- Aerospace & Defense

- Aerospace Fasteners Market

Aerospace Fasteners Market Size, Share, and Growth Forecast, 2026 - 2033

Aerospace Fasteners Market by Material Type (Aluminum, Titanium, Stainless Steel, Superalloy, Others), Superalloy Material (A286, Inconel 718, Waspaloy, Others), Application (Airframe, Engine, Interiors, Others), and Regional Analysis for 2026 – 2033

Aerospace Fasteners Market Size and Trends Analysis

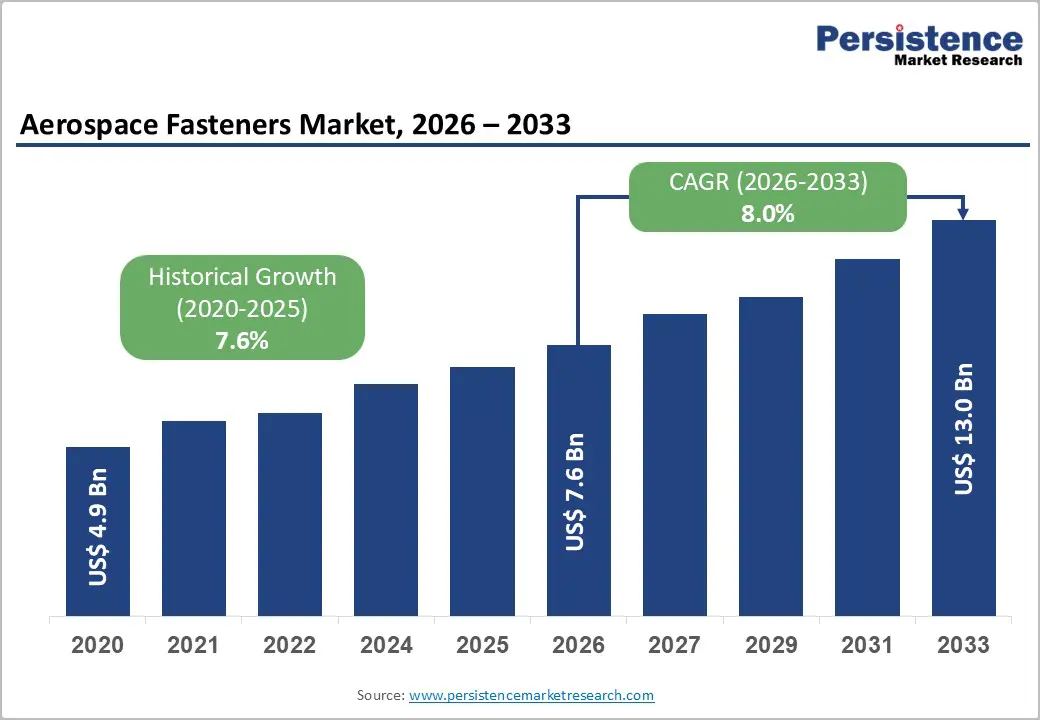

The global aerospace fasteners market size is likely to be valued at US$7.6 billion in 2026, and is expected to reach US$13.0 billion by 2033, growing at a CAGR of 8.0% during the forecast period from 2026 to 2033, driven by the increasing prevalence of new aircraft production, rising aftermarket demand for MRO (maintenance, repair, and overhaul), and growing adoption of lightweight, high-strength fasteners in commercial and defense platforms.

Growing demand for titanium and superalloy aerospace fasteners, especially in airframe and engine applications, is accelerating adoption across OEMs and aftermarket channels. Advances in corrosion-resistant coatings, additive-manufactured fasteners, and hybrid material designs are further boosting uptake by offering better fatigue life and weight savings. Increasing recognition of aerospace fasteners as critical for structural integrity, weight reduction, and extended service intervals in emerging sustainable aviation and next-generation aircraft markets remains a major driver of market growth.

