- Construction & Engineering

- Advanced Glazing Systems Market

Advanced Glazing Systems Market Size, Share, and Growth Forecast, 2025 - 2032

Advanced Glazing Systems Market By Product Type (Insulating Glass Units (IGU), Smart Glass), Glazing Material (Low-Emissivity (Low-E) Glass, Tinted and Reflective Glass), Application, and Regional Analysis for 2025 - 2032

Advanced Glazing Systems Market Size and Trends Analysis

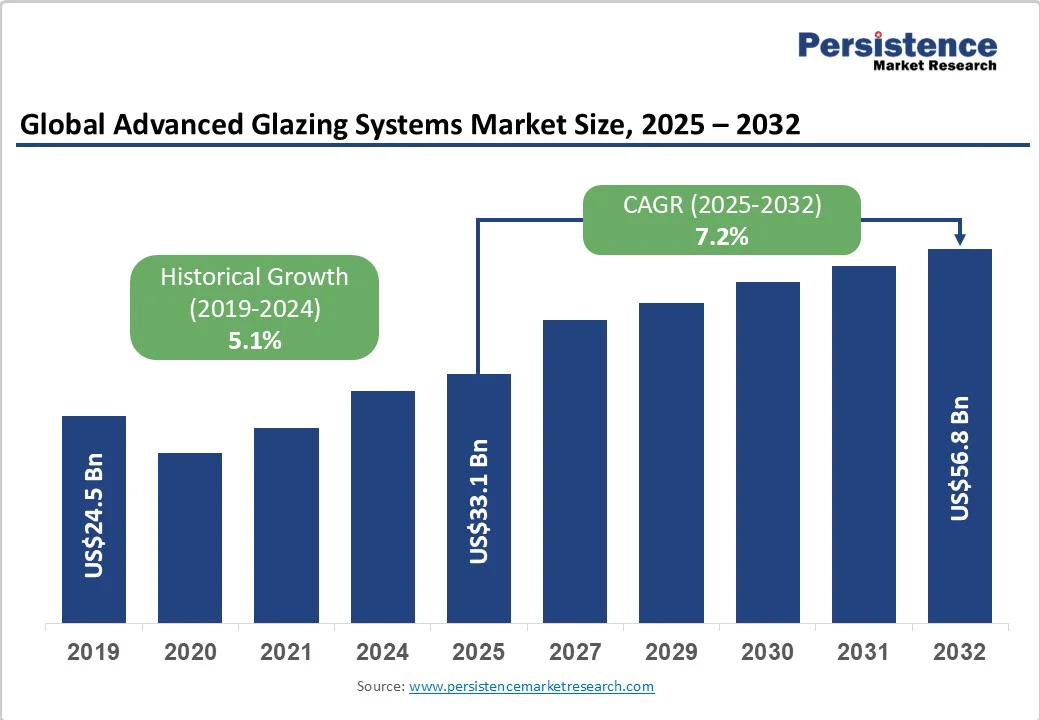

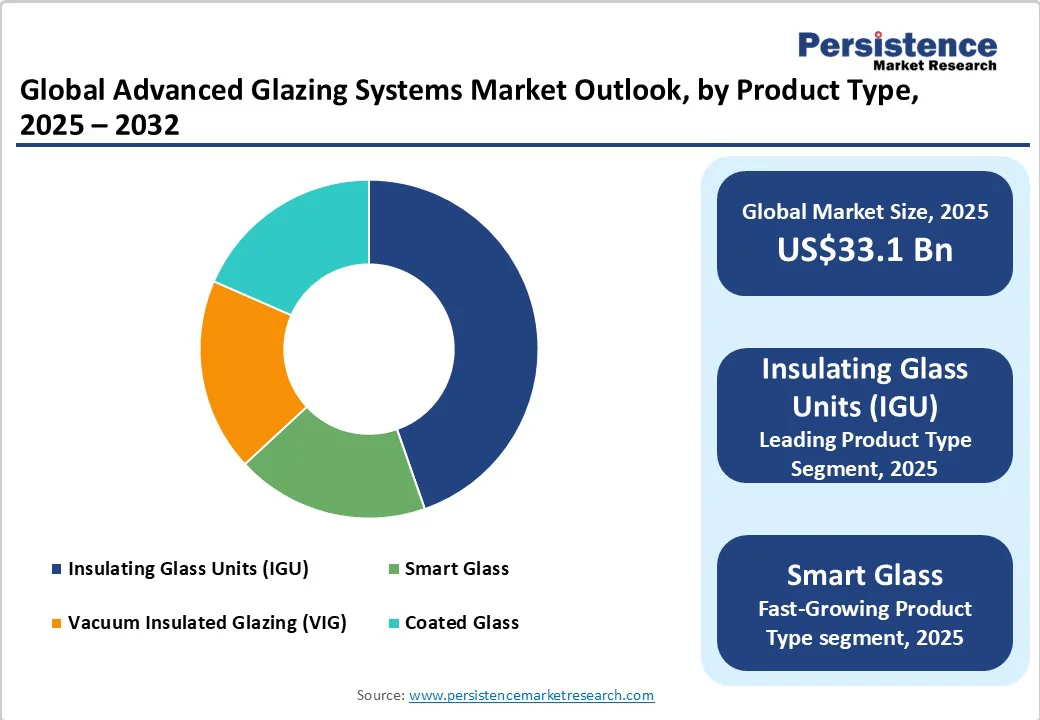

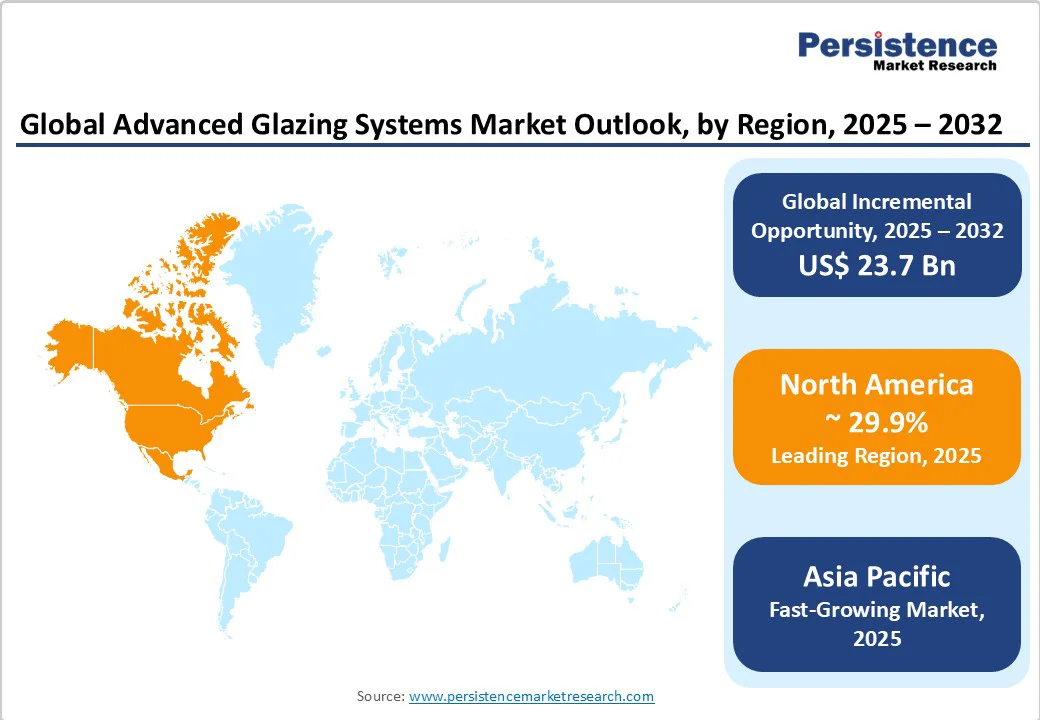

The global advanced glazing systems market size is likely to be valued at US$33.1 Billion in 2025 and is expected to reach US$56.8 Billion by 2032, growing at a CAGR of 7.2% during the forecast period from 2025 to 2032, driven by stricter energy efficiency regulations, the rising demand for smart and electrochromic glazing in modern architecture, and the rapid expansion of sustainable building practices worldwide.

Technological advancements in vacuum-insulated and dynamic glass, alongside major investments in green infrastructure, are further accelerating adoption across residential, commercial, and automotive applications.

Key Industry Highlights

- Leading Region: North America, accounting for approximately 29.9% of the global market share in 2025, driven by high adoption in commercial and institutional retrofits, smart building integration, and strong energy-efficiency mandates.

- Fastest-Growing Region: Asia Pacific projected to grow at a high CAGR between 2025 and 2032, fueled by rapid urbanization, infrastructure expansion, and growing demand for sustainable and high-performance building materials.

- Investment Plans: Significant capital allocation by key players, including View Inc.’s smart glass plant expansion in Mississippi (2024), AGC’s VIG facility in Belgium (2023), and AGC-Tata joint venture in Gujarat, India (2025), targeting both domestic and export markets.

- Dominant Product Type: Insulating Glass Units (IGUs) holding 46% of the market share in 2025, widely used in high-rise commercial buildings, airports, and healthcare facilities for thermal and acoustic benefits.

- Leading Material: Low-Emissivity (Low-E) Glass, accounting for over 39% of the market share in 2025, offering superior energy efficiency while maintaining natural light transmission, prevalent across commercial, residential, and automotive applications.

| Key Insights | Details |

|---|---|

|

Advanced Glazing Systems Market Size (2025E) |

US$33.1 Bn |

|

Market Value Forecast (2032F) |

US$56.8 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.1% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Regulatory Pressure for Energy Efficiency

Governments across the U.S., EU, and Asia are implementing stricter building codes to improve thermal performance and energy savings. Advanced glazing, featuring low-emissivity coatings and dynamic tinting, significantly reduces heat transfer and reliance on HVAC systems. The European Commission’s energy directive mandates nearly zero-energy buildings by 2030, driving the installation of high-performance glass. This regulatory momentum has resulted in an increased retrofit rate in commercial buildings and an expected incremental market contribution of over US$6 Billion by 2030 from policy-driven projects.

Technological Innovation and Integration

Emerging technologies such as electrochromic, suspended particle device (SPD), and vacuum-insulated glazing have transformed performance standards. Advancements have reduced switching times, improved transparency, and increased durability, enhancing building aesthetics and occupant comfort. Lower manufacturing costs and integration with smart building management systems are accelerating adoption, with the smart glazing segment expected to grow at a CAGR exceeding 10% through 2032, indicating a clear shift toward intelligent façade solutions.

Rising Commercial Retrofits and Urban Redevelopment

Urban infrastructure modernization is a key growth engine, particularly in North America and Europe, where older commercial buildings are being upgraded with advanced glazing systems. Retrofit programs that improve insulation and daylight control offer measurable returns through reduced energy bills and enhanced building value. In the U.S., federal energy-efficiency programs are expected to add approximately US$4–5 Billion in retrofit glazing demand by 2030, underscoring the sector’s investment attractiveness.

Barrier Analysis - High Initial Costs and Complex Installation

Despite long-term energy savings, the upfront cost of advanced glazing systems remains 25–40% higher than traditional glazing. Specialized installation processes and the need for integrated control systems increase project costs. This creates adoption barriers in cost-sensitive regions and mid-scale developments, limiting penetration in residential sectors.

Supply Chain Dependencies and Material Volatility

Dependence on high-performance coatings, specialized polymers, and conductive films has exposed manufacturers to raw-material shortages and price fluctuations. Limited production capacity of conductive oxides and interlayers has occasionally led to extended lead times, particularly in Asia. Such constraints can elevate production costs and affect project timelines.

Opportunity Analysis - Smart Glass in Commercial and Healthcare Infrastructure

The demand for electrochromic and SPD smart glass in offices, hospitals, and educational institutions is expanding rapidly. These products enhance visual comfort, support circadian lighting, and meet sustainability goals. The segment represents an opportunity exceeding US$8 Billion by 2032, supported by strong retrofitting activity in developed markets and urban expansion in emerging economies.

Vacuum Insulated Glazing (VIG) for Space-Constrained Retrofits

Vacuum-insulated glazing, offering up to five times higher thermal resistance in thinner profiles, is emerging as a preferred solution for heritage and high-rise retrofits. As cities move toward stricter insulation requirements, the VIG segment is projected to record a CAGR of over 9% from 2025 to 2032, positioning it as a core growth avenue for high-performance building envelopes.

Manufacturing Growth in Asia Pacific

Asia Pacific’s combination of cost-efficient production, urbanization, and export-oriented manufacturing is creating major opportunities for glass producers. Investments in new coating lines and electrochromic assembly plants in China and Japan will strengthen the region’s dominance, making it a hub for both domestic consumption and global exports by 2032.

Category-wise Analysis

Product Type Insights

Insulating Glass Units (IGU) dominate the market, holding nearly 46% of the total revenue share in 2025. These multi-pane glass systems consist of two or more glass panes separated by a sealed air or gas-filled space, effectively improving energy efficiency by minimizing heat transfer. They are now a standard in modern construction, meeting stringent green building certifications such as LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method). IGUs are extensively deployed in high-rise offices, airports, shopping complexes, and hospitals due to their superior thermal insulation, noise reduction, and condensation resistance. For instance, Guardian Glass provides advanced double- and triple-glazed IGUs integrated with low-emissivity (Low-E) coatings that can cut annual HVAC energy consumption by nearly 20–25% in commercial buildings.

The smart glass segment comprises electrochromic, suspended particle device (SPD), and thermochromic technologies. Its ability to dynamically adjust light transmission and solar heat gain in response to environmental conditions or electronic control makes it ideal for next-generation architectural designs. Commercial offices, airports, and healthcare facilities are key adopters, as smart glass enhances occupant comfort while cutting energy costs by up to 30%. Major companies such as View Inc., Gentex Corporation, and Saint-Gobain are leading innovation in this category. View’s electrochromic glass installed in Google’s Bay View Campus and Dallas–Fort Worth Airport Terminal C exemplifies the transition toward adaptive façades that integrate with IoT-enabled building management systems. SPD smart glass, developed by Research Frontiers Inc., is increasingly used in automotive panoramic roofs by brands like Mercedes-Benz and McLaren, enhancing passenger comfort and safety.

Glazing Material Insights

Low-E glass remains the most widely used glazing material, accounting for over 39% of the total market share in 2025. It features microscopically thin metallic coatings that minimize infrared and ultraviolet radiation without compromising visible light transmission. This balance of efficiency and aesthetics makes Low-E glass indispensable in both residential and commercial sectors. Prominent examples include Saint-Gobain’s COOL-LITE® XTREME and AGC’s Planibel Clearlite Low-E, which are used in energy-efficient skyscrapers and eco-certified housing projects. These products deliver up to 60% improvement in thermal performance compared with conventional glazing, aligning with zero-energy building mandates across the EU and North America. With more cities adopting carbon-neutral construction goals, the demand for Low-E glass is expected to remain resilient.

Vacuum Insulated Glazing (VIG) is emerging as one of the most advanced technologies in the glazing market. VIG panels consist of two glass sheets separated by a narrow vacuum gap, often less than 0.2 mm, achieving up to five times the thermal resistance of traditional double glazing at half the thickness. This makes VIG an attractive solution for space-constrained retrofits, heritage buildings, and high-performance windows in dense urban environments. Manufacturers such as Nippon Sheet Glass (NSG Group) and Schott AG have developed commercial-scale VIG solutions such as Pilkington Spacia and Schott’s VacuMax, which are now deployed in Japan, the U.K., and Germany. For example, Pilkington Spacia was installed in the Himeji Castle restoration project in Japan, where it provided enhanced insulation without altering the building’s historic appearance.

Regional Insights

North America Advanced Glazing Systems Market Trends-Smart Glazing Innovation Driven by Retrofit Demand

North America represents one of the most advanced and innovation-driven regions in the market, accounting for nearly 29.9% of the total market share in 2025. The United States remains the dominant country, propelled by a robust commercial real estate sector, stringent energy codes, and a well-developed manufacturing ecosystem. The U.S. Department of Energy (DOE) and Environmental Protection Agency (EPA) continue to enforce high-performance building standards such as ENERGY STAR and ASHRAE 90.1, which mandate the use of energy-efficient façade materials, including insulated and low-emissivity glazing. Retrofitting of aging building stock, particularly in major urban centers such as New York, Chicago, and San Francisco, is driving replacement demand.

Major corporations such as Guardian Glass, Corning Incorporated, and View Inc. have strengthened regional innovation capacity through localized R&D and production facilities. For example, View Inc. expanded its smart glass production plant in Olive Branch, Mississippi, in 2024, tripling its electrochromic glazing output to serve growing demand from corporate campuses and healthcare institutions. Guardian Glass, part of Koch Industries, partnered with Vitro Architectural Glass in 2025 to co-develop next-generation low-E coatings optimized for North American climates. The integration of glazing solutions with IoT-based building automation systems, notably through partnerships with companies such as Honeywell and Johnson Controls, is reshaping the regional market.

Europe Advanced Glazing Systems Market Trends-Policy-Led Transition to Low-Carbon Glazing Solutions

Europe commands a substantial portion of the market. The region’s growth is underpinned by the European Green Deal and the Energy Performance of Buildings Directive (EPBD), both of which enforce strict efficiency standards and mandate near-zero energy consumption in new buildings by 2030. Countries such as Germany, the U.K., France, and the Netherlands are spearheading the transition through large-scale renovation programs and adoption of vacuum-insulated and electrochromic glazing technologies.

Germany continues to lead in innovation and implementation, supported by strong domestic players such as Schott AG, Saint-Gobain Sekurit, and AGC Glass Europe. In 2024, Saint-Gobain launched its Glass for Future initiative, investing €120 Million (US$139.44 Million) to develop low-carbon glass manufacturing lines in France and Poland. Similarly, AGC Glass Europe inaugurated a VIG production facility in Belgium in late 2023 to meet growing demand from high-performance residential retrofits and commercial tower refurbishments.

The U.K. market, driven by the UK Net Zero Strategy, has seen increasing use of smart glazing in public infrastructure, including Crossrail stations and Heathrow Terminal expansions, to enhance energy savings and passenger comfort. In addition, the European Union’s focus on life cycle sustainability and recyclability is pushing manufacturers to adopt closed-loop production models and green hydrogen furnaces for glass melting. The Renovation Wave Initiative, aimed at modernizing over 35 million buildings by 2030, continues to be a major growth catalyst.

Asia Pacific Advanced Glazing Systems Market Trends-Rapid Urban Growth Boosting High-Performance Glass Adoption

Asia Pacific stands as the fastest-growing regional market. The region’s growth is primarily fueled by rapid urbanization, industrial expansion, and an increasing focus on energy-efficient architecture. China and Japan dominate the regional production landscape, while India, South Korea, and Southeast Asia are emerging as key demand centers due to expanding infrastructure and rising adoption of smart and sustainable building practices.

China remains the largest market within the region, accounting for over 40% of Asia Pacific’s glazing system consumption in 2025. Its robust construction sector, backed by government initiatives such as the 14th Five-Year Plan for Green Building Development, emphasizes energy-efficient façades and high-performance window systems. Companies such as Xinyi Glass Holdings and CSG Holding Co. Ltd. have expanded their float glass and Low-E coating lines to serve both domestic and export markets.

For instance, Xinyi Glass launched a new high-transmittance glass line in Anhui Province in 2024, aimed at meeting the surging demand for solar control glazing in smart city projects. In Japan, technological innovation continues to drive adoption. Nippon Sheet Glass (NSG Group) introduced its Pilkington Spacia™ vacuum glazing for commercial retrofit programs, aligning with Japan’s Zero Energy Building (ZEB) initiative. The product has been widely deployed in Tokyo’s Marunouchi business district and Osaka’s high-rise office complexes, where space and thermal efficiency are critical. India’s market is experiencing exponential growth, supported by government initiatives such as the Smart Cities Mission and the Energy Conservation Building Code (ECBC). Indian developers are increasingly partnering with global suppliers such as Saint-Gobain India and Asahi India Glass (AIS) to integrate solar-control and laminated glazing into high-end commercial and residential projects.

Competitive Landscape

The global advanced glazing systems market is moderately consolidated, with a few multinational corporations controlling the majority of production capacity for coated and insulating glass. Companies such as Saint-Gobain, AGC Inc., and NSG Group maintain extensive global footprints. Emerging smart-glass innovators such as View Inc. and Gentex Corporation are capturing specialized niches through proprietary technologies and integration with digital building platforms.

Leading companies emphasize product innovation, vertical integration, and sustainability leadership. Strategies include R&D investment in low-carbon glass manufacturing, expansion of coating lines, and partnerships with façade system integrators to strengthen downstream presence.

Key Industry Developments

- In March 2025, View Inc. inaugurated a new electrochromic smart glass manufacturing facility in Olive Branch, Mississippi, tripling production capacity to cater to growing demand in commercial office and healthcare projects across North America.

- In February 2025, NSG Group (Pilkington) introduced its Spacia™ vacuum-insulated glass panels in Japan, expanding applications in space-constrained retrofits and ZEB-certified office buildings.

Companies Covered in Advanced Glazing Systems Market

- Saint-Gobain

- AGC Inc.

- Guardian Glass

- NSG Group (Pilkington)

- View Inc.

- Corning Incorporated

- Xinyi Glass Holdings

- Fuyao Glass Industry Group

- Gentex Corporation

- Research Frontiers Inc.

- Central Glass Co.

- Schott AG

- PPG Industries

- Cardinal Glass Industries

- Asahi Glass Co. (AGC Japan)

- Lotte Chemical

- HanGlas

- Sisecam Group

- Taiwan Glass Industry Corporation

- Nippon Electric Glass Co.

Frequently Asked Questions

The advanced glazing systems market size in 2025 is US$33.1 Billion.

The advanced glazing systems market is projected to reach US$56.8 Billion by 2032.

Key trends include growing adoption of smart and electrochromic glass integrated with building automation systems and increasing retrofits of commercial and institutional buildings to meet energy-efficiency regulations.

The Insulating Glass Units (IGUs) segment is the leading product type, accounting for 45% of total revenue in 2025, widely used in commercial buildings, airports, and healthcare facilities for thermal and acoustic performance.

The market is expected to grow at a CAGR of 7.2% from 2025 to 2032, driven by technological innovations, regulatory mandates, and increasing sustainable construction adoption.

Major players include Saint-Gobain, AGC Inc., Guardian Glass, NSG Group (Pilkington), and View Inc.