- Advanced Materials

- Aerospace Composites Market

Aerospace Composites Market Size, Share, and Growth Forecast 2025 - 2032

Aerospace Composites Market by Fiber Type (Carbon Fiber Composites, Ceramic Fiber Composites, Glass Fiber Composites, Aramid Fiber Composites, Others), Matrix Type (Polymer Matrix, Ceramic Matrix, Metal Matrix), Application (Interior Components, Exterior Components, Engine & Propulsion Systems, Others), Manufacturing Process, Aircraft Type, by Regional Analysis, 2025 - 2032

Aerospace Composites Market Size and Trend Analysis

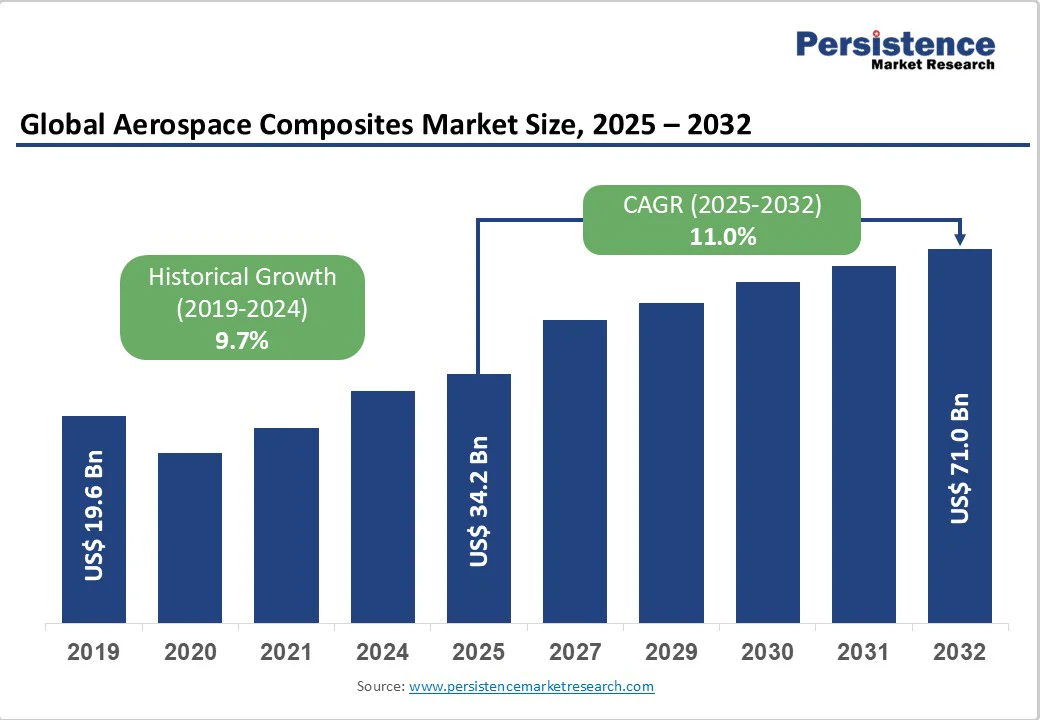

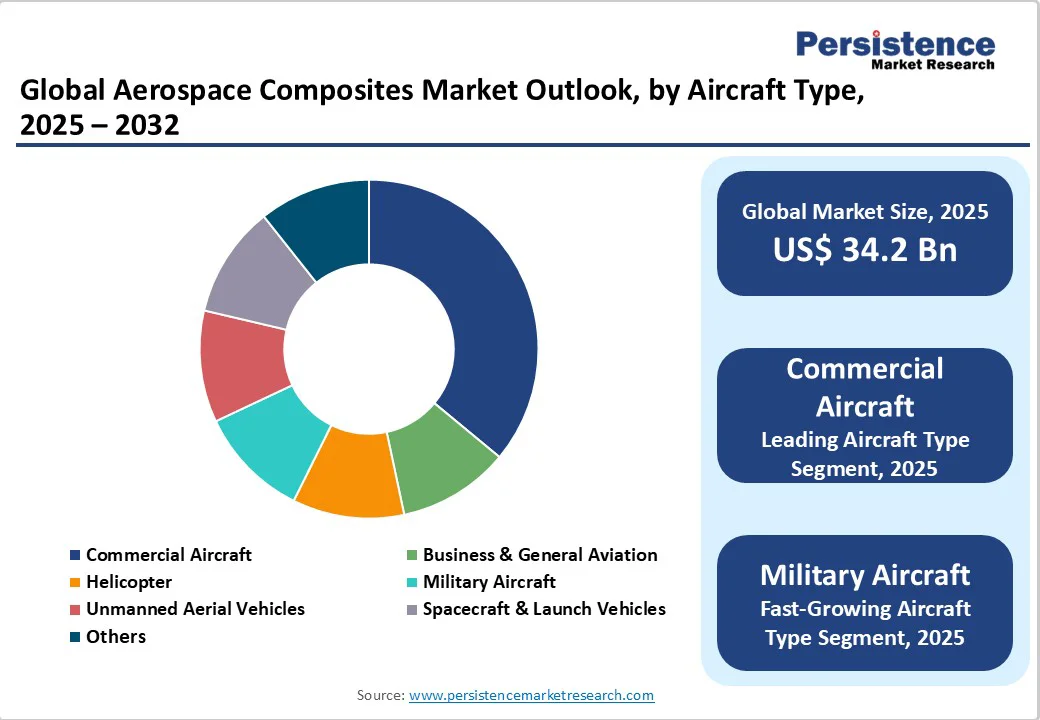

The global aerospace composites market size is valued at US$34.2 billion in 2025 and projected to reach US$71.0 billion by 2032, growing at a CAGR of 11.0% between 2025 and 2032.

The market’s expansion is further supported by rising aircraft production rates, stringent environmental regulations driving the adoption of fuel-efficient technologies, and ongoing advancements in composite manufacturing processes.

