- Beverages

- Fortified Wine Market

Fortified Wine Market Size, Share, and Growth Forecast, 2026 – 2033

Fortified Wine Market by Product Type (Port, Vermouth, Sherry, Others), Body Type (Heavy-Bodied, Medium-Bodied, Light-Bodied), Production Method (Solera System, Others), Raw Material Source, End-user Application, and Regional Analysis 2026 – 2033

Fortified Wine Market Size and Trends Analysis

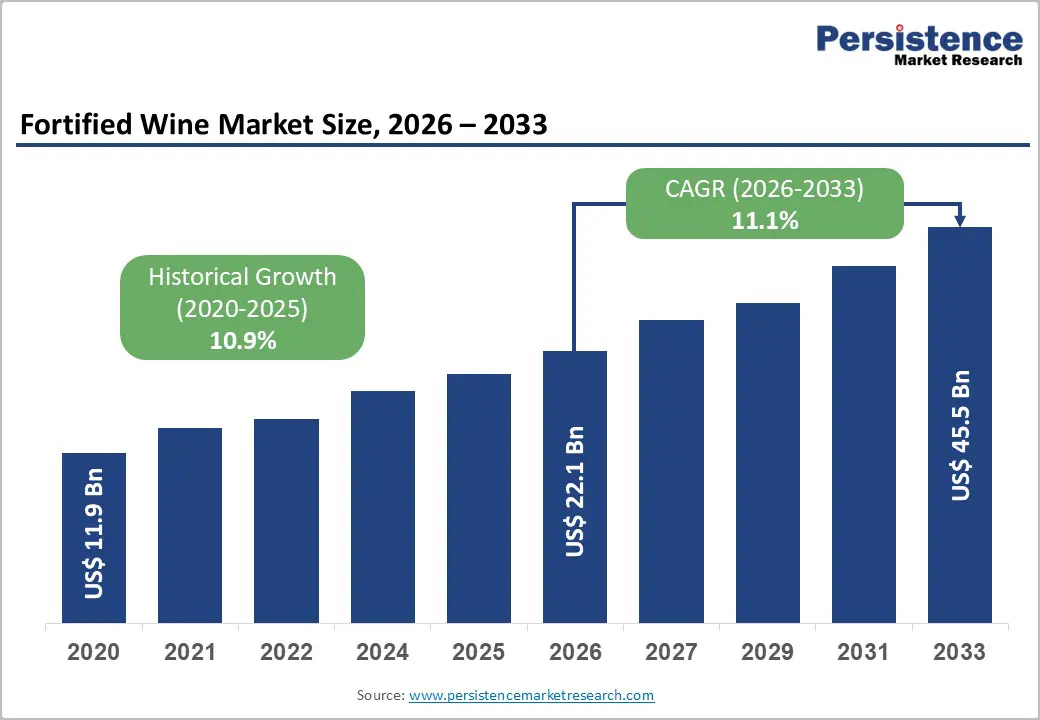

The global fortified wine market size is likely to be valued at US$22.1 billion in 2026 and is expected to reach US$45.5 billion by 2033, growing at a CAGR of 11.1% during the forecast period from 2026 to 2033, driven by premiumization, cocktail culture expansion, and premium alcohol demand in emerging markets.

The forecast period will likely see accelerated value expansion due to innovative product formats (canned ready-to-drink options) and the rising popularity of low-ABV (alcohol by volume) aperitifs. Growth is further bolstered by a robust recovery in the hospitality sector and the expansion of e-commerce channels for vintage wine investments.

Key Industry Highlights:

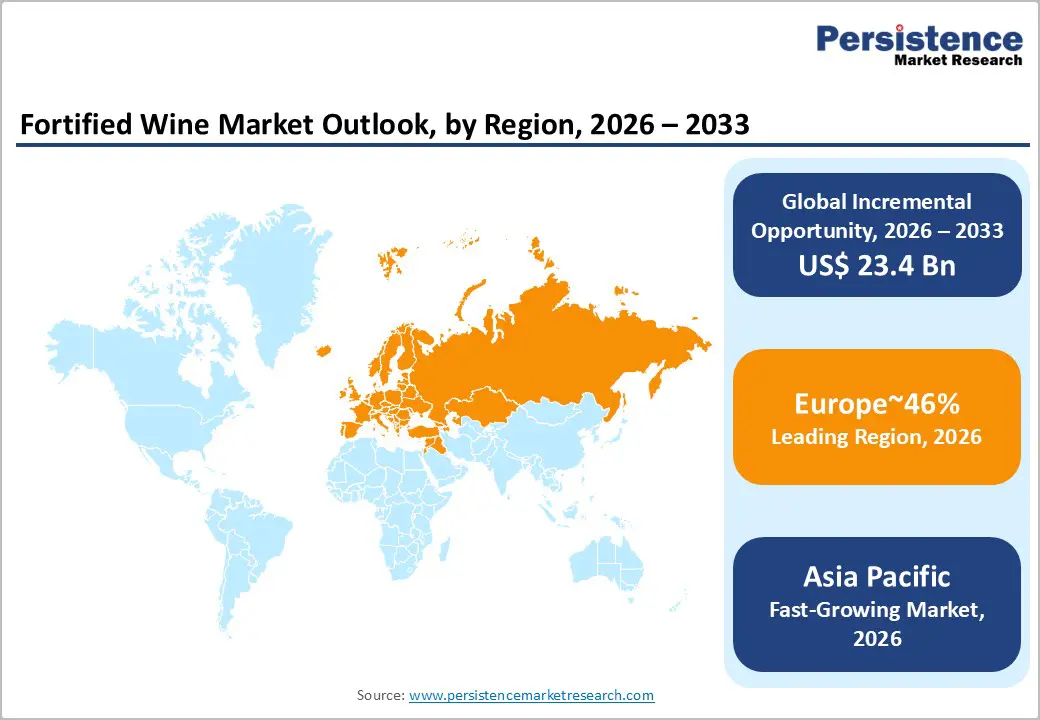

- Leading Region: Europe is expected to lead the market with approximately 46% share, as it is the historic production hub of fortified wines, including Port, Sherry, and Vermouth, with established vineyards, aging facilities, and export networks.

- Fastest-growing Region: Asia Pacific is likely to be the fastest-growing market for fortified wines, accounting for approximately 18% of global demand and expected to be the key driver of incremental volume growth in the medium term.

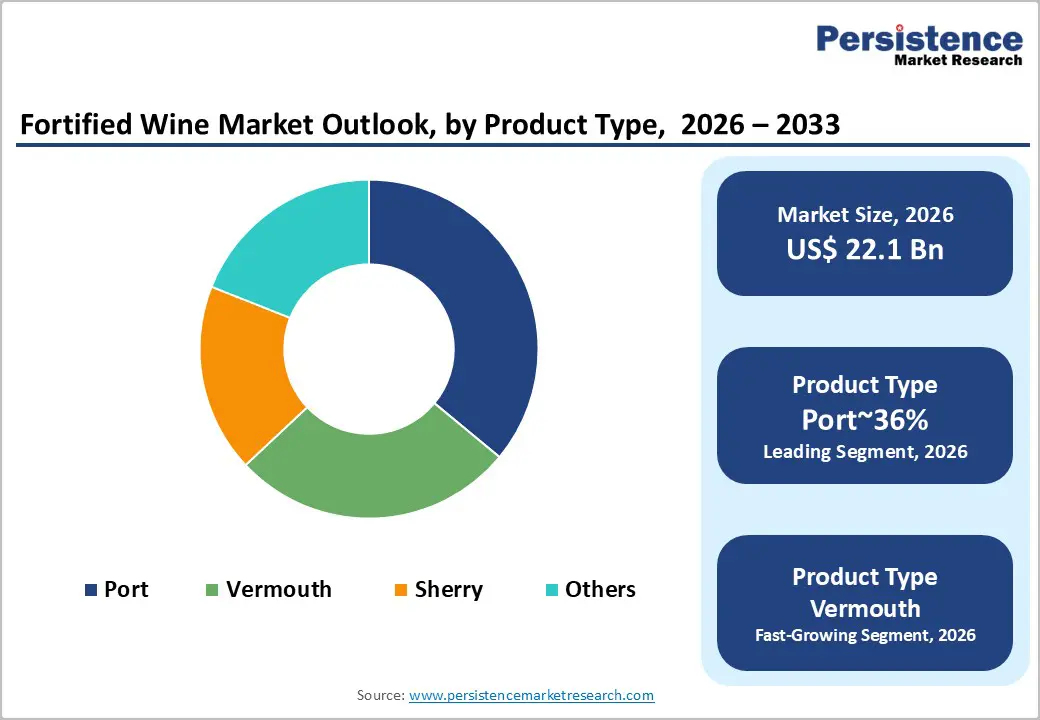

- Leading Product Type: Port is expected to dominate the market with approximately 36% share, supported by strong heritage, global consumer familiarity, and sustained demand in both off-trade retail and cocktail applications.

