- Media & Entertainment

- 3D Animation Market

3D Animation Market Size, Share, and Growth Forecast 2026 - 2033

3D Animation Market by Component (Software, Hardware, Services), Technique (3D Modeling, Motion Graphics, 3D Rendering, Visual Effects (VFX), Others), Deployment (On-Premise, On-Demand), End-user (Media & Entertainment, Gaming & Interactive Media, Architecture & Construction, Manufacturing & Engineering, Education & Academics, Healthcare & Life Sciences, Government & Defense, Other), and Regional Analysis for 2026 - 2033

3D Animation Market Size and Trend Analysis

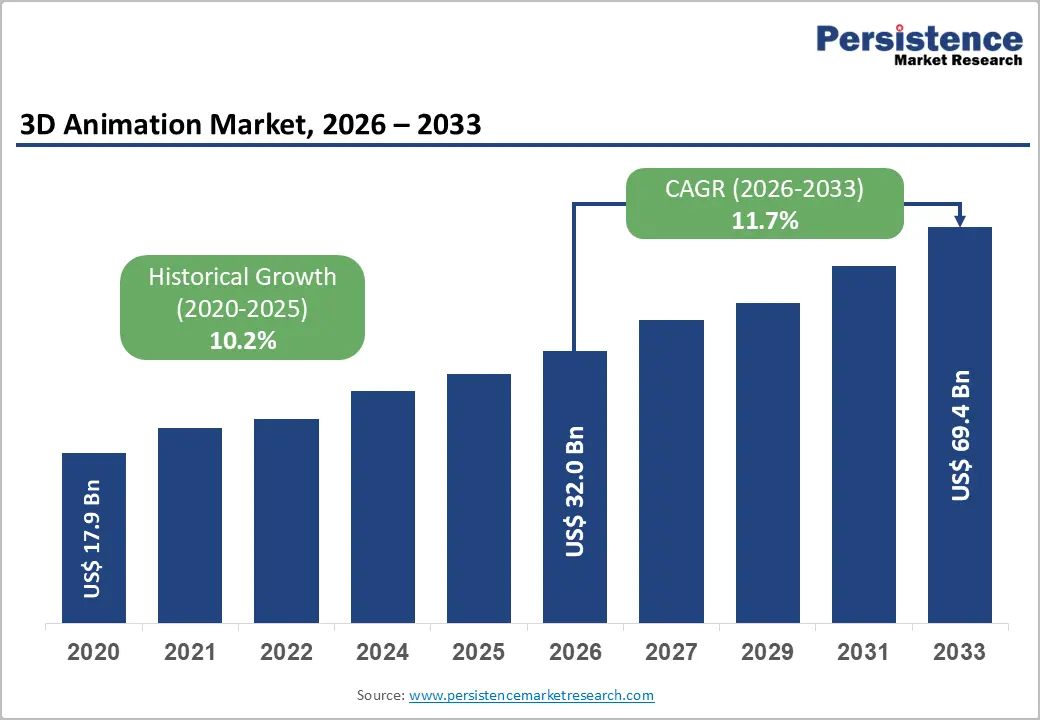

The global 3D Animation market is valued at US$ 32 billion in 2026 and is projected to reach US$ 69.4 billion by 2033, growing at a CAGR of 11.7% between 2026 and 2033. On the demand side, the accelerating global appetite for high-fidelity visual content, spanning blockbuster films, OTT streaming series, immersive gaming experiences, and virtual reality, continues to push studios and enterprises to invest heavily in 3D animation capabilities.

Simultaneously, supply-side advances, including the proliferation of artificial intelligence (AI)-assisted animation tools, cloud-based rendering platforms, and real-time graphics engines, are dramatically lowering production costs and timelines.

Key Industry Highlights:

