- Pharmaceuticals

- Advanced Cancer Pain Management Market

Advanced Cancer Pain Management Market Size, Share, and Growth Forecast, 2026 – 2033

Advanced Cancer Pain Management Market by Drug Class (Monoclonal Antibody, Cannabinoid, Aminoindane, Others), Route of Administration (Intravenous, Inhalational, Oral, Subcutaneous), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), and Regional Analysis for 2026-2033

Advanced Cancer Pain Management Market Share and Trends Analysis

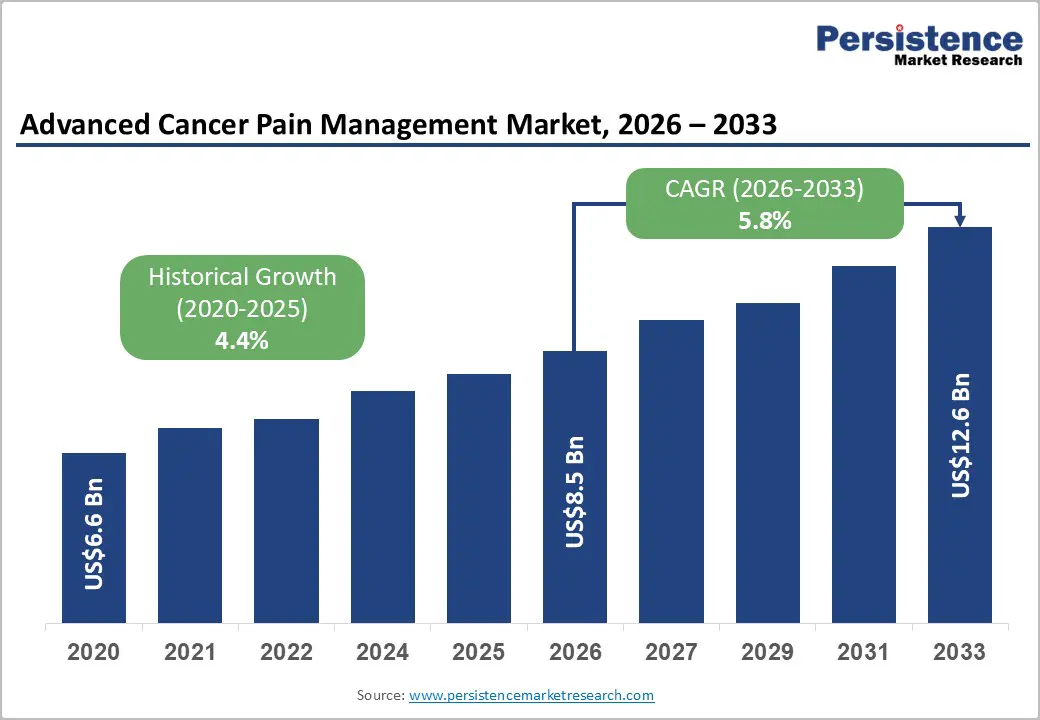

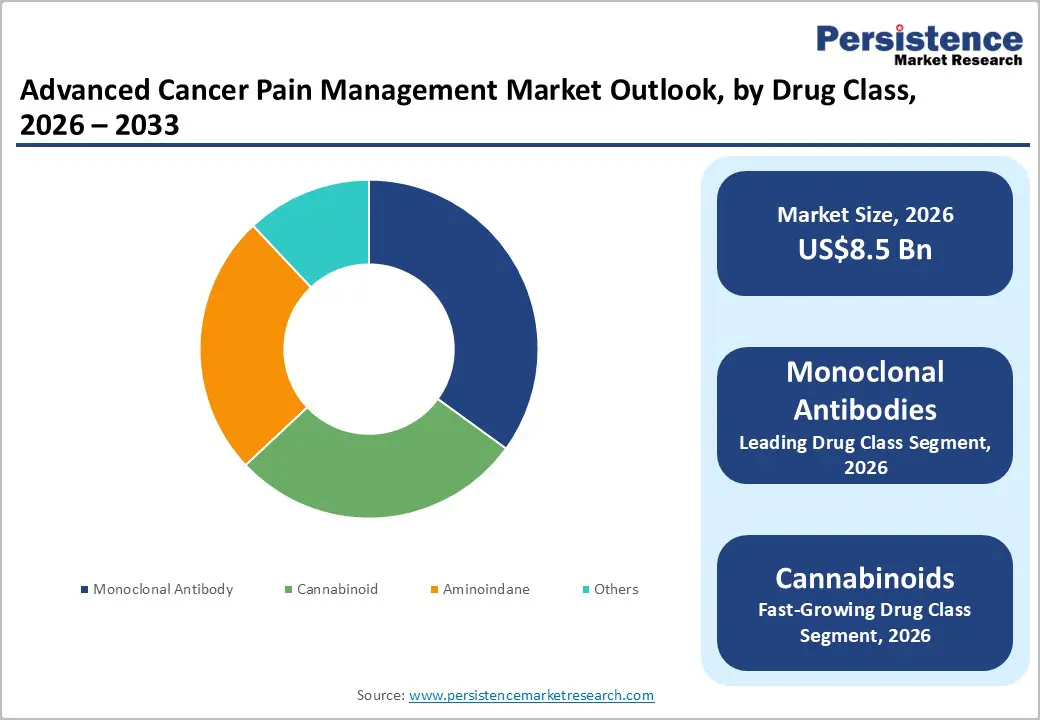

The global advanced cancer pain management market size is likely to be valued at US$ 8.5 billion in 2026, and is projected to reach US$ 12.6 billion by 2033, growing at a CAGR of 5.8% during the forecast period 2026−2033.

Rising incidence of advanced-stage cancer and an aging population drive demand for effective pain management solutions. Enhanced clinical awareness and adoption of multimodal therapies contribute to broader treatment acceptance across oncology care networks. Technological integration, including precision drug delivery and digital monitoring tools, enables targeted therapy and improved patient adherence. Expansion of healthcare infrastructure and oncology centers in urban and semi-urban regions facilitates treatment accessibility and capacity scaling.

Regulatory endorsement of novel analgesics and biologics fosters confidence among providers, supporting sustained market expansion. Investment in research and development for innovative therapeutics accelerates the availability of personalized pain management options, enhancing the quality of care.

Key Industry Highlights

- Leading Drug Class: Monoclonal antibodies are projected to lead with around 35% revenue share in 2026, supported by targeted action and high efficacy.

- Fastest-growing Drug Class: Cannabinoids are expected to grow the fastest between 2026 and 2033, supported by clinical acceptance and regulatory approvals.

