- Beverages

- Canned Wine Market

Canned Wine Market Size, Share, Growth, and Regional Forecast, 2026 to 2033

Canned Wine Market by Product Type (Sparkling Wine, Still White Wine, Still Red Wine, Rosé), by Nature (Alcoholic, Non-Alcoholic), by Sales Channel (Hypermarkets/Supermarkets, Wine shops & liquor stores, Convenience Stores, Bars and Restaurants, Online Retail, Others), by Regional Analysis, 2026-2033

Canned Wine Market Share and Trends Analysis

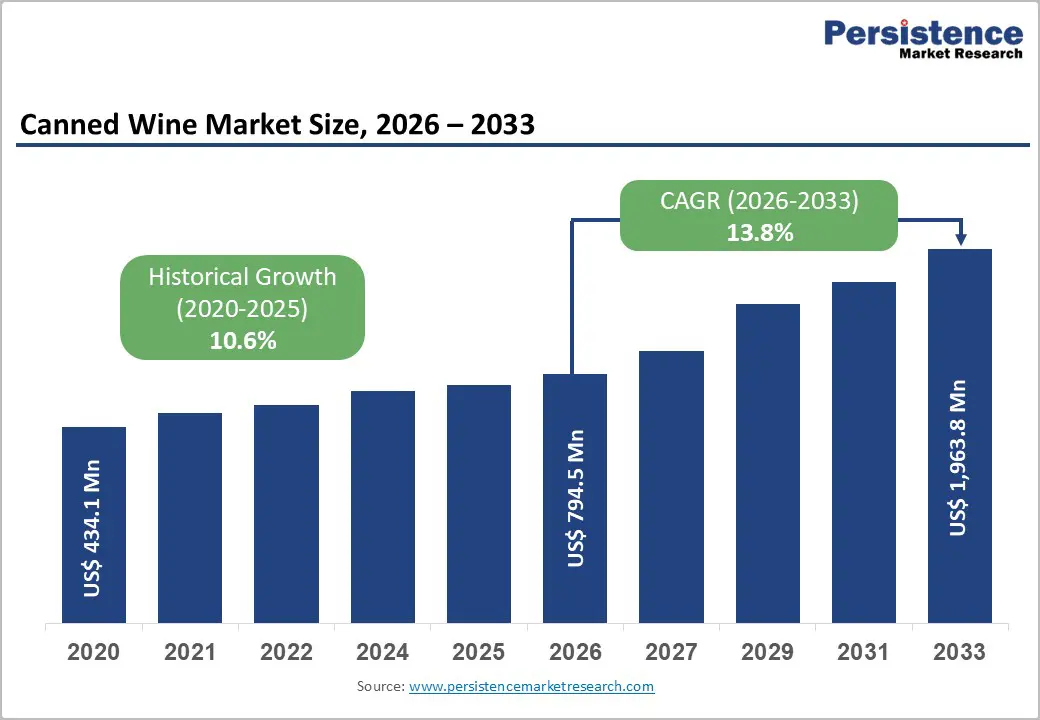

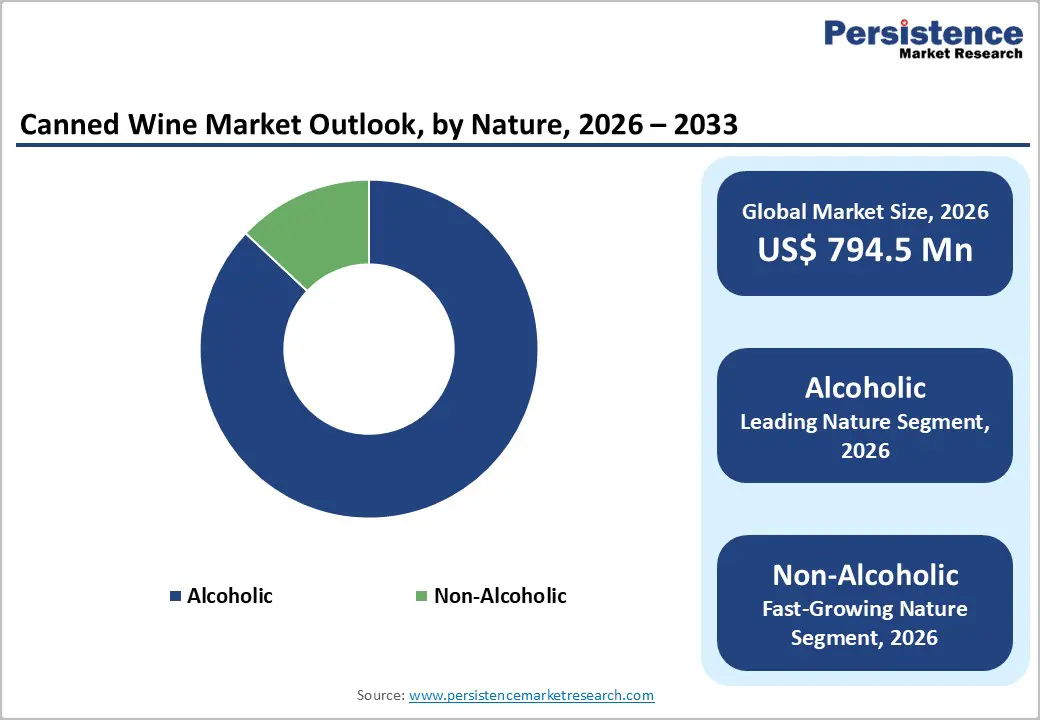

The global canned wine market size is expected to be valued at US$ 794.5 million in 2026 and projected to reach US$ 1,963.8 million by 2033, growing at a CAGR of 13.8% between 2026 and 2033

The market is experiencing a significant transformation driven by the rising demand for convenience and the widespread adoption of single-serve packaging formats among younger demographics. This growth is underpinned by the increasing frequency of outdoor social gatherings, where portable and unbreakable containers are preferred over traditional glass bottles. Furthermore, the shift toward sustainable packaging solutions has positioned aluminum cans as a superior choice due to their high recyclability and lower carbon footprint during transportation.

Key Industry Highlights

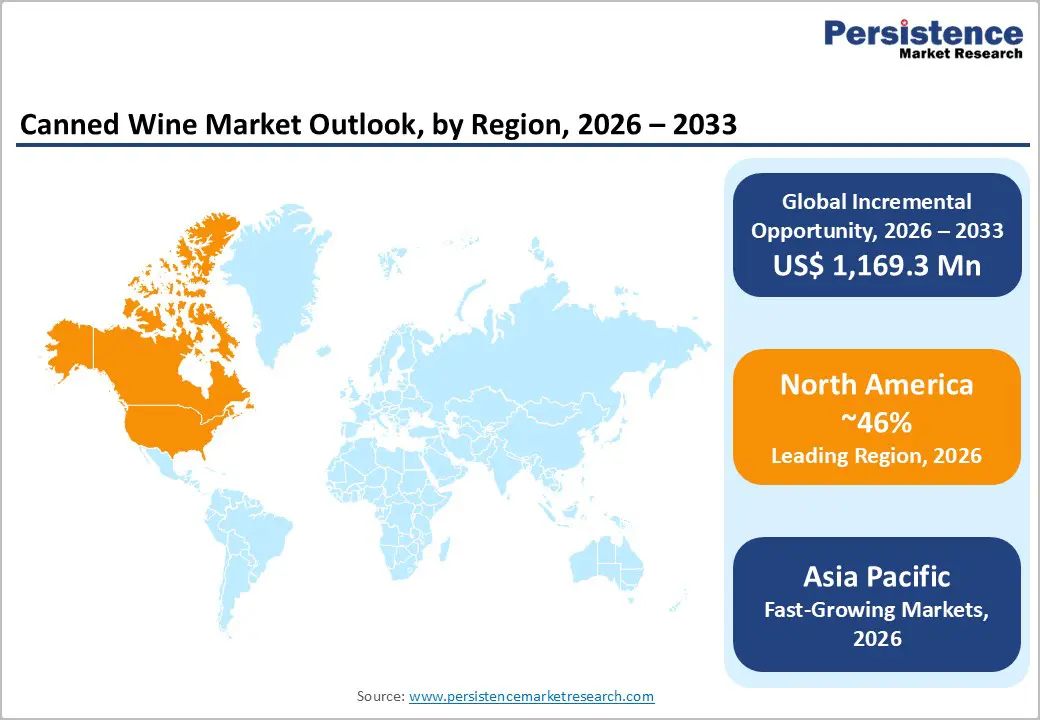

- Leading Region: North America leads the global Canned Wine market with a 46% share, supported by early adoption of alternative wine formats, regulatory flexibility, and a strong outdoor and convenience-driven consumption culture.

- Fastest-Growing Region: Asia Pacific is the fastest-growing regional market, driven by urbanization, rising middle-class incomes, and openness to non-traditional wine packaging.

- Fastest-Growing Nature Segment: Non-alcoholic canned wine is the fastest-growing nature segment, propelled by wellness trends, alcohol moderation movements, and improved de-alcoholization technologies.

- Dominant Nature Segment: Alcoholic canned wine dominates the market due to entrenched consumer perceptions of wine as a social alcoholic beverage and strong availability across mainstream retail.

- Market Drivers: Shifting consumer lifestyles favor lightweight, single-serve, and glass-free packaging suited for outdoor activities, travel, and informal social settings.

- Key Developments: In January 2026, Gratsi announced a record-breaking 2025, selling 350,000 nine-liter cases and ranking as the fastest-growing boxed wine brand in the U.S., reinforcing premiumization and alternative-format momentum; In September 2025, French Bloom, the non-alcoholic sparkling wine brand backed by Moët Hennessy, partnered with Formula 1 to elevate global visibility and premium lifestyle positioning.

| Key Insights | Details |

|---|---|

| Canned Wine Market Size (2026E) | US$ 794.5 Mn |

| Market Value Forecast (2033F) | US$ 1,963.8 Mn |

| Projected Growth (CAGR 2026 to 2033) | 13.8% |

| Historical Market Growth (CAGR 2020 to 2025) | 10.6% |

Market Dynamics

Driver – Rising Consumer Preference for Portability and Convenience in Outdoor Settings

The primary driver of the Canned Wine Market is the evolving lifestyle of Millennial and Gen Z consumers who prioritize convenience and mobility. Traditional wine consumption was often tethered to formal settings requiring corkscrews and glassware; however, the canned format eliminates these barriers, making wine accessible for picnics, music festivals, hiking, and sporting events. According to data from the Wine Institute, the volume of wine consumed in non-traditional venues has seen a steady increase, as aluminum cans are lighter and less fragile than glass. This transition is further supported by the International Air Transport Association (IATA), which notes that airlines are increasingly adopting canned beverages to reduce weight and simplify onboard service. The ability to chill cans faster than bottles also appeals to spontaneous social drinkers, solidifying the product's place in the modern "on-the-go" beverage portfolio.

Restraints – Regulatory Hurdles and Standardized Packaging Constraints

The Canned Wine Market faces complex regulatory challenges that vary significantly by region. In the United States, the Tax and Trade Bureau (TTB) previously had strict regulations on "standards of fill," which limited the sizes in which wine could be sold, although some of these rules were relaxed in 2020 to allow 355ml cans. However, in Europe, the European Commission maintains rigorous labeling and volume standards that can complicate cross-border trade for smaller producers. Furthermore, strict alcohol advertising laws in countries like France (under Loi Évin) and high excise taxes on "ready-to-drink" (RTD) products in parts of Asia and the Middle East can inflate prices, making canned wine less competitive against beer or local spirits.

