- Medical Devices

- Advanced Wound Dressing Market

Advanced Wound Dressing Market Size, Share, and Growth Forecast, 2026 - 2033

Advanced Wound Dressing Market by Product Type (Foam Dressings, Hydrocolloid Dressings, Film Dressings, Others), Application (Chronic Wounds, Acute Wounds), End-User (Hospitals, Specialty Clinics, Home Healthcare, Physician Office, Nursing Homes, Others), and Regional Analysis for 2026 - 2033

Advanced Wound Dressing Market Share and Trends Analysis

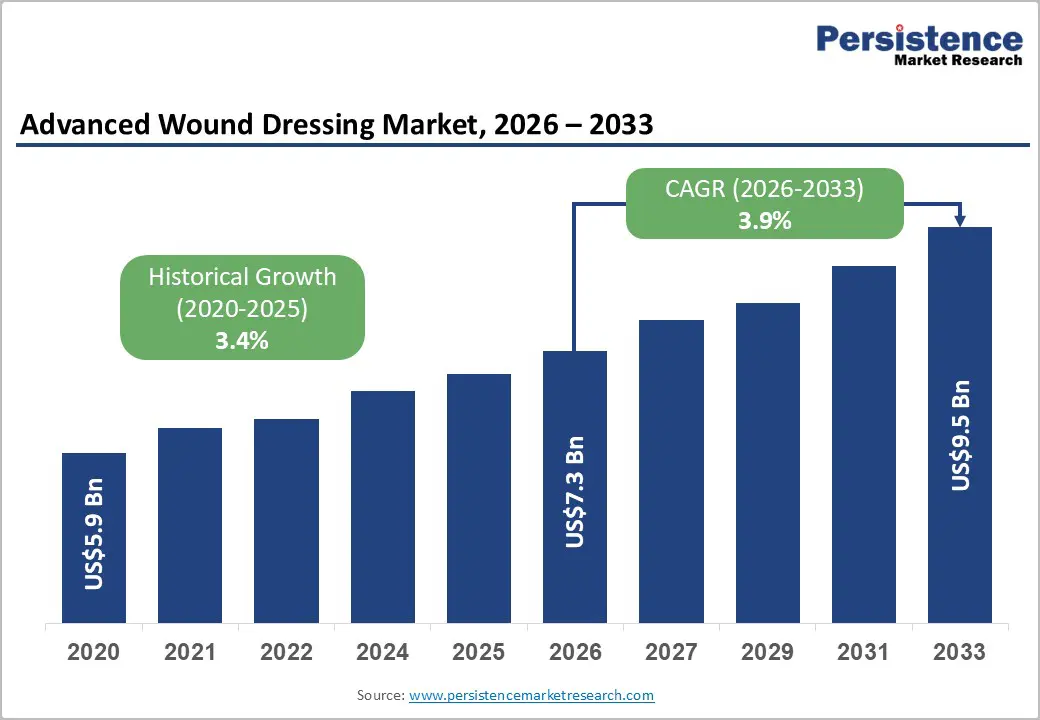

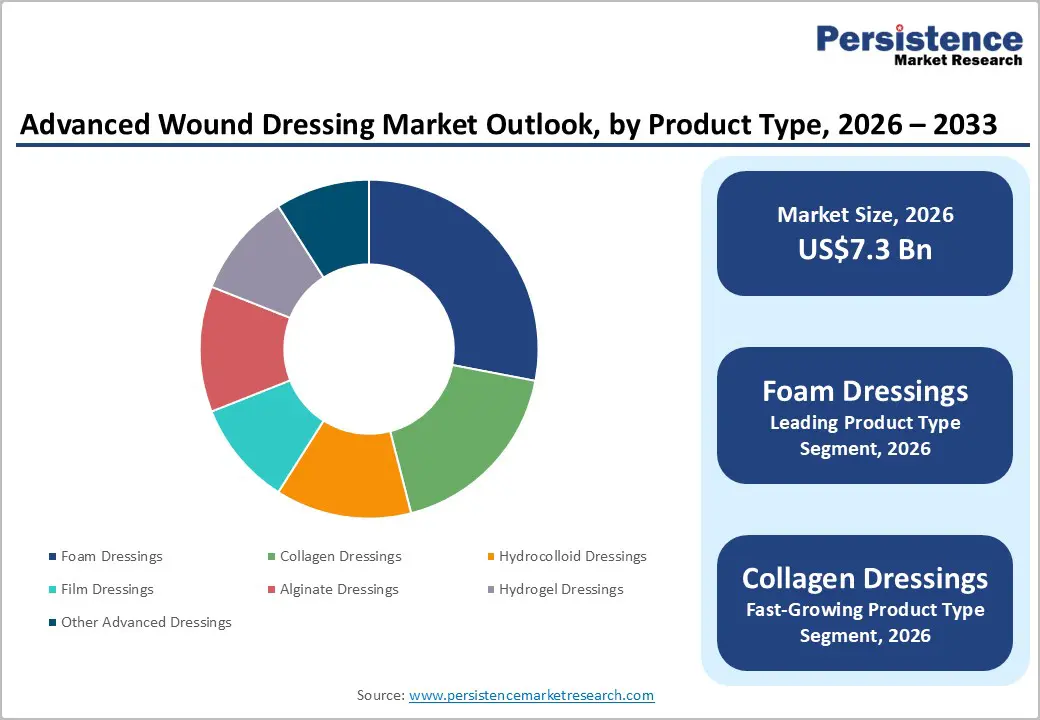

The global advanced wound dressing market size is likely to be valued at US$7.3 billion in 2026 and is estimated to reach US$9.5 billion by 2033, growing at a CAGR of 3.9% during the forecast period from 2026 to 2033, driven by rising chronic wound prevalence, expanding geriatric populations, and accelerating adoption of bioactive dressing technologies across clinical settings.

The aging global demographic is a foundational catalyst. The United Nations Department of Economic and Social Affairs projects the population aged 65 and above will reach 1.5 billion by 2050. This trend substantially increases patient burden associated with diabetic foot ulcers, pressure injuries, and venous leg ulcers.

Key Industry Highlights:

- Leading Product Type: Foam dressings are set to hold around 28% revenue share in 2026, driven by broad clinical adoption in pressure injury management protocols across acute care facilities.

- Fastest-growing Product Type: Collagen dressings are projected as the fastest-growing segment, supported by increasing clinical validation in bioactive wound management and adoption within advanced wound care center formularies.

- Leading Application: Chronic wounds are estimated to hold roughly 62% revenue share in 2026, due to the high global prevalence of diabetic foot ulcers and pressure injuries, creating sustained, recurring clinical demand.

- Fastest-Growing Application: Acute wounds are forecast to record the fastest growth, driven by rising global surgical volumes and integration of advanced dressings into post-operative enhanced recovery protocols.

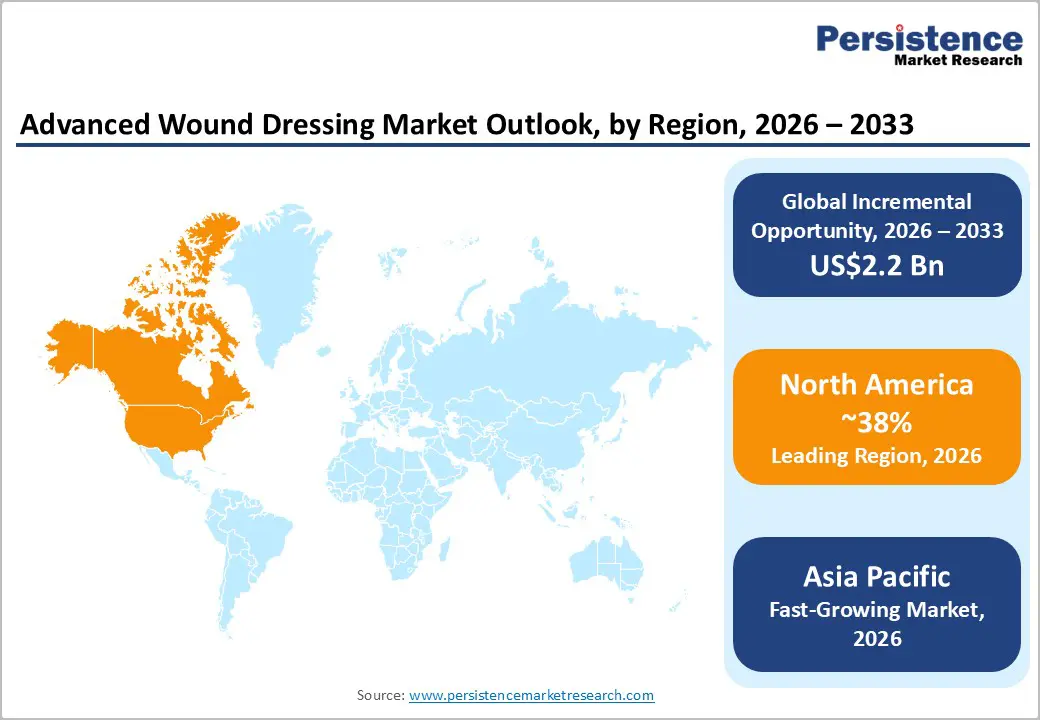

- Regional Leadership: North America is projected to capture roughly 38% of the advanced wound dressing market share in 2026, while Asia Pacific is forecast to record the fastest growth due to rapid hospital infrastructure modernization.

- Innovation Trends: Technological advancements in bioactive dressing matrices, digital wound monitoring integration, and smart dressing platforms incorporating real-time infection biomarker detection are shaping long-term market evolution and investment direction.

DRO Analysis

Driver - Rising Global Prevalence of Diabetes and Chronic Wounds

The escalating incidence of diabetes is generating sustained demand for advanced wound dressings. According to the International Diabetes Federation, approximately 537 million adults were living with diabetes in 2021, projected to reach 783 million by 2045. Diabetic foot ulcers affect an estimated 15% of diabetic patients during their lifetime. This epidemiological pressure directly translates into procurement volumes for foam, hydrocolloid, and alginate formats.

Suboptimal wound management amplifies this urgency. Extended wound chronicity leads to higher rates of infection, limb amputation, and inpatient readmissions. Health systems seeking to contain these downstream expenditures are increasingly standardizing on advanced dressing protocols. This institutional demand sustains market momentum through the forecast period.

Restraint - Supply Chain Limitations for Bioactive Wound Care Materials

Manufacturing of advanced dressings depends on a reliable supply of alginate fibers, medical-grade silicone, hydrogel polymers, and collagen materials. Production delays or shortages increase operational costs and reduce inventory availability for hospitals and distributors. Global transportation disruptions and quality compliance requirements continue to affect delivery timelines across wound care supply networks.

Stringent sterilization and packaging standards increase operational complexity for manufacturers operating across multiple regulatory jurisdictions. Scaling bioactive dressing production requires high capital investment in cleanroom infrastructure and quality validation systems. Smaller manufacturers face challenges related to procurement stability and regulatory certification, reducing competitive flexibility in emerging healthcare markets.

Opportunity - Expansion of Home Healthcare and Remote Wound Monitoring

Home healthcare expansion is creating new commercial opportunities for easy-to-apply advanced dressings designed for long-duration wear and lower replacement frequency. Healthcare providers are encouraging outpatient recovery models to reduce hospital congestion and treatment costs. Remote wound monitoring technologies are supporting earlier intervention and improving treatment continuity for chronic wound patients receiving care outside hospital settings.

Manufacturers can strengthen market penetration through the development of smart dressings integrated with moisture sensors, antimicrobial indicators, and digital monitoring compatibility. Telehealth adoption is supporting collaboration between wound specialists and home healthcare providers. Product portfolios designed for elderly patient groups and diabetic wound management are expected to achieve stronger adoption across community healthcare systems and post-acute care environments.

Category-wise Analysis

Product Type Insights

Foam dressings are anticipated to secure around 28% of the advanced wound dressing market share in 2026, reflecting widespread clinical adoption for moderate to heavily exuding wounds. Products from Molnlycke Health Care are routinely specified in pressure injury management protocols due to superior absorbency. This enables extended wear periods that reduce dressing change frequency and associated labor costs in acute care settings.

Collagen dressings are expected to be the fastest-growing segment, propelled by the rising adoption of bioactive wound management protocols. Products such as Integra Dermal Regeneration Template, deployed in chronic wound settings across leading U.S. academic medical centers, demonstrate collagen scaffolding efficacy in stimulating granulation tissue. This directly drives formulary adoption and above-average segment growth through the forecast period.

Application Insights

Chronic wounds are poised to dominate with a forecast market share of over 62% in 2026, powered by growing global prevalence of diabetic foot ulcers, venous leg ulcers, and pressure injuries. Specialized wound care clinics such as the Healogics network in the U.S. deploy advanced dressing protocols as standard of care, generating consistently high product utilization volumes and sustaining segment leadership.

Acute wounds are estimated to be the fastest-growing segment, fueled by rising surgical procedure volumes globally and expanding post-operative wound care standardization. Hospitals such as Mayo Clinic are integrating advanced post-surgical dressing protocols into enhanced recovery after surgery (ERAS) programs. This reduces surgical site infection rates and validates the clinical rationale for premium acute wound dressing adoption.

End-user Insights

Hospitals are likely to be the leading segment with a projected 44% of the advanced wound dressing market share in 2026, due to the concentration of complex wound management cases and institutional formulary systems. Major hospital networks such as HCA Healthcare have centralized wound care supply chain management. This enables bulk purchasing agreements with manufacturers and sustains high, predictable utilization volumes.

Home healthcare is anticipated to be the fastest-growing segment, fueled by the global transition toward decentralized care delivery driven by cost-containment pressures and aging-in-place patient preferences. Companies such as Amedisys and LHC Group in the U.S. are expanding home wound care service lines. This creates consistent demand for user-friendly advanced dressing formats that non-clinical caregivers can apply with minimal training.

Regional Insights

North America Advanced Wound Dressing Market Trends

North America is expected to lead with an estimated 38% of the advanced wound dressing market share in 2026, supported by high chronic wound prevalence, advanced reimbursement systems, and strong hospital infrastructure. Large diabetic patient populations are increasing the demand for foam, collagen, and hydrogel dressing technologies.

U.S. Advanced Wound Dressing Market Insights

The U.S. is projected to account for the dominant share within North America. Approximately 6.5 million Americans are estimated to be affected by chronic wounds annually, as referenced by the National Institutes of Health. Adoption of value-based care contracts by major payers is expected to accelerate integration of advanced dressings into bundled payment arrangements, directly increasing procurement volumes.

Canada Advanced Wound Dressing Market Insights

Canada is forecast to exhibit steady growth through 2033, supported by provincial health authority procurement standardization. Health Canada's regulatory alignment with international ISO standards is expected to streamline market entry for innovative dressing formats. Partnerships between Canadian wound care centers and manufacturers such as Coloplast are likely to expand advanced dressing access across both urban academic centers and rural community hospitals.

Europe Advanced Wound Dressing Market Trends

Europe is expected to hold a major share of the global market, driven by structured National Health Service frameworks and rising investments in geriatric care management solutions across Western European nations. Clear clinical protocols prioritizing moist wound healing methods over conventional practices maintain consistent demand for hydrocolloid and foam categories.

Germany Advanced Wound Dressing Market Insights

Germany is likely to be the primary revenue contributor within Europe, supported by comprehensive statutory health insurance coverage and a well-integrated network of specialized outpatient wound management centers. Institutional procurement groups show strong preferences for multi-layer dressings featuring integrated exudate-locking technologies to optimize total cost of treatment metrics.

U.K. Advanced Wound Dressing Market Insights

The U.K. is forecast to record steady growth as National Health Service (NHS) initiatives focus on shifting chronic ulcer management from expensive secondary acute facilities into community care environments. This policy shift increases the utilization of advanced, extended-wear alginate and hydrogel dressings by community-based nursing teams.

Asia Pacific Advanced Wound Dressing Market Trends

Asia Pacific is forecast to be the fastest-growing market for advanced wound dressing, stimulated by expanding clinical infrastructure developments, rising healthcare access levels, and surging type 2 diabetes diagnoses across urban centers. Emerging healthcare reforms across key developing nations accelerate the institutional modernization of secondary care networks.

China Advanced Wound Dressing Market Insights

China is projected to exhibit rapid market expansion, supported by national manufacturing initiatives and extensive hospital construction programs designed to expand specialized medical access across secondary cities. Local clinical guidelines increasingly incorporate advanced foam and antimicrobial configurations to address expanding post-operative patient volumes.

India Advanced Wound Dressing Market Insights

India is expected to register significant growth velocity, driven by escalating diabetic populations and an expanding private hospital sector investing heavily in specialized surgical infrastructure. Rising disposable incomes and expanding private medical insurance penetration support an ongoing clinical transition from basic dressings to modern advanced wound therapies.

Competitive Landscape

The global advanced wound dressing market is moderately consolidated, with a small group of multinational corporations commanding substantial combined revenue share through diversified product portfolios and established hospital relationships. Key participants, including Smith and Nephew, 3M Company, Molnlycke Health Care, Coloplast, and Acelity (a KCI Company), leverage scale advantages in regulatory compliance and global distribution to sustain competitive positioning against regional competitors.

The mid-tier competitive landscape is characterized by specialty manufacturers focusing on specific wound types or dressing technologies. Emerging entrants from Asia Pacific are gaining ground in price-sensitive segments by offering regulatory-compliant products at lower cost structures. This dynamic is intensifying competitive pressure on margins in standardized product categories while creating differentiation incentives in bioactive and smart dressing tiers.

Key Industry Developments:

- In May 2026, Smith+Nephew announced the launch of ALLEVYN COMPLETE CARE Dressing and RENASYS EDGE tNPWT technologies at EWMA 2026, reinforcing innovation in chronic wound management and advanced wound dressing solutions.

- In January 2026, Tiger BioSciences acquired Platelet-Rich Fibrin Matrix wound care technology from Bahia Medical Inc., reinforcing the expansion of autologous advanced wound dressing therapy capabilities for chronic and complex wound treatment.

- In September 2025, Smith+Nephew launched the CENTRIO Platelet-Rich-Plasma System to expand its advanced wound bioactives portfolio, reinforcing innovation in autologous advanced wound dressing therapies for chronic wound management.

Companies Covered in Advanced Wound Dressing Market

- Smith and Nephew plc

- 3M Company

- Molnlycke Health Care AB

- Coloplast A/S

- Acelity L.P. Inc. (KCI)

- Medline Industries LP

- Paul Hartmann AG

- Integra LifeSciences Holdings Corporation

- Convatec Group plc

- Derma Sciences Inc.

- Winner Medical Co. Ltd.

- Hollister Incorporated

- Cardinal Health Inc.

- Essity AB

- Nitto Denko Corporation

Frequently Asked Questions

The advanced wound dressing market is projected to reach US$7.3 billion in 2026.

Rising prevalence of chronic wounds, increasing diabetic ulcer cases, expanding elderly population groups, and growing adoption of infection-control wound management technologies are driving the advanced wound dressing market.

The advanced wound dressing market is poised to witness a CAGR of 3.9% from 2026 to 2033.

Expansion of home healthcare services, development of bioactive and antimicrobial dressings, and integration of smart wound monitoring technologies are creating significant growth opportunities in the advanced wound dressing market.

Some of the key market players include Smith and Nephew, 3M Company, Molnlycke Health Care, Coloplast, and Acelity.