- Home Care & Utilities

- Bar and Wine Tools Market

Bar and Wine Tools Market Size, Share, and Growth Forecast 2026 - 2033

Bar and Wine Tools Market by Product Type (Cocktails, Wine/Beer, Smoking), by Application (Households, Bar and Wine Shops, Restaurants, Shops, Others), by Distribution Channel (Online Channels, Offline Channels), by Regional Analysis, 2026 - 2033

Bar and Wine Tools Market Size and Trend Analysis

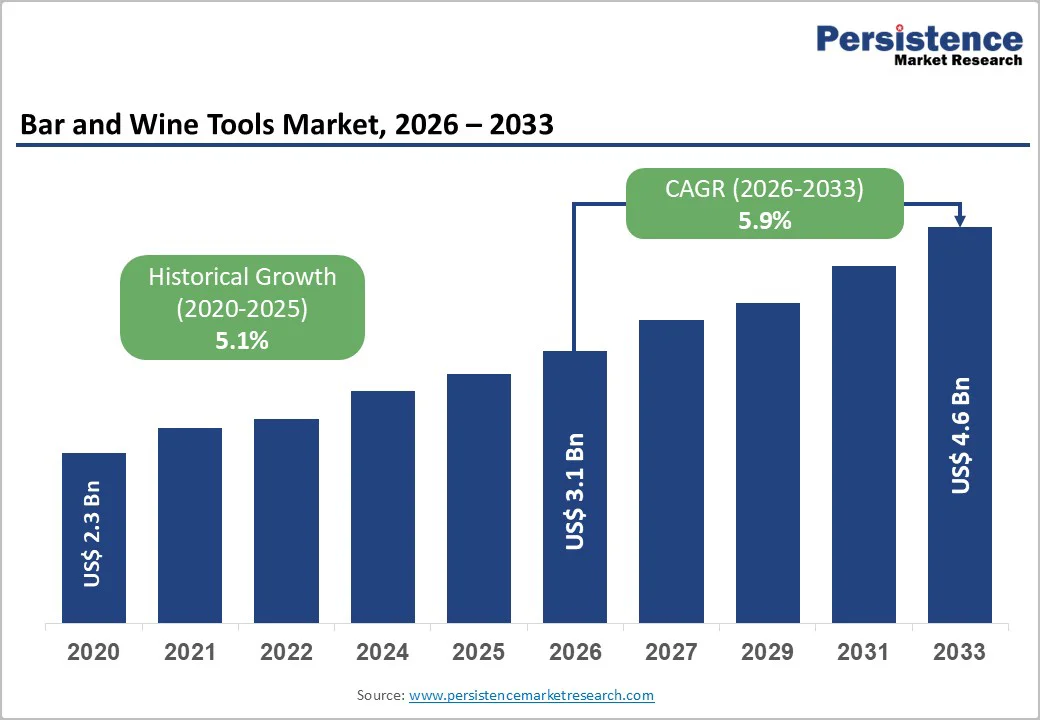

The global bar and wine tools market size is likely to be valued at US$ 3.1 Billion in 2026 and is expected to reach US$ 4.6 Billion by 2033, growing at a CAGR of 5.9% during the forecast period from 2026 to 2033.

Rising at-home consumption of cocktails and wine, coupled with the premiumization of barware, is accelerating demand for tools such as shakers, openers, aerators, and preservation systems across both developed and emerging economies.

Key Industry Highlights:

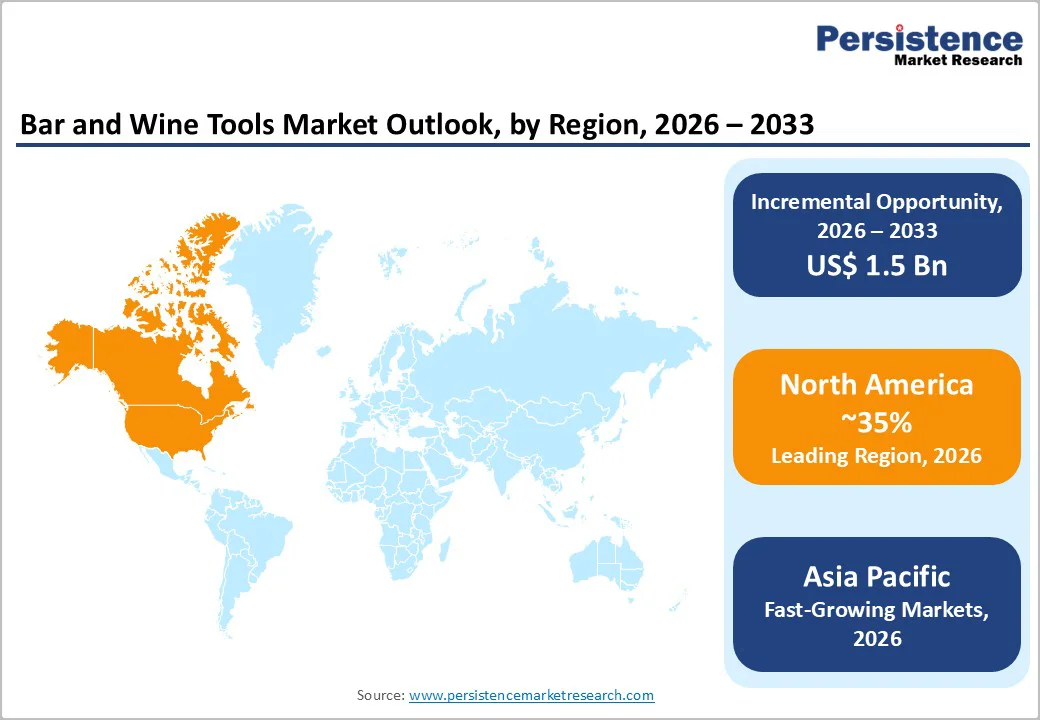

- Leading Region: North America remains a leading region for bar and wine tools holding 35% of global revenue, supported by high wine and cocktail consumption, dense restaurant and bar networks, and strong adoption of premium accessories across the U.S. and Canada.

- Fastest-Growing Region: Asia Pacific is the fastest-growing region as rising incomes with rising CAGR of 7%, urban nightlife, and expanding hospitality infrastructure in China, India, Japan, and ASEAN countries drive rapid uptake of barware and wine accessories.

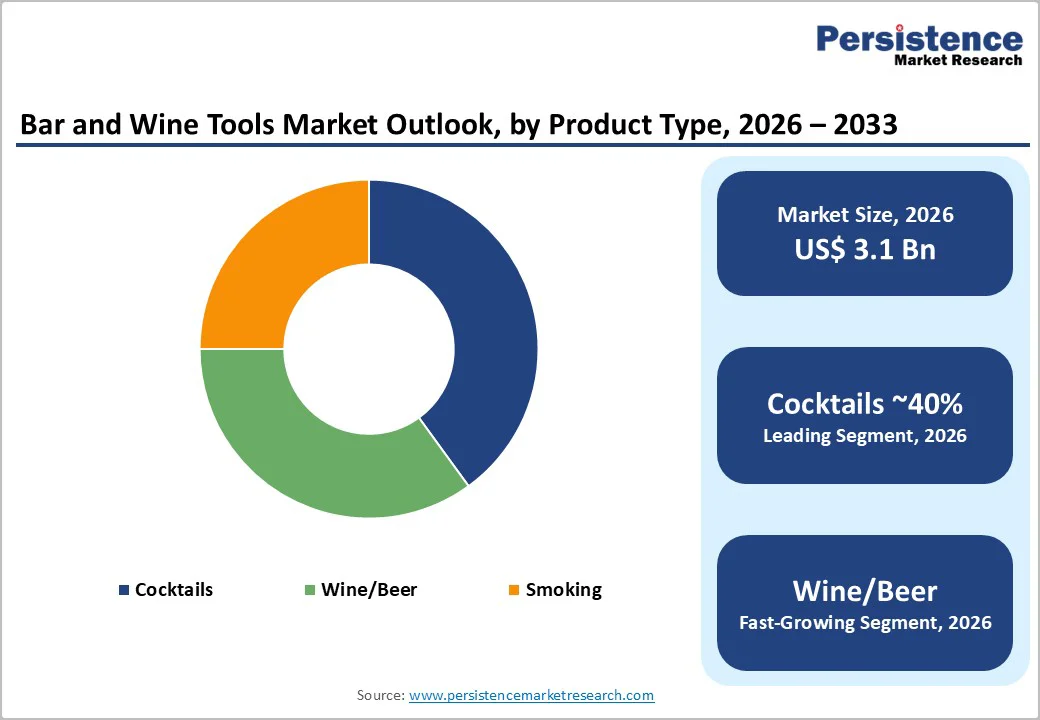

- Leading Segment: Cocktail tools are the dominant product segment with 40% share, due to their central role in preparing an expanding range of mixed drinks and mocktails, leading to high usage intensity and frequent replacement cycles in both home and professional settings.

