- Home Appliances

- Freezer, Beverage and Wine Cooler Market

Freezer, Beverage and Wine Cooler Market Size, Share, and Growth Forecast 2026 - 2033

Freezer, Beverage and Wine Cooler Market by Installation Type (Freestanding, Countertop, Built-In), by Bottle Capacity (Less than 10, 1 to 30, 31 to 50, 51 to 300, 301 and Above), by Door Type (4 Doors and Above Type, 3 Door Type, 2 Door Type, 1 Door Type), by End-user (Residential, Commercial), by Regional Analysis, 2026 - 2033

Freezer, Beverage and Wine Cooler Market Size and Trend Analysis

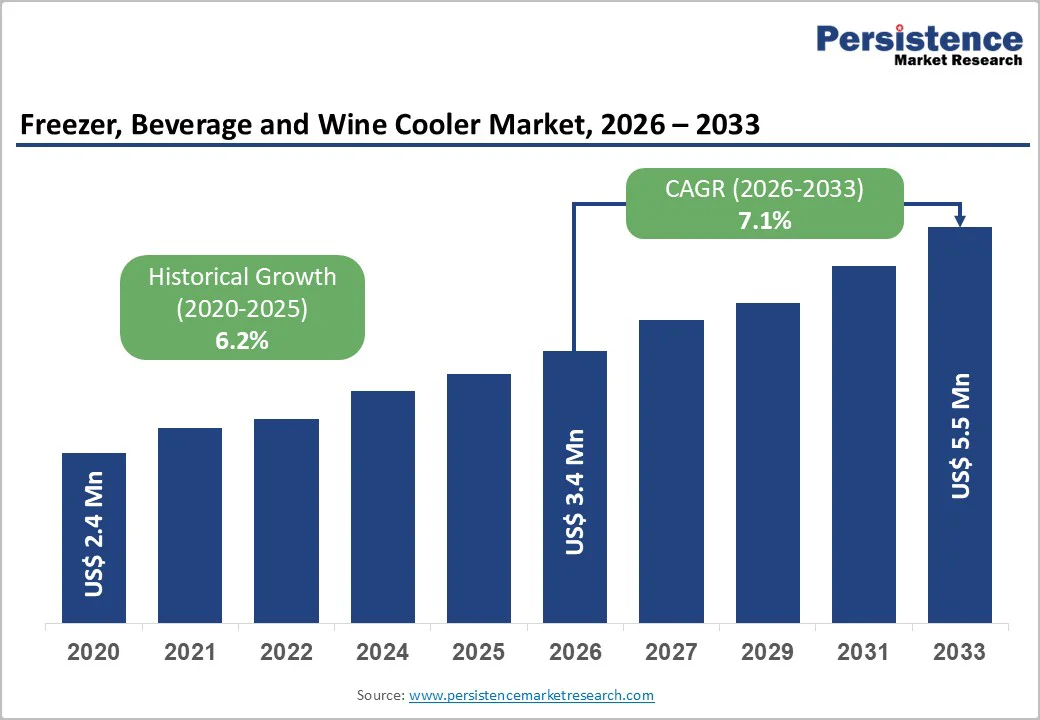

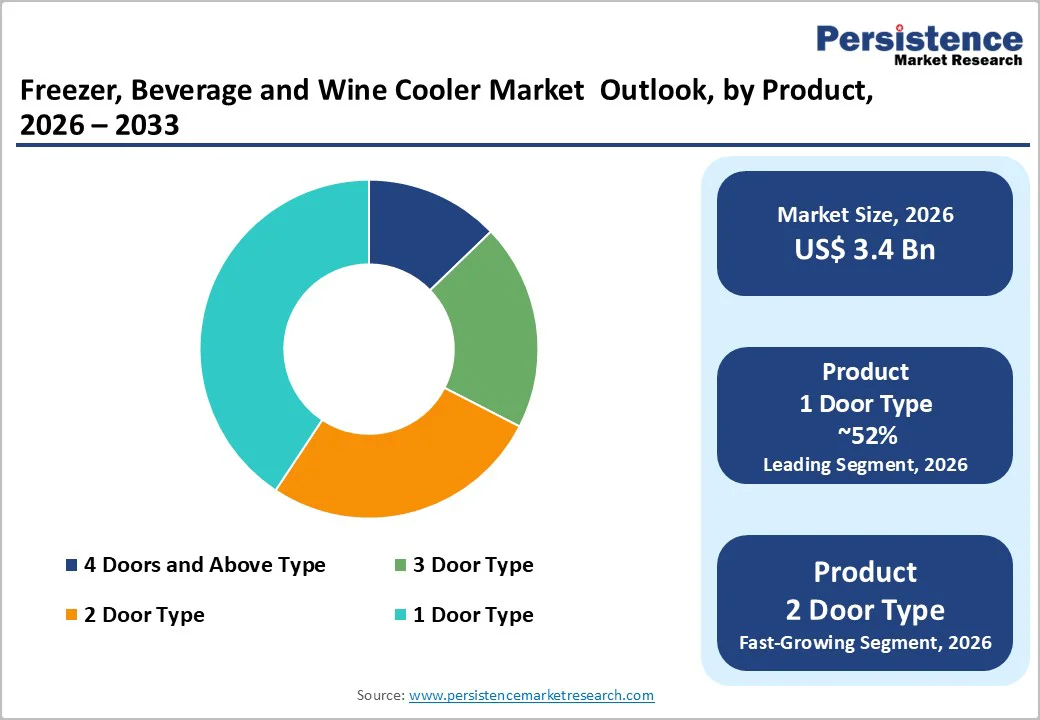

The global freezer, beverage, and wine cooler market size is projected to reach a value of US$ 3.4 billion by 2026, expanding further to US$ 5.5 billion by 2033 at a CAGR of 7.1% from 2026 to 2033.

Rise in consumer preference for premium kitchen appliances and the increasing integration of smart cooling technologies drive demand. Higher disposable incomes, particularly in emerging economies, are accelerating demand for specialized beverage and wine storage solutions as home entertainment and modern lifestyle habits evolve. Furthermore, regulatory shifts promoting energy-efficient refrigeration and the gradual phase-out of high-GWP refrigerants are encouraging manufacturers to innovate, strengthening market momentum and broadening the adoption of advanced cooling appliances.

Key Market Highlights

- Leading Region: North America leads the global market with a 34.2% share, supported by strong premium appliance demand, strict energy-efficiency regulations, and high smart-home adoption.

