- Technology

- Veterinary Software Market

Veterinary Software Market Size, Share, and Growth Forecast for 2025 - 2032

Veterinary Software Market Size, Share and Growth Forecast by Product(Practice Management Software, Imaging Software), by Delivery Mode(On-premise, Cloud/Web-based), by Practice Type(Small Animals, Mixed Animals, Equine, Food-producing Animals), by End Use(Hospitals/Clinics, Reference Laboratories), and Regional Analysis

Veterinary Software Market Size and Share Analysis

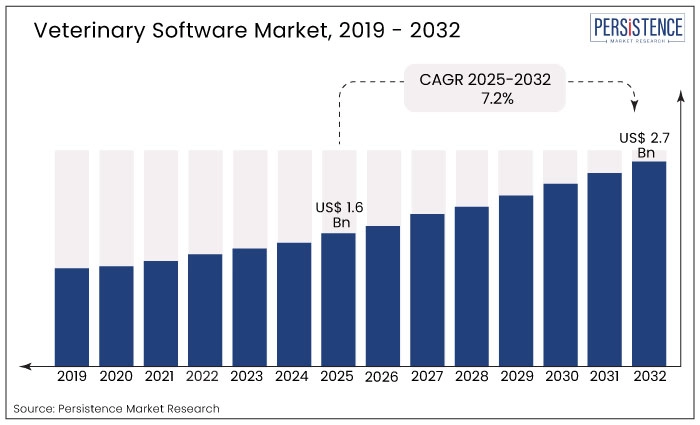

The global veterinary software Market is forecast to expand at a CAGR of 7.2% and thereby increase from a value of US$ 1.6 Bn in 2025 to US$ 2.7 Bn by the end of 2032.

|

Attributes |

Key Insights |

|

Market Size (2025E) |

US$ 1.6 Bn |

|

Projected Market Value (2032F) |

US$ 2.7 Bn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

7.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2024) |

7.1% |

|

Revenue Share of Top Four Countries (2024E) |

45% |

Market Introduction and Definition

Veterinary software comprises specialized computer programs that are intentionally developed to optimize and augment diverse facets of veterinary practice administration. These all-encompassing solutions comprise patient records, appointment scheduling, billing, and inventory administration, with the overarching goal of enhancing operational effectiveness and healthcare provision in veterinary clinics. By incorporating sophisticated technologies, including data analytics and cloud-based systems, veterinary software enables efficient data-driven decision-making and communication, which ultimately contributes to the provision of superior pet care.

The worldwide market for veterinary software market is expanding rapidly due to a number of significant factors. The demand for advanced veterinary management tools is stimulated by the rising awareness of pet healthcare and the increasing adoption rates of pets. Enhanced patient care via electronic health records, the automation of administrative tasks, and the incorporation of telemedicine solutions all contribute to the expansion of the market. Furthermore, the increasing prevalence of emergency and specialty veterinary services drives the implementation of advanced software solutions. Technological progress, including the integration of artificial intelligence and Internet of Things (IoT) functionalities into veterinary software, significantly influences the trajectory of the market by presenting novel approaches to enhanced diagnostics and treatment.

Market Growth Drivers

Incorporation of State-Of-The-Art Technologies

Technological advancements are a significant catalyst for the global veterinary software market to enter a new era characterized by enhanced efficiency, accuracy, and comprehensive pet care. The incorporation of state-of-the-art technologies, including artificial intelligence (AI) and the Internet of Things (IoT), significantly influences the restructuring of veterinary practice administration.

A paradigm shift is imminent with the incorporation of artificial intelligence into veterinary software, which significantly improves diagnostic capabilities and treatment planning. By training AI algorithms on extensive datasets of veterinary information, software systems are empowered to analyze intricate patterns present in patient data. The application of this analytical capability not only accelerates the detection of illnesses but also aids in the prognostication of possible health complications by leveraging past data. These insights can be utilized by veterinary professionals to develop proactive healthcare strategies, individualized treatment plans, and preventative measures. As an illustration, medical image analysis such as X-rays and MRIs can be expedited and rendered more precise by AI-powered diagnostic tools, which ultimately result in opportune interventions and enhanced patient prognoses. The implementation of AI in veterinary practices yields substantial efficiency improvements, which in turn promote the development of a culture that values and implements evidence-based decision-making.

