- Medical Devices

- Treatment Planning Systems and Advanced Image Processing Market

Treatment Planning Systems and Advanced Image Processing Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Treatment Planning Systems and Advanced Image Processing Market by Component (Treatment Planning Software and Advanced Image Processing Software), by Technique (3D Image Reconstruction, In-Room Imaging, and Image Registration using Graphics Processor Unit), by Application (Adaptive Radiotherapy, Online Monitoring, Tracking, Dose Accumulation, and Validation of Image Registration) by End User (Hospitals, Specialty clinics, Ambulatory Surgical Centers, and Diagnostics Centers), and Regional Analysis from 2026 to 2033.

Treatment Planning Systems and Advanced Image Processing Market Share and Trend Analysis

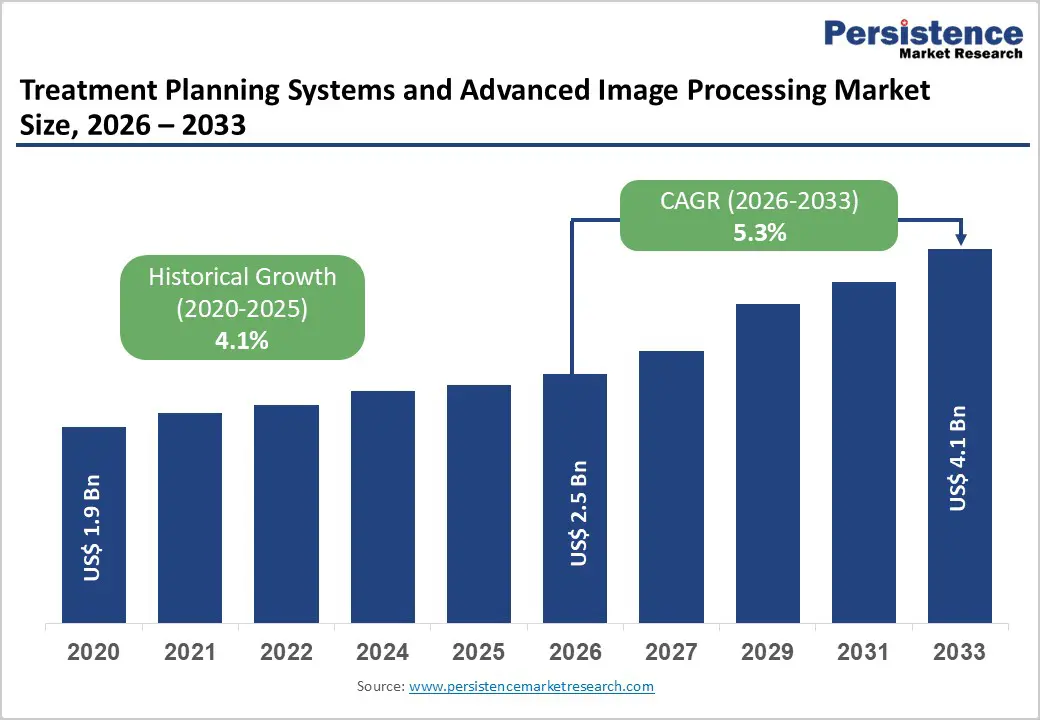

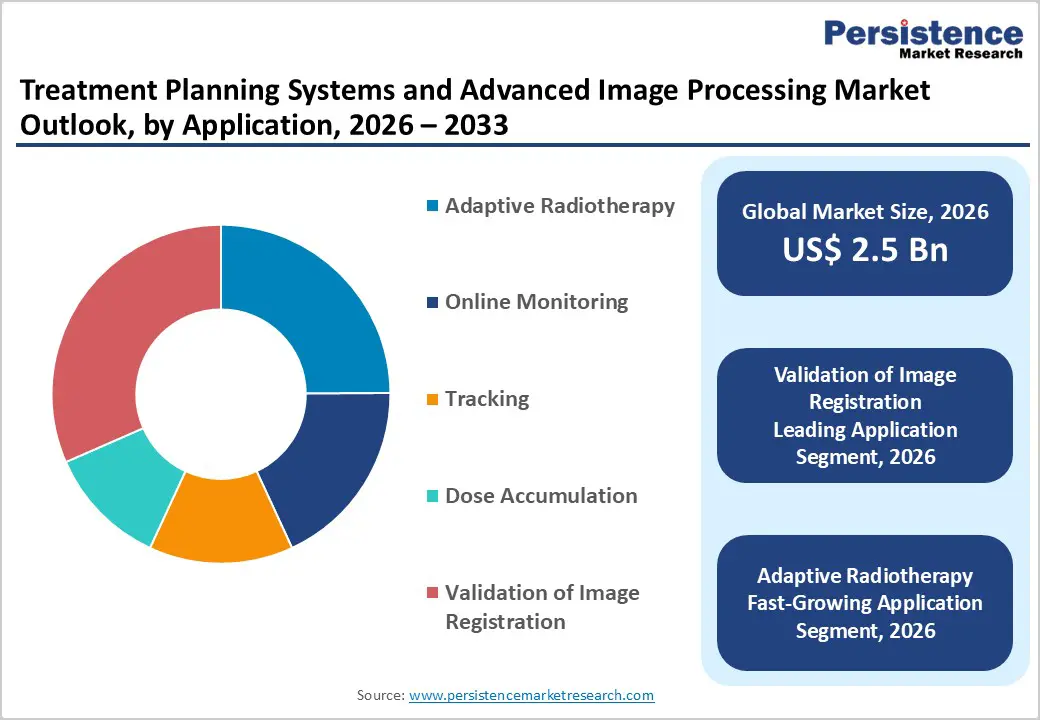

The global treatment planning systems and advanced image processing market size is estimated to grow from US$ 2.5 Bn in 2026 to US$ 4.1 Bn by 2033. The market is projected to record a CAGR of 5.3% during the forecast period from 2026 to 2033.

Global demand for treatment planning systems and advanced image processing solutions is increasing steadily, driven by rising cancer incidence, expanding radiotherapy capacity, and growing reliance on precision-guided treatment planning across hospitals and oncology centers. Increasing volumes of radiation therapy procedures, adoption of advanced techniques such as IMRT, VMAT, stereotactic radiosurgery, and proton therapy, and the need for accurate dose delivery are supporting sustained market growth across both developed and emerging healthcare systems. Higher utilization of image-guided and adaptive radiotherapy, coupled with longer treatment courses and repeat planning requirements, is further accelerating demand. Continuous improvements in image registration accuracy, dose calculation speed, AI-assisted contouring, and workflow automation are enhancing clinical efficiency and treatment outcomes. In addition, growing investments in cancer care infrastructure, outpatient oncology services, and digital health integration are further propelling the global treatment planning systems and advanced image processing market.

Key Industry Highlights

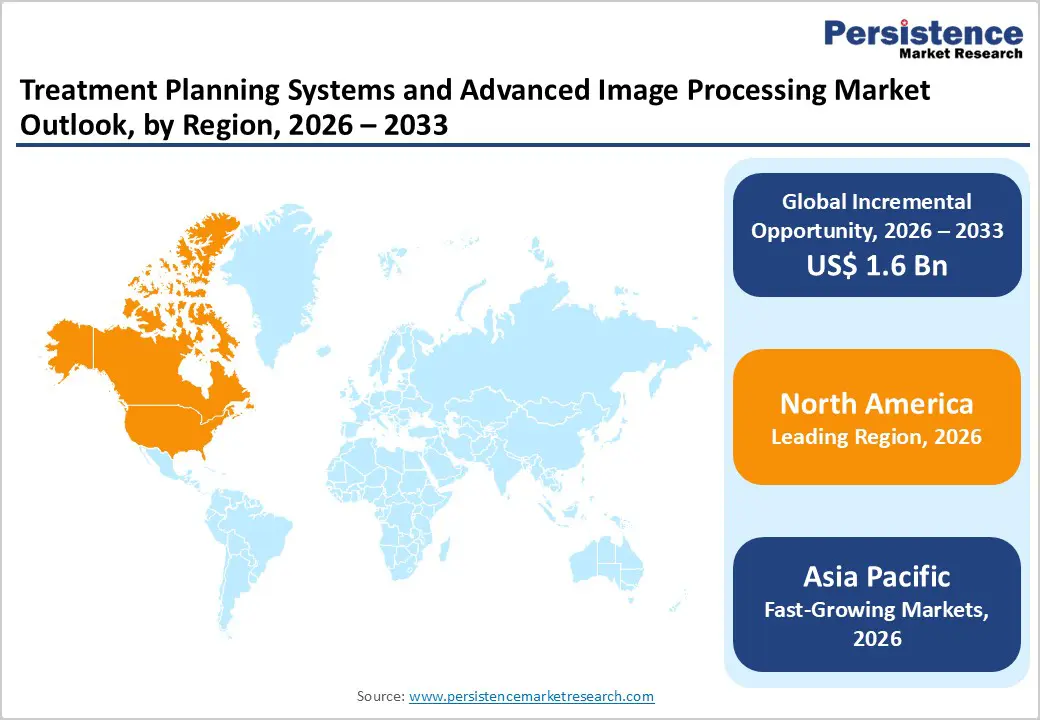

- Leading Region: North America holds the largest share at 46.7%, supported by advanced healthcare infrastructure, high radiotherapy adoption rates, strong reimbursement frameworks, and the presence of major treatment planning and imaging software providers.

- Fastest-Growing Region: Asia Pacific is expanding fastest due to rapid oncology infrastructure development, rising cancer burden, increasing radiotherapy installations, and growing government healthcare investments.

- Leading Component Segment: Treatment planning software dominates the market due to its recurring and long-term use across all radiotherapy workflows, including dose calculation, plan optimization, and treatment verification.

- Fastest-Growing Component Segment: Advanced image processing software is expanding rapidly as demand rises for adaptive radiotherapy, multimodal imaging integration, and real-time treatment monitoring.

- Leading Technique Segment: In-room imaging remains the most widely adopted technique, driven by its critical role in image-guided radiotherapy and on-table treatment verification.

- Fastest-Growing Technique Segment: Image registration using graphics processor unit is scaling quickly as providers seek faster processing speeds, higher accuracy, and support for adaptive and deformable image registration workflows.

| Key Insights | Details |

|---|---|

| Treatment Planning Systems and Advanced Image Processing Market Size (2026E) | US$ 2.5 Bn |

| Market Value Forecast (2033F) | US$ 4.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 5.3% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Dynamics

Driver – Rising Cancer Burden and Growing Reliance on Precision-Guided Radiotherapy

Growth is strongly driven by the increasing global burden of cancer and the expanding role of radiotherapy as a core treatment modality across oncology care pathways. Treatment planning systems and advanced image processing tools are fundamental to accurate tumor delineation, dose optimization, and protection of surrounding healthy tissues. Rising incidence of solid tumors, coupled with earlier diagnosis and improved survival rates, is increasing the total number of patients requiring radiation therapy over extended treatment cycles. In parallel, growing adoption of advanced techniques such as IMRT, VMAT, stereotactic radiosurgery, and proton therapy is intensifying the need for sophisticated planning and imaging capabilities.

Hospitals and cancer centers are increasingly prioritizing precision, reproducibility, and treatment efficiency, which directly supports continuous utilization of planning software and image registration tools. Aging populations further amplify demand, as cancer prevalence rises sharply with age. Additionally, expansion of radiotherapy infrastructure in emerging markets and increased access to oncology care are contributing to higher procedure volumes. Collectively, these factors are reinforcing sustained demand for advanced treatment planning and image processing solutions as essential components of modern cancer care delivery.

Restraints – High Implementation Costs, Workflow Complexity, and Regulatory Burden

Market growth is constrained by the high cost and operational complexity associated with implementing advanced treatment planning and image processing systems. These solutions require substantial upfront investment in software licenses, high-performance computing infrastructure, imaging integration, and ongoing maintenance. Smaller hospitals and standalone oncology centers often face budget limitations, delaying adoption or restricting upgrades to newer platforms. In addition, integration with existing hospital information systems, imaging modalities, and radiotherapy equipment can be technically challenging, increasing deployment timelines and reliance on specialized technical expertise.

Regulatory and quality assurance requirements further add to the burden, as treatment planning software must comply with stringent safety, validation, and documentation standards. Any software malfunction or planning error carries significant clinical risk, increasing liability concerns and slowing adoption of newer technologies. Frequent software updates, cybersecurity considerations, and staff training requirements also contribute to operational strain. In cost-sensitive healthcare systems, reimbursement constraints and pressure to control oncology treatment expenses can limit purchasing decisions. Together, these financial, technical, and regulatory challenges act as barriers to rapid penetration, particularly in low- and middle-income regions.

Opportunity – AI Integration, Adaptive Radiotherapy, and Expansion in Emerging Oncology Markets

Significant opportunities are emerging from technological advancements and evolving clinical practices that emphasize personalization and adaptability in cancer treatment. The growing integration of artificial intelligence and machine learning into treatment planning and image processing is enhancing automation, reducing planning time, and improving consistency across complex cases. Adaptive radiotherapy, which requires frequent imaging, plan modification, and dose recalculation, is gaining traction and creating demand for robust image registration and validation tools.

Expansion of cancer care infrastructure in emerging economies represents another major growth avenue, as governments invest in radiotherapy centers and digital health modernization. Increasing availability of trained medical physicists and radiation oncologists in these regions is further supporting adoption. Additionally, vendors are developing cloud-based platforms and modular software offerings that lower entry barriers and enable scalable deployment. Growing emphasis on value-based care and treatment outcome optimization is encouraging providers to invest in technologies that improve accuracy and reduce re-treatment rates. As clinical confidence in advanced planning algorithms grows, suppliers are well positioned to capture long-term demand across both mature and developing oncology markets.

Category-wise Analysis

Radiotherapy Workflows

The treatment planning software segment is projected to dominate the global treatment planning systems and advanced image processing market in 2026, accounting for a revenue share of 87.6%. This dominance is primarily driven by its indispensable role in radiation oncology workflows, where accurate dose calculation, target delineation, and treatment optimization are required for every patient undergoing radiotherapy. Treatment planning software is used repeatedly across planning, simulation, plan adaptation, and verification stages, resulting in high utilization rates across hospitals and cancer centers. The increasing adoption of intensity-modulated radiotherapy (IMRT), volumetric modulated arc therapy (VMAT), stereotactic radiosurgery, and proton therapy further reinforces demand. Rising cancer incidence, growth in radiotherapy infrastructure, and increasing preference for adaptive and image-guided treatments are accelerating software deployment. Additionally, continuous upgrades, software licensing models, and integration with imaging and oncology information systems contribute to recurring revenues, supporting the segment’s leadership position within the market.

By Application, Validation of Image Registration Leads Due to Its Critical Importance in Treatment Accuracy

The validation of image registration segment is expected to dominate the global treatment planning systems and advanced image processing market in 2026, accounting for a revenue share of 28.4%. This leadership is driven by the critical need to ensure spatial accuracy when integrating multimodal imaging data such as CT, MRI, and PET scans for radiotherapy planning and delivery. Accurate image registration validation is essential for precise tumor localization, organ-at-risk delineation, and dose distribution verification, particularly in complex cases involving adaptive radiotherapy. Increasing use of image-guided radiotherapy, motion management techniques, and deformable image registration has significantly elevated the importance of robust validation tools. The growing volume of radiotherapy procedures, coupled with stricter clinical quality assurance requirements, is further driving adoption. As treatment precision becomes increasingly central to improving outcomes and minimizing toxicity, validation of image registration continues to represent the most revenue-generating application segment.

By End User, Hospitals Lead Due to High Radiotherapy Volumes and Advanced Oncology Infrastructure

The hospitals segment is projected to dominate the global treatment planning systems and advanced image processing market in 2026, accounting for a revenue share of 45.0%. Hospitals serve as the primary centers for cancer diagnosis, radiotherapy delivery, and multidisciplinary oncology care, resulting in high and consistent utilization of treatment planning and imaging software. Large patient inflows for cancer treatment, trauma care, and complex surgical interventions necessitate advanced imaging, precise planning, and continuous treatment optimization. Hospitals are also more likely to invest in high-end radiotherapy systems, including linear accelerators, proton therapy units, and hybrid imaging platforms, which require sophisticated planning and image processing solutions. The presence of specialized oncology departments, trained medical physicists, and integrated IT infrastructure further supports adoption. Additionally, expansion of public and private hospitals, particularly tertiary care centers, continues to reinforce hospitals as the dominant end-user segment.

Region-wise Insights

North America Treatment Planning Systems and Advanced Image Processing Market Trends

North America is expected to dominate the global treatment planning systems and advanced image processing market with a value share of 46.7% in 2026, led primarily by the United States. The region benefits from a highly advanced healthcare infrastructure, widespread availability of radiotherapy centers, and early adoption of cutting-edge oncology technologies. High cancer prevalence and strong screening programs drive sustained demand for radiation therapy, directly supporting the use of treatment planning and advanced imaging software.

North America also records high utilization of IMRT, VMAT, stereotactic radiosurgery, and proton therapy, all of which require sophisticated planning and image processing capabilities. Favorable reimbursement policies and standardized clinical protocols encourage consistent adoption across hospitals and specialty cancer centers. The region is home to several leading market players, fostering rapid innovation, AI integration, and continuous software upgrades. Additionally, strong regulatory oversight and emphasis on treatment accuracy and patient safety further strengthen North America’s leadership position.

Europe Treatment Planning Systems and Advanced Image Processing Market Trends

The Europe treatment planning systems and advanced image processing market is expected to grow steadily, supported by well-established public healthcare systems, increasing cancer burden, and strong focus on precision medicine. Countries such as Germany, the U.K., France, Italy, and the Nordic nations exhibit high adoption of radiotherapy, driving demand for advanced treatment planning and imaging solutions. Aging populations and rising incidence of solid tumors and hematological malignancies are increasing the volume of radiation treatments across the region.

Europe also demonstrates strong adherence to clinical guidelines, quality assurance standards, and regulatory frameworks, which promotes the use of validated image registration and planning software. Government-funded healthcare systems ensure broad access to cancer care, resulting in consistent utilization across public hospitals. Furthermore, ongoing investments in radiotherapy modernization, adoption of adaptive radiotherapy, and expansion of outpatient oncology services continue to support market growth across Europe.

Asia Pacific Treatment Planning Systems and Advanced Image Processing Market Trends

The Asia Pacific treatment planning systems and advanced image processing market is expected to register a relatively higher CAGR of around 7.2% between 2026 and 2033, driven by rapid expansion of healthcare infrastructure and increasing cancer patient volumes. Large populations in China, India, Japan, and Southeast Asia, combined with rising cancer incidence, are significantly boosting demand for radiotherapy services and associated software solutions. Governments across the region are investing heavily in hospital construction, cancer centers, and radiotherapy equipment to improve access to oncology care.

Growing medical tourism in countries such as India and Thailand further contributes to increased treatment volumes. Cost-sensitive markets are encouraging adoption of scalable and locally supported software platforms. Additionally, improving awareness of early cancer diagnosis, expanding insurance coverage, and increasing adoption of advanced imaging technologies are expected to sustain long-term market growth across the Asia Pacific region.

Market Competitive Landscape

The global treatment planning systems and advanced image processing market is highly competitive, with strong participation from companies such as Accuray Incorporated, Elekta, Koninklijke Philips NV, RaySearch Laboratories, and Varian Medical Systems. These players leverage extensive global sales and service networks, strong brand equity, and continuous software-driven innovation across treatment planning platforms, imaging analytics, and workflow integration tools to support precise, efficient, and patient-specific radiation therapy delivery.

Rising demand for hospital-based cancer care, increasing radiotherapy procedures, growing adoption of adaptive radiotherapy, and the need for accuracy in complex treatment planning are driving portfolio expansion and solution differentiation. Vendors are increasingly focusing on AI-enabled image processing, faster dose calculation, improved image registration accuracy, and seamless integration with imaging and oncology information systems. Strategic priorities include strengthening collaborations with hospitals and cancer centers, expanding presence in emerging healthcare markets, and investing in R&D to support advanced imaging algorithms and next-generation treatment planning capabilities, thereby sustaining long-term market growth.

Key Industry Developments:

- In November 2025, ConcertAI’s TeraRecon announced TeraRecon AV™, an advanced AI-enabled medical imaging visualization platform designed to improve diagnostic accuracy and streamline clinical workflows. The secure, cloud-based solution integrates seamlessly with existing radiology and cardiology PACS, enabling enterprise-wide imaging standardization and supporting multiple clinical sub-specialties through automated and specialized visualization tools.

- In February 2025, Philips introduced new AI-assisted workflow and quantitative measurement capabilities across its EPIQ Elite and Affiniti ultrasound systems, aimed at accelerating exam times and enhancing diagnostic consistency. These enhancements reduce operator dependency, support faster clinical decision-making, and improve overall confidence in routine and complex ultrasound assessments.

Companies Covered in Treatment Planning Systems and Advanced Image Processing Market

- Accuray Incorporated

- Elekta

- Koninklijke Philips NV

- RaySearch Laboratories

- Varian Medical Systems

- Brainlab

- Prowess

- DOSIsoft SA

- Viewray

- MIM Software

- GE HealthCare

- Hitachi, Ltd.

- IBA Radiopharma Solutions

- Others

Frequently Asked Questions

The global treatment planning systems and advanced image processing market is projected to be valued at US$ 2.5 Bn in 2026.

The global treatment planning systems and advanced image processing market is driven by rising hospitalizations, increasing surgical procedures, growing chronic disease burden, and expanding use of IV therapy in critical and long-term care.

The global treatment planning systems and advanced image processing market is poised to witness a CAGR of 5.3% between 2026 and 2033.

Key opportunities lie in the expansion of home-based infusion therapy, demand for ready-to-use and customized IV formulations, and rapid healthcare infrastructure growth in emerging markets.

Accuray Incorporated, Elekta, Koninklijke Philips NV, RaySearch Laboratories, and Varian Medical Systems are some of the key players in the treatment planning systems and advanced image processing market.