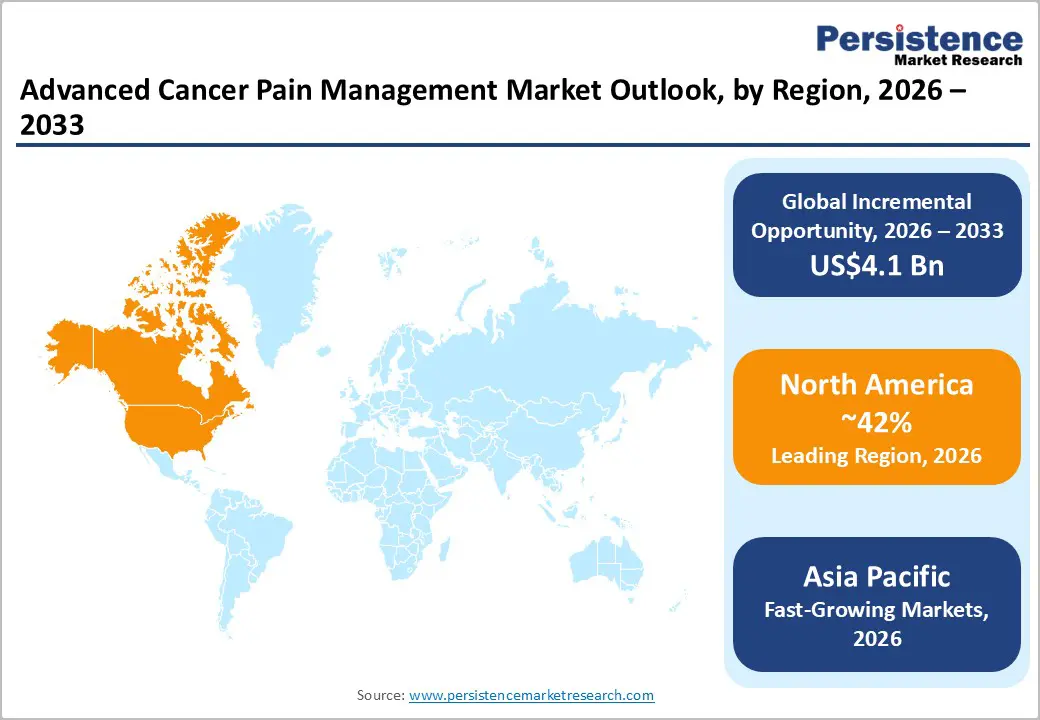

- Dominant Region: North America is projected to lead with roughly 42% market share in 2026, driven by high cancer incidence and strong healthcare infrastructure.

- Fastest-growing Regional Market: The Asia Pacific market is forecasted to grow the fastest between 2026 and 2033, fueled by rising cancer cases and healthcare expansion.

| Key Insights | Details |

|---|---|

|

Advanced Cancer Pain Management Market Size (2026E) |

US$ 8.5 Bn |

|

Market Value Forecast (2033F) |

US$ 12.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

5.8% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Prevalence of Advanced-Stage Cancer

The rise in patients with advanced-stage cancer intensifies demand for specialized pain management as more individuals progress to stages characterized by chronic, severe pain requiring ongoing clinical intervention. Tumor invasion, metastasis, and nerve involvement contribute to complex pain syndromes that standard analgesics often fail to control. This increased patient burden pressures oncology networks, palliative care units, and multidisciplinary teams to prioritize comprehensive pain strategies.

Health systems respond by directing resources toward advanced therapies, clinician training, and integrated care pathways to ensure functional maintenance and quality of life. Clinical focus shifts from solely treating cancer to managing long-term symptom control.

National data indicate that approximately 18.6 million people in the United States were alive after a cancer diagnosis as of January 1, 2025, reflecting growing survivorship and a larger population at risk for symptom burdens, including pain. Extended survival increases the likelihood of progression to advanced disease stages, driving the need for tailored pain management interventions. Aging populations and improved detection amplify this trend, prompting governments and healthcare authorities to support scalable pain management frameworks within oncology care to meet growing clinical demand.

Technological Advancements in Pain Management Solutions

Rapid innovation in pain management technology is transforming clinical workflows and enhancing patient outcomes for cancer-related pain. Data from the U.S. Centers for Disease Control and Prevention (CDC) indicate that in 2025, approximately 50 million adults in the United States experience chronic pain that limits daily activities, highlighting a substantial need for effective interventions. Advanced platforms such as artificial intelligence (AI)-driven analytics, digital remote monitoring, and decision support systems improve objective pain assessment. These tools enable clinicians to identify pain patterns, optimize therapy selection, and anticipate exacerbations, thereby increasing treatment precision and improving overall patient management.

Integration of device innovations and digital health solutions expands personalized care access. Neuromodulation implants, smart drug delivery systems, and mobile applications generate continuous patient data streams, supporting adherence and real-time monitoring. Interoperable platforms enable coordinated care across multiple providers and settings, reducing fragmentation. Enhanced data insights strengthen evidence-based protocols and operational efficiency, allowing timely adjustments to treatment plans.

Clinicians gain the ability to deliver patient-specific interventions tailored to pain severity and context. Longitudinal outcome tracking improves overall symptom control, supporting proactive management and better quality of life for diverse patient populations across care environments.

High Treatment Costs and Reimbursement Limitations

Restrictive reimbursement policies significantly influence patient access to advanced therapies and supportive care services by shifting a larger portion of costs onto individuals and providers. Expensive pharmacological treatments, extended-release formulations, and device-based interventions require substantial investment from healthcare providers, creating financial pressure when reimbursement rates lag behind acquisition and administration costs. Payers often impose prior authorizations or coverage limits, which can delay treatment initiation and reduce adoption of clinically effective options. Providers may respond by limiting the availability of high-cost therapies or prioritizing patients with better coverage, impacting overall care accessibility and treatment consistency across patient populations.

