- Animal Health

- Swine Autogenous Vaccines Market

Swine Autogenous Vaccines Market Size, Share, and Growth Forecast, 2026 - 2033

Swine Autogenous Vaccines Market by Strain Type (Bacterial Strain, Viral Strain), Application (Respiratory Diseases, Gastrointestinal Diseases, Others), End-user (Veterinary Clinics and Hospitals, Livestock Farming Companies, Research and Academic Institutes), and Regional Analysis for 2026 - 2033

Swine Autogenous Vaccines Market Size and Trends Analysis

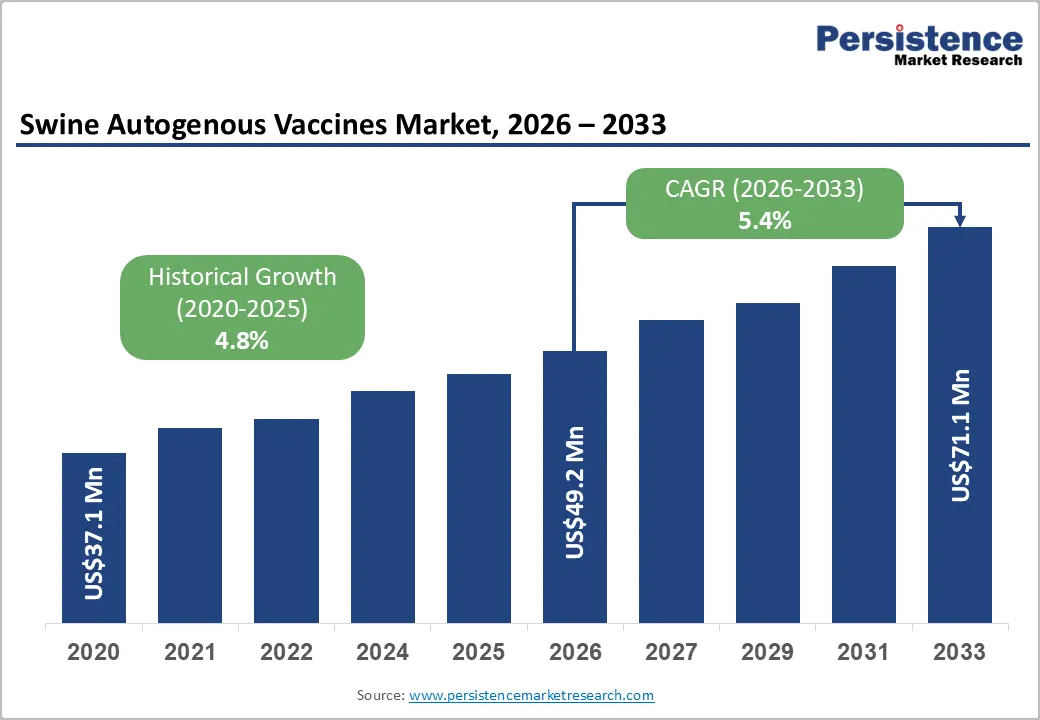

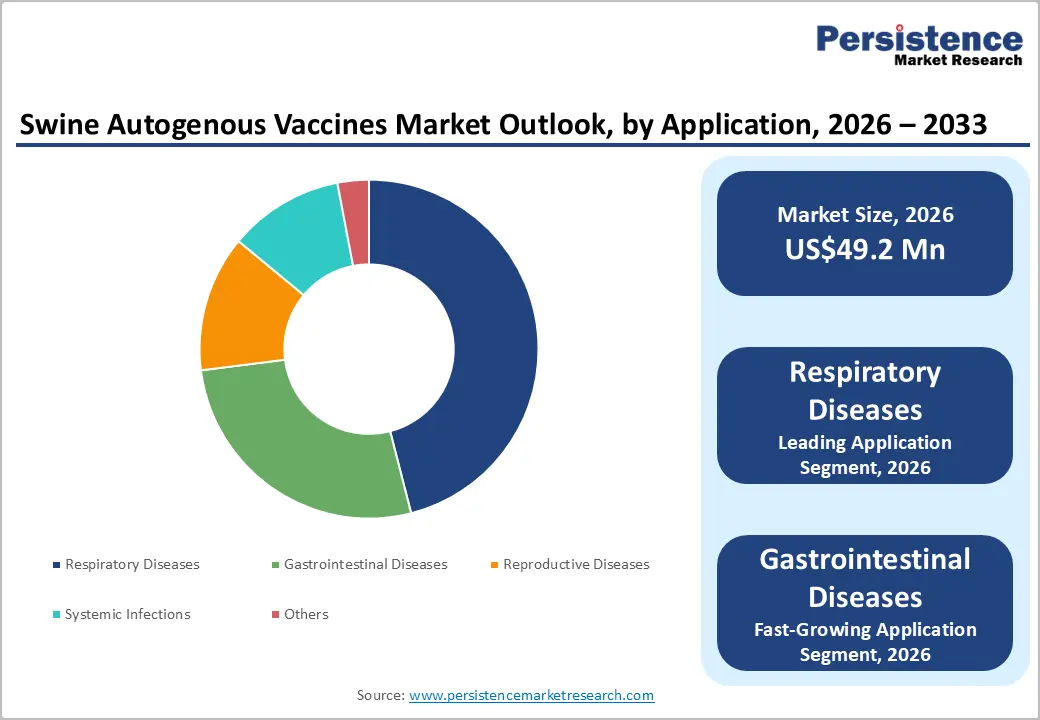

The global swine autogenous vaccines market size is likely to be valued at US$49.2 million in 2026 and is estimated to reach US$71.1 million by 2033, growing at a CAGR of 5.4% during the forecast period from 2026 to 2033, driven by increasing disease pressure in intensive swine production systems, rising demand for herd-specific immunization solutions, expansion of veterinary diagnostic infrastructure, and accelerated adoption of precision livestock health management systems.

Growth momentum is supported by rising protein consumption, particularly increasing pork demand among urban populations. Regulatory frameworks promoting antimicrobial reduction in livestock production strengthen reliance on autogenous vaccine strategies. Technology adoption in genomic sequencing and pathogen isolation enhances strain-specific vaccine design efficiency.

Key Industry Highlights:

- Leading Strain Type: Bacterial strain is set to hold around 58% revenue share in 2026, driven by the dominance of Actinobacillus pleuropneumoniae as the primary isolate source in commercial respiratory disease programs.

- Fastest-growing Strain Type: The viral strain is projected to be the fastest-growing segment, supported by the accelerating detection of novel PRRS variants diverging from existing commercial vaccine seed strains.

- Leading Application: Respiratory diseases are estimated to hold roughly a 46% revenue share in 2026, driven by the high clinical burden of porcine respiratory disease complex in high-density confinement production systems.

- Fastest-growing Application: Gastrointestinal diseases are forecast to record the fastest growth, driven by rising antimicrobial-resistant E. coli strains converting antibiotic budgets into autogenous vaccine procurement under EU regulations.