- Fastest-Growing Segment: Within distribution, offline retail currently leads sales; however, online channels are the fastest-growing as consumers increasingly purchase bar sets, preservation devices, and design-led glassware through e-commerce platforms and brand websites.

- Key market opportunity lies in premium and smart bar and wine tools, including advanced wine preservation systems, connected devices, and sustainable materials that command higher margins and align with evolving consumer lifestyle and environmental preferences.

| Key Insights | Details |

|---|---|

| Bar and Wine Tools Market Size (2026E) | US$ 3.1 Billion |

| Market Value Forecast (2033F) | US$ 4.6 Billion |

| Projected Growth CAGR (2026 - 2033) | 5.9% |

| Historical Market Growth (2020 - 2025) | 5.1% |

Market Dynamics

Drivers - Rising global consumption of wine and premium cocktails

Global demand for wine, spirits, and premium cocktails continues to grow steadily across both on-trade and off-trade channels, creating a strong foundation for rising sales of bar and wine tools. According to the International Organisation of Vine and Wine (OIV), worldwide wine consumption has remained stable at nearly 25 billion liters annually, with sparkling and premium wine categories expanding faster than the overall market. This shift directly increases demand for accessories such as corkscrews, aerators, stoppers, and preservation systems that improve flavor and reduce product wastage.

At the same time, the growing popularity of mixology, especially in urban centers, high-end restaurants, and tourism-driven destinations, has encouraged bars to adopt standardized, professional-grade tools including cocktail shakers, jiggers, strainers, and muddlers. These trends collectively support recurring replacement demand and drive steady market growth for manufacturers and distributors.

Expansion of home bars and experiential home entertaining

Home bars are becoming increasingly popular due to rising urbanization, higher household incomes, and lifestyle changes shaped by hybrid or work-from-home environments. Consumer surveys from North America and Europe show a clear rise in home-based social gatherings, pushing demand for barware kits, elegant glassware, and easy-to-use wine openers designed for non-professional users.

E-commerce platforms amplify this trend by offering bundled bar sets, premium designs, and seasonal gifting options that appeal to younger and style-conscious buyers. Social media platforms such as Instagram, Pinterest, and YouTube are also shaping buying behavior by popularizing at-home mixology tutorials, cocktail recipes, and wine-tasting content. As consumers increasingly view bar and wine tools as lifestyle accessories, this category benefits from higher aesthetic preferences, frequent gifting demand, and repeat purchases for home entertainment.

Restraints - Regulatory pressures and health-conscious consumption patterns

Regulatory restrictions around alcohol sales, taxation, and advertising in many countries can indirectly impact demand for bar and wine tools by influencing consumption habits and bar establishment openings. Higher duties, licensing rules, and limitations on promotional activities often reduce on-premise alcohol sales, thereby lowering procurement volumes for professional bar tools. At the same time, global health campaigns encouraging moderate drinking, as well as the growing adoption of low-alcohol or alcohol-free beverages, are influencing consumption frequency among specific demographic groups.

While several bar tools are now used for mocktails, fresh-fruit mixes, and non-alcoholic beverages, overall demand remains closely tied to alcoholic drink volumes. These shifts can affect unit sales, particularly for tools designed exclusively for spirits or wine. Consequently, manufacturers must adapt portfolios to cater to evolving consumer preferences and regulatory environments.

Market fragmentation and price sensitivity in lower tiers

The global bar and wine tools market remains fragmented, with a significant presence of unbranded, mass-produced, and private-label products that place pricing pressure on established manufacturers. This is especially noticeable in categories such as basic openers, standard shakers, and everyday glassware, where consumers in emerging economies often opt for low-priced imports instead of premium branded options.

