- Advanced Materials

- Aerospace Sealants Market

Aerospace Sealants Market Size, Share, and Growth Forecast, 2026 - 2033

Aerospace Sealants Market by Product Type (Adhesives, and Sealants), by Resin Type (Epoxy Silicone Polyurethane Others), By Technology (Reactive Sealants, Solvent-based, Water-based and Others), By User Type (OEM and MRO), by End-user (Commercial, Military, and General Aviation), and Regional Analysis for 2026 - 2033

Aerospace Sealants Market Size and Trends Analysis

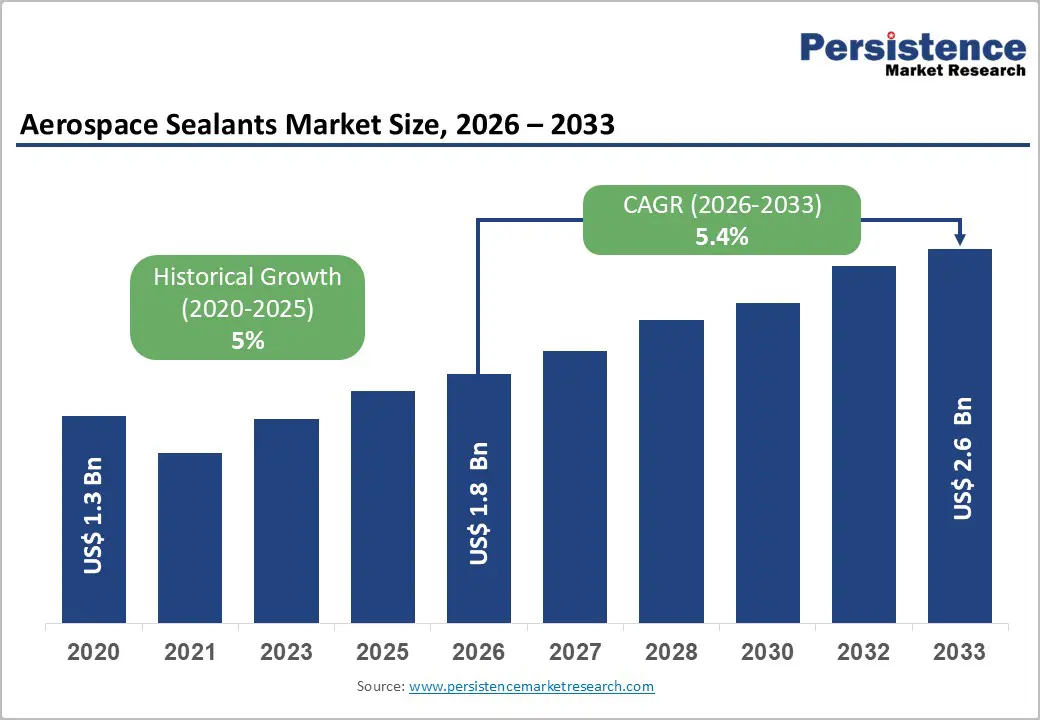

The global aerospace sealants market size was valued at US$ 1.8 billion in 2026 and is projected to reach US$ 2.6 billion by 2033, growing at a CAGR of 5.4% between 2026 and 2033. Over 2020–2026, the market expanded from US$ 1.3 billion, reflecting a historical CAGR of about 5%, broadly aligned with independent industry analyses indicating mid-single-digit growth for aerospace sealants and adjacent aircraft seals. Medium-term expansion is underpinned by rising commercial aircraft production, fleet renewal, and a steadily growing MRO spend base.