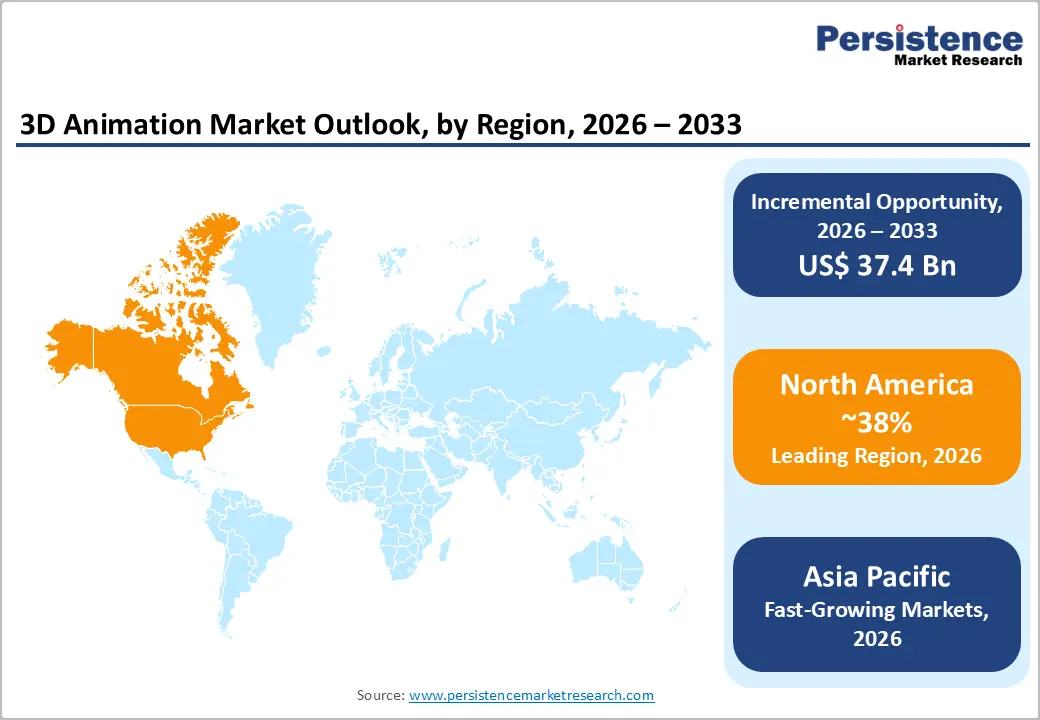

- Leading Region: North America commands approximately 38% of the global 3D Animation market revenue share, anchored by world-class studios, leading software developers, and the highest per-capita consumption of animated content across entertainment and gaming platforms.

- Fastest Growing Region: Asia Pacific is the fastest-growing regional market, projected at a CAGR of 14.4%, driven by surging domestic content demand, government investment in creative technology industries, and India's emergence as a global animation outsourcing hub.

- Leading Component: Software segment holds approximately 54% of component-level revenue, driven by widespread enterprise adoption of leading platforms such as Autodesk Maya, Adobe Creative Cloud, and Maxon Cinema 4D through recurring subscription models.

- Fast-Growing Segment: The Visual Effects (VFX) segment is projected to grow at a CAGR of 14.8% from 2026 to 2033, propelled by the rise in consumer demand for photorealistic content in streaming films, AAA gaming titles, and immersive virtual reality experiences.

- Key Opportunity: The intersection of 3D animation with healthcare simulation and metaverse platform development represents a high-growth incremental opportunity, with companies such as Meta and medical training platform providers actively investing in AI-powered 3D world-building and surgical simulation technologies.

DRO Analysis

Drivers - Surging Demand for High-Quality Content on OTT and Streaming Platforms

The explosive growth of over-the-top (OTT) streaming services has emerged as one of the most formidable drivers of the global 3D Animation market. Platforms such as Netflix, Disney+, and Amazon Prime Video are racing to build expansive libraries of animated feature films, episodic series, and short-form content, placing enormous demand on animation studios worldwide. According to the U.S. Bureau of Economic Analysis (BEA), the film and television industries contributed over US$ 200 billion to the U.S. economy in 2020, with animated content accounting for a material share of box-office and streaming revenue.

Learners also retain 60% more information when content is visualized through animation, reinforcing demand in education-linked streaming. As global broadband penetration rises, U.S. households with broadband connections exceeded 118 million by 2021, per the U.S. Federal Communications Commission (FCC), the subscriber base for OTT services continues to expand, compelling platform operators to greenlight an ever-larger slate of 3D-animated productions.

Rapid Adoption of AI and Real-Time Rendering Technologies

Technological advancements in artificial intelligence (AI), machine learning (ML), and real-time rendering are fundamentally transforming 3D animation workflows, making high-quality production faster and more cost-effective. AI-driven tools are automating labor-intensive tasks such as motion capture cleaning, facial expression rigging, and in-between frame generation, dramatically reducing per-minute production costs.

NVIDIA Corporation's Omniverse platform, for instance, enables collaborative real-time 3D production across geographically distributed teams, shortening project timelines significantly. In December 2024, World Labs introduced an AI system capable of generating interactive 3D environments from a single 2D image, illustrating the pace of innovation reshaping the industry. These efficiencies are attracting a broader cohort of small studios and independent creators into the market.

