- Advanced Materials

- Advanced Functional Materials Market

Advanced Functional Materials Market Size, Share, and Growth Forecast, 2025 - 2032

Advanced Functional Materials Market by Material Type (Ceramics, Composites, Conductive Polymers, Nanomaterials, Energy Materials, Others), End-use (Electrical and Electronics, Automotive, Healthcare, Aerospace and Defense, Energy and Power, Others), and Regional Analysis for 2025 - 2032

Advanced Functional Materials Market Size and Trend Analysis

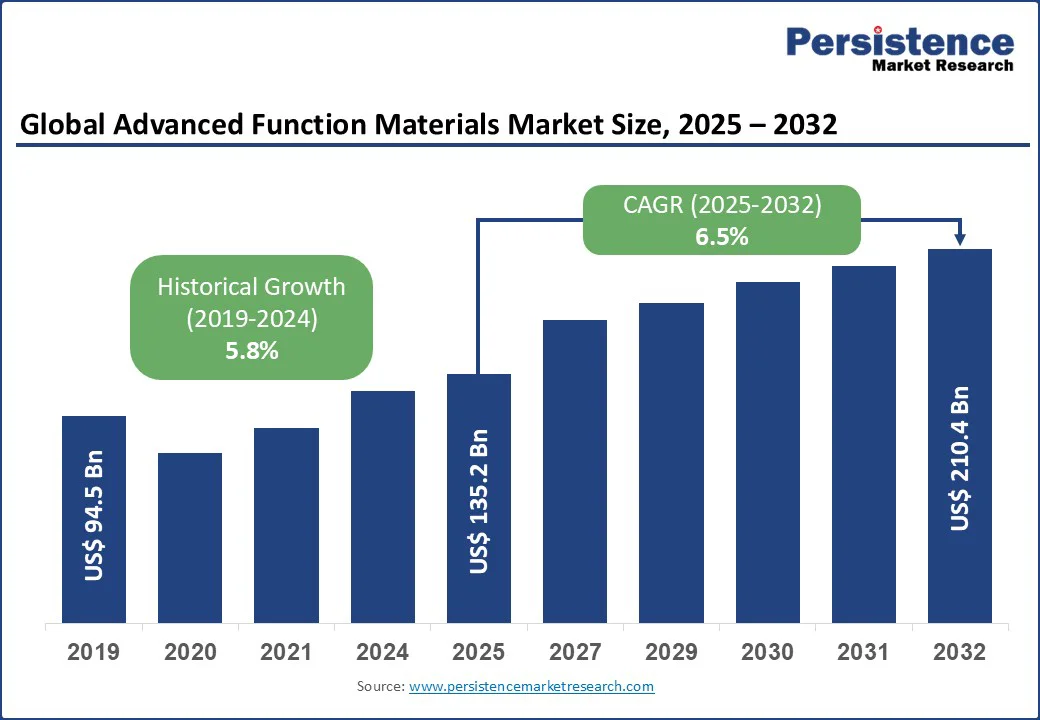

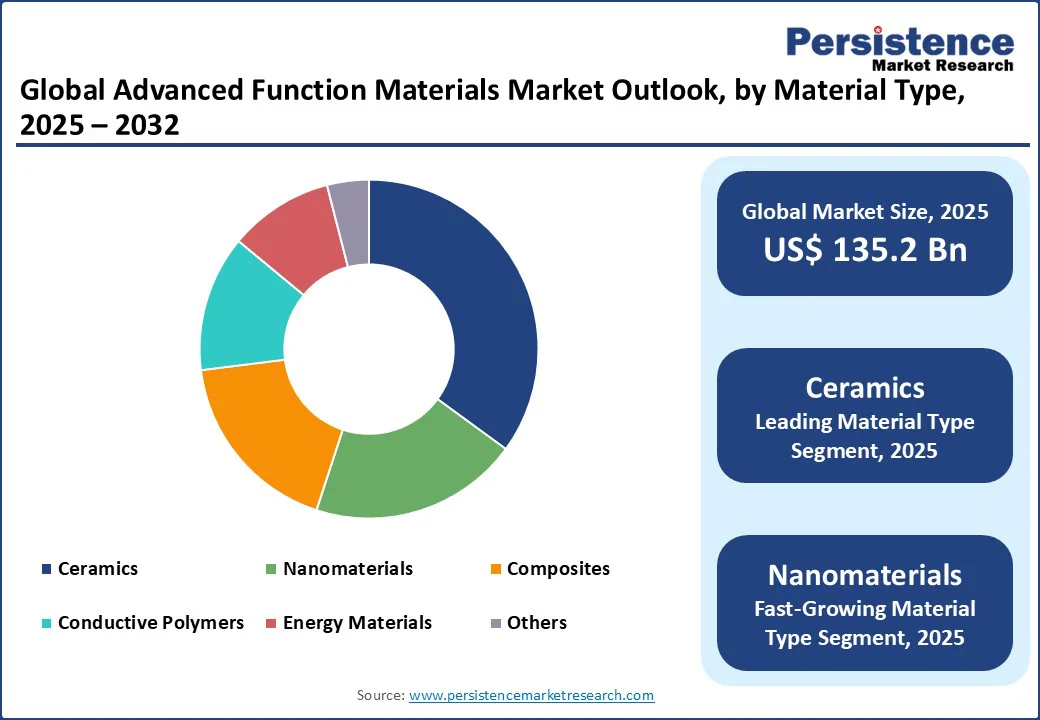

The global advanced functional materials market is projected to reach US$135.2 Bn in 2025 and US$210.4 Bn by 2032, growing at a CAGR of 6.5% from 2025 to 2032.

The advanced functional materials industry is experiencing robust growth, driven by increasing demand from industries such as electrical and electronics, automotive, and healthcare, where properties such as lightweight, durability, and conductivity are critical.

Advanced functional materials, including ceramics, composites, and nanomaterials, are essential for applications in energy storage, medical devices, and high-performance manufacturing. The rise in global technological advancements, coupled with investments in sustainable solutions, supports market expansion.

Key Industry Highlights:

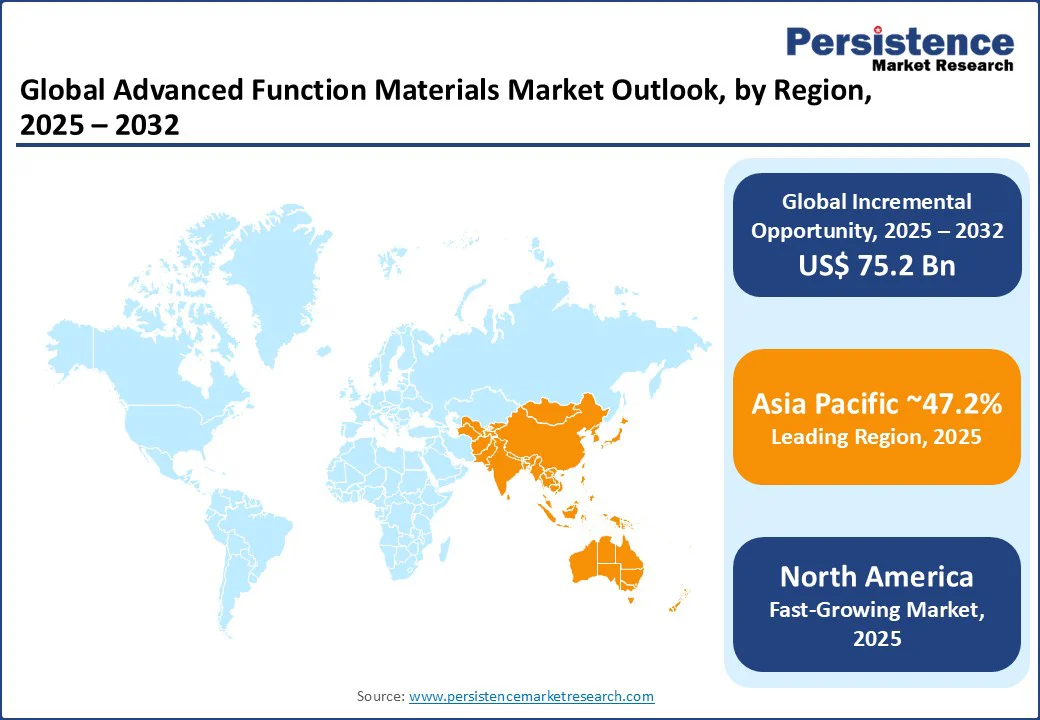

- Leading Region: Asia Pacific holds 47.2% market share in 2025, driven by rapid industrialization, technological advancements, and high production capacities in countries such as China and Japan.

- Fastest-growing Region: North America is the fastest-growing region, propelled by strong demand from the aerospace and defense sectors in the U.S., supported by advanced R&D infrastructure.

- Investment Plans: (January 2025) The U.S. Department of Commerce has finalized an award of up to US$325 million to Hemlock Semiconductor (HSC) to build a new polysilicon manufacturing facility in Hemlock, Michigan, under the CHIPS Incentives Program.

- Dominant Material Type: Nanomaterials account for nearly 38.6% of the market, driven by their unique properties and applications in electronics and healthcare.

- Leading End-use: Electrical and Electronics contributes over 42.1% of market revenue, driven by demand for conductive polymers and nanomaterials in consumer electronics.

|

Global Market Attribute |

Key Insights |

|

Advanced Function Materials Market Size (2025E) |

US$135.2 Bn |

|

Market Value Forecast (2032F) |

US$210.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.5% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.8% |

Market Dynamics

Driver: Surge in Demand from Electronics and Renewable Energy Sectors

The global advanced functional materials market is experiencing significant growth driven by rising demand from the electronics and renewable energy sectors. Advanced functional materials, such as conductive polymers and nanomaterials, are critical for manufacturing semiconductors, sensors, and energy storage devices.

According to the International Data Corporation (IDC), global semiconductor sales are expected to reach US$1 trillion by 2030, driving demand for high-performance materials.

In renewable energy, materials such as energy materials and composites are vital for solar panels, wind turbines, and battery technologies. The International Energy Agency (IEA) projects global renewable energy capacity to increase by 2.7 times by 2030, with solar and wind projects driving demand for lightweight, durable materials.

In the Asia-Pacific region, China’s focus on 5G technology and Japan’s advancements in battery manufacturing are fueling the adoption of advanced materials. Companies such as 3M Company and Kyocera Corporation reported increased sales of conductive materials in 2024, driven by growth in consumer electronics. Government initiatives, such as the U.S. CHIPS Act, further support semiconductor production, ensuring sustained demand for advanced functional materials through 2032.

Restraint: High Production Costs and Complex Manufacturing Processes

The advanced functional materials market faces challenges due to high production costs and complex manufacturing processes. Producing nanomaterials and conductive polymers requires advanced technologies and significant energy inputs, increasing operational costs. In 2023, raw material price fluctuations, particularly for rare earth elements used in ceramics and energy materials, impacted production costs. This volatility creates pricing pressures, especially for smaller manufacturers, limiting their market competitiveness.

Additionally, competition from traditional materials, such as metals and plastics, poses a challenge due to their lower costs and established supply chains. Regulatory complexities in some regions, particularly for nanomaterials due to environmental and health concerns, further hinder adoption. These factors collectively restrain market growth, particularly in cost-sensitive industries such as automotive and construction.

Opportunity: Growing Applications in Healthcare and Biomedical Sectors

The increasing focus on healthcare and biomedical applications presents significant opportunities for the advanced functional materials market. Materials such as ceramics and nanomaterials are critical for medical devices, drug delivery systems, and tissue engineering.

The World Health Organization estimates global healthcare expenditure reached US$9.8 trillion in 2021, accounting for 10.3% of global GDP, with rising investments in advanced medical technologies. Nanomaterials, for instance, are used in targeted drug delivery and diagnostic imaging, while ceramics are integral to dental and orthopedic implants.

Companies such as DuPont de Nemours and CeramTec are innovating with biocompatible materials for surgical applications, aligning with healthcare trends. Government initiatives, such as the EU’s Horizon Europe program, promote R&D in biomedical materials, creating opportunities for manufacturers to develop high-performance, eco-friendly materials.

The growing demand for personalized medicine and minimally invasive procedures further drives the adoption of advanced functional materials through 2032.

Category-wise Insights

By Material Type

- Ceramics accounted for 35.06% of the global advanced functional materials market in 2025, driven by their excellent thermal, electrical, and mechanical properties. They are widely used in semiconductor substrates, electric vehicle components, and biocompatible medical implants. Growing demand in the electronics and healthcare sectors is fueling market growth. Advances in ceramic matrix composites also boost applications in the aerospace and automotive industries. Asia-Pacific leads the market due to strong industrial and technological development.

- Nanomaterials are the fastest-growing material segment, due to their unique properties, such as a high strength-to-weight ratio and conductivity. Widely used in electronics, healthcare, and energy storage, nanomaterials are favored for their versatility in applications such as semiconductors and drug delivery systems. Companies such as Kuraray Co. Ltd. and Sumitomo Chemical lead with innovative nanomaterial portfolios, catering to demand in the Asia-Pacific and North America.

By End-use

- The electrical and electronics sector accounts for over 42.1% of market revenue in 2025, driven by demand for conductive polymers and nanomaterials in semiconductors, displays, and batteries. Major players such as 3M Company and Kyocera Corporation supply advanced materials for consumer electronics, particularly in the Asia-Pacific region, where growth in 5G and IoT fuels demand.

- The healthcare sector is the fastest-growing end-use, propelled by rising investments in medical devices and biocompatible materials. Advanced functional materials are used in implants, diagnostics, and drug delivery, with companies such as DuPont and CeramTec innovating for high-performance applications. Growth in North America and Europe, driven by healthcare infrastructure, supports this segment’s rapid expansion.

Regional Insights

Asia Pacific Advanced Functional Materials Market Trends

Asia Pacific dominates the advanced functional materials market, accounting for 47.2% of the market share, fueled by rapid industrialization, technological advancements, and high production capacities in countries such as China and Japan. China, a global leader in electronics manufacturing, contributes significantly to material demand, per the China Electronics Industry Association.

Japan’s focus on advanced battery technologies and 5G infrastructure drives the adoption of nanomaterials and conductive polymers. India’s growing automotive and healthcare sectors, supported by initiatives such as Make in India, boost demand for composites and ceramics.

The region’s robust supply chain and government-led investments, such as China’s $300 billion high-tech industry plan, ensure sustained market growth. Companies such as Showa Denko and Kyocera Corporation expand their presence, catering to the electronics and energy sectors through 2032.

North America Advanced Functional Materials Market Trends

North America is the fastest-growing region, driven by strong demand from aerospace, defense, and healthcare sectors in the U.S. and Canada, supported by advanced R&D infrastructure. The U.S. aerospace industry generated US$995 billion in 2024, and relies on composites and ceramics for lightweight, high-strength applications.

Canada’s healthcare sector drives demand for biocompatible materials, per Health Canada reports. Major players such as 3M Company and Hexcel Corporation dominate, with extensive distribution networks that cater to defense and electronics projects. Consumer preference for sustainable, high-performance materials strengthens North America’s market position through 2032.

Europe Advanced Functional Materials Market Trends

Europe is the second fastest-growing region, driven by stringent regulations, rising demand in the automotive and healthcare sectors, and infrastructure development in countries such as Germany and France. Germany’s healthcare sector, a key consumer of ceramics, benefits from players such as CeramTec. The EU’s Green Deal promotes renewable energy and sustainable materials, increasing demand for energy materials in solar and wind applications.

Competitive Landscape

The global advanced functional materials market is highly competitive and fragmented, with numerous domestic and international players ranging from large corporations to regional manufacturers. Leading companies such as 3M Company, DuPont, and Kyocera Corporation dominate through extensive product portfolios and global distribution networks.

Regional players such as Showa Denko focus on localized offerings in the Asia Pacific. Companies are investing in R&D and sustainable materials to enhance market share, driven by demand for high-performance materials in electronics and healthcare.

Key Industry Developments

- August 2025: Group14 Technologies closed a US$463 million Series D funding round, led by SK Inc., to expand the production of its silicon?carbon anode material (SCC55) for electric vehicle (EV) batteries and other applications. The round also saw participation from investors such as Porsche, Microsoft, and ATL.

- May 2025: Group14 Technologies and BASF introduced a breakthrough "drop-in" silicon-dominant anode solution for lithium-ion batteries, combining BASF's Licity 2698 X F binder and Group14's SCC55 silicon-carbon material. This partnership creates a commercially viable technology that significantly boosts battery performance, offering enhanced energy density, faster charging, and improved durability, with test cells exceeding 1,000 cycles at room temperature and over 500 cycles at 45°C.

Companies Covered in Advanced Functional Materials Market

- 3M Company

- Arkema S.A.

- CeramTec

- Covestro AG

- DuPont de Nemours Inc.

- Henkel AG & Co. KGaA

- Hexcel Corporation

- Kuraray Co. Ltd

- Kyocera Corporation

- Momentive Inc.

- Morgan Advanced Materials

- Showa Denko K.K.

- Sumitomo Chemical Co. Ltd.

- Others

Frequently Asked Questions

The advanced functional materials market is projected to reach US$ 135.2 Bn in 2025.

Growing demand from electronics, renewable energy, and healthcare sectors is the key market driver.

The advanced functional materials market is poised to witness a CAGR of 6.5% from 2025 to 2032.

The rising demand in the healthcare and biomedical sectors are key market opportunities.

3M Company, DuPont, Kyocera Corporation, and CeramTec are key market players.