Payment structures for complex supportive care frequently undervalue resource-intensive interventions. Multidisciplinary approaches, including interventional techniques, counseling, and ongoing monitoring, require personnel, equipment, and administrative coordination, yet reimbursement often reflects only a portion of actual expenses. Public payers adhere to rate schedules and aggregate payment caps that fail to align with actual costs, thereby reducing providers' incentives to implement comprehensive protocols.

Administrative burdens, documentation requirements, and delayed payments further strain financial feasibility, forcing healthcare facilities to balance service quality with economic sustainability while managing competing demands for time and resources.

Regulatory and Compliance Challenges

Complex federal and state regulations create significant operational and clinical challenges for providers of cancer-related pain therapies. Prescribers must adhere to strict guidelines for controlled substances, including documentation of patient assessment, treatment rationale, and ongoing monitoring under Drug Enforcement Administration (DEA) and state Prescription Drug Monitoring Program (PDMP) requirements. Compliance demands increase administrative workload and expose clinicians to legal and financial risks, influencing treatment decisions. Oversight from multiple agencies necessitates constant updates to protocols and training, while risk of audits or penalties can deter adoption of advanced therapies.

Public health priorities drive regulatory focus on preventing opioid misuse, diversion, and overdose fatalities. Policies designed to protect communities impose limitations on prescribing practices, requiring extensive justification for initiation and continuation of potent analgesics. These controls, while intended to enhance safety, can delay the introduction of innovative treatment options and reduce provider willingness to use certain interventions. Clinicians must balance effective pain relief with strict adherence to legal requirements, affecting clinical workflows and patient access. The complexity of regulatory frameworks continues to shape adoption rates and decision-making in clinical pain management.

Integration of AI and Predictive Analytics for Personalized Care

Predictive analytics powered by artificial intelligence enables a shift from generalized care to precision health, tailoring treatments to individual patient characteristics, including genetics, clinical history, and lifestyle factors. This approach increases treatment effectiveness by aligning interventions with patient-specific needs and anticipated responses. According to the U.S. CDC, precision health models improve risk stratification and therapy selection, allowing clinicians to focus on interventions most likely to succeed for each patient. In clinical settings, this approach supports data-driven decision-making, enhances the relevance of treatment plans, and reduces exposure to ineffective therapies.

Advanced predictive models also facilitate proactive care and continuous monitoring, using data from electronic health records, wearable devices, and biomarkers to forecast patient-specific clinical events. Early detection of adverse responses allows for timely adjustments in therapy, optimizing outcomes while minimizing complications. Operational efficiency improves through better allocation of resources, targeted interventions, and streamlined clinical workflows.

Federal precision health initiatives emphasize the importance of integrating predictive analytics to enhance individualized treatment strategies. These efforts support the adoption of patient-centric care pathways, improve clinical decision-making accuracy, and foster measurable improvements in both short-term and long-term health outcomes.

Development of Non-Opioid and Targeted Pain Therapies

A transition to non-opioid and targeted pain solutions responds to clinical and societal challenges associated with traditional opioid therapy, including addiction, tolerance, and adverse side effects. The U.S. Food and Drug Administration (FDA) issued 2025 guidance to accelerate the development of safe, effective non-opioid analgesics, highlighting the need for alternatives to conventional pain medications. Federal directives, such as the CDC Clinical Practice Guideline for Prescribing Opioids for Pain, emphasize prioritizing non-opioid treatments where clinically appropriate, reinforcing alignment with updated care standards. This approach supports clinicians in delivering effective pain relief while reducing reliance on opioids and mitigating long-term patient risk.

Federal projections indicate substantial health and economic benefits from wider adoption of non-opioid therapies. Modeling in 2025 estimates that replacing 10% of opioid prescriptions with non-opioid alternatives could prevent hundreds of thousands of opioid use disorder cases and thousands of overdose deaths, generating significant cost savings for the healthcare system. Government agencies underscore the importance of targeted pain management interventions to reduce opioid-related harm while maintaining effective analgesia. Focused development of these therapies enables tailored treatment, supports multidisciplinary care strategies, and addresses unmet needs in chronic pain management, driving strategic investment and research opportunities.