- Leading Raw Material Source: Red grapes are anticipated to lead the market with the market share of approximately 58%, reflecting their use in Port, Sherry, and other traditional fortified wines, offering rich flavor, color, and complexity.

| Key Insights | Details |

|---|---|

| Fortified Wine Market Size (2026E) | US$ 22.1 Bn |

| Market Value Forecast (2033F) | US$ 45.5 Bn |

| Projected Growth (CAGR 2026 to 2033) | 11.1% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Resurgence of Cocktail Culture and Mixology

The expansion of contemporary cocktail culture is structurally increasing demand for fortified wines by repositioning these products as core mixology inputs rather than peripheral digestifs. On-premise and premium casual channels are integrating vermouth and sherry into low-alcohol beverage architectures to align with shifting consumption preferences toward moderated intake and session-oriented formats. This reframing elevates fortified wines from legacy categories into high-velocity cocktail components, expanding usage occasions across pre-dinner, aperitif, and social drinking contexts. The resulting uplift in on-trade throughput is reinforcing demand visibility and increasing the relevance of fortified wines within bar programs that prioritize balance, complexity, and repeatable drink construction.

From a market-structure perspective, the normalization of fortified wines within cocktail menus is reshaping value-chain dynamics by increasing pull-through across premiumized SKUs and diversified flavor profiles. Higher rotation in on-trade settings improves inventory economics and shortens replenishment cycles, while product differentiation around botanical complexity and consistency strengthens brand positioning within bartender-led procurement ecosystems. This demand reconfiguration also supports margin stability through higher mix-driven consumption and reduces reliance on seasonal, occasion-bound demand patterns, embedding fortified wines more deeply into everyday beverage programs across urban hospitality and experiential retail formats.

Premiumization and Artisanal Fortified Wine Demand

Premiumization trends across alcoholic beverages are structurally elevating demand for fortified wines positioned within artisanal and craft-aligned consumption frameworks. Rising discretionary spending and preference shifts toward quality, provenance, and differentiated flavor profiles are reconfiguring purchasing behavior away from commoditized alcohol toward premium categories with stronger experiential value. Cultural anchoring in established consumption regions sustains baseline demand, while cocktail-led experimentation in newer markets is expanding fortified wine relevance within contemporary drinking occasions. This demand reorientation reinforces fortified wines as premium social beverages rather than legacy after-dinner formats, increasing velocity in on-trade channels and strengthening price realization across curated retail environments.

From a market-structure perspective, premiumization is improving category margin profiles by shifting mix toward higher-value SKUs with greater botanical complexity, aging differentiation, and origin signaling. Producers are reallocating portfolio emphasis toward artisanal positioning, smaller-batch formats, and design-led branding to capture premium shelf space and bartender-led procurement influence. This evolution raises content value per unit and supports margin resilience despite cost pressures across inputs and distribution. Collectively, artisanalization and premium demand are embedding fortified wines within higher-value consumption ecosystems, structurally strengthening revenue quality and reducing dependence on volume-driven growth models. González Byass released the 15th edition of its Tío Pepe Fino En Rama in 2024, an unfiltered, artisanal "SACA" that emphasizes provenance and minimal intervention to cater to the growing consumer demand for "raw" and complex flavor profiles.

Barrier Analysis – Climate Volatility and Viticultural Supply Constraints

The production base for fortified wines remains structurally exposed to climatic volatility due to geographic concentration in origin-linked viticultural regions. Rising temperature profiles, erratic precipitation, and shifting growing conditions are disrupting yield stability and altering grape composition, complicating consistency in sugar-acidity balance that underpins fortified wine quality and style profiles. These agronomic pressures increase dependency on adaptive cultivation practices, water management, and vineyard reconfiguration, elevating cost intensity across the upstream value chain. As production variability increases, supply predictability weakens, tightening raw material availability and constraining throughput for producers reliant on region-specific appellations and legacy cultivation systems.