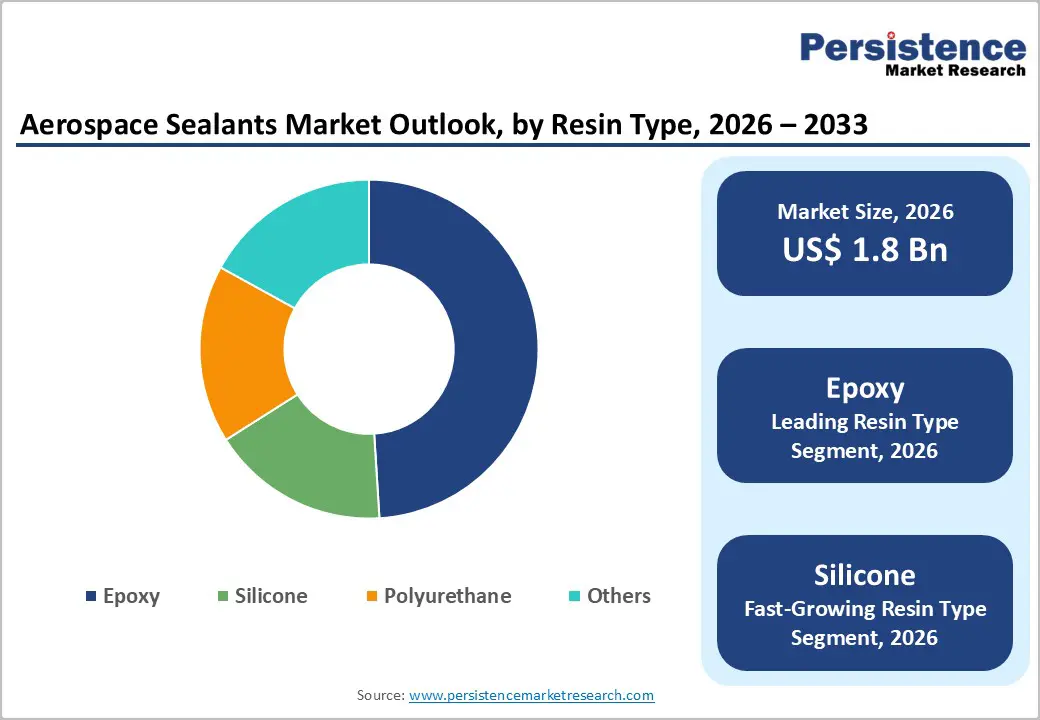

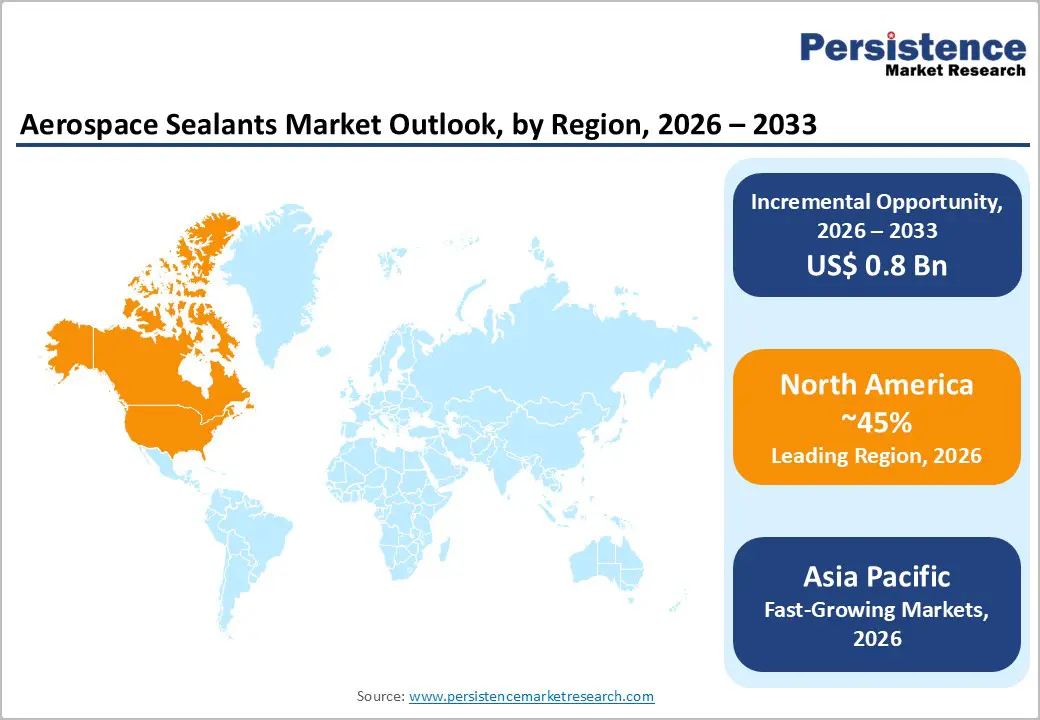

At the same time, stricter VOC, REACH and aviation safety regulations are accelerating product substitution toward higher-value, compliant chemistries, reinforcing value growth beyond pure volume gains. Within this context, adhesives account for roughly 59% of 2026 revenues, epoxy resins for over 52%, reactive technologies for above 40%, OEMs for nearly 62%, commercial aviation for over 63%, and North America for more than 40% of global turnover, while Asia Pacific is the fastest-growing regional market.