Category-wise Analysis

Drug Class Insights

Monoclonal antibody is likely to be the leading segment with 35% of the advanced cancer pain management market revenue share in 2026, due to targeted mechanism of action, high clinical efficacy, and provider preference for precision therapy. Adoption is supported by evidence-based clinical protocols recommending biologics for moderate-to-severe cancer pain. Hospitals and specialty oncology centers prioritize therapies with predictable pharmacokinetics and favorable safety profiles. Manufacturing improvements and expanded distribution networks enhance accessibility, enabling consistent supply. Patient adherence benefits from reduced dosing frequency and controlled side-effect profiles.

Cannabinoid is expected to witness the fastest growth between 2026 and 2033, as increasing clinical acceptance and regulatory approvals facilitate adoption. Emerging evidence supports analgesic efficacy in refractory cancer pain, promoting clinician confidence. Development of standardized formulations and delivery mechanisms enhances patient adherence and treatment precision. Telemedicine platforms enable remote prescription and monitoring, particularly in regions with evolving legal frameworks. Market expansion is bolstered by rising awareness among patients and providers of cannabinoid-based adjunct therapies.

Route of Administration Insights

Intravenous route of administration is poised to lead with a forecasted over 40% market share in 2026, owing to immediate therapeutic effect, controlled dosing, and hospital-based administration preference. Hospitals and oncology centers favor intravenous administration for moderate-to-severe pain requiring rapid onset. Clinical acceptance is high due to predictable pharmacodynamics and compatibility with combination regimens. Institutional protocols and inpatient monitoring infrastructure reinforce adoption.

The route supports adherence and safety oversight, particularly for biologics and high-potency analgesics. Centralized procurement and integration with infusion centers enhance operational efficiency and scalability.

Oral administration is anticipated to be the fastest-growing segment between 2026 and 2033, driven by patient preference for convenience, outpatient compatibility, and long-term adherence. Technological developments in sustained-release and bioavailable formulations improve therapeutic outcomes. Telehealth and digital prescription systems facilitate access and monitoring, increasing adoption. Expanding retail and online pharmacy networks enhances reach and affordability.

Cultural acceptance and preference for non-invasive delivery further support growth. Innovations in oral formulations for cannabinoids and aminoindane derivatives provide additional growth levers, addressing unmet patient needs in home-based care settings.

Regional Insights

North America Advanced Cancer Pain Management Market Trends

North America is anticipated to lead with an estimated 42% of the advanced cancer pain management market share in 2026, supported by a combination of structural healthcare advantages and high unmet clinical demand. The United States drives the majority of this share due to approximately 1.9 million new cancer diagnoses annually, generating a persistent need for comprehensive pain solutions. Strong insurance reimbursement systems and integrated care models in the United States and Canada facilitate the adoption of advanced therapies, including targeted drug delivery and specialist-led palliative care.

High clinical trial activity and established research networks accelerate early adoption of innovative pain management modalities.

Key factors reinforcing dominance include concentrated investment in oncology research and well-developed commercialization networks. Multinational pharmaceutical and device companies maintain substantial operations in the United States and Canada, leveraging strong intellectual property protections and broad distribution channels. Elevated per capita healthcare expenditure enables uptake of premium therapies and supports specialized workforce training.

Proactive regulatory oversight combined with sustained R&D investment reduces entry barriers for advanced treatments. Growing geriatric populations with complex pain profiles create continuous clinical demand, reinforcing strategic focus on innovative, high-value pain management solutions.

Europe Advanced Cancer Pain Management Market Trends

Europe demonstrates steady adoption of advanced cancer pain management solutions, supported by national healthcare systems and structured palliative care programs. Government-backed reimbursement schemes and universal healthcare coverage facilitate integration of pharmacological and device-based therapies. Networks of specialized oncology centers enable the deployment of multimodal pain strategies, enhancing accessibility across inpatient and outpatient settings. Investment in clinical trials and hospital-pharmaceutical collaborations accelerates introduction of innovative treatments while ensuring regulatory compliance.

Focused research and development initiatives advance non-opioid and targeted therapies, improving patient outcomes and treatment precision, reinforcing the region’s capacity to implement sophisticated pain management solutions effectively.

Awareness among healthcare professionals and patients regarding quality-of-life outcomes drives demand for personalized pain management approaches. Countries such as Germany and France are expanding digital health platforms to support remote monitoring, pain assessment, and follow-up care. Streamlined regulatory pathways encourage the commercialization of novel analgesics and medical devices, enhancing therapy adoption. Aging populations with complex pain profiles in Italy and the United Kingdom maintain a persistent demand for comprehensive pain management programs.