Market Restraints

Difficulty of Achieving Interoperability

An important factor that restricts the growth of the worldwide veterinary software industry is the difficulty of achieving interoperability. As veterinary practices proliferate in their adoption of various software solutions to optimize their operations, a significant obstacle emerges in the form of imperfect integration and communication among distinct platforms. When veterinary software systems, developed by disparate vendors, encounter challenges in efficiently exchanging and interpreting data, interoperability concerns emerge. Critical information, including patient records, diagnostic outcomes, and treatment strategies, cannot be exchanged efficiently due to software application incompatibilities.

Mounting Apprehension Regarding Data Security

An increasingly significant obstacle confronting the worldwide veterinary software market industry is the mounting apprehension regarding data security. With the growing dependence of veterinary practices on digital platforms for the management of sensitive patient information, the implementation of strong cybersecurity protocols becomes critical. The substantial volumes of personal and medical data stored, in conjunction with the interconnected nature of veterinary software systems, render them appealing targets for cyber threats. Protecting proprietary veterinary practice data, financial information, and confidential patient records from unauthorized access, data breaches, or malevolent activities constitutes a significant challenge.

Opportunities

Strategic Incorporation of Telemedicine

One of the most significant trends influencing the worldwide veterinary software market is the strategic incorporation of telemedicine, which is bringing about a paradigm shift in the way veterinary services are provided and broadening the scope of the sector. Telemedicine, which is enabled by sophisticated veterinary software solutions, has the potential to revolutionize the provision of pet healthcare, presenting practitioners and pet owners with unparalleled prospects.

The veterinary field has undergone a fundamental transformation with the introduction of telemedicine, which facilitates remote consultations, diagnostics, and follow-ups. Telemedicine functionalities integrated into veterinary software platforms enable practitioners to conduct virtual consultations, thereby overcoming geographical limitations and providing accessibility to a wider community of pet owners. Pet owners, in turn, experience the advantages of obtaining expert veterinary advice from the comfort of their residences, thereby mitigating the strain placed on their animals during journeys and visits to clinics. Not only does this paradigm shift improve the overall customer experience, but it also provides veterinary practices with access to new revenue streams and a greater market share that extends beyond their immediate physical reach.

Analyst’s Viewpoint

The worldwide veterinary software is positioned for significant expansion, propelled by a number of pivotal factors that influence the industry's dynamics. An essential determinant driving market growth is the escalating global pet ownership rate and the subsequent surge in awareness regarding pet healthcare. The adoption of companion animals by households leads to a concomitant increase in the need for sophisticated veterinary services and administration tools, including diagnostic solutions and practice management software.

The increased consciousness of this matter is causing a fundamental change in the field of veterinary care, which is placing greater emphasis on holistic and preventative medicine for animals. As a result, the implementation of cutting-edge software solutions is gaining momentum. The correlation between veterinary software manufacturers and consumers significantly influences the sales dynamics of the latter. There is a growing trend among manufacturers to prioritize customization options, user-friendly interfaces, and interoperability in order to cater to the varied requirements of veterinary professionals.

The integration of software developers and veterinarians into the software development process guarantees a smooth and uninterrupted flow of operations for clinics and institutions. By promoting collaboration, veterinary practices are able to not only increase their efficiency but also cultivate a favorable user experience. Manufacturers are allocating resources towards ongoing research and development, integrating state-of-the-art technologies such as cloud computing and artificial intelligence, in order to maintain a competitive advantage in the market and satisfy the changing needs of consumers. In addition, rising investments in animal health research are anticipated to stimulate expansion in the worldwide veterinary software market.

In the pursuit of remaining informed about the most recent advancements in diagnostics and treatment modalities, veterinary professionals require software solutions that enable research collaboration and data-driven decision-making. The incorporation of artificial intelligence and big data analytics into veterinary software will be instrumental in elucidating insights from enormous datasets, thereby making significant contributions to the progress of personalized medicine for animals.