Key Market Highlights

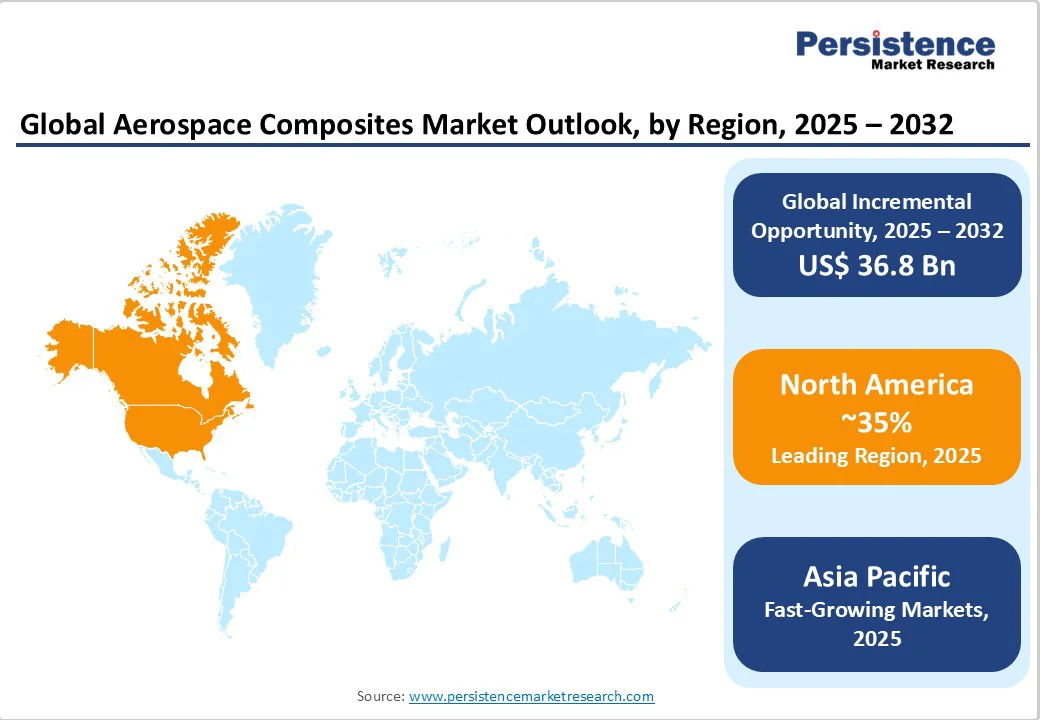

- Leading Region: North America leads the aerospace composites market with a 35% share, driven by established aerospace manufacturers and strong government support for advanced materials development.

- Emerging Region: Asia Pacific is the fastest-growing region, with China leading the CAGR, supported by expanding domestic aerospace programs and manufacturing capabilities.

- Dominant Segment: Carbon fiber composites dominate the market with over 52% share due to superior strength-to-weight ratios and proven performance in commercial aircraft applications.

- Fastest Growing Segment: Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) represent the fastest-growing manufacturing processes, enabling high-precision production for large-scale aerospace structures.