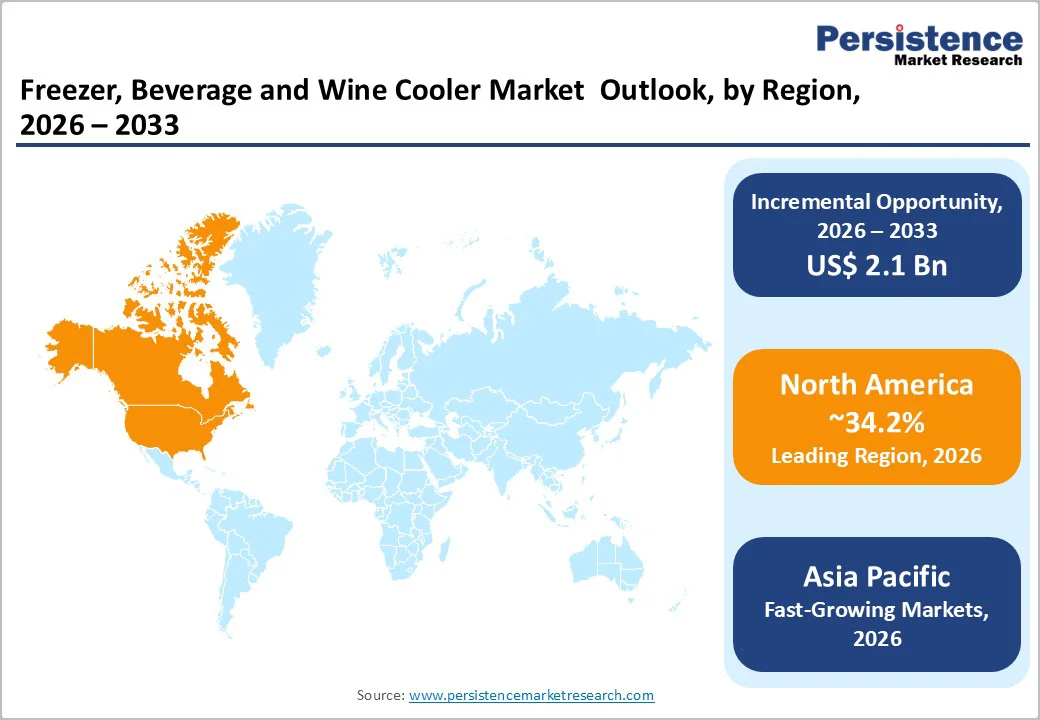

- Fastest-Growing Region: Asia Pacific holds a 31.1% share and is the fastest-growing region, driven by urbanization, rising incomes, and commercial refrigeration growth.

- Leading Category: Freestanding installation models dominate with a 58% market share, driven by affordability, easy installation, and broad applicability across homes and commercial settings.

- Fastest-Growing Category: 1–30 bottle capacity models lead growth at over 9% annually, supported by rising residential adoption among wine enthusiasts and home-entertainment users.

- Key Market Opportunity: Smart technology and energy-efficient, low-GWP systems remain key opportunities, enabling manufacturers to capture premium demand and regulatory-driven market segments.

| Key Insights | Details |

|---|---|

|

Freezer, Beverage and Wine Cooler Market Size (2026E) |

US$ 3.4 Billion |

|

Market Value Forecast (2033F) |

US$ 5.5 Billion |

|

Projected Growth CAGR(2026-2033) |

7.1% |

|

Historical Market Growth (2020-2025) |

6.2% |

Market Dynamics

Drivers - Rising Wine and Beverage Consumption Among Affluent Consumers

Global wine and premium beverage consumption is steadily increasing, fueled by shifting lifestyle preferences, expanding middle-class populations in Asia-Pacific and Latin America, and growing interest among younger demographics. In the United States alone, 42% of homeowners upgraded their kitchens in 2023, with wine coolers emerging among the top integrated appliance choices. The rise of wine culture, craft drinks, and home-entertainment habits is boosting demand for high-quality storage units that maintain ideal temperatures and safeguard flavor integrity.

Commercial spaces such as bars, restaurants, lounges, and hotels are also driving significant demand by adopting premium beverage coolers to preserve product quality and enhance customer experience. This growing adoption across the hospitality sector continues to create strong global opportunities for specialized cooling appliances.

Technological Innovation and Smart Appliance Integration

Manufacturers are increasingly embedding IoT connectivity, AI-driven controls, and mobile app integration into freezers, beverage coolers, and wine storage units. Smart coolers equipped with remote monitoring, automated temperature adjustment, humidity management, and predictive maintenance are gaining appeal among modern, tech-oriented consumers. These features help deliver precise environmental control, safeguard perishable beverages, and simplify daily operation.

Advancements such as energy-efficient compressors, improved insulation materials, and eco-friendly low-GWP refrigerants are aligning with global sustainability goals. These innovations not only reduce energy consumption and operational costs but also improve product performance and regulatory compliance, strengthening the competitiveness of premium and mid-range cooling appliance segments.

Restraints - Stringent Regulatory Requirements and Refrigerant Phase-Out Mandates

Environmental regulations across major regions are tightening rapidly, placing significant compliance pressure on freezer and beverage cooler manufacturers. The European Union’s F-Gas Regulation (EU) 2024/573, effective January 2025, enforces a near-total phase-out of high-GWP fluorinated gases, prohibiting the use of all F-gases in domestic refrigeration by 2026. Similarly, the U.S. Environmental Protection Agency (EPA), under the AIM Act, is mandating an 85% reduction in HFC production by 2036. These mandates require substantial R&D investments, product redesigns, and adoption of low-GWP refrigerants such as R290 and R600a.

As a result, manufacturers face increased production complexity, re-engineering costs, and long timelines for certification and testing. Smaller players, in particular, struggle with financial and technical barriers in aligning with evolving regulatory frameworks. The transition to sustainable refrigerants, though beneficial in the long term, continues to strain operational budgets and delays time-to-market for upgraded product lines.

High Initial Capital Expenditure and Raw Material Cost Volatility

Premium freezers, wine coolers, and beverage storage units especially built-in, large-capacity, and smart-connected models carry high upfront costs, restricting adoption among budget-conscious residential buyers and smaller commercial operators. The significant price gap between standard and advanced models creates a barrier to wider market penetration, particularly in emerging economies where affordability remains a key purchasing determinant.

Volatility in key raw materials such as copper, aluminum, steel, and specialized insulating polymers also contributes to unpredictable production expenses. Global supply chain disruptions driven by geopolitical tensions, trade restrictions, and rising logistics costs further amplify pricing instability. These challenges compel manufacturers to raise retail prices, potentially weakening demand in price-sensitive regions and tightening profit margins across the industry.

Opportunity - Rapid Urbanization and Middle-Class Expansion in Emerging Economies

Urbanization across Asia-Pacific and Africa is accelerating at an unprecedented pace, driving strong demand for modern refrigeration and specialized beverage storage units. Rapid economic growth in China, India, and Southeast Asia, along with Africa’s urban population expected to double from 700 million to 1.4 billion by 2050, is expanding the consumer base for premium home appliances. Rising disposable incomes and lifestyle upgrades are pushing households toward advanced cooling solutions that enhance convenience and food preservation.

At the same time, commercial refrigeration needs are intensifying across emerging markets. India’s commercial refrigeration sector, growing at a 3.3% CAGR, reflects rising investments in foodservice outlets, cloud kitchens, supermarkets, and e-commerce grocery fulfillment. This trend is driving significant demand for energy-efficient beverage coolers and compact freezers tailored for small and mid-sized commercial businesses seeking reliable, cost-effective, and technologically advanced cooling systems.

Energy-Efficient and Eco-Friendly Product Development Aligned with Sustainability Goals

Growing environmental awareness and sustainability-driven purchasing behavior are creating substantial opportunities for manufacturers of energy-efficient cooling appliances. Hospitality venues, retail chains, and foodservice establishments are increasingly adopting Energy Star-certified or low-energy models to reduce operating costs and meet corporate ESG commitments. This shift is motivating manufacturers to develop natural refrigerant-based, inverter-driven, and highly insulated cooling systems with superior efficiency and performance.

Companies pioneering green technologies are gaining a competitive advantage as regulatory bodies tighten energy-performance standards. The global energy-efficient beverage cooler market, valued at US$ 3.6 billion in 2024 and projected to reach US$ 7.2 billion by 2033 at an 8.1% CAGR, highlights the strong demand for sustainable cooling innovations. This momentum presents extensive growth potential for manufacturers investing in eco-friendly product lines and next-generation cooling architectures.

Category-wise Analysis

Installation Type Insights

Freestanding installation models dominate the freezer, beverage, and wine cooler market with nearly 58% share, driven by affordability, flexible placement, and ease of installation without requiring kitchen modifications. These units cater widely to both households and commercial buyers, offering generous storage capacity between 100 and 600 liters. Their plug-and-play nature, combined with minimal setup costs, makes them attractive to cost-conscious users, small restaurants, and retail environments requiring rapid deployment. This widespread utility keeps freestanding systems the most adopted installation format.

Built-in installation units are emerging as the fastest-growing category, supported by rising premium home renovation trends, aesthetic kitchen integration needs, and increasing demand for luxury appliances. Their flush-fit design, seamless cabinetry alignment, and higher-end finish appeal strongly to upscale households and hospitality spaces prioritizing modern minimalist interiors and noise-controlled operation.

Bottle Capacity Insights

The 1–30 bottle capacity segment leads the beverage and wine cooler market with about 45% share, reflecting strong acceptance among residential consumers, compact homes, and small entertainment spaces. This segment balances affordability, energy efficiency, and practicality, often becoming the first choice for beginners, casual wine drinkers, and modern urban households. Its space-saving design makes it suitable for apartments, small bars, and home entertainment setups where versatility and compactness are crucial. The segment’s broad appeal across millennials and young professionals further reinforces its leadership.

The 31–50 bottle capacity category is expanding the fastest as mid-range consumers upgrade to larger collections and hospitality venues seek moderate storage without transitioning to large commercial units. Growing interest in wine collecting, home bars, and premium kitchen appliances is accelerating demand for this capacity range.

Door Type Insights

Single-door units remain the leading door-type segment, accounting for roughly 52% share, supported by wide adoption across residential households, cafés, and small commercial environments. These models offer simplicity, low maintenance needs, and sufficient temperature consistency for beverage and food storage. Their compact footprint and lower upfront cost make them attractive for consumers seeking reliable cooling performance without advanced features. This segment continues to dominate due to the popularity of small-capacity and standard freezer and beverage cooler designs that meet everyday household requirements.

Two-door units are witnessing the fastest growth as demand rises for multi-zone cooling, larger storage volumes, and improved organization. Increasing consumer preference for dual-temperature functionality, especially among wine enthusiasts and premium kitchen users, is accelerating the adoption of these advanced configurations.

End-User Insights

The residential segment leads the freezer, beverage, and wine cooler market with nearly 64% share, driven by lifestyle upgrades, rising disposable incomes, and increased interest in premium home appliances. Young urban consumers and wine culture adoption are reinforcing demand for compact beverage coolers, freestanding freezers, and home-bar-friendly models. Residential buyers increasingly prefer appliances that combine aesthetics, convenience, and enhanced food preservation capabilities. This strong behavioral shift, coupled with modern kitchen remodeling trends, keeps the residential category the dominant market contributor.

The commercial segment is expanding the fastest, owing to rising installations across restaurants, supermarkets, hospitality chains, and pharmaceutical storage facilities. Growing regulatory compliance requirements, higher food safety standards, and demand for durable, high-capacity units are accelerating investment in commercial-grade cooling equipment.

Regional Insights

North America Freezer, Beverage, and Wine Cooler Market Trends

North America accounts for around 34.2% of the global freezer, beverage, and wine cooler market, supported by strong demand for premium refrigeration appliances and advanced smart-home adoption. The United States drives most of the regional volume, driven by high wine consumption, a mature home entertainment culture, and regulatory pressure encouraging the use of low-GWP refrigerants. EPA policies, Energy Star standards, and SNAP guidelines continue to reshape product innovation, pushing manufacturers toward sustainable, energy-efficient models. These structural advantages maintain North America’s leadership position.

Canada represents the fastest-growing country in the region, supported by increasing investments in modern foodservice infrastructure and rising adoption of energy-efficient refrigeration. Strict food safety regulations and expanding commercial refrigeration needs across retail and healthcare are accelerating demand for technologically advanced cooling systems.

Europe Freezer, Beverage, and Wine Cooler Market Trends

Europe exhibits steady expansion at a CAGR of about 7.4%, driven by stringent environmental regulations, strong wine culture, and widespread preference for premium, energy-efficient cooling appliances. Germany, France, the UK, and Spain remain the largest markets, supported by well-established hospitality sectors and a highly mature consumer base. The newly implemented EU F-Gas Regulation encourages transition to natural refrigerants and low-GWP technologies, strengthening demand for compliant, eco-friendly cooling systems across residential and commercial applications.

Smart wine coolers represent the region’s fastest-growing category, supported by rising demand for IoT-enabled temperature control, multi-zone cooling, and high-end kitchen integration. Europe’s focus on circular economy principles and sustainability is accelerating innovations in insulation, compressor efficiency, and recyclable appliance design.

Asia Pacific Freezer, Beverage, and Wine Cooler Market Trends

Asia Pacific captures approximately 31.1% of the global market, making it one of the largest and fastest-growing regions. Rapid urbanization, middle-class expansion, and rising disposable incomes across China, India, Japan, and Southeast Asia are significantly accelerating appliance adoption. China and Japan lead with mature smart refrigeration demand, while India records the strongest growth momentum due to rising household incomes and nationwide retail modernization. Manufacturers such as Haier, Midea, and Hisense continue to strengthen their production footprint and supply-chain dominance in the region.

Commercial refrigeration is expanding the fastest, driven by the rapid growth of foodservice establishments, modern retail formats, and cloud kitchen ecosystems. Government initiatives promoting energy-efficient appliances and eco-friendly refrigerants are further boosting the adoption of advanced refrigeration technologies across the region.

Competitive Landscape

The freezer, beverage, and wine cooler market reflects moderate concentration, shaped by strong product differentiation, broad distribution reach, and continuous innovation in smart connectivity and energy-efficient technologies. Competition spans premium, mid-range, and value segments, with brands focusing on advanced features, design flexibility, and regulatory compliance to strengthen positioning.

Emerging and regional players intensify competition by emphasizing affordability, localized features, and service accessibility. Key differentiators include smart-home integration, energy-efficiency performance, warranty depth, after-sales service networks, and sustainability commitments aligned with evolving environmental standards. These factors collectively define competitive advantage and influence purchasing decisions across residential and commercial end-users.

Key Market Developments:

- In July 2025, Market Expansion Initiative Midea signed as the official sponsor of the 2025 Africa Cup of Nations, advancing its expansion strategy across the Middle East and Africa region. The company established manufacturing facilities in Egypt for refrigerator production, scheduled for November 2025 launch, complementing existing operations in dishwashers and washing machines, demonstrating a strategic commitment to emerging market development.

- In January 2025, the Environmental Compliance Regulation (EU) 2024/573 F-Gas Regulation entered into force, mandating the prohibition of all F-gases in domestic refrigerators and freezers by 2026, compelling manufacturers globally to accelerate transition to natural refrigerants (R290, R600a) and low-GWP alternative technologies, reshaping competitive dynamics and investment priorities.

- In May 2024, Technological Innovation GE Appliances achieved 19 prestigious industry awards during 2024, including triple crown recognition at CES 2024, driven by revolutionary AI-enabled appliances, smart indoor smoking technology, and Energy Star certification across 95% of new product launches, reinforcing technological leadership and premium market positioning.

Companies Covered in Freezer, Beverage and Wine Cooler Market

- Whirlpool

- Bosch

- Haier

- LG

- Samsung

- Liebherr

- Sub-Zero/Wolf

- U-Line

- Vinotemp

- Danby

- NewAir

- Frigidaire

- Midea

- GE Appliances

- Haier-Hisense

Frequently Asked Questions

The market is expected to grow from US$ 3.4 Billion in 2026 to US$ 5.5 Billion by 2033, registering a 7.1% CAGR during the forecast period.

Demand is driven by rising wine and beverage consumption, rapid smart-home adoption, middle-class expansion in emerging markets, and regulatory pressure for energy-efficient, low-GWP refrigeration.

Freestanding models lead with a 58% share, driven by affordability, easy installation, and broad residential–commercial suitability.

North America leads with a 34.2% share through established consumer demand, robust regulatory frameworks, and smart home ecosystem adoption.

The strongest opportunity lies in energy-efficient, eco-friendly refrigeration, with the energy-efficient cooler segment growing at an 8.1% CAGR through 2033.

Leading market players include Whirlpool Corporation, LG Electronics, Samsung Electronics, Bosch, Haier Group, and Hisense.