Opportunity – Expansion into On-Premise Venues and Travel Retail Channels

There is a substantial opportunity for market participants to penetrate the HoReCa (Hotels, Restaurants, and Cafes) and travel retail sectors. Hotels and beach resorts are increasingly looking for glass-free options for poolside service to ensure safety without compromising on the beverage experience. Additionally, the recovery of global tourism, as highlighted by World Tourism Organization (UNWTO) reports, suggests a resurgence in demand at airports and train stations. Canned wine is perfectly suited for these environments due to its ease of storage and speed of service. Producers can leverage this by creating "Barista" or "Sommelier-selected" canned ranges specifically for high-end hospitality. Strategic partnerships with outdoor stadium operators and concert organizers, such as Live Nation, can also provide high-volume sales opportunities that were previously dominated exclusively by the beer industry.

Category-wise Analysis

By Nature, alcoholic canned wine dominates the global market

In terms of nature, the Alcoholic segment held a commanding leading position with a 87% market share in 2025. Most consumers still view wine primarily as an alcoholic beverage for social relaxation, and established brands have focused their production lines on traditional wine varieties. However, the Non-Alcoholic segment is the fastest-growing category during the forecast period. Driven by a global shift toward wellness and the "Dry January" movement, the demand for zero-proof wine has surged. The World Health Organization (WHO) has been active in promoting reduced alcohol consumption, which has influenced consumer behavior toward "zero-proof" alternatives. Modern de-alcoholization processes have improved significantly, allowing brands to retain the aromatic profiles of the grapes. This segment is expected to see a 16.8% CAGR as technological advancements allow for better flavor retention and as more "lifestyle" brands enter the market to cater to the health-conscious Gen Z demographic.

By sales channel, online retail is expected to show promising growth in the global market

Hypermarkets/Supermarkets represent the leading sales channel for the Canned Wine Market, accounting for over 48% of the total revenue in 2025. The ability of large retailers like Walmart, Tesco, and Carrefour to offer diverse brand selections and competitive pricing through bulk purchasing makes them the primary destination for the average consumer. These outlets also provide high visibility for new product launches through end-cap displays. On the other hand, the Online Retail segment is the fastest-growing sales channel expected to grow at CAGR of 15.4%. The convenience of home delivery, the rise of wine subscription services like Maker Wine, and the ability to read peer reviews have shifted consumer habits. Post-pandemic data indicates that e-commerce in the alcohol sector is not just a temporary trend but a structural change. Direct-to-consumer (DTC) models allow boutique wineries to bypass traditional distribution tiers, offering unique canned selections directly to a loyal fan base, which is particularly effective for the niche and premium canned wine segments.

Region-wise Insights

North America Canned Wine Market Trends and Insights

North America is the undisputed leader in the global Canned Wine Market, holding a dominant 46% market share in 2025. The region's leadership is anchored by the United States, where the "craft" beverage movement first seen in beer has successfully transitioned to wine. The U.S. Tax and Trade Bureau (TTB)'s 2020 amendment to standards of fill was a pivotal moment, allowing the popular 355ml (12 oz) can size to be sold individually, which aligned the product with standard soda and beer packaging.

Innovation in this region is led by both massive conglomerates like E. & J. Gallo Winery and Constellation Brands, and nimble startups in California, Oregon, and Washington. The innovation ecosystem in Silicon Valley and the Napa Valley has led to the development of premium canned wines that challenge the "low quality" stigma. Consumers in this region are particularly responsive to the sustainability narrative, with many West Coast wineries moving toward Certified Sustainable and B-Corp statuses. The prevalence of outdoor recreation—from National Park visits to tailgating at NFL games provides a consistent and growing demand for portable wine solutions.