Key Industry Highlights:

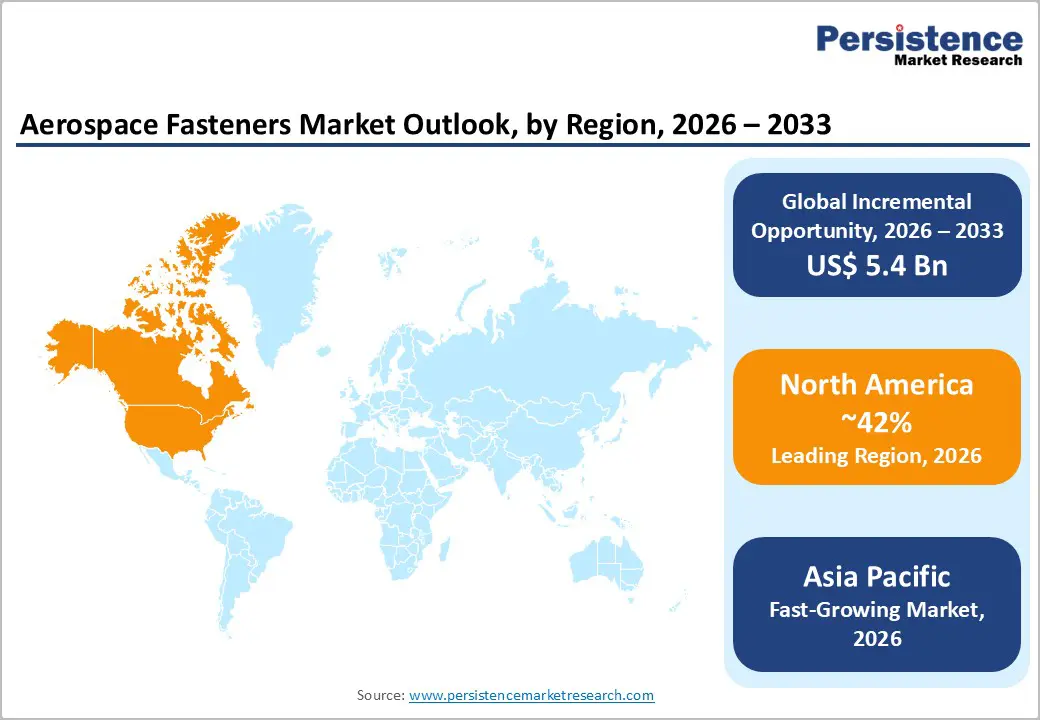

- Leading Region: North America, anticipated to account for a 42% market share in 2026, driven by dominant OEM production (Boeing, Lockheed Martin), strong defense spending, and high MRO volumes in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by rapid fleet expansion, increasing domestic aircraft manufacturing (COMAC, HAL), and growing aftermarket demand in China and India.

