’s growth is strongly supported by collaborative initiatives under the European Space Agency (ESA), which focus on advancing astronaut health, operational medicine, and preventive healthcare protocols for space missions. ESA-funded research programs develop countermeasures for microgravity-induced muscle and bone loss, radiation exposure, cardiovascular challenges, and psychological stress, ensuring astronaut safety during long-duration missions.

In parallel, major aerospace companies such as Airbus are actively implementing health programs for pilots, crew, and aerospace personnel. These programs emphasize preventive care, fatigue management, medical monitoring, and emergency preparedness, addressing the unique physiological and operational risks associated with aviation and space environments. Germany and France also benefit from robust medical infrastructure, advanced research institutions, and regulatory frameworks that support high standards of aerospace medicine practice.

Asia Pacific Aerospace Medicine Market Trends

Asia Pacific commands around 20% share and is the fastest-growing region. This growth is largely fueled by the rapid expansion of space programs in China and India. China’s space agency, CNSA (China National Space Administration), continues to launch ambitious missions, including crewed spaceflights and space station operations, which require comprehensive aerospace medical support to ensure astronaut health and performance in microgravity and high-radiation environments. Similarly, India’s ISRO (Indian Space Research Organisation) is expanding its capabilities in satellite launches, crewed missions, and long-duration space projects, further driving the need for specialized operational medicine services in the region.

The increasing scale and complexity of space activities have prompted investments in research, medical infrastructure, and technological innovations, including telemedicine, health monitoring systems, and countermeasures for physiological challenges like bone density loss, cardiovascular strain, and psychological stress.

Competitive Landscape

The global aerospace medicine market is highly competitive, driven by rapid advancements in aviation and space exploration, along with increasing demand for specialized healthcare services for aircrew, astronauts, and commercial passengers. Major players are focusing heavily on research and development (R&D) to innovate solutions that address the unique physiological challenges of aerospace environments, including microgravity, high G-forces, radiation exposure, and long-duration missions. These innovations encompass advanced medical monitoring systems, wearable health devices, telemedicine platforms, and countermeasures to prevent muscle atrophy, bone loss, and cardiovascular strain in astronauts and pilots.

Strategic partnerships and collaborations are also shaping market dynamics. Companies such as NASA, Boeing, SpaceX, Lockheed Martin, and Blue Origin are partnering with academic institutions, healthcare technology firms, and regulatory agencies to develop comprehensive aerospace health solutions.

Key Developments:

- In March 2025, Defense Minister Rajnath Singh launched a new ICMR research project at the Indian Air Force Institute of Aerospace Medicine (IAM) in Bengaluru. The project is titled "Space Psychology: Selection and Behavioral Health Training of Astronauts & Astronaut Designates for Indian Space Missions," and aims to bolster research in astronaut psychology for future Indian space missions.

- In April 2025, the Indian Space Research Organisation (ISRO) partnered with the Sree Chitra Tirunal Institute for Medical Sciences & Technology (SCTIMST) to develop space medicine solutions for the Gaganyaan human spaceflight program. The collaboration will focus on areas like astronaut physiology, telemedicine, radiation protection, and mental health.

Companies Covered in Aerospace Medicine Market

- NASA

- SpaceX

- Boeing

- ICMR

- ISRO-SCTIMIST

- Lockheed Martin

- Blue Origin

- Virgin Galactic

- Northrop Grumman

- the European Space Agency (ESA)

Frequently Asked Questions

The global aerospace medicine market is projected to reach US$63.2 Bn in 2025, driven by surging space missions and commercial aviation health needs.

Increasing passenger traffic, particularly in long-haul flights, drives the need for in-flight health monitoring, fatigue management, and preventive care for pilots and crew.

The market is poised to witness a CAGR of 9.3% from 2025 to 2032, supported by AI diagnostics and telemedicine innovations.

Expansion in space tourism projected at US$10 Billion by 2030 offers key opportunities for preventive and recovery services in commercial flights.

Key players include NASA, SpaceX, Boeing, Lockheed Martin, and ESA, leading through R&D in space health and mission support