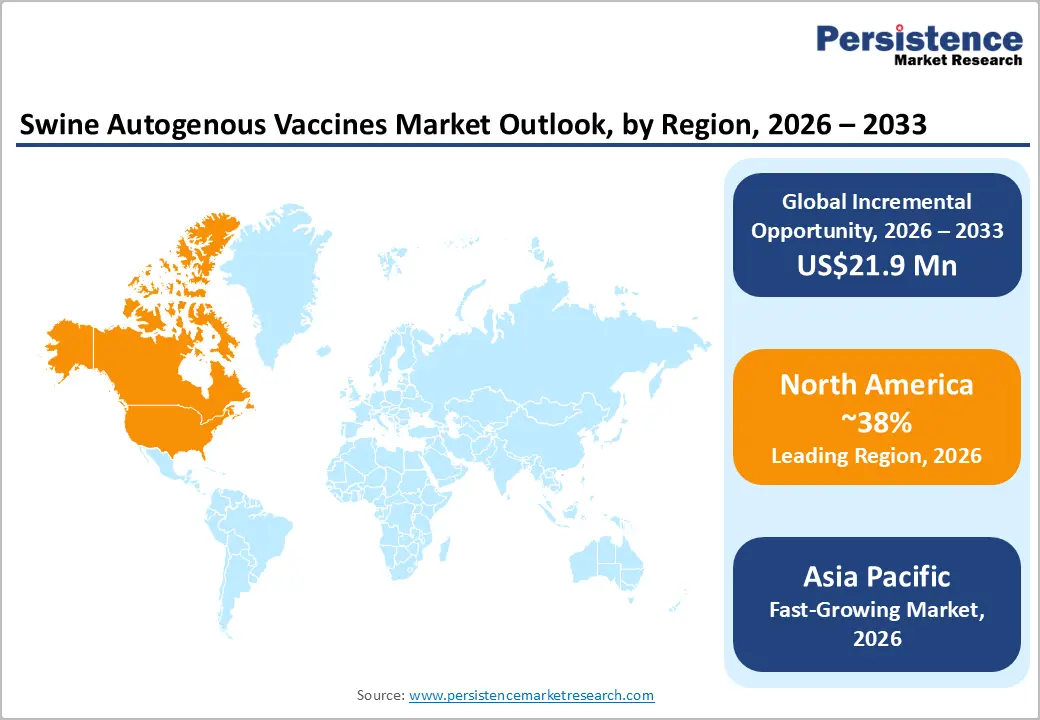

- Regional Leadership: North America is projected to account for roughly 38% of global market revenue, driven by high vertical integration and mature veterinary healthcare infrastructure.

- Competitive Environment: The market reflects a moderately fragmented structure, with key players such as Boehringer Ingelheim Animal Health and Merck Animal Health leveraging isolated bank depth and regulatory compliance capabilities to maintain positioning.

- Innovation Trends: Genomic sequencing integration in antigen selection, regional isolate banking in Asia Pacific, and EU regulatory harmonization are shaping long-term market evolution and investment direction.

DRO Analysis

Driver - Escalating Pathogen Genetic Drift and Commercial Vaccine Failures

Rapid mutations within endemic swine viral and bacterial populations severely compromise the efficacy of standard commercial vaccines. Standardized formulations often fail to provide cross-protection against newly emerged field strains, leaving herds vulnerable to catastrophic economic losses. Porcine Reproductive and Respiratory Syndrome (PRRS) and Streptococcus suis exhibit high genetic variability, enabling them to bypass conventional herd immunity.

The resulting production deficits compel farm operators to turn toward custom biological solutions. Autogenous production platforms utilize pathogens isolated directly from the affected herd, guaranteeing an exact antigenic match. This direct correlation between isolated field strains and vaccine composition eliminates the risk of strain mismatch. Herd-specific formulation provides targeted immunological defense, restoring stability to commercial swine populations and lowering overall mortality.

Restraint - High Unit Development Costs and Scale Deficits

The customized manufacturing process required for autogenous biologicals prevents the realization of traditional economies of scale. Every product batch demands separate diagnostic isolation, pathogen cultivation, and formulation protocols tailored to a single production site. These highly individualized production steps elevate the cost per dose far above standard mass-manufactured alternatives.

Small and independent livestock operators often find these upfront diagnostic and formulation fees prohibitive. The absence of bulk volume distribution structures compresses profit margins for producers operating in low-margin pork segments. Consequently, high capital requirements limit widespread adoption to wealthy, vertically integrated livestock corporations.

Opportunity - Integration of Genomic Sequencing Technologies in Antigen Identification

Next-generation sequencing platforms are enabling veterinary laboratories to characterize swine pathogens at a molecular resolution that was previously unavailable within clinically relevant timeframes. The application of whole-genome sequencing to swine respiratory and enteric isolates allows manufacturers to select antigen candidates with a precision that substantially improves vaccine efficacy. The FDA authorized expanded use of genomic characterization data in biological license submissions in 2024, creating a formal regulatory pathway for sequence-based antigen selection.