Intense competition within these segments limits companies’ ability to increase prices even when raw material costs rise, particularly for metals, glass, and packaging inputs. As a result, brand-building efforts and differentiation strategies become more challenging. Companies operating in the mid-premium and premium segments must invest heavily in design, material innovation, and marketing to justify higher prices and maintain profitability. High fragmentation also complicates distribution efficiency and reduces brand visibility in retail environments.

Market Opportunities

Premiumization and smart wine preservation systems

Premium bar and wine tools, including conneacted or technology-enabled devices, present strong opportunities for manufacturers seeking differentiation and higher margins. Advanced wine preservation systems, such as those offered by brands like Coravin, allow users to pour wine without removing the cork, significantly reducing wastage and enabling restaurants and wine bars to offer premium wines by the glass. Increasing consumer interest in premium wine experiences at home also supports adoption of these products.

Integration of digital features such as Bluetooth connectivity, automated pour measurement, recipe suggestions, and inventory tracking further enhances value and encourages consumers to upgrade from basic tools to smart barware ecosystems. As smart kitchen environments expand globally, demand for high-tech, app-enabled tools is expected to grow substantially, offering companies strong opportunities for innovation and brand leadership.

E-commerce expansion and experiential retailing in emerging markets

Rapid growth of online retail platforms across Asia Pacific, Latin America, and the Middle East & Africa is widening market access for bar and wine tools, particularly for premium brands that previously had limited physical distribution. Cross-border e-commerce allows consumers to purchase high-quality barware from global brands, while regional marketplaces collaborate with influencers, bartenders, and mixology experts to create curated collections and subscription kits.

Experiential retail formats are also gaining popularity, with retailers hosting live cocktail-making sessions, wine-tasting events, and in-store demonstrations that educate new consumers and drive higher-value purchases. These initiatives encourage upselling, improve category awareness, and help build customer loyalty. Combined with rising disposable incomes and modern retail expansion, these trends position emerging markets as major growth zones for value-added and premium-tier bar and wine tools.

Category-wise Analysis

Product Type Insights

Within the product type category, cocktail tools, especially shakers and jiggers, are estimated to contribute around 40% of total bar and wine tools revenue in the mid-2020s. This estimate is commonly referenced across industry market research reports and mixology equipment studies. The cocktail shaker segment is projected to grow at 5% annually, supported by rising demand for crafted cocktails across homes, bars, and hospitality venues. Multifunctional shakers with built-in strainers, ergonomic grips, and measurement markers attract both new consumers and trained bartenders. Additionally, the expansion of mixology courses, social-media cocktail content, and home-bar culture, as highlighted in trade publications such as the Beverage Trade Network, continues to boost demand for premium stirrers, jiggers, and bar sets.

Application Insights

Across different applications, restaurants and bar & wine shops together are expected to account for nearly 55% of global demand for bar and wine tools, based on consolidated insights from hospitality equipment market surveys and foodservice industry reports. Full-service restaurants and high-traffic bars rely on a wide set of tools, such as shakers, pourers, corkscrews, and wine-service accessories, to support diverse drink menus and maintain service efficiency. Meanwhile, specialized wine shops and tasting venues invest in premium glassware, preservation systems, and display-oriented tools to enhance customer experiences and drive upselling.

Distribution Channel Analysis

In terms of distribution channel performance, Online Channels are the fastest-growing segment, projected to capture about 35% of total sales by the early 2030s, according to trends reported by e-commerce retail analytics groups and consumer goods market research firms. Digital platforms provide wide product choices, customer reviews, and bundled bar or wine kits, making comparisons easier for both beginners and enthusiasts. Subscription boxes, influencer partnerships, and limited-edition drops further encourage repeat purchases and brand loyalty. While online sales rise sharply, offline specialty stores and department outlets continue to attract customers who prefer hands-on product evaluation, a trend consistently highlighted in omnichannel retail industry reports.

Regional Insights

North America Bar and Wine Tools Market Trends

North America stands out as one of the most mature and innovation-driven markets, supported by high per-capita alcohol consumption and a strong culture of premium wine and artisanal cocktails. The region hosts numerous craft cocktail bars, high-end restaurants, and wine-focused venues, boosting demand for advanced preservation systems, precision shakers, aerators, and other professional tools.