Strategic collaborations, technological advancements, and supportive policy frameworks collectively strengthen market growth and sustainable implementation of advanced solutions.

Asia Pacific Advanced Cancer Pain Management Market Trends

Asia Pacific is forecasted to be the fastest-growing market for advanced cancer pain management between 2026 and 2033, stimulated by the rapid expansion of healthcare delivery systems and rising disease prevalence in nations including China and India. Increasing cancer cases in these countries drive demand for sophisticated pain management solutions. Investments in hospital infrastructure, specialized oncology and palliative care centers, and availability of advanced analgesics and device-based therapies accelerate adoption.

Government programs improving access to quality care support service expansion and technology uptake, enhancing treatment accessibility and overall market growth during the forecast period.

A key growth factor is the adoption of comprehensive and multimodal pain management strategies as clinical practice evolves. Educational initiatives for clinicians and rising patient awareness of quality-of-life outcomes strengthen clinical pathways. Expanding private and public healthcare infrastructure in India and modernization of hospital systems in China create opportunities for pharmaceutical and device innovators. Telemedicine and digital platforms extend care to underserved populations, while regulatory frameworks facilitate introduction of non-opioid and targeted therapies, addressing unmet needs and sustaining momentum in advanced pain management solutions.

Competitive Landscape

The global advanced cancer pain management market exhibits a moderately consolidated structure with a mix of global pharmaceutical leaders and specialized biotechnology firms. Key players, including Pfizer, AstraZeneca, GlaxoSmithKline, Jazz Pharmaceuticals, Tetra Bio-Pharma, and WEX Pharmaceuticals, collectively account for an estimated 40% market share, reflecting concentration in innovative therapy development. Smaller biotechnology companies contribute to fragmentation through niche therapies, specialized formulations, and novel delivery systems. Differentiation relies on clinical validation, therapeutic innovation, and digital health integration.

High research and development costs, stringent regulatory scrutiny, and complex clinical trial requirements act as barriers to entry, preserving dominance of established players while creating opportunities for strategic alliances and acquisitions. Collaboration with smaller biotechnology firms accelerates commercialization of non-opioid and targeted therapies. Investment in advanced delivery systems, personalized treatment approaches, and telemedicine-supported pain management strengthens competitive positioning and sustains growth across regional markets.

Key Industry Developments

- In January 2026, Sun Pharmaceutical Industries made UNLOXCYT, an FDA-approved anti-PD-L1 therapy for adults with metastatic or locally advanced cutaneous squamous cell carcinoma, commercially available for prescription in the United States, offering a new targeted treatment option for advanced skin cancer patients.

- In October 2025, Telix dosed the first patient in its Phase 1 SOLACE trial evaluating TLX090, a radiopharmaceutical designed to deliver targeted radiation for pain relief in metastatic bone cancer. The therapy aims to provide a systemic, non-opioid alternative with potentially long-lasting pain relief.

- In September 2025, Sylvester Comprehensive Cancer Center at University of Miami Health System launched one of the first multidisciplinary tumor boards in the United States focused solely on addressing cancer-related pain, bringing together specialists from palliative care, interventional radiology, oncology and surgery to create individualized pain management plans for patients.

Companies Covered in Advanced Cancer Pain Management Market

- Pfizer Inc.

- AstraZeneca

- GlaxoSmithKline plc

- Jazz Pharmaceuticals

- Tetra Bio-Pharma Inc.

- WEX Pharmaceuticals Inc.

- Nobelpharma Co., Ltd

- Sigma-Aldrich

- Recipharm

- Eurofins

Frequently Asked Questions

The global advanced cancer pain management market is projected to reach US$ 8.5 billion in 2026.

Rising cancer prevalence, demand for effective pain relief, and advancements in pharmacological and interventional therapies are driving the market.

The market is poised to witness a CAGR of 5.8% from 2026 to 2033.

Expansion of non‑opioid and targeted therapies, digital health integration, and growth in emerging healthcare markets present key opportunities.

Some of the key market players include Pfizer, AstraZeneca, GlaxoSmithKlin, Jazz Pharmaceuticals, Tetra Bio-Pharma, and WEX Pharmaceuticals.