From a market-structure perspective, climate-driven yield volatility transmits cost inflation into production economics, compressing margins or necessitating price adjustments across downstream channels. Higher input volatility elevates working capital requirements and increases inventory risk, particularly for aged and origin-protected categories with limited geographic substitution. Price transmission into entry-tier fortified wines heightens demand elasticity in price-sensitive segments, constraining volume scalability outside premium channels. Collectively, climate exposure introduces structural supply risk that weakens planning certainty, elevates compliance and sourcing complexity, and embeds long-term fragility within geographically constrained fortified wine value chains.

Opportunity Analysis – Low-ABV Innovation and RTD Fortified Formats

Innovation in low-alcohol and ready-to-drink fortified formats is expanding consumption contexts by repositioning legacy categories within convenience-led, occasion-driven beverage ecosystems. RTD adaptations of vermouth- and port-based serves are enabling penetration into casual, outdoor, and event-driven settings historically dominated by beer and cider, where portability and immediacy shape purchase behavior. This format shift lowers cognitive and usage barriers associated with traditional fortified wine rituals, broadening category accessibility and normalizing fortified profiles within informal social consumption. The resulting channel diversification strengthens off-trade rotation and embeds fortified wines within impulse-driven retail environments aligned with contemporary lifestyle consumption patterns.

From a market-structure perspective, RTD formats reconfigure the value chain toward packaging-intensive, formulation-driven differentiation, increasing content value per unit while introducing new cost structures across canning, cold-chain logistics, and regulatory compliance for mixed beverages. Low-alcohol positioning aligns with evolving moderation norms, extending addressable demand without displacing core premium formats. As distribution tilts toward convenience retail and experiential venues, margin realization becomes increasingly linked to branding coherence, formulation stability, and scale in RTD production. Collectively, low-ABV RTD innovation strengthens category resilience by diversifying demand pools and reducing reliance on traditional on-trade ritualized consumption.

Culinary Gastronomy and Food Pairing Integration

Culinary repositioning of fortified wines within savory gastronomy is expanding consumption occasions by embedding these products into contemporary food-pairing architectures. Dry and oxidative profiles are being aligned with tapas culture and umami-forward cuisines, reframing fortified wines as functional complements to multi-course dining rather than post-meal accompaniments. This integration into experiential dining formats increases relevance within chef-led menu design and elevates fortified wines within premium hospitality ecosystems. As pairing narratives gain traction, fortified wines benefit from higher menu visibility and structured trial mechanisms that support category re-entry into curated on-trade environments.

From a market-structure perspective, gastronomic integration shifts value capture toward on-trade channels with higher margin potential and stronger influence over consumer discovery pathways. Partnership-driven formats such as tasting flights embed fortified wines into premium dining journeys, increasing per-occasion spend and reinforcing premium positioning. This channel realignment elevates the importance of sommelier education, menu engineering, and consistency in supply quality, while reducing dependence on traditional retail-driven demand. Collectively, culinary alignment strengthens category differentiation, supports price realization through experiential framing, and stabilizes on-trade recovery by anchoring fortified wines within evolving food-centric consumption rituals. The Fladgate Partnership (Taylor’s Port) utilized 2023 to aggressively expand the presence of its Chip Dry White Port within the global "White Port & Tonic" movement, specifically targeting the savory aperitif hour in European on-trade hospitality.

Category-wise Analysis

Product Insights

Port wine is anticipated to lead, accounting for approximately 36% of the total demand. The segment increasingly operates as a premium, asset-like category rather than a volume-driven dessert wine. Producers such as Taylor’s and Graham’s continue to prioritize long-aged Tawny and Vintage releases, using extended cellar maturation, limited allocations, and high-spec presentation formats to reinforce scarcity value and price discipline. Port also benefits from strong performance in gifting, collector purchases, and curated tasting experiences, where vintage dating and house reputation function as trust anchors. Portfolio strategies that emphasize Single Quinta bottlings, premium glass, and narrative-driven packaging are likely to sustain brand-led pricing power and keep Port anchored as the category’s dominant revenue generator.

Vermouth is anticipated to be the fastest-growing product type, driven by its expanding role across cocktails, low-ABV occasions, and premium home mixology. Brands such as Martini Riserva, Carpano Antica Formula, and Noilly Prat increasingly position their products as essential back-bar foundations rather than secondary modifiers, supported by upgrades in wine base selection, botanical transparency, and longer infusion protocols. Premium cues now include single-variety wine bases, clearly disclosed herb profiles, and craft-style production stories that resonate with trade professionals and enthusiasts alike. Ongoing portfolio premiumization, stronger on-trade advocacy, and product designs that emphasize versatility are likely to keep Vermouth on a structurally higher growth trajectory within fortified wines.