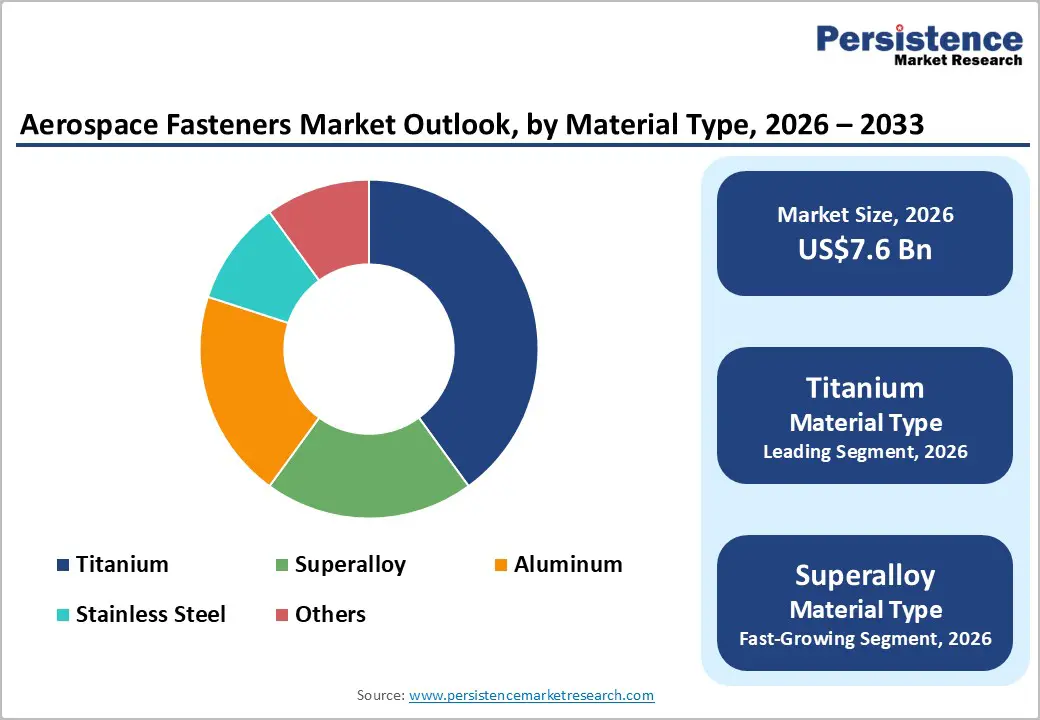

- Dominant Material Type: Titanium, to hold approximately 45% of the market share, as it offers the best strength-to-weight ratio and corrosion resistance.

- Leading Application: Airframe, accounting for over 52% of the market revenue, due to the highest fastener count per aircraft.

| Key Insights | Details |

|---|---|

| Aerospace Fasteners Market Size (2026E) | US$7.6 Bn |

| Market Value Forecast (2033F) | US$13.0 Bn |

| Projected Growth CAGR (2026-2033) | 8.0% |

| Historical Market Growth (2020-2025) | 7.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Surging Commercial Aircraft Production and Aftermarket MRO Demand

The commercial aviation sector is experiencing significant growth, driven by rising air travel demand and fleet expansions, particularly in emerging markets. Airlines are increasingly placing orders for new, fuel-efficient aircraft to meet passenger growth and reduce operating costs, resulting in a surge in commercial aircraft production. This expansion is supported by technological advancements in aircraft design, lightweight materials, and more efficient engines, enabling manufacturers to deliver higher-performance planes while adhering to stricter environmental regulations.

Production growth and the demand for aftermarket maintenance, repair, and overhaul (MRO) services are also accelerating. As fleets age and operational intensity rises, airlines require comprehensive MRO solutions to ensure aircraft safety, reliability, and compliance with regulatory standards. Predictive maintenance technologies, digital monitoring systems, and advanced repair techniques are enhancing service efficiency, reducing aircraft downtime, and optimizing operational costs.

Increasing Adoption of Lightweight and High-Strength Materials

The aerospace, automotive, and transportation sectors are increasingly embracing lightweight and high-strength materials to improve efficiency, performance, and sustainability. These materials, including advanced aluminum alloys, titanium, carbon fiber-reinforced polymers, and high-performance composites, offer a superior strength-to-weight ratio compared to traditional metals. By reducing structural weight, manufacturers can enhance fuel efficiency, lower emissions, and increase payload capacity, which is especially critical in aviation and electric vehicles where energy efficiency directly impacts operational cost and range.

Beyond energy considerations, lightweight and high-strength materials contribute to improved safety and durability. High-strength alloys and composites can withstand greater stress, fatigue, and corrosion, extending the lifespan of components while maintaining structural integrity under extreme conditions. Their adoption also enables innovative design possibilities, allowing engineers to create complex geometries and optimize aerodynamics without compromising performance.

Barrier Analysis – High Raw Material Costs and Supply Chain Volatility

Industries across the globe are facing significant challenges due to high raw material costs and supply chain volatility. Prices of critical inputs such as metals, polymers, and specialty chemicals have surged, driven by factors like resource scarcity, geopolitical tensions, inflationary pressures, and rising energy costs. These increases directly affect manufacturing expenses, squeezing profit margins for companies and sometimes forcing them to adjust product pricing or limit production.

Supply chain volatility further complicates the situation. Disruptions caused by natural disasters, geopolitical conflicts, labor shortages, and transportation bottlenecks have made it difficult for manufacturers to secure consistent supplies of essential materials. Extended lead times and fluctuating availability create uncertainty, making it challenging to plan production schedules, maintain inventory levels, and meet customer demand reliably. Companies are responding by diversifying suppliers, exploring alternative raw materials, and adopting digital supply chain management tools to improve visibility and agility. Strategic stockpiling and closer collaboration with suppliers are also being leveraged to mitigate risks.

Stringent Certification and Qualification Cycles

Stringent certification and qualification cycles have become a defining feature of industries such as aerospace, automotive, medical devices, and electronics, where safety, reliability, and regulatory compliance are paramount. These cycles involve rigorous testing, documentation, and approval processes that ensure products meet exacting standards before they can enter the market. Certification authorities, whether governmental agencies or industry bodies, require manufacturers to demonstrate consistent performance under various operational conditions, adherence to material specifications, and compliance with environmental and safety regulations.

While these processes are essential for safeguarding end-users and ensuring long-term product reliability, they also extend development timelines and increase costs. Each iteration of design, testing, and validation can take months or even years, particularly for high-technology products where failure can have severe consequences. Companies must allocate substantial resources to maintain quality management systems, conduct repeated testing, and maintain detailed records to satisfy auditors and regulators. Qualification cycles are often influenced by evolving standards and emerging technologies, requiring continuous adaptation and re-certification.

Opportunity Analysis – Expansion of Additive-Manufactured and Coated Aerospace Fasteners

The aerospace industry is witnessing a growing expansion in the adoption of additive-manufactured (AM) and coated fasteners, driven by the need for lightweight, high-performance, and corrosion-resistant components. Additive manufacturing enables the production of complex geometries that are difficult or impossible to achieve through traditional machining, allowing engineers to optimize fastener design for strength, weight reduction, and material efficiency. This capability is particularly valuable in aerospace, where every gram of weight saved contributes to fuel efficiency and overall aircraft performance.

Coated fasteners are also gaining prominence due to their ability to withstand extreme environmental conditions, including high temperatures, humidity, and exposure to corrosive chemicals. Advanced coatings, such as titanium nitride, zinc-nickel, or ceramic-based layers, enhance wear resistance, reduce friction during assembly, and extend the service life of components. Combining additive manufacturing with advanced coating technologies allows manufacturers to produce fasteners that are not only lightweight but also highly durable and reliable in critical applications, such as airframe structures, engines, and landing gear.

Development in Urban Air Mobility and Sustainable Aviation

Urban Air Mobility (UAM) and sustainable aviation are emerging as transformative trends in the aerospace industry, driven by rising urbanization, environmental concerns, and advancements in electric propulsion technologies. UAM focuses on the development of small, efficient air vehicles, including electric vertical take-off and landing (eVTOL) aircraft, designed to provide rapid, on-demand transport within cities and between urban hubs. These vehicles aim to reduce ground congestion, improve connectivity, and offer flexible, time-saving transportation alternatives.

Sustainable aviation is being prioritized through innovations in fuel efficiency, electrification, and the use of alternative energy sources such as hydrogen and sustainable aviation fuels (SAFs). Aircraft manufacturers and airlines are investing in lightweight materials, aerodynamic optimizations, and hybrid-electric propulsion systems to lower carbon emissions and meet stricter environmental regulations. Integration of digital technologies, such as predictive maintenance and AI-based traffic management, further enhances operational efficiency while reducing environmental impact.

Category-wise Analysis

Material Type Insights

Titanium is expected to lead the market in 2026, capturing around 45% of the total share, due to its exceptional combination of strength, lightweight properties, and corrosion resistance. Its high strength-to-weight ratio makes it ideal for aerospace, automotive, and industrial applications where performance and fuel efficiency are critical. Titanium’s durability under extreme temperatures and harsh environments enhances its appeal for critical structural components and high-performance fasteners. The Boeing, Seattle, WA, USA 787 Dreamliner incorporates about 15 % titanium by weight in its airframe, particularly in engine components, fasteners, and other structural parts. This high proportion of titanium helps reduce weight while maintaining strength and corrosion resistance, contributing to better fuel efficiency and performance on long haul flights.

Superalloy represents the fastest-growing material type, supported by its exceptional mechanical strength, corrosion resistance, and ability to maintain stability at extremely high temperatures. These properties make them indispensable in aerospace, power generation, and industrial gas turbine applications, where components are exposed to intense thermal and mechanical stress. Advanced superalloys, including nickel-, cobalt-, and iron-based variants, enable engines and turbines to operate more efficiently while extending service life. For example, manufacturers such as Precision Castparts Corp. are developing superalloy grades targeting engine hot sections, enabling highly durable delivery, and showing promising results in thermal-resistance studies for advanced propulsion.

Superalloy Material Insights

Inconel 718 is expected to dominate the superalloy segment, contributing nearly 55% of superalloy revenue in 2026, fueled by outstanding high-temperature strength, corrosion resistance, and fatigue performance. This nickel-chromium-based superalloy is widely used in aerospace, gas turbines, and industrial engines, where components must withstand extreme heat and mechanical stress. Its ability to maintain structural integrity under demanding conditions makes it ideal for critical parts such as turbine blades, rocket engines, and fasteners. For example, large engine manufacturers routinely use Inconel 718 fasteners in turbine sections while also participating in advanced blend trials, ensuring components receive specialized, heat-resistant solutions with high standards.

A286 is the fastest-growing superalloy, driven by an exceptional combination of high-temperature strength, oxidation resistance, and corrosion protection. This iron-nickel-chromium alloy is particularly suited for applications in aerospace, automotive, and industrial sectors, where components such as fasteners, valves, and turbine parts are exposed to extreme heat and stress. Its ability to retain mechanical properties at elevated temperatures, along with good fabricability and weldability, makes it highly versatile. Aerospace suppliers produce Incoloy A-286 (UNS S66286) fasteners, which are iron-nickel-chromium superalloy bolts, nuts, and screws designed to withstand extreme heat and mechanical stress in jet engines and gas turbines, critical applications in aircraft propulsion systems.

Regional Insights

North America Aerospace Fasteners Market Trends

North America is projected to dominate, accounting for nearly 42% revenue in 2026, propelled by the region’s dominant OEM production (Boeing, Lockheed Martin), strong defense procurement, and high MRO volumes. Production systems in the U.S. and Canada provide extensive support for aerospace fasteners programs, ensuring wide accessibility across titanium, superalloy, and airframe populations. Increasing demand for high-strength, convenient, and easy-to-install forms is further accelerating adoption, as these formats improve assembly efficiency and reduce barriers associated with legacy designs.

Innovation in aerospace fastener technology, including stable superalloy, improved coating delivery, and targeted lightweight enhancement, is attracting significant investment from both public and private sectors. Government initiatives and DoD/FAA campaigns continue to promote use against weight risks, fatigue concerns, and emerging sustainable aviation threats, creating sustained market demand. The growing focus on engine grades and specialty uses, particularly for airframe and other applications, is expanding the target applications for aerospace fasteners.

Europe Aerospace Fasteners Market Trends

Europe is supported by increasing awareness of lightweighting benefits, strong regulatory systems, and government-led aerospace sustainability programs. Countries such as France, Germany, the U.K., and Spain have well-established OEM frameworks (Airbus, Rolls-Royce) that support routine aerospace fastener use and encourage adoption of innovative fastening methods, including titanium and superalloy solutions. These high-performance formulations are particularly appealing for airframe populations, regulation-conscious OEMs, and engine users, improving efficiency and coverage rates.

Technological advancements in aerospace fasteners development, such as enhanced coatings, application-targeted delivery, and improved superalloy grades, are further boosting market potential. European authorities are increasingly supporting research and trials for fasteners against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, low-weight options is aligned with the region’s focus on preventive CO2 reduction and sustainable aviation fuel compatibility. Public awareness campaigns and promotion drives are expanding reach in both civil and defense sectors, while suppliers are investing in manufacturing and novel variants to increase efficacy.

Asia Pacific Aerospace Fasteners Market Trends

Asia Pacific is likely to be the fastest-growing market for aerospace fasteners, driven by rising aircraft production awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting fastener campaigns to address fleet growth and emerging domestic manufacturing needs. Aerospace fasteners are particularly attractive in these regions due to their cost-effective administration, ease of integration, and suitability for large-scale airframe and engine drives in both commercial and defense populations.

Technological advancements are supporting the development of stable, effective, and easy-to-install aerospace fasteners, which can withstand challenging certification conditions and minimize weight dependence. These innovations are critical for reaching domestic OEMs and improving overall aircraft coverage. Growing demand for titanium, superalloy, and airframe applications is contributing to market expansion. Public-private partnerships, increased aerospace expenditure, and rising investment in fastener research and production capacity are further accelerating growth. The convenience of fastener delivery, combined with improved strength and reduced risk of failure, positions it as a preferred choice.

Competitive Landscape

The global aerospace fasteners market features competition between established tier-1 suppliers and emerging precision forging specialists. In North America and Europe, Howmet Aerospace and Precision Castparts Corp. lead through strong R&D, distribution networks, and OEM ties, bolstered by innovative titanium and superalloy programs. In Asia Pacific, domestic players advance with cost-competitive solutions, enhancing accessibility. Superalloy delivery boosts thermal performance, cuts fatigue risks, and enables mass integrations across aircraft. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Coated formulations solve corrosion issues, aiding penetration in legacy fleet MRO.

Key Industry Developments

- In January 2026, NAFCO (TWSE: 3004) held a groundbreaking ceremony for Phase II of its Malaysia M2 Plant, hosted by Chairman Francis Tsai and President Alvin Lin. Government officials, industry partners, and key stakeholders attended. The expansion strengthened aerospace fastener production capacity and reinforced NAFCO’s global supply chain, supporting future international growth.

- In February 2025, Airbus awarded a multi-year global contract to TriMas Aerospace’s Monogram Aerospace Fasteners™, Allfast Fastening Systems®, and Mac Fasteners™ brands. The contract expanded scope across all fastener business units and strengthened TriMas Aerospace’s position within Airbus’s global supply chain, underscoring its growing influence in the aerospace fasteners market.

Companies Covered in Aerospace Fasteners Market

- Howmet Aerospace

- Precision Castparts Corp. (Berkshire Hathaway Inc.)

- LISI AEROSPACE

- TriMas Aerospace

- Stanley Black & Decker, Inc.

- National Aerospace Fasteners Corporation

Frequently Asked Questions

The global aerospace fasteners market is projected to reach US$7.6 billion in 2026.

Rising global air travel, especially in emerging markets, is driving airlines to expand and modernize their fleets. To lower fuel costs, improve efficiency, and comply with stricter environmental regulations, airlines are placing large orders for next-generation aircraft, which directly drives higher aircraft production and associated component demand across the aerospace supply chain.

The aerospace fasteners market is poised to witness a CAGR of 8.0% from 2026 to 2033.

The growing demand for high-performance engines, gas turbines, and structural components in the aerospace and defense sectors presents a significant opportunity for superalloys such as Inconel 718 and A286.

Howmet Aerospace, Precision Castparts Corp., LISI AEROSPACE, TriMas Aerospace, and Stanley Black & Decker, Inc. are the key players.