Asia Pacific Canned Wine Market Trends and Insights

Asia Pacific is identified as the fastest-growing region in the Canned Wine Market for the 2025-2032 period. This growth is fueled by the rapid urbanization of China, India, and ASEAN countries, where a burgeoning middle class is adopting Western consumption patterns. Unlike Europe, many Asian markets do not have a centuries-old "bottle culture," making consumers more open to innovative packaging like cans. In Japan, companies like Suntory Holdings Limited have already seen massive success with "Highball" cans and are now successfully pivoting to canned wine spritzers and still wines to cater to solo drinkers and the "convenience store culture."

The region also benefits from significant manufacturing advantages, with Australia and New Zealand serving as major production hubs that export canned products across the continent. In China, the rise of social media platforms like TikTok and Little Red Book has made aesthetic, "Instagrammable" cans a hit among young urban professionals. Furthermore, the high prevalence of e-commerce and mobile payment systems in Asia Pacific facilitates the rapid growth of the Online Retail channel, allowing international brands to reach inland cities without the need for extensive physical footprints.

Market Competitive Landscape

The Canned Wine Market currently exhibits a fragmented structure with a blend of global beverage giants and specialized boutique producers. Major players such as E. & J. Gallo Winery, Constellation Brands, and Treasury Wine Estates are using their vast resources to acquire successful canned brands or launch canned versions of their flagship labels (e.g., Dark Horse, 19 Crimes). These companies focus on scale, utilizing their existing supply chains to place products in thousands of Supermarkets and Convenience Stores.

Conversely, smaller entities like Maker Wine and Sans Wine Co. are employing a "premiumization" strategy, focusing on high-quality, vintage-dated, and single-vineyard wines in cans to differentiate themselves from "bulk" competitors. Emerging business model trends include a focus on DTC (Direct-to-Consumer) and subscription-based services, which foster brand loyalty through storytelling and exclusive releases. R&D efforts are heavily concentrated on internal can liners that preserve the delicate pH and sulfite levels of wine, ensuring a shelf life that competes with bottled alternatives.

Key Developments:

- In January 2026, Gratsi, a premium Mediterranean wine brand redefining the boxed wine segment, announced the completion of a record-breaking 2025, selling 350,000 nine-liter cases and ranking as the fastest-growing boxed wine brand in the U.S., reinforcing premiumization and format innovation trends within the wine market.

- In September 2025, French Bloom, the first non-alcoholic sparkling wine brand backed by Moët Hennessy entered a strategic partnership with Formula 1, strengthening its premium positioning and global brand visibility within high-income, lifestyle-driven consumer segments.

- In August 2025, AFicioNAdo™, the world’s first professional training and certification program dedicated to alcohol-free and non-alcoholic adult beverages announced the launch of AFNA Wine Certified™, establishing a formal quality and education benchmark for the rapidly expanding non-alcoholic wine category.

Companies Covered in Canned Wine Market

- Constellation Brands

- Treasury Wine Estates

- E. & J. Gallo Winery

- Diageo PLC

- Brown-Forman Corporation

- LVMH

- Pernod Ricard

- Sans Wine Co.

- Suntory Holdings Limited

- Maker Wine

- Union Wine Company

- Others

Frequently Asked Questions

The global Canned Wine market is projected to be valued at US$ 794.5 Mn in 2026.

The demand is primarily driven by the need for portability and convenience in outdoor settings like festivals and beaches, as well as a growing consumer emphasis on packaging sustainability and recyclability.

The Global Canned Wine market is poised to witness a CAGR of 13.8% between 2025 and 2032

Key opportunities include the expansion of Non-Alcoholic canned wines to meet health trends and the penetration of travel retail and on-premise venues that require glass-free packaging.

The market features industry giants like Constellation Brands, E. & J. Gallo Winery, and Treasury Wine Estates, alongside specialized premium players like Maker Wine and Sans Wine Co.