Supply-side Dynamics

The worldwide veterinary software industry is characterized by the existence of significant actors who propel market share and innovation. Prominent entities including IDEXX Laboratories, Henry Schein, Inc., and Covetrus, among others, provide all-encompassing software solutions for veterinary practice administration and healthcare delivery that address a wide range of requirements. These industry leaders hold a substantial portion of the market due to their extensive range of products, ongoing commitment to research and development, and strategic partnerships within the sector.

North American nations, with Canada and the United States being in particular prominent in their adoption of veterinary software solutions. The prevalence of advanced software in these regions can be attributed to several factors, including a durable veterinary care infrastructure, significant pet ownership rates, and a technologically proficient populace. To illustrate, veterinary clinics in the United States utilize practice management software such as Cornerstone, which was developed by IDEXX Laboratories. This software is employed to optimize administrative processes, expedite workflows, and improve the quality of patient care. Another influential entity that is propelling change is Covetrus, which emphasizes interoperability and collaborative care. Covetrus promotes a holistic approach to veterinary care through the development of software that integrates seamlessly with diagnostic instruments and other healthcare systems. These prominent entities are not only establishing benchmarks within the industry but also exerting an impact on worldwide patterns, promoting a transition towards all-encompassing, data-centric, and technologically sophisticated solutions within the veterinary software sector. Their ongoing strategic initiatives and persistent innovation make substantial contributions to the ever-changing market dynamics, thereby guaranteeing the market's expansion and pertinence in the swiftly progressing domain of veterinary healthcare.

Top Regional Markets

Why is North America Emerging as a Dominating Region?

Heightened Technological Advanced and Increased Rate of Pet Ownerships to Promote Growth

With the highest potential market share, North America is positioned to dominate the worldwide veterinary software industry. The aforementioned supremacy can be ascribed to the region's well-developed healthcare infrastructure, substantial rates of pet ownership, and early integration of technological advancements within veterinary clinics. Hospitals and veterinary clinics across North America are currently leading the way in the integration of all-encompassing software designed to facilitate patient care, diagnostics, and practice management. Due to its firmly established veterinary care sector and its significant focus on animal health and welfare, North America is positioned as a prominent contributor to the worldwide veterinary software market. In addition to a strong regulatory framework and a culture of ongoing innovation, the presence of key market participants further solidifies North America's position as the market share leader.

What Opportunities Lie in East Asia for Manufacturers?

Accelerated Pet Ownership and Widened Urbanization to Provide Revenue

It is expected that East Asia will witness the most rapid expansion of the worldwide veterinary software . A growing consciousness regarding the well-being of pets, accelerated economic growth, and urbanization all contribute to the escalating need for sophisticated veterinary software solutions in the region. The increasing prevalence of pet ownership in East Asian nations (China, Japan, in particular) has generated a burgeoning demand for digital tools that augment veterinary services. Accelerating technological adoption in veterinary practices is the result of implementation of cloud-based solutions, the incorporation of artificial intelligence, and the digitization of healthcare processes. Due to its ever-changing market conditions and increasing investment in pet care, East Asia is well positioned to experience the most rapid expansion in the veterinary software industry. As a result, the region will have a significant impact on the trajectory of the sector.

Competitive Intelligence and Business Strategy

Prominent entities in the worldwide veterinary software industry, including IDEXX Laboratories, Henry Schein, Inc., and Covetrus, maintain and increase their market presence through the implementation of diverse and comprehensive strategies. An integral component of their methodology is an unwavering commitment to innovation. These organizations make consistent investments in research and development in order to introduce state-of-the-art technologies to the field of veterinary software. As an example, IDEXX Laboratories has emerged as a leader in the integration of artificial intelligence (AI) into its platforms, thereby propelling progress in personalized pet care and augmenting diagnostic capabilities.

Strategic collaborations and partnerships are essential elements in the market share expansion strategies of the dominant actors. Through strategic partnerships with pharmaceutical companies and manufacturers of diagnostic instruments, these entities establish all-encompassing ecosystems that effectively address the varied requirements of veterinary practitioners. By offering integrated solutions through strategic partnerships with multiple software developers and healthcare service providers, Henry Schein, Inc. has strengthened its market position and provided veterinary practices with a one-stop-shop. Moreover, these participants place a premium on customer-centric solutions. