- Beverages

- Wine Vinegar Market

Wine Vinegar Market Size, Share, and Growth Forecast 2026 - 2033

Wine Vinegar Market by Product Type (Red Wine Vinegar, White Wine Vinegar, Sherry Vinegar, Champagne Vinegar, Others), Nature (Organic, Conventional), Application (Food & Beverages, Household, Healthcare, Others), Distribution Channel (Supermarkets/Hypermarkets, Convenience Stores, Specialty Stores, Online Retail, Others), by Regional Analysis, 2026 - 2033

Wine Vinegar Market Share and Trends Analysis

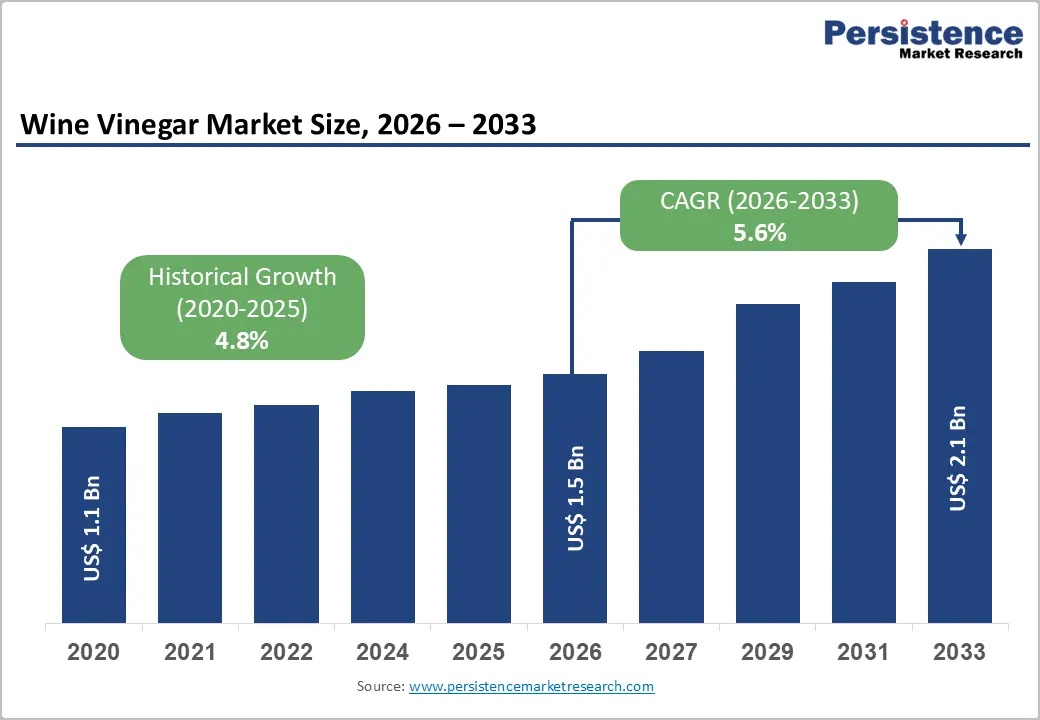

The global Wine Vinegar market size is expected to be valued at US$ 1.5 billion in 2026 and projected to reach US$ 2.1 billion by 2033, growing at a CAGR of 5.6% between 2026 and 2033. This is propelled by accelerating consumer preference for natural, fermented condiments aligned with the global health and wellness movement, rising culinary sophistication, particularly in North America and Europe, and the rapid penetration of premium specialty vinegar varieties across organised retail and foodservice channels.

The Food and Agriculture Organization (FAO) reports sustained global growth in fermented food and condiment consumption, while the proliferation of Mediterranean-inspired diets and artisanal cooking culture further augments demand for quality wine vinegars across both developed and emerging markets.

Key Industry Highlights

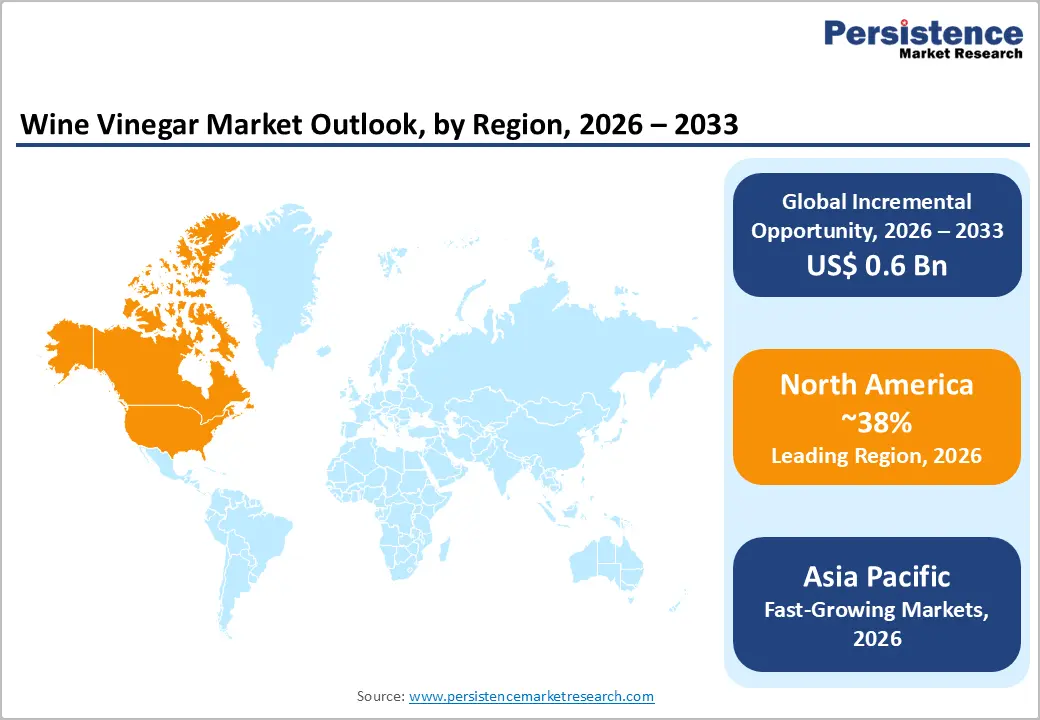

- Leading Region – North America dominates the global wine vinegar market with approximately 38% revenue share in 2025, driven by high condiment consumption, premium food culture, Mediterranean cuisine adoption, and robust organic product demand across U.S. retail channels.

- Fastest Growing Region – Asia Pacific is the fastest-growing regional market, fuelled by rapid urbanisation, rising disposable incomes in China and India, expanding foodservice infrastructure, and accelerating e-commerce penetration, driving demand for premium imported condiments.

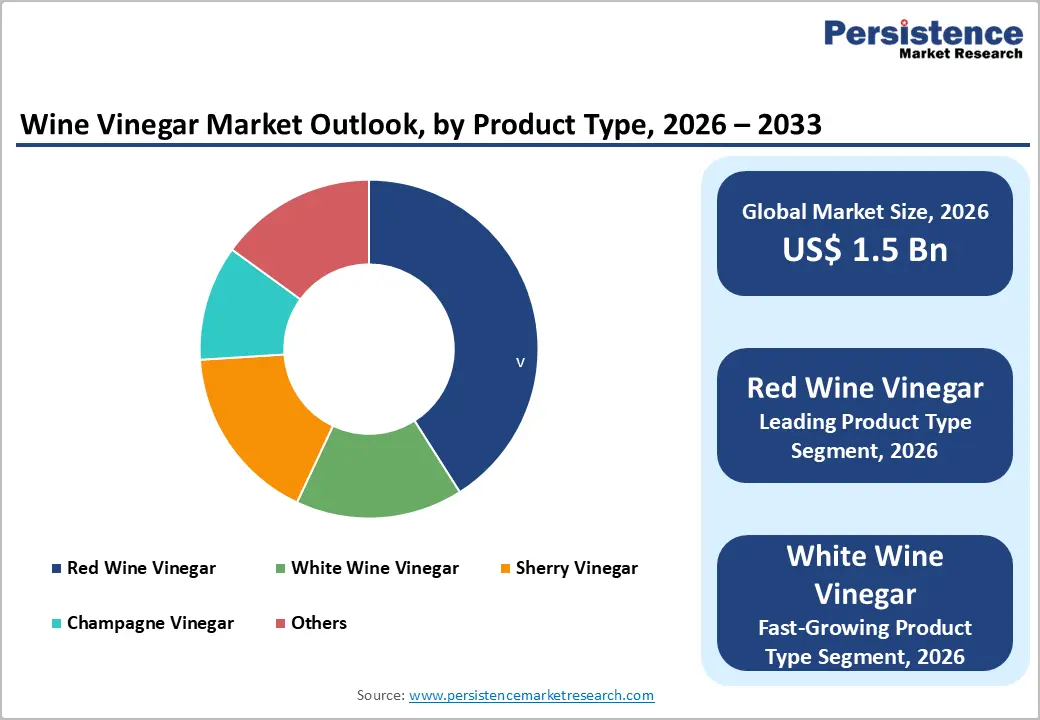

- Dominant Product Segment – Red wine vinegar leads the product type segment with approximately 41% market share in 2025, underpinned by its deep culinary heritage in European and North American cuisines, robust polyphenol content, and strong premium positioning through geographic certifications.

- Fastest Growing Product Segment – White wine vinegar is the fast-growing product type segment, while the organic nature sub-segment records the strongest CAGR, supported by clean-label consumer trends, EU organic policy frameworks, and expanding health-focused retail formats.

- Key Opportunity – The penetration of E-commerce presents significant opportunities in the Asia Pacific, with China's online food sales growing at over 20% annually and U.S. organic condiment sales reaching US$ 67.6 billion across all food categories.

Market Dynamics

Drivers - Health and Wellness Trends Driving Demand for Fermented Condiments

The global pivot toward functional foods and naturally fermented products is a powerful structural driver for the wine vinegar market. Wine vinegar, particularly unfiltered and organic variants, contains acetic acid, polyphenols, and antioxidants that have been associated with glycaemic regulation, digestive health, and cardiovascular support in peer-reviewed literature. The World Health Organization (WHO) has consistently promoted dietary patterns rich in fermented foods, and consumer awareness of these benefits has grown markedly.

A 2023 IFIC Food & Health Survey found that over 54% of U.S. consumers actively seek fermented or cultured food products. This awareness is translating into elevated retail demand for premium wine vinegars, notably red wine and sherry variants, which are perceived as superior to refined synthetic acetic acid-based alternatives.

Expansion of the Foodservice Industry and Mediterranean Cuisine Adoption

The global foodservice sector's resurgence post-pandemic has created sustained institutional demand for wine vinegar as a culinary essential. The National Restaurant Association reported that U.S. restaurant industry revenues exceeded US$ 1.1 trillion in 2024, with Mediterranean and European cuisine formats among the fastest-growing menu categories.

Wine vinegar is a foundational ingredient in vinaigrettes, marinades, braised preparations, and classical European sauces, ensuring consistent offtake across hotels, restaurants, and catering operations. In Europe, the HORECA (hotel, restaurant, catering) channel accounts for a significant share of specialty vinegar consumption, particularly in France, Italy, and Spain, where culinary traditions mandate quality-grade wine vinegars in professional kitchens.

Restraints - Price Sensitivity and Competition from Alternative Vinegar Varieties

Wine vinegar commands a price premium relative to distilled white vinegar and apple cider vinegar, which limits adoption among cost-sensitive consumer segments and in price-competitive retail environments. In emerging markets, where per-capita disposable income remains constrained, lower-cost alternatives, particularly synthetic acetic acid solutions continue to dominate household usage. According to FAO data, synthetic acetic acid production accounts for over 75% of global vinegar supply by volume, demonstrating the competitive pressure wine vinegar producers face in volume-driven channels. This pricing gap suppresses mass-market penetration and confines wine vinegar consumption largely to premium retail tiers and professional foodservice applications.

Raw Material Supply Vulnerability Linked to Wine Industry Dynamics

Wine vinegar production is intrinsically tied to the availability and pricing of wine and grape must, making producers susceptible to upstream supply chain disruptions. Fluctuations in European wine harvests driven by climate variability, disease pressure such as the Xylella fastidiosa pathogen affecting Southern European vineyards, and shifting EU wine production quotas can materially impact raw material availability and cost structures. The International Organisation of Vine and Wine (OIV) reported a 7% decline in global wine production in 2023 due to adverse weather conditions, directly affecting the feedstock economics of wine vinegar manufacturers across France, Italy, and Spain.

Opportunities - Organic Wine Vinegar – Capitalising on Clean Label and Sustainability Trends

The organic segment presents a compelling revenue expansion opportunity for wine vinegar market participants. Consumer demand for clean-label, additive-free, and sustainably produced condiments is rising sharply across North America and Europe. The Organic Trade Association (OTA) reported that U.S. organic food sales reached US$ 67.6 billion in 2023, with condiments and sauces among the fastest-growing organic subcategories. Similarly, Eurostat data indicate that organic farmland in the EU grew by 5.7% in 2023, with dedicated organic vinegar production facilities proliferating in France and Italy. Companies investing in USDA Organic, EU Organic Regulation (EU) 2018/848-compliant production and transparent provenance labelling are well-positioned to capture outsized margin premiums, particularly through e-commerce and specialty retail channels.

Category-wise Analysis

Product Type Insights

Red wine vinegar leads the global wine vinegar market by product type, accounting for approximately 41% of total market share in 2025. Its dominance is rooted in its deep culinary heritage across Europe and North America, where it is a staple ingredient in vinaigrettes, marinades, sauces, and pickling preparations. Red wine vinegar's robust flavour profile, attributed to its polyphenol and anthocyanin content derived from red grape varieties, aligns with consumer preferences for full-bodied, complex condiment flavours.

Acetum S.p.A. and De Nigris, among the leading Italian producers, have invested in aged red wine vinegar lines with IGP (Indicazione Geografica Protetta) certification, reinforcing premiumisation. White wine vinegar is the fast-growing sub-segment to gain traction for its versatility in lighter culinary applications and growing preference in Asian markets.

Nature Insights

Conventional wine vinegar holds the dominant share in the nature segment, representing approximately 76% of total market revenue in 2025. The prevalence of conventional variants reflects established production infrastructure, competitive pricing at the retail level, and longstanding brand loyalty among mainstream consumers and foodservice operators.

Major brands, including Mizkan Holdings, Carl Kühne KG, and Pompeian, Inc. continue to distribute high-volume conventional wine vinegar through hypermarket and supermarket chains globally. Nevertheless, the organic segment is the fastest-growing nature category, with health-conscious consumers increasingly seeking products free from synthetic additives and aligned with sustainability values. Growth in certified organic wine vinegar is particularly strong in Germany, France, and the U.S., where regulatory clarity around organic certification, including USDA NOP and EU Organic Regulation standards, underpins consumer trust.

Application Insights

The food & beverages is the dominant application category, accounting for an estimated 68% of total Wine Vinegar market revenue in 2025. Wine vinegar's essential role as a culinary condiment deployed in dressings, sauces, pickling, braising, and reduction preparations ensures consistent and structurally durable demand across both household and professional food preparation contexts. The European Commission's Regulation (EC) No 110/2008 and food additive frameworks recognise wine vinegar as a traditional, naturally produced ingredient, reinforcing its preference over synthetic acidulants in EU-regulated food formulations.

The healthcare application is an emerging and fast-growing sub-segment, with vinegar-based functional health products gaining shelf space in pharmacies and health food stores, particularly in North America and Japan, driven by evidence of acetic acid's metabolic health benefits.

Distribution Channel Insights

Supermarkets and Hypermarkets represent the leading distribution channel for wine vinegar globally, accounting for approximately 48% of total retail sales in 2025. The dominance of organised retail is a reflection of high household grocery consolidation in North America and Western Europe, where multinational chains such as Walmart, Carrefour, Tesco, and Kroger offer extensive condiment assortments with both national brands and private-label options. However, online retail is the fastest-growing channel, with global e-commerce food and beverage sales expanding rapidly post-pandemic.

Specialty stores are also gaining relevance, particularly for premium aged, organic, and single-origin wine vinegar variants that command higher price points and require informed consumer engagement. Fleischmann's Vinegar and Rex Wine Vinegar Company have expanded digital commerce initiatives to capture growing online consumer demand.

Regional Insights

North America Wine Vinegar Market Trends and Insights

North America leads the global Wine Vinegar market, holding approximately 38% of the total revenue share in 2025. The region's dominance is underpinned by high per-capita condiment consumption, a thriving premium food culture, the proliferation of Mediterranean and European cuisine formats, and robust organic product adoption across U.S. natural and specialty retail channels. E-commerce growth is further amplifying premium wine vinegar accessibility.

U.S. Wine Vinegar Market Size

The U.S. accounts for the majority of North America's wine vinegar revenues, representing approximately 82–84% of the regional market in 2025. Strong consumer demand for organic, non-GMO, and artisanal condiments supported by a retail landscape featuring dedicated natural food retailers such as Whole Foods Market and Sprouts, drives consistent premium product offtake. Brands including Pompeian, Inc. and Fleischmann's Vinegar maintain a strong shelf presence nationally.

Europe Wine Vinegar Market Trends and Insights

Europe represents the second-largest regional market for wine vinegar, characterised by deep-rooted culinary traditions, stringent EU food quality regulations, and a rich heritage of geographical indication-protected wine vinegar production. Growing demand for organic and aged specialty variants, combined with a strong HORECA sector, sustains consistent volume and value growth across the region's mature and premium market segments.

Germany Wine Vinegar Market Size

Germany is among the largest wine vinegar markets in Europe, accounting for an estimated 18–20% of Europe revenue share. Strong demand for premium organic variants, a well-developed specialty food retail ecosystem, and high consumer health consciousness drive consistent growth. Carl Kühne KG, headquartered in Hamburg, maintains significant domestic market leadership through extensive supermarket distribution and a broad product portfolio.

U.K. Wine Vinegar Market Size

The U.K. wine vinegar market is driven by growing interest in Mediterranean cooking, clean-label condiment preferences, and expanding availability of imported European specialty vinegars through online and specialty retail channels. The U.K. contributes approximately 12–14% of total European market revenues. Aspall Cyder Limited, a premium British heritage brand, plays a significant role in the domestic premium vinegar segment alongside imported brands.

France Wine Vinegar Market Size

France holds a structurally important position in both wine and vinegar production and consumption within Europe. The country's centuries-old vinegar-making tradition, exemplified by Orléans-method wine vinegar bearing IGP status, sustains a premium domestic market. France accounts for approximately 15–17% of European regional revenues, with strong demand from professional culinary channels and premium retail driven by Charbonneaux-Brabant and other regional producers.

Asia Pacific Wine Vinegar Market Trends and Insights

Asia Pacific is the fastest-growing regional market for wine vinegar, driven by rapid urbanisation, rising disposable incomes, and the westernisation of food habits across China, India, Japan, and Southeast Asia. China is the dominant country market, with increasing premium condiment imports distributed through Tmall and JD.com. Foodservice chain expansion and the growth of European-style bistros and restaurants are contributing to rising wine vinegar demand across the region.

India Wine Vinegar Market Size

India represents a nascent but fast-emerging wine vinegar market, driven by the expanding urban middle class, rising interest in international cuisines, and growth in modern organized retail. India contributes an estimated 4–5% of Asia Pacific regional revenues in 2025. Growth is concentrated in metropolitan centres including Mumbai, Delhi, and Bengaluru, where premium hypermarkets and e-commerce platforms drive imported specialty condiment sales.

Japan Wine Vinegar Market Size

Japan is a structurally important Asia Pacific market for wine vinegar, accounting for approximately 18–20% of regional revenues. Japanese consumers exhibit a sophisticated appreciation for fermented condiments, and wine vinegar is well integrated into Western-influenced cuisine segments. The country's premium food retail sector, including chains such as Kinokuniya and Dean & DeLuca Japan, supports consistent premium product offtake and steady volume growth.

Southeast Asia Wine Vinegar Market Size

Southeast Asia is an emerging growth frontier for wine vinegar, with increasing urbanisation, expanding hotel and restaurant infrastructure, and growing exposure to European culinary traditions. The sub-region encompassing Thailand, Vietnam, Indonesia, and Malaysia accounts for approximately 10–12% of Asia Pacific regional revenues. The HORECA sector and upscale retail formats are primary demand drivers, with import volumes growing steadily through organised regional distribution networks.

Competitive Landscape

The wine vinegar market is highly competitive, with manufacturers focusing on product quality, premiumization, and regional flavor preferences to strengthen their market position. Companies are expanding organic and naturally fermented product lines to meet rising consumer demand for clean-label and health-oriented ingredients. Innovation in flavored variants, sustainable packaging, and premium gourmet offerings is helping brands attract both retail and foodservice customers. Strategic partnerships with supermarkets, specialty stores, and online platforms are improving product accessibility.

Key Developments

- In June 2025, O Olive Oil & Vinegar launched the first California-certified organic extra virgin olive oil (EVOO) in a chef-style squeeze bottle, designed for both professional chefs and home kitchens. The company also introduced a California Premium EVOO in the same BPA-free, recyclable squeeze bottle format to improve convenience, precision, and ease of use.

- In June 2025, American Vinegar Works launched a new food-service product line developed exclusively for professional kitchens. The range included seven of its most popular barrel-aged vinegars, such as Ultimate Red Wine Vinegar, California Junmai Sake Rice Wine Vinegar, and Barrel-Aged Honey Wine Vinegar.

Global Wine Vinegar Market - Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 1.1 Billion |

|

Current Market Value (2026) |

US$ 1.5 Billion |

|

Projected Market Value (2033) |

US$ 2.1 Billion |

|

CAGR (2026–2033) |

5.6% |

|

Leading Region |

North America, 38% market share (2025) |

|

Dominant Category (Product Type) |

Red Wine Vinegar, ~41% market share (2025) |

|

Top-ranking Category (Nature) |

Conventional Wine Vinegar, ~76% market share (2025) |

|

Incremental Opportunity |

US$ 0.6 Billion (2026–2033) |

Companies Covered in Wine Vinegar Market

- Mizkan Holdings Co., Ltd.

- Carl Kühne KG

- Acetum S.p.A.

- De Nigris

- Burg Group B.V.

- Aspall Cyder Limited

- Pompeian, Inc.

- Charbonneaux-Brabant

- Australian Vinegar

- Acetificio Galletti

- Fleischmann’s Vinegar Company, Inc.

- Rex Wine Vinegar Company

- Classic Wine Vinegar

Frequently Asked Questions

The global wine vinegar market is estimated to be valued at US$ 1.5 billion in 2026.

Primary demand drivers include the global health and wellness movement promoting fermented and functional foods, the resurgence of the foodservice industry with strong appetite for Mediterranean and European cuisine formats, and rising consumer preference for natural, clean-label condiments.

North America is the leading region in the global Wine Vinegar market, accounting for approximately 38% of total revenue in 2025.

Growth opportunities lie in organic wine vinegar product development aligned with U.S. and EU organic certification frameworks and clean-label consumer demand and in Asia Pacific e-commerce penetration, particularly in China, where online food sales are growing at over 20% annually.

The leading companies operating in the global Wine Vinegar market include Mizkan Holdings Co., Ltd., Carl Kühne KG, Acetum S.p.A., De Nigris, Pompeian, Inc., Charbonneaux-Brabant, Aspall Cyder Limited, Fleischmann's Vinegar Company, Inc., and Rex Wine Vinegar Company, among others.