North America accounts for roughly 35% of global revenue in wine aerator categories. Regulatory standards emphasize safety, hygiene, and quality, which further increases demand for certified, food-grade bar tools. Innovation is a key competitive driver, with companies like Coravin continuously launching upgraded devices for still and sparkling wines. Robust e-commerce adoption, combined with widespread specialty retail networks, makes premium barware easily accessible to both consumers and hospitality businesses

Europe Bar and Wine Tools Market Trends

Europe’s bar and wine tools market is shaped by its strong wine-drinking heritage and well-developed cocktail culture, especially in countries such as France, Spain, Germany, and the U.K. High wine consumption per capita and the presence of numerous wine bars, restaurants, and tourism-driven hospitality venues sustain steady demand for corkscrews, preservation systems, and premium glassware.

European Union regulations on food-contact materials and product safety ensure that manufacturers adhere to strict quality standards, which benefits established and certified brands. Sustainability is gaining traction, particularly in Germany and Nordic countries, where demand for reusable, recyclable, and eco-friendly bar tools, such as stainless steel straws and bamboo accessories, is rising. This preference drives innovation in packaging and materials, further diversifying the premium and mid-range segments

Asia Pacific Bar and Wine Tools Market Trends

Asia Pacific is currently the fastest-growing region, driven by rising disposable incomes, urbanization, and the increasing influence of Western dining and drinking culture. Countries such as China, Japan, India, and those in ASEAN are witnessing strong growth in both home entertaining and commercial bar setups, particularly in metropolitan and emerging tier-2 cities. China remains a global manufacturing hub for bar and wine tools, enabling cost-effective production and extensive export activity.

Japan and South Korea are recognized for their craftsmanship and premium-quality bar tools and glassware. Rising penetration of modern retail formats and e-commerce platforms across the region is broadening consumer access to branded barware. As hospitality infrastructure expands and cocktail culture gains popularity, the Asia Pacific continues to be a major growth engine for the global market.

Competitive Landscape

The bar and wine tools market is moderately fragmented, with a mix of global brands, regional manufacturers, and numerous private-label and unbranded suppliers competing across price tiers. Leading players differentiate through design aesthetics, premium materials, patented preservation technologies, and curated product bundles targeting both professional and home users. Companies are investing in new product development, such as electric corkscrews, multi-functional bar sets, and advanced preservation devices, while expanding distribution via specialty retail, e-commerce, and hospitality partnerships to capture higher-value segments.

Key Market Developments:

- In January 2025, Coravin introduced updated Timeless and Pivot systems with enhanced aeration and preservation accessories, targeting premium home and on-trade wine-by-the-glass programs.

- In June 2024, Trudeau Corporation expanded its barware collection with new stainless-steel cocktail tools and insulated wine tumblers, focusing on design-driven products for North American retailers.

- In November 2023, John Lewis & Partners reported strong seasonal demand for curated barware and wine accessory gift sets across U.K. stores and online, highlighting the growing importance of gifting occasions for market growth.

Companies Covered in Bar and Wine Tools Market

- John Lewis & Partners

- Morris & Co.

- Alessi

- Vinturi

- Metrokane (Taylor Precision)

- Vintorio

- Zazzol

- Soireehome

- Aervana

- Tribellawin

- Vita Saggia

- Shenzhen Sinowin Wine Accessories

- Zhuhai Kelitong Electronic

- Trudeau Corporation

- Coravin

Frequently Asked Questions

The global bar and wine tools market is projected to reach around US$ 4.6 Billion by 2033, growing at a CAGR of about 5.9% between 2026 and 2033.

Key demand drivers include rising global wine and cocktail consumption, expansion of home bars and at‑home entertaining, and increasing adoption of premium and technologically advanced tools in both home and commercial settings.

Cocktail tools such as shakers, strainers, and jiggers hold the leading share of the market, accounting for roughly 35% of global revenue due to their essential role in preparing a wide variety of drinks.

North America commands a significant share, supported by high per‑capita wine consumption, a dense network of bars and restaurants, and strong uptake of advanced wine accessories and preservation systems.

A major opportunity lies in premium and smart bar and wine tools, including sophisticated wine preservation systems, connected devices, and eco‑friendly materials that deliver higher margins and align with evolving consumer preferences.

Prominent players include John Lewis & Partners, Morris & Co., Alessi, Vinturi, Metrokane (Taylor Precision), Trudeau Corporation, Coravin, Vintorio, Zazzol, and several regional manufacturers and private‑label brands serving different price tiers.