Restraints - High Production Costs and Hardware Investment Requirements

Despite technological advancements, the high capital requirements associated with premium 3D animation production remain a significant barrier to market participation, particularly for small and mid-sized studios. Creating a single minute of high-quality 3D animated content can cost between US$ 7,000 and US$ 8,000, and major animated feature films, such as those produced by Walt Disney Animation Studios or Pixar Animation Studios, routinely carry budgets exceeding US$ 200 million.

Beyond creative costs, the specialized hardware required for rendering, including high-performance workstations, GPU-accelerated rendering farms, and enterprise-grade storage, represents a substantial ongoing capital expenditure. Approximately 47% of smaller studios and educational institutions cite cost barriers as a primary constraint on their adoption of advanced 3D tools, limiting competitive breadth in the market and concentrating premium production capacity among large incumbents.

Talent Shortages and Skill Gaps

The 3D animation industry is confronted with a persistent and intensifying shortage of skilled professionals. Producing photorealistic, technically complex animation demands expertise spanning 3D modeling, rigging, rendering, compositing, VFX supervision, and pipeline engineering, disciplines that require years of specialized training. Approximately 54% of animation studios report difficulty in sourcing adequately skilled talent, constraining production capacity and driving up labor costs.

As the demand for animated content across entertainment, gaming, healthcare, and architecture accelerates, the talent gap is expected to widen unless addressed through expanded vocational training and academic programs. Furthermore, the rapid evolution of production tools, particularly AI-integrated platforms and real-time engines, necessitates continuous upskilling, adding to human resource overheads. This deficit in the talent pipeline poses a measurable drag on the market's ability to scale production output in line with demand.

Opportunities - Healthcare and Life Sciences: Expanding Frontier for Medical Visualization

The healthcare and life sciences sector represents a high-growth, high-value opportunity for 3D animation market participants. Medical institutions, pharmaceutical companies, and surgical device manufacturers are increasingly deploying 3D animation for patient education, surgical simulation, equipment marketing, and medical training. Companies such as Osso VR are pioneering virtual reality-based surgical training platforms that leverage sophisticated 3D animation to allow medical professionals to rehearse complex procedures in risk-free simulated environments.

The global healthcare VR market is expanding rapidly alongside virtual production, creating a broad addressable market. The Asia Pacific region's burgeoning healthcare infrastructure modernization is expected to generate additional demand. As regulatory bodies and hospital networks incorporate digital simulation into clinical training curricula, 3D animation service providers with domain-specific expertise stand to capture recurring, high-margin contracts in this adjacent vertical.

Metaverse and Immersive Experience Development

The emergence of the metaverse and the proliferation of augmented reality (AR) and virtual reality (VR) platforms are creating substantial new demand for interactive 3D animation content. Meta Platforms' partnership with James Cameron's Lightstorm Vision, announced in December 2024, to produce immersive 3D content for the Meta Quest headset ecosystem, is a landmark example of how technology platforms are commissioning original high-fidelity animated content at scale.

Similarly, in December 2024, Google DeepMind introduced Genie 2, an AI system capable of generating fully playable 3D worlds from simple text or image prompts, signaling a transformative shift in content creation economics. As enterprise use cases in virtual meetings, digital twins, product design, and consumer entertainment coalesce around immersive environments, companies with robust 3D modeling, rendering, and real-time animation capabilities are well-positioned to secure long-term platform partnerships and licensing revenues.

Category-wise Analysis

Component Insights

The Software segment holds the dominant position within the 3D Animation market by component, accounting for approximately 54% of total market revenue. This leadership is driven by the ubiquitous deployment of professional-grade animation platforms, including Autodesk Maya, Adobe After Effects, Cinema 4D by Maxon Computer GmbH, and open-source solutions such as Blender, across studios of all sizes.

Software solutions command recurring licensing revenues, particularly as vendors transition to subscription-based models that provide predictable cash flows. The migration of rendering and pipeline management to cloud-based software platforms is further reinforcing the segment's dominance, as on-premise hardware requirements are increasingly offset by Software-as-a-Service (SaaS) and cloud rendering subscriptions.

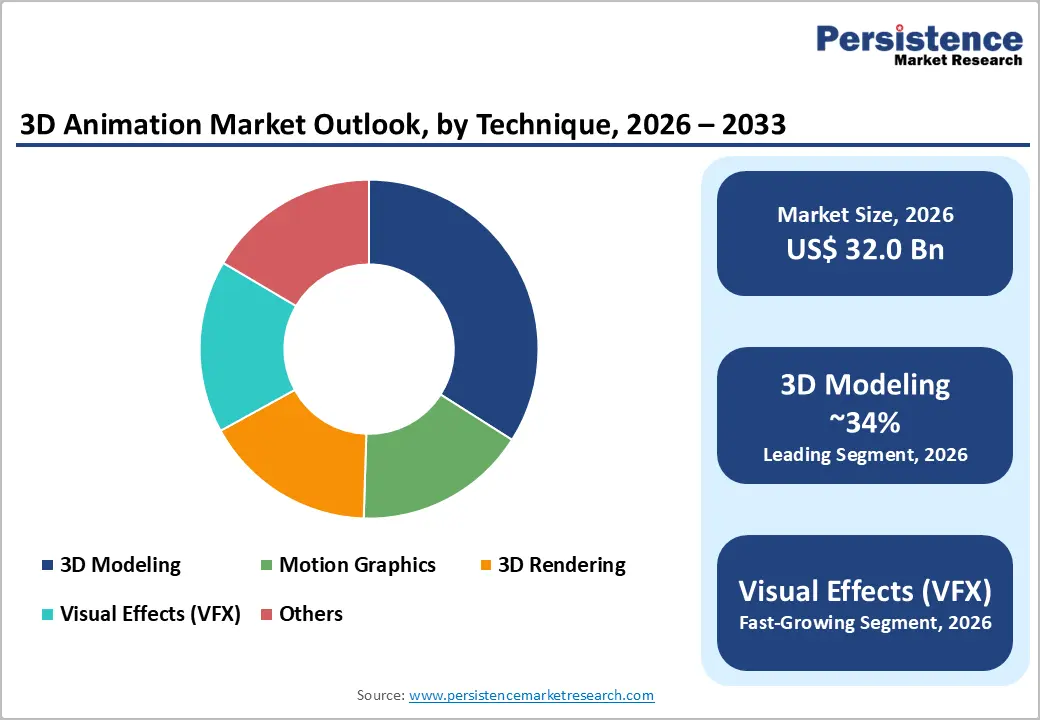

Technique Insights

The 3D Modeling segment leads the technique category, capturing approximately 34% of the 3D Animation market revenue share. 3D modeling forms the foundational layer of virtually all animation pipelines, from feature films and video games to architectural visualization and product design, making it an indispensable and high-frequency procurement area for studios and enterprises.

The segment's dominance reflects the breadth of industries relying on precise and detailed 3D models as the primary deliverable. However, the Visual Effects (VFX) segment is the fastest-growing technique, with a projected CAGR of 14.8% between 2026 and 2033, propelled by rising consumer expectations for photorealistic content in blockbuster films, episodic streaming series, and live sports broadcast enhancements.

Deployment Insights

The On-Demand (cloud-based) deployment segment is the largest as well as the fastest-growing deployment mode within the 3D Animation market, registering a 65% market share and CAGR of 12.2%, steadily gaining share against the traditional On-Premise segment. Cloud delivery platforms allow animation studios, particularly small and mid-sized enterprises, to access scalable rendering capacity, collaborative workflow tools, and large-format asset storage without the capital expenditure of maintaining on-premise infrastructure.

The adoption is supported by improved cloud delivery mechanisms that automate content processing once a creator uploads a project file. Large providers, including Adobe (via Creative Cloud) and various third-party cloud rendering farms, have further legitimized this shift. Despite some persistent challenges around data transfer latency, security, and proprietary software compatibility, the overarching trend favors cloud delivery as studios seek to support geographically distributed teams and reduce total cost of ownership.

End-user Insights

The Media & Entertainment segment is the dominant end-use vertical for 3D animation, accounting for approximately 35% of global market revenue, a leadership position that is expected to persist throughout the forecast period. This dominance reflects the scale and variety of animated content demanded across theatrical films, episodic television, streaming platforms, and advertising. According to the U.S. Bureau of Economic Analysis (BEA), animated content plays a key role in the U.S. film and television industries' combined economic contribution of over US$ 200 billion.

Major studios, including Walt Disney Animation Studios, DreamWorks Animation LLC, and Framestore, are continuously expanding their production slates. The Gaming & Interactive Media segment is the fastest-growing end-use vertical, powered by surging investment in console, PC, and mobile gaming, as well as the development of eSports content. The Healthcare & Life Sciences and Education & Academics verticals are also registering rapid growth.

Regional Insights

North America 3D Animation Market Trends & Analysis

North America holds the largest regional share in the global 3D Animation market, accounting for approximately 38% of total revenue in 2025. The region's dominance is anchored by the concentration of the world's most influential animation studios, including Walt Disney Animation Studios, DreamWorks Animation LLC, Pixar Animation Studios, Industrial Light & Magic, and Framestore, alongside a mature ecosystem of software developers such as Autodesk Inc., Adobe Inc., and Side Effects Software Inc.

U.S. 3D Animation Market Size

The United States is the single largest national market for 3D animation, contributing the 85% market share of North America's regional share. The country is home to Hollywood's global animation supply chain, spanning studios and software developers, and benefits from institutional investment by major streaming platforms in original animated content. Netflix, Disney+, and Amazon Prime Video are collectively commissioning billions of dollars of animated programming annually, creating durable domestic demand.

Europe 3D Animation Market Trends, Drivers, & Insights

Europe is the second-largest regional market for 3D animation, with 29% market share, characterized by a diverse ecosystem spanning large-scale production studios, specialized VFX boutiques, and world-class academic institutions. The region benefits from strong public broadcasting mandates and government support for domestic content production, with the European Union's Creative Europe program specifically funding audiovisual and animation co-productions across member states.

Germany 3D Animation Market Size

Germany is Europe's leading national market for 3D animation in industrial applications, with 27% regional market share, demanding significantly from its automotive sector, home to manufacturers such as BMW, Volkswagen, and Daimler. In January 2023, BMW Welt in Munich deployed an AI-powered 3D facial animation installation at its museum, illustrating the sector's appetite for experiential animation solutions.

U.K. 3D Animation Market Size

The United Kingdom is one of Europe's most vibrant centers of 3D animation and VFX production, with 21% market share, home to world-renowned studios including Framestore, the recipient of multiple Academy Awards for visual effects. The U.K.'s strong university system, with institutions like Bournemouth University's National Centre for Computer Animation, supplies a steady pipeline of trained animators and technical directors.

France 3D Animation Market Size

France is a significant European market for 3D animation, with 17% market share, supported by robust public funding through the Centre national du cinéma et de l'image animée (CNC), which subsidizes domestic animation co-productions and distributes television animation grants. France has historically been a leader in animated feature film production, with studios producing internationally distributed content.

Asia Pacific 3D Animation Market Drivers & Analysis

Asia Pacific is the fastest-growing regional market for 3D animation, with a projected CAGR of approximately 14.4% through 2033, outpacing all other geographies. Japan's globally influential anime industry, which commands a multi-billion-dollar international licensing and merchandise market, represents a structural pillar of regional demand.

China 3D Animation Market Size

China represents the largest single national market in the Asia Pacific for 3D animation, with 34% market share, driven by government support for domestic cultural industries and a massive consumer base with an appetite for animated entertainment. Mobile gaming and 3D animation-integrated interactive experiences are generating incremental demand among younger demographics.

India 3D Animation Market Size

India is one of the fastest-growing markets for 3D animation within the Asia Pacific, with 21% market share, functioning simultaneously as a significant consumer market and a major outsourcing destination for global studios. The country's animation and VFX sector has benefited from government-backed skill development programs and the establishment of dedicated animation clusters in cities such as Mumbai, Hyderabad, and Bengaluru.

Japan 3D Animation Market Size

Japan occupies a unique and influential position in the global 3D animation market, with 31% market share, anchored by its iconic anime industry, which generated exports worth hundreds of billions of yen and commands a dedicated global fanbase. Japanese animation studios are increasingly integrating 3D computer-generated imagery (CGI) techniques alongside traditional 2D animation to enhance visual quality and production efficiency.

Competitive Landscape

The global 3D Animation market exhibits a fragmented yet consolidating competitive structure, characterized by a mix of large, diversified technology companies, specialized animation software vendors, and vertically integrated entertainment studios. Market leaders, including Autodesk Inc., Adobe Inc., and NVIDIA Corporation, command significant software and hardware revenue shares, leveraging deep product ecosystems, global distribution networks, and substantial R&D investment to sustain competitive moats. Smaller boutique studios differentiate through creative specialization, regional relationships, and niche end-market expertise, particularly in healthcare visualization and architectural animation.

Key Developments

- March 2026: Autodesk announced the launch of its Wonder 3D generative AI model within Autodesk Flow Studio, aimed at significantly accelerating 3D content creation in the animation and VFX ecosystem. The new AI model enables creators to convert text prompts and 2D images into fully editable 3D characters and objects, reducing the complexity and time traditionally associated with 3D modeling workflows.

- March 2026: Adobe Inc. and NVIDIA Corporation announced a strategic partnership to accelerate AI-powered content creation, 3D workflows, and marketing automation in the 3D animation and creative software. The collaboration focuses on developing the next generation of Adobe Firefly generative AI models using NVIDIA’s advanced computing technologies, including CUDA-X and NeMo libraries, enabling higher precision, control, and scalability in creative workflows.

- April 2026: Adobe Inc. announced the launch of its new Creative Agent, introduced through the Firefly AI Assistant, marking a major shift toward agentic AI-driven workflows in the 3D animation and creative software market. The Creative Agent enables users to describe desired outcomes in natural language, after which the AI orchestrates and executes complex, multi-step tasks across Adobe’s Creative Cloud applications such as Photoshop, Premiere Pro, and Illustrator, eliminating the need for manual tool navigation.

Top Companies in 3D Animation Market

Autodesk Inc. (San Rafael, U.S.) is the market's most influential software provider, with its flagship Maya and 3ds Max platforms serving as the industry standard for professional 3D animation and visual effects production worldwide. Autodesk's Media & Entertainment Collection bundles animation, simulation, and pipeline management tools, generating substantial recurring subscription revenue.

Adobe Inc. (San Jose, U.S.) occupies a critical position in the 3D animation ecosystem through its Creative Cloud suite, particularly Adobe After Effects and Adobe Substance 3D, which are widely adopted for motion graphics, compositing, and photorealistic material creation. In 2024, Adobe integrated real-time rendering capabilities into its Creative Cloud, reported to reduce animation production timelines by approximately 28%.

NVIDIA Corporation (Santa Clara, U.S.) plays a foundational role in the 3D animation market through its GPU hardware and software platforms, particularly the Omniverse collaborative simulation platform and the RTX rendering architecture, which underpin real-time rendering and AI-accelerated animation workflows across the industry.

Global 3D Animation Market Report – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 17.9 Bn |

|

Current Market Value (2026) |

US$ 32.0 Bn |

|

Projected Market Value (2033) |

US$ 69.4 Bn |

|

CAGR (2026–2033) |

11.7% |

|

Leading Region |

North America, ~39–40% |

|

Dominant Segment |

Software (Component), ~54% |

|

Top-ranking Segment (Technique) |

3D Modeling, ~34% |

|

Incremental Opportunity (2026–2033) |

~US$ 37.4 Bn |

Companies Covered in 3D Animation Market

- Autodesk Inc.

- Adobe Inc.

- NVIDIA Corporation

- Maxon Computer GmbH

- Toon Boom Animation Inc.

- Walt Disney Animation Studios

- DreamWorks Animation LLC

- Framestore

- Side Effects Software Inc.

- Corel Corporation

- Zco Corporation

- Corus Entertainment Inc.

Frequently Asked Questions

The global 3D Animation market is valued at US$ 32.0 Bn in 2026 and is projected to reach US$ 69.4 Bn by 2033, expanding at a CAGR of 11.7% during the forecast period.

The key drivers include the surging demand for high-quality animated content on OTT streaming platforms such as Netflix and Disney+, the rapid integration of artificial intelligence (AI) and real-time rendering technologies into animation workflows, expanding cross-industry adoption in healthcare, architecture, and education, and the emergence of immersive metaverse and AR/VR content ecosystems.

The 3D Modeling segment is the leading technique segment, accounting for approximately 34% of market revenue. Its dominance reflects its foundational role across all animation pipelines, from film and gaming to architectural visualization. The Visual Effects (VFX) segment is the fastest-growing technique, projected to grow at a CAGR of 14.8% through 2033.

North America is the leading regional market, accounting for approximately 38% of global 3D Animation revenue in 2025. The region's dominance is driven by the presence of world-class studios, including Walt Disney Animation Studios, DreamWorks Animation LLC, and Framestore, along with a mature software ecosystem led by Autodesk Inc. and Adobe Inc. Asia Pacific is the fastest-growing region.

The most compelling emerging opportunity lies at the intersection of 3D animation and the healthcare & life sciences sector, coupled with the development of metaverse and immersive reality platforms. Medical simulation, surgical training, and VR-based patient education are generating high-margin demand, while platform investments by companies such as Meta Platforms and the emergence of AI-powered 3D world-generation tools are creating new content commissioning pipelines at scale.