Raw Material Source Insights

Red grapes are expected to dominate, accounting for approximately 58% of the total usage in 2025, and this position is expected to remain structurally entrenched over the forecast period due to their functional and commercial advantages in premium fortified styles. Red grape bases are anticipated to continue anchoring high-value Port, Marsala Rubino, and Sweet Vermouth portfolios because elevated tannin, anthocyanin stability, and phenolic density support long-term aging, oxidative resilience, and visual richness after fortification. Brand portfolios such as Taylor’s Vintage expressions, Graham’s long-aged Tawny programs, and Florio Rubino lines increasingly emphasize structured red grape profiles to sustain premium positioning and cellar-worthiness. Investment in estate-controlled vineyards and tighter integration of fermentation systems is expected to reinforce supply security and stylistic consistency for flagship labels.

Botanical infusion is anticipated to be the fastest-growing raw material source, driven by the premiumization of Vermouth and the rising strategic importance of botanical differentiation in brand architecture. Products such as Carpano Antica Formula, Cocchi Storico, Noilly Prat Original Dry, and St. Agrestis increasingly foreground complex herbal matrices, longer maceration protocols, and clearly articulated botanical provenance to justify trade-up pricing and higher on-trade relevance. Botanical intensity is expected to gain prominence as consumers gravitate toward bitter-complex profiles and aperitivo-style consumption occasions, expanding demand beyond classic cocktail modifiers into standalone long-drink formats. Advanced extraction techniques and barrel-rested infusions are likely to deepen flavor layering and extend product line segmentation within premium and super-premium Vermouth ranges.

Regional Insights

Europe Fortified Wine Market Trends

Europe is expected to be the dominant region in the global fortified wine market, accounting for roughly 46% of worldwide demand and anchoring both production and consumption. The region functions as the category’s structural core rather than a growth outlier, with deeply embedded consumption rituals, protected appellations, and export-oriented legacy houses sustaining volume and value. The U.K. operates as a major import and trading hub, France anchors aperitif wine consumption, and Germany contributes a large, urban, on-trade driven demand base, while Southern Europe remains the supply and heritage engine. Investment flows are concentrated in enotourism, direct-to-consumer channels, and portfolio premiumization, reinforcing Europe’s role as both the price-setter and innovation reference point for the category.

Spain and Portugal form the strategic production axis that defines the region’s fortified wine economics. Spain’s Jerez cluster, built around the Solera system, continues to anchor global sherry supply. Competitive structure is relatively concentrated, with established houses such as Symington and Lustau controlling significant branded volume and distribution leverage, alongside targeted acquisitions of boutique producers to capture premium and experiential demand. The current cycle is shaped by cocktail-led rediscovery, urban on-trade activation, and premium-led trade-up, which together reinforce Europe’s dominance rather than alter the regional balance of power.

North America Fortified Wine Market Trends

North America is a stable and premium-oriented market for fortified wines, supported by high disposable income and a mature cocktail culture across the U.S. and Canada. The U.S. leads regional consumption and import demand for vermouth, sherry, and port, driven by the normalization of premium mixology across on-premise channels such as cocktail bars, upscale casual dining, and hotel lounges. Retail distribution is increasingly omnichannel, with major wine groups and specialty retailers expanding direct-to-consumer and e-commerce presence, which is expected to further formalize premium category penetration across urban and suburban markets. Market momentum is expected to be shaped by premiumization, low-ABV positioning, and the craft fortified wine movement, particularly among millennial and Gen Z consumers seeking sessionable aperitifs and cocktail-forward formats.

The regulatory environment, overseen by the U.S. Alcohol and Tobacco Tax and Trade Bureau, continues to emphasize strict labeling and appellation clarity, which supports brand equity for authenticated vermouth and sherry styles but also raises compliance costs for smaller producers. Competitive dynamics remain fragmented, with large wine groups such as E. & J. Gallo Winery retaining scale advantages in distribution, while boutique players such as Sokol Blosser are expanding aperitif-led portfolios to capture at-home consumption occasions.

Asia Pacific Fortified Wine Market Trends

Asia Pacific represents the fastest-growing regional market for fortified wines, accounting for roughly 18% of global demand and structurally positioned as the primary incremental volume contributor over the medium term. China functions as the scale driver, with urban consumption shifting from traditional red wine toward diversified premium imports, including Port and Sherry, supported by premium gifting occasions and the normalization of Western aperitif culture in Tier-1 and Tier-2 cities. Digital commerce and social-led discovery are central demand enablers across China, Japan, and India, allowing premium fortified wine brands to bypass fragmented traditional distribution and directly access urban consumers.

India represents an early-stage but structurally important growth node, underpinned by urbanization, rising disposable incomes, and premiumization within metropolitan on-trade clusters. Australia provides regional production depth through heritage fortified styles such as Rutherglen Muscat and Tokay, with producers such as Campbells and Chambers supplying both domestic demand and selected Asian export channels, creating logistical and tariff advantages within the region. The competitive structure remains import-led, but localized bottling, regional branding initiatives, and bar-led cocktail adoption continue to accelerate fortified wine penetration across Asia Pacific’s major consumption corridors.

Competitive Landscape

The fortified wine market is moderately consolidated, with power concentrated among multinational beverage groups such as E. & J. Gallo, Campari, Bacardi, and The Wine Group, alongside heritage producers such as Sogrape that anchor premium categories. These players matter because their scale, brand portfolios, and global distribution networks shape shelf presence, pricing power, and category visibility across vermouth, sherry, port, and Madeira. Leadership at the top coexists with a broad base of historic estates that retain influence in protected-origin segments, reinforcing a two-tier structure between mass-market volumes and premium heritage positioning.

Competitive positioning reflects a clear split between portfolio-driven conglomerates competing on global reach and brand activation, and heritage-led producers differentiating through provenance, aging credentials, and appellation control. Industry behavior shows growing portfolio rationalization, premiumization strategies, and selective acquisitions, while the lower end remains dynamic as craft and botanical-focused producers fragment niche demand. This pattern signals gradual consolidation at the top alongside sustained experimentation and brand storytelling among boutique challengers.

Key Industry Developments:

- In February 2026, Redbreast (Irish Distillers) launched Moscatel Wine Cask Edition whiskey finished in fortified Moscatel casks. The use of fortified casks highlights cross-category partnerships, boosting fortified wine visibility.

- In April 2025, Tri-Vin Imports launched XXL, a high-alcohol fruit-flavored fortified wine. The product appeals to younger demographics with innovative flavors, potentially revitalizing category consumption.

- In January 2025, Taylor’s Port established the 80-Year-Old Tawny Port category and released "Victory Port" to mark the 80th anniversary of WWII's end. This rare release reinforces the premiumization trend by targeting collectors with limited-edition "liquid assets," with only 1,945 numbered bottles produced.

Companies Covered in Fortified Wine Market

- E. & J. Gallo Winery

- Constellation Brands, Inc.

- Treasury Wine Estates

- Davide Campari-Milano

- Bacardi Limited

- The Wine Group

- Sogrape Vinhos

- Symington Family Estates

- The Fladgate Partnership

- González Byass

- Bodegas Lustau

- Kopke Group (formerly Sogevinus Fine Wines)

- Trinchero Family Estates

- Osborne Group

- Quinta do Noval

- Fratelli Branca Distillerie

- Giulio Cocchi Spumanti

Frequently Asked Questions

The global fortified wine market is projected to be valued at US$22.1 billion in 2026 and is expected to reach US$45.5 billion by 2033, driven by premiumization, the resurgence of cocktail culture, and rising demand in emerging markets.

Fortified wines such as Vermouth and Sherry are being redefined as key low-ABV ingredients in cocktails and aperitifs, boosting their use in bars and social settings beyond traditional after-dinner drinks.

The fortified wine market is forecast to grow at a CAGR of 11.1% from 2026 to 2033, reflecting strong demand from premiumization trends and innovative product formats such as ready-to-drink (RTD) options.

Europe is the leading regional market, accounting for approximately 46% share, supported by its historic role as the production hub for iconic styles such as Port and Sherry, deeply embedded consumption rituals, and a strong export-oriented heritage.

The market is moderately consolidated, led by multinational beverage giants such as E. & J. Gallo, Campari, and Bacardi, while heritage producers, including Symington, Fladgate, and González Byass, dominate the premium segment with strong brand equity and appellation control in Port and Sherry.