Manufacturers integrating bioinformatics platforms into their production workflows are positioned to reduce isolate-to-batch timelines from weeks to days, expanding the addressable customer base to include operations requiring rapid outbreak response. This technological capability creates a defensible competitive moat for early adopters and supports premium pricing models that can sustain higher gross margins across the production cycle.

Category-wise Analysis

Product Type Insights

Bacterial strain is anticipated to secure around 58% of the swine autogenous vaccines market share in 2026, reflecting the clinical dominance of Actinobacillus pleuropneumoniae and Haemophilus parasuis in commercial herd disease burden. Boehringer Ingelheim has expanded multi-valent bacterial formulation services across North American integrated operations. Commercial vaccines cannot replicate farm-derived antigenic combinations. This gap sustains consistent procurement of bacterial autogenous protocols.

Viral strain is expected to be the fastest-growing segment, propelled by increasing detection of novel PRRS variants and porcine circovirus type 3 strains showing antigenic drift from licensed commercial seed strains. Merck Animal Health has introduced rapid viral isolate processing capabilities. Expanding PCR-based surveillance is identifying divergent strains earlier. Upstream demand for autogenous viral formulations is rising ahead of outbreak escalation.

Application Insights

Respiratory diseases are poised to dominate with a forecast market share of over 46% in 2026, powered by the polymicrobial nature of the porcine respiratory disease complex requiring multi-component autogenous biologics. Huvepharma has deployed customized multivalent respiratory formulations across large European integrated operations. Clinical and economic losses are highest in high-density confinement systems. Procurement volumes concentrate among the largest commercial producers.

Gastrointestinal diseases are estimated to be the fastest-growing segment, fueled by rising post-weaning diarrhea caused by antimicrobial-resistant enterotoxigenic E. coli strains. Elanco Animal Health has recorded growing autogenous E. coli formulation demand across EU farrowing units. Antibiotic reduction mandates are eliminating therapeutic alternatives. Autogenous vaccination is becoming the primary preventive intervention in affected systems.

End-user Insights

Livestock farming companies are likely to be the leading segment with a projected 52% of the swine autogenous vaccines market share in 2026 due to the concentration of high-density commercial production within vertically integrated operators. Smithfield Foods has institutionalized autogenous vaccination within its national herd health management program. Integrated systems generate the isolated volumes and procurement scale needed to justify autogenous program development costs.

Research and academic institutes are anticipated to be the fastest-growing segment, fueled by rising public and private investment in swine immunology and pandemic preparedness. Iowa State University Veterinary Diagnostic Laboratory expanded its swine pathogen banking services in 2025. USDA APHIS biosurveillance funding is channeling capital into academic diagnostic infrastructure. This indirectly accelerates autogenous biological program development at scale.

Regional Insights

North America Swine Autogenous Vaccines Market Trends

North America is expected to lead with an estimated 38% of the market share in 2026, supported by high vertical integration and mature veterinary healthcare infrastructure. Corporate swine integrators focus extensively on custom preventative biological portfolios to protect profit margins against endemic disease waves. The widespread availability of next-generation diagnostic centers enables rapid pathogen extraction, which shortens total production cycles.

U.S. Swine Autogenous Vaccines Market Insights

The U.S. is projected to secure around 84% of the regional market share in 2026, driven by high adoption of precision livestock farming tools and strict pathogen monitoring. Large-scale production operations utilize customized biologicals to combat persistent localized variations of Porcine Reproductive and Respiratory Syndrome. This structural emphasis on biosecurity ensures continuous funding for advanced autogenous development.

Canada Swine Autogenous Vaccines Market Insights

Canada is forecast to account for nearly 16% of the regional market share in 2026, propelled by export-oriented pork manufacturing regulations that mandate minimal antibiotic residues. Production facilities increasingly deploy custom autogenous formulations to satisfy strict global trade compliance requirements. This focus on premium quality standards fosters steady integration with domestic custom vaccine manufacturers.

Europe Swine Autogenous Vaccines Market Trends

Europe is projected to maintain a substantial market presence with roughly 28% of the global share in 2026, influenced by strict regional bans on antibiotic growth promoters and rising animal welfare requirements. European producers depend on tailored biological alternatives to control subclinical infections in high-density installations without using chemicals.

Germany Swine Autogenous Vaccines Market Insights

Germany is anticipated to capture approximately 31% of the regional market share in 2026, driven by the urgent need to control persistent wild boar pathogen spillover. Agricultural operations rely on custom-tailored biological solutions to shield commercial herds from external regional viral variations. This defensive biosecurity posture stabilizes consistent domestic procurement volumes.

Spain Swine Autogenous Vaccines Market Insights

Spain is expected to command around 24% of the regional market share in 2026, supported by the ongoing consolidation of its commercial pork production infrastructure. Large integrated operations adopt custom autogenous programs to maintain herd efficiency across expanding processing assets. This scale expansion ensures long-term partnerships with specialized regional biological laboratories.

Asia Pacific Swine Autogenous Vaccines Market Trends

Asia Pacific is forecast to be the fastest-growing market for swine autogenous vaccines, stimulated by rapid livestock industrialization and a massive domestic pork production base. Rising consumer meat demand encourages the transition from small backyard farms to automated, high-density corporate production hubs. This consolidation increases herd vulnerability to infectious epidemics, driving heavy corporate investment into customized biosecurity measures.

China Swine Autogenous Vaccines Market Insights

China is likely to claim over 58% of the regional market share in 2026, propelled by the large-scale reconstruction of modern corporate swine facilities. Corporate producers utilize autogenous formulations to build robust herd defense systems against highly variable regional field strains. This systemic transition to industrial biosecurity generates significant demand for custom antigen production.

Vietnam Swine Autogenous Vaccines Market Insights

Vietnam is expected to capture roughly 12% of the regional market share in 2026, fueled by rising investments in commercial veterinary infrastructure and expanding livestock operations. Farms implement customized autogenous programs to limit economic losses from multi-drug resistant enteric bacterial outbreaks. This shifting clinical practice accelerates market penetration within emerging commercial farming networks.

Competitive Landscape

The global swine autogenous vaccines market is moderately fragmented. Large multinationals and specialized manufacturers compete across regional markets. Scale advantages favor established players in antigen production and cold-chain logistics. Key participants include Boehringer Ingelheim Animal Health, Merck Animal Health, Elanco Animal Health, Ceva Santé Animale, and Newport Laboratories.

Specialized autogenous manufacturers compete on turnaround speed and flexible batch sizing. Biological specificity limits product transferability across farms and geographies. Winner-takes-all dynamics do not apply in this market. Regional isolate bank relationships create durable competitive differentiation for smaller focused manufacturers.

Companies Covered in Swine Autogenous Vaccines Market

- Boehringer Ingelheim Animal Health

- Merck Animal Health (MSD Animal Health)

- Elanco Animal Health

- Ceva Santé Animale

- Newport Laboratories (Sioux Biochemical)

- Huvepharma

- IDT Biologika

- Phibro Animal Health Corporation

- Zoetis Inc.

- Colorado Serum Company

- Hygieia Biological Laboratories

- Veterinary Biologics Inc.

- Intervet International BV

- Diagnostix Inc.

- Profection Biologicals

Frequently Asked Questions

The global swine autogenous vaccines market is projected to reach US$49.2 million in 2026.

The swine autogenous vaccines market is driven by rising incidence of swine infectious diseases, expansion of intensive livestock production systems, and increasing regulatory pressure to reduce antimicrobial usage.

The swine autogenous vaccines market is poised to witness a CAGR of 5.4% from 2026 to 2033.

Key market opportunities include the expansion of precision livestock farming, growth in veterinary diagnostic infrastructure, and increasing adoption of farm-specific vaccine customization.

Some of the key market players include Boehringer Ingelheim Animal Health, Merck Animal Health, Elanco Animal Health, Ceva Santé Animale, and Newport Laboratories.