Key Industry-Highlights:

- Rising Global Air Traffic: Global passenger traffic is projected to grow 4.9% in 2026, supporting airline fleet expansion and aircraft production, thereby increasing demand for aerospace sealants used in aircraft assembly and structural applications.

- Expanding Aircraft Production Pipeline: Boeing forecasts nearly 44,000 new aircraft deliveries between 2024 and 2043, creating long-term demand for sealants used in fuel tanks, fuselage joints, doors, and cabin structures.

- Composites and Lightweight Materials Adoption: Increasing use of composite materials and advanced alloys in aircraft structures is driving demand for specialized sealants compatible with lightweight components and high-performance bonding systems.

- Growth in Aircraft Maintenance and MRO: The global aviation MRO market is projected to exceed USD 110 billion by 2030, boosting recurring demand for sealants used in aircraft repair, structural sealing, and corrosion protection.

- Adhesives Dominate Product Landscape: Aerospace adhesives account for over 59% of bonding and sealing revenue in 2026, reflecting their critical role in structural bonding, composite assemblies, and aircraft interior applications.

- Epoxy Resin Leads Material Segment: Epoxy-based sealants capture over 52% of market revenue in 2026, driven by strong adhesion, thermal stability, and compatibility with composite aircraft structures.

- Commercial Aviation Drives Market Demand: Commercial aircraft account for over 63% of aerospace sealant consumption, driven by rising passenger traffic, airline fleet expansion, and increasing aircraft deliveries worldwide.

- Asia Pacific Emerges as Fastest-Growing Market: Rapid aviation growth in China, India, and Southeast Asia, along with increasing aircraft orders and expanding MRO capacity, is accelerating aerospace sealant demand in the region.

| Key Insights | Details |

|---|---|

|

Aerospace Sealants Market Size (2026E) |

US$ 335.4 Mn |

|

Market Value Forecast (2033F) |

US$ 616.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.9% |

Market Dynamics

Drivers - Rising global air traffic and fleet expansion

From the perspective of aerospace sealant manufacturers, the long-term expansion of global aviation continues to create a strong and predictable demand environment. For 2026, the International Air Transport Association (IATA) forecasts 4.9% year-on-year growth in global passenger traffic (measured in RPK), with the Asia Pacific region leading growth at around 7.3%. Although this growth represents a slight moderation compared with 2025, the slowdown is mainly due to supply-side constraints such as limited aircraft availability and labor shortages rather than weak demand. In fact, airlines continue to operate with record load factors of approximately 83.8%, which supports profitability and encourages continued fleet expansion and replacement programs. Strong travel demand and stable ticket yields are also expected to help the global airline industry surpass USD 1 trillion in revenue for the first time in 2025, further strengthening airlines' financial capacity to invest in new aircraft.

This sustained aviation growth directly translates into long-term opportunities for manufacturers of aerospace sealants and adhesives, as these materials are essential for aircraft assembly, structural integrity, and fuel system protection. According to IATA’s long-term outlook, global passenger numbers are expected to grow at approximately 3.8–4.2% annually through the early 2040s, adding over 4 billion additional passenger journeys between 2023 and 2043.

Supporting this trend, Boeing’s 2024 Commercial Market Outlook projects demand for nearly 44,000 new commercial aircraft between 2024 and 2043, with the global aircraft fleet expected to almost double during this period. A significant portion of these deliveries will consist of single-aisle aircraft, which are produced in high volumes and require standardized sealing solutions across fuel tanks, fuselage joints, control surfaces, doors, and cabin structures. As original equipment manufacturers (OEMs) increase production rates and airlines accelerate fleet renewal to improve fuel efficiency and meet environmental targets, demand for qualified aerospace sealants grows almost in proportion to aircraft manufacturing volumes and line-fit installations. Consequently, sealant manufacturers are positioned to benefit from the expanding aircraft production pipeline, increasing maintenance cycles, and stricter safety and durability requirements in modern aviation platforms.

Lightweighting, composites, and advanced materials innovation

Aircraft OEMs and tier suppliers continue to increase composite content and adopt advanced alloys to meet fuel-burn and emissions targets, which demands compatible structural adhesives and sealants with tailored thermal, chemical, and fatigue performance. Market studies on aerospace adhesives and sealants point to a strong R&D focus on epoxy, polysulfide, and silicone systems that bond composite structures, enable thinner joints, and reduce fastener count while meeting FAA and EASA flammability and durability standards. New product introductions, such as Syensqo’s AeroPaste epoxy pastes and PPG’s latest epoxy syntactic adhesives, are designed for high-rate manufacturing and advanced air mobility platforms, thereby driving sealant demand in next-generation aircraft architectures.

Restraint - High cost of aerospace-grade and sustainable chemistries

Aerospace-qualified sealants and adhesives are formulated from high-purity resins, fillers and specialty additives, often incorporating non-chromate corrosion inhibitors and low-density technologies that increase unit cost. In parallel, aviation decarbonisation roadmaps such as Europe’s Destination 2050 highlight that sustainable aviation fuels (SAF) are currently 3–10 times more expensive than conventional kerosene, putting pressure on airlines’ operating economics and capital budgets. These cost headwinds intensify price sensitivity in both OEM and MRO channels, limiting the pace of adoption of the most advanced sealant grades and encouraging the continued use of legacy products where certifications allow.

Stringent environmental, VOC and chemical regulations

Regulations such as the EU’s REACH framework and U.S. EPA VOC limits for adhesives and sealants are progressively restricting hazardous substances and tightening emission caps. Aviation-specific rules, including regional aerospace coating and sealant VOC limits (for example, SCAQMD Rule 1124) and FAA flammability standards like FAR 25.853, require complex qualification, documentation and change-control processes for every product reformulation. Compliance raises R&D and certification costs, extends time-to-market for new sealants and can force early obsolescence of established chemistries, increasing supply risk for operators.

Opportunity - MRO digitalization and 3D-printed sealant solutions

Aviation MRO reports emphasize accelerating adoption of AI-enabled predictive maintenance, digital twins and advanced analytics to reduce downtime and optimize maintenance scheduling, with the aviation MRO market forecast to exceed US$ 110 billion by 2030. PPG’s introduction of 3D-printed sealant gaskets and pre-formed shapes, showcased around 2024, illustrates how additive manufacturing can standardize application, reduce waste and cut labor in both OEM and MRO settings. Integrating such products with digital work instructions and automated dispensing creates an opportunity for sealant vendors to move up the value chain from materials supply into process solutions and service-based offerings.

Category-wise Analysis

Product Type Insights

Adhesives account for above 59% of aerospace bonding and sealing revenues in 2026, reflecting their pervasive use in structural bonding, composite assemblies and interior applications where weight reduction and load transfer are critical. The dominance of adhesives is consistent with broader aerospace adhesives and sealants studies that highlight high penetration of epoxies and film adhesives across commercial and military platforms. Given the complexity of qualifications and long program lives, adhesive suppliers benefit from entrenched positions on major airframes, generating predictable OEM revenue streams.

Sealants, while representing the smaller revenue base in 2026, are the fastest-growing type segment with an estimated CAGR of about 6% between 2026 and 2033, outpacing the overall market. Their growth is driven by intensive use in fuel tanks, fuselage joints, canopies and access panels, and by rising aircraft utilization, which boosts replacement and repair demand in MRO environments. As operators prioritize corrosion control and leak prevention across aging fleets, demand for high-performance, rapid-cure polysulfide and silicone sealants is expected to expand disproportionately.

Resin Type Insights

Epoxy-based systems dominate the resin landscape, capturing above 52% of aerospace sealants and structural adhesive revenues in 2026, owing to their high bonding strength, temperature stability and compatibility with composite substrates. Epoxy chemistries are central to many structural paste adhesives and film adhesives qualified for use in interior structures, fuselage components and high-load joints, and are widely referenced in aerospace adhesive supplier benchmarks as core products. This entrenched role supports continued epoxy leadership in absolute revenue terms over the forecast horizon.

Silicone is the fastest-growing resin segment with an estimated CAGR of roughly 6.2% from 2026 to 2033, reflecting its superior flexibility, UV resistance and wide service-temperature window for applications such as windows, windshields and high-temperature zones. Industry reports on aircraft sealants note increasing adoption of silicone for cabin pressure seals and exterior joints where movement and environmental exposure are severe. As more aircraft architectures incorporate complex glazing and thermal management solutions, silicone-based sealants are expected to gain share, particularly in premium and high-performance niches.

Technology Insights

Reactive sealant technologies, including two-part polysulfide and epoxy systems, account for above 40% of aerospace sealant revenues in 2026, reflecting their central role in critical fuel tank, fuselage and structural sealing applications where in-situ curing and high mechanical performance are essential. These chemistries are widely referenced in OEM specifications and military standards, underpinning their continued dominance in both OEM line-fit and heavy-maintenance applications. Reactive products also enable tailored cure profiles and density reductions, supporting lightweighting and cycle-time optimization.

Solvent-based technologies are identified as the fastest-growing technology segment, with a CAGR of about 6.6%, largely due to reformulated, low-VOC products and niche applications where penetration into complex geometries and fast drying remain advantageous. However, tightening VOC regulations in North America and Europe, alongside EU REACH obligations, are pushing suppliers toward water-based and high-solids alternatives. Over the forecast period, solvent-based products that deliver clear compliance advantages or unique performance (for example, specific adhesion promoters or primers) are expected to sustain growth, while commodity solvent systems are expected to undergo a gradual phase-down.

User Type Insights

OEM customers represent the largest user segment, accounting for above 61.8% of aerospace sealants and adhesives revenues in 2026, reflecting significant material consumption in aircraft production and systems integration. This aligns with market reports that show North American and European OEM clusters anchoring global sealant demand, supported by robust order backlogs at major commercial airframers. OEM specifications lock in qualified products for decades, providing high visibility on baseline volumes across aircraft programs.

The MRO segment, while smaller in 2026, is the fastest-growing user type with an estimated CAGR of about 7% through 2033, outpacing OEM growth. Steady expansion of the global aircraft fleet, extended asset lives and increasing outsourcing of heavy checks are all driving MRO spend. Because sealants are regularly consumed during maintenance, repair and overhaul, suppliers that deepen channel reach, offer MRO-oriented packaging and provide technical support can capture an outsized share of incremental demand.

End-user Insights

Is commercial aviation the largest end-use, generating above 63% of aerospace sealants revenue in 2026, underpinned by high volumes of single-aisle and wide-body deliveries and intensive use of sealants across cabins, structures and fuel systems. Passenger air traffic recovery and subsequent growth, especially on intra-regional and low-cost carrier routes, reinforces this segment’s primacy, as each new aircraft embodies substantial line-fit sealant content. Commercial fleets also drive recurring aftermarket demand, given high utilization and cabin refurbishment cycles.

Is the military segment the fastest-growing end use, with an estimated CAGR of around 7.2%, supported by modernization of fighter, transport and rotorcraft fleets and sustained spending on mission-critical platforms. Defense applications typically require sealants with enhanced resistance to extreme temperatures, fuels and battlefield environments, driving higher material intensity per aircraft. Additionally, growth in unmanned systems and specialized mission aircraft further broadens the envelope of sealing requirements in the military domain

Regional Insights and Trends

North America Combines Scale, Defense Spend, Innovation Leadership

North America is the largest regional market, with market research placing its share at around 40–42% of global aerospace sealants revenues in the mid-2020s, in line with the segmentation above, which indicates a 2026 share above 40%. The U.S. anchors this position through its commercial OEMs, engine manufacturers, extensive MRO providers and one of the world’s largest defense budgets, all of which consume substantial volumes of qualified sealants. Growth over 2026–2033 is expected to be moderate but stable, supported by aircraft replacement cycles and continued fleet expansion.

Key performance drivers include strong order books for next-generation narrow-body and wide-body aircraft, high defense procurement of fighters, transports and rotorcraft, and a robust business aviation and general aviation base. The regulatory environment is characterized by stringent VOC and hazardous air pollutant controls enforced by the U.S. EPA and local air-quality districts, including aerospace-specific VOC rules (e.g., Rule 1124) that directly limit sealant formulations. These rules, combined with FAA safety and flammability standards, push suppliers toward low-VOC, non-chromate and high-solids technologies, reinforcing demand for value-added products. The competitive landscape is relatively consolidated, with PPG, 3M, Henkel, Dow and H.B. Fuller among the leading vendors, often integrating sealants with coatings, adhesives and engineered materials. Investment trends favor R&D in rapid-cure, lightweight and 3D-printed sealants, as seen in PPG’s innovations and the U.S. ecosystem’s strong patenting and qualification activity.

Asia Pacific Drives Incremental Demand and Cost Advantage

Asia Pacific is the fastest-growing regional market for aerospace sealants, with multiple aviation outlooks projecting passenger traffic growth of about 4.5% per year to 2040 and several national markets, including India, posting aviation CAGRs of roughly 5.8–7%. Regional market research indicates that Asia Pacific already accounts for around a quarter to one-third of global aerospace sealants and related revenues, with the share rising as fleets and infrastructure expand. China, Japan, India and the ASEAN bloc drive most of this growth through large commercial orders, airport construction and domestic MRO capacity building.

Manufacturing cost advantages, government-backed aerospace industrial policies and the expansion of local OEMs and Tier-2 suppliers are attracting sealant production and formulating capacity to the region. MRO investments are particularly strong, with Asia Pacific expected to emerge as a major hub for heavy maintenance by 2030 and beyond, reinforcing demand for sealant replacement and repair applications. Regulatory regimes are gradually converging with global VOC and chemical safety norms, though enforcement and timelines vary by country, creating opportunities for differentiated product and service offerings tailored to local needs. Competition is intensifying as global leaders such as PPG, 3M, Henkel and Solvay expand footprints alongside regional players and aviation conglomerates like AVIC, often via partnerships and technical service centers.

Aerospace Sealants Market Competitive Landscape

The aerospace sealants market is moderately concentrated, with the top five players (including PPG Industries, 3M, Henkel, Chemetall and Flamemaster) collectively controlling just over 50% of global revenues according to several industry analyses. Broader aerospace adhesives and sealants studies similarly show leading vendors such as PPG, Henkel and 3M holding significant combined shares, while a long tail of regional and niche suppliers addresses specific aircraft platforms, applications or geographies. Competitive positioning is shaped by depth of qualified product portfolios, global supply capability, technical service support and the ability to meet evolving environmental and performance standards.

Key Industry Developments:

- In August 2025, CDI Products launches a new Aerospace Sealing System Product Line and Digital Catalogue

- On December 16, 2024, 3M announced a structured transition of its aerospace sealant portfolio, including reformulated AC-series polysulfide sealants, with product qualification and initial shipments targeted for 2025 to support supply continuity and updated material chemistries.

- In May 2024, Syensqo Launches AeroPaste 1003 Epoxy Paste: Syensqo introduced AeroPaste 1003, an advanced epoxy-based structural paste adhesive designed to support high-rate aircraft production, particularly for advanced air mobility, commercial aviation, and defense platforms, improving assembly efficiency and processing flexibility.

- In February 2024, PPG Expands Aerospace Adhesives Portfolio: PPG launched PR-2940 and PR-2936 aerospace adhesives, with PR-2936 combining shim and sealant functionality for attaching aircraft outer skins to internal structures, enabling weight reduction, improved bonding performance, and enhanced manufacturing efficiency for OEM and MRO applications.

- In 2024, PPG Demonstrates 3D-Printed Sealant Technologies: PPG showcased 3D-printed sealant gaskets and pre-formed sealant components at the MRO Americas 2024 event, highlighting additive manufacturing approaches that reduce labor requirements, material waste, and variability in sealant application during aircraft manufacturing and maintenance.

Companies Covered in Aerospace Sealants Market

- 3M

- Henkel AG & Co. KGaA

- Huntsman Corporation

- Master Bond Inc.,

- Flamemaster Corporation

- Hernon Manufacturing, Inc

- Solvay

- PPG Industries Inc.

- Cytec Solvay Group

Frequently Asked Questions

The Aerospace Sealants market is estimated to be valued at US$ 1.8 Bn in 2026.

The key demand driver for the Aerospace Sealants Market is the growing global aircraft production and fleet expansion, driven by rising air passenger traffic and increasing demand for commercial, defense, and maintenance (MRO) activities requiring high-performance sealing solutions.

In 2026, the North America region will dominate the market with an exceeding 45% revenue share in the global Aerospace Sealants market.

Epoxy resin dominates the resin type landscape, commanding over 52% of total market revenue in 2026, driven by strong adhesion properties, high mechanical strength, chemical resistance, and its widespread use in aircraft structural bonding and composite assemblies.

Key players in the Aerospace Sealants Market include 3M, Henkel AG & Co. KGaA, Huntsman Corporation, Master Bond Inc., Flamemaster Corporation, Hernon Manufacturing, Inc., Solvay, PPG Industries, Inc., and Cytec Solvay Group.