- Key Opportunity: The Space Exploration and Urban Air Mobility sectors offer significant growth opportunities for advanced Ceramic Matrix Composites and thermoplastic materials.

| Key Insights | Details |

|---|---|

| Aerospace Composites Market Size (2025E) | US$34.2 Bn |

| Market Value Forecast (2032F) | US$71.0 Bn |

| Projected Growth CAGR (2025 - 2032) | 11.0% |

| Historical Market Growth (2019-2024) | 9.7% |

Market Dynamics

Driver - Increasing Demand for Fuel-Efficient Aircraft and Weight Reduction

The aerospace industry faces mounting pressure to develop fuel-efficient aircraft that comply with stringent environmental regulations while reducing operational costs. The Boeing 787 Dreamliner and Airbus A350 demonstrate the transformative impact of composites, with over 50% of their structures made from composite materials, resulting in 20-25% weight reduction compared to traditional aluminum structures.

According to aviation industry analysis, eliminating 1 kilogram of material from an aircraft saves approximately 106 kilograms of jet fuel annually, directly reducing greenhouse gas emissions. The International Civil Aviation Organization (ICAO) regulations continue to drive manufacturers toward advanced materials that enable significant fuel savings and emission reductions, making composites essential for next-generation aircraft development.

Advancements in Automated Manufacturing Technologies

The evolution of Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) technologies has revolutionized composite manufacturing, enabling high-precision, high-speed production of complex aerospace structures. These automated processes have increased production rates from the traditional manual layup rate of 2.5 lbs/hour to significantly higher throughput while maintaining superior quality standards.

Spirit AeroSystems successfully manufactures the massive Boeing 787 nose and front fuselage sections using these automated technologies, demonstrating their capability for large-scale aerospace applications. The integration of thermoplastic composites with AFP/ATL processes offers additional advantages, including recyclability, rapid processing, and enhanced damage tolerance, particularly valuable for eVTOL aircraft, helicopters, and space launch vehicles applications.

Restraint - High Material and Processing Costs

Despite their performance advantages, aerospace composites face significant cost challenges that limit widespread adoption. Carbon fiber composites, which dominate the market with over 50% share, require expensive raw materials and complex manufacturing processes that significantly exceed the costs of traditional aluminum.

The machinery and equipment required for thermoplastic and other advanced composite processing are capital-intensive, resulting in high product costs that challenge commercial viability for large-scale applications.

Complex Certification and Regulatory Requirements

Aerospace composites face lengthy certification processes and stringent regulatory requirements, which delay product development and market entry. The FAA and EASA have established comprehensive guidelines for composite structures that require extensive testing and validation to ensure safety and reliability standards.

Bonded structure regulations particularly impact composite applications, with requirements for structural damage capability assessment and long-term durability validation creating significant development timelines. The complexity of composite failure modes compared to traditional materials necessitates sophisticated analysis and testing protocols, extending certification periods and increasing development costs for manufacturers seeking aerospace approvals.

Market Opportunities

Emerging Space Exploration and Commercial Space Sectors

The rapidly expanding space exploration sector presents unprecedented opportunities for aerospace composites applications. NASA has awarded significant contracts for advanced composite technologies, including the US$799,954 Phase II STTR contract to AnalySwift LLC for developing the Design Tool for Advanced Tailorable Composites (DATC).

Ceramic Matrix Composites (CMCs) are particularly valuable for space applications, offering exceptional temperature resistance above 2370°F (1300°C) while maintaining only one-third the density of superalloys. The growth of commercial space ventures and reusable launch vehicles creates substantial demand for lightweight, high-temperature-resistant materials that can withstand extreme space environments while enabling cost-effective space access.

Next-Generation Aircraft Programs and Urban Air Mobility

The development of next-generation aircraft programs, including electric aircraft, hybrid propulsion systems, and Urban Air Mobility (UAM) vehicles, creates significant growth opportunities for advanced composites. Airbus and MTU Aero Engines are actively developing zero-emission aircraft programs that require lightweight, high-performance materials to compensate for battery weight and achieve viable flight performance.

The Aircraft Engines Market expansion, coupled with the Aerospace Thermoplastic Composites Market growth, indicates strong demand for advanced materials that enable innovative aircraft designs. eVTOL aircraft and urban air mobility applications particularly benefit from composite materials’ design flexibility, allowing complex geometries and integrated structures that optimize aerodynamic performance while meeting stringent weight requirements.

Category-wise Insights

Fiber Type Analysis

Carbon Fiber Composites dominate the aerospace composites market with over 52% market share in 2025, driven by their exceptional strength-to-weight ratio and proven performance in critical aerospace applications. Boeing 787 and Airbus A350 extensively use Carbon Fiber Reinforced Plastic (CFRP), reducing the aircraft's weight by 20% compared to aluminum while delivering superior mechanical properties.

Toray Industries and Hexcel Corporation supply high-performance carbon fibers for aerospace applications, with Toray’s TORAYCA™ fibers being globally recognized for outstanding quality and consistency. The T300 fiber has become the de facto standard in aerospace applications, while advanced grades such as T1100G are being developed for next-generation aircraft that require enhanced performance.

Matrix Type Analysis

Polymer matrix composites account for a significant share of the aerospace composites market due to their versatility and established manufacturing processes. Thermoset composites currently dominate aerospace applications, offering excellent high-temperature performance and dimensional stability required for primary aircraft structures.

However, thermoplastic composites are gaining traction for their recyclability, rapid processing, and enhanced damage-tolerance properties. The aerospace thermoplastic composites market is particularly driven by applications in Boeing and Airbus next-generation narrow-body aircraft, where thermoplastics enable production rates of 80-100 aircraft per month through advanced welding and forming technologies.

Ceramic matrix composites represent an emerging, high-growth segment, particularly valuable for engine applications requiring extreme temperature resistance.

Application Analysis

Exterior components account for nearly 45% share in the aerospace composites market in 2025, encompassing wings, fuselage sections, and tail assemblies, where weight reduction directly impacts fuel efficiency. Primary structures, including wing boxes and fuselage panels, benefit significantly from composite materials’ directional strength properties and corrosion resistance.

Interior Components applications continue expanding as airlines prioritize passenger comfort while maintaining weight efficiency, with composites enabling complex designs and integrated functionality. The Aircraft Engines Market drives increasing adoption of composites in engine components, particularly Ceramic Matrix Composites for high-temperature applications in combustor liners and turbine components.

Manufacturing Process Analysis

Lay-up processes lead the aerospace composites manufacturing with approximately 40% market share, encompassing both manual and automated techniques that provide flexibility for complex geometries and prototype development. Automated Fiber Placement (AFP) and Automated Tape Laying (ATL) technologies are rapidly gaining market share due to their precision, repeatability, and production efficiency advantages.

These automated processes enable the manufacture of large-scale components, such as Boeing 787 fuselage sections, with consistent quality and reduced labor requirements. The transition from manual layup rates of 2.5 lbs/hour to automated processes represents a fundamental shift toward industrial-scale composite manufacturing capability.

Aircraft Type Analysis

Commercial Aircraft lead the aerospace composites market with 36% global demand, driven by airlines’ focus on fuel efficiency and operational cost reduction. The segment benefits from strong aircraft delivery forecasts, with Airbus projecting demand for 43,420 new passenger and freighter aircraft over 2025 - 2044.

Boeing Commercial Market Outlook similarly indicates robust demand for 43,600 deliveries through 2044, with 76% being single-aisle aircraft that increasingly incorporate composite materials. Military Aircraft applications drive demand for specialized composites with enhanced performance characteristics, while Unmanned Aerial Vehicles and Spacecraft & Launch Vehicles segments offer high-growth opportunities for advanced composite technologies.

Regional Insights

North America Aerospace Composites Market Trends

North America dominates the global aerospace composites market with 35% market share in 2025, anchored by the United States’ robust aerospace manufacturing ecosystem and established supply chains.

The region benefits from major aerospace manufacturers, including Boeing, Lockheed Martin, and Northrop Grumman, which drive substantial demand for advanced composite materials. U.S. government support through research funding and tax incentives fosters innovation in composite technologies, with defense spending contributing significantly to the development of advanced materials.

The region’s aerospace composites industry is supported by leading material suppliers including Hexcel Corporation, Owens Corning, and Toray Composite Materials America, which maintain significant manufacturing capabilities across multiple states.

Spirit AeroSystems demonstrates the region’s advanced manufacturing capabilities through the production of large-scale composite structures for commercial aircraft programs. The U.S. aerospace composites market is projected to expand at a 9% CAGR through 2032, supported by strong demand for commercial aircraft and military modernization programs.

Europe Aerospace Composites Market Trends

Europe represents a significant aerospace composites market with established manufacturing capabilities and strong research and development infrastructure. Germany, United Kingdom, France, and Spain lead regional aerospace activities, with Airbus serving as the primary driver of composite material demand through programs including A350 XWB and A320neo family aircraft.

The European Aviation Safety Agency (EASA) has established comprehensive regulations on composite materials that harmonize with FAA requirements, supporting global supply chain integration.

Toray operates carbon fiber manufacturing facilities in France and Hungary, while Hexcel maintains production capabilities across multiple European locations. The “Lightweight Innovations for Tomorrow” project in Germany demonstrates public-private collaboration in advancing composite materials and manufacturing methods.

European aerospace manufacturers benefit from stringent environmental regulations that drive adoption of fuel-efficient technologies, creating sustained demand for advanced composite materials in both commercial and military applications.

Asia Pacific Aerospace Composites Market Trends

Asia Pacific is the fastest-growing region in the aerospace composites market, driven by expanding aviation sectors and rising manufacturing capabilities in China, Japan, India, and ASEAN countries.

China’s aerospace composites market is expected to grow at a 9.4% CAGR through 2024, supported by government investments in both commercial and military aerospace programs. Commercial Aircraft Corporation of China (COMAC) development programs create substantial demand for advanced composite materials and local supply chain capabilities.

Japan maintains strong aerospace manufacturing capabilities with Toray Industries serving as a global leader in carbon fiber production, operating major facilities across the region.

India presents significant growth opportunities through increased aircraft manufacturing and maintenance activities, supported by government initiatives and private-sector investments in aerospace capabilities. The region benefits from cost-effective manufacturing advantages while developing sophisticated technical capabilities that support both domestic aerospace programs and global supply chain participation.

Competitive Landscape

The aerospace composites market demonstrates a moderately consolidated structure dominated by several key players with significant barriers to entry including extensive certification requirements, substantial capital investments, and established customer relationships.

Leading companies including Toray Industries, Hexcel Corporation, Owens Corning, Teijin Limited, and Mitsubishi Chemical Holdings Corporation, maintain strong market positions through integrated supply chains and advanced manufacturing capabilities.

The industry exhibits high switching costs due to lengthy qualification processes and performance validation requirements that create sustained competitive advantages for established suppliers. Technological differentiation remains crucial, with companies investing heavily in research and development to advance composite materials performance, manufacturing processes, and sustainability initiatives, including recycling technologies and carbon-neutral production methods.

Key Market Developments

- February 2025: Hexcel Corporation exhibited advanced aerospace composite materials at Aero India 2025, including HexTow® IM9 24K carbon fiber and HiTape® carbon reinforcement technologies, both engineered for automated manufacturing via ATL/AFP and out-of-autoclave processes.

- August 2024: ÉireComposites signed a contract with AVIC SAC Commercial Aircraft Co. Ltd. to manufacture internal composite components for the Airbus A220, strengthening its position in aerospace composite supply chains.

- June 2025: Composite Recycling announced a strategic collaboration with Owens Corning’s glass reinforcements business to co-develop circular composite waste recycling solutions using thermolysis technology, aiming to reintegrate reclaimed fibers into glass fiber production.

Companies Covered in Aerospace Composites Market

- Owens Corning

- Toray Industries, Inc.

- Teijin Limited

- Mitsubishi Chemical Holdings Corporation

- Hexcel Corporation

- SGL Group

- Spirit AeroSystems

- Solvay SA

- Royal Ten Cate N.V.

- Materion Corp.

- Absolute Composites

- Aernnova Aerospace

- Avior Integrated Products

- FDC Composites

- Lee Aerospace

- Composite Recycling

- ÉireComposites

- AnalySwift LLC

Frequently Asked Questions

The global aerospace composites market was valued at US$ 34.2 billion in 2025 and is projected to reach US$ 71.0 billion by 2032, growing at a CAGR of 11.0% during the forecast period.

The market is primarily driven by increasing demand for fuel-efficient aircraft, stringent environmental regulations, advancement in automated manufacturing technologies like AFP/ATL, and the need for weight reduction in aerospace applications to achieve 20-25% weight savings compared to traditional materials.

Carbon Fiber Composites dominate the market with over 52% market share in 2025, driven by their exceptional strength-to-weight ratio and proven performance in commercial aircraft like Boeing 787 and Airbus A350.

North America leads the aerospace composites market with 35% market share in 2025, supported by major aerospace manufacturers including Boeing, Lockheed Martin, and strong government support for advanced materials development.

Key opportunities include the emerging space exploration sector, Urban Air Mobility (UAM) applications, next-generation electric aircraft programs, and growing demand for Ceramic Matrix Composites in high-temperature engine applications.

Leading market players include Toray Industries, Inc., Hexcel Corporation, Owens Corning, Teijin Limited, Mitsubishi Chemical Holdings Corporation, Spirit AeroSystems, and Solvay, among others, who maintain strong positions through integrated supply chains and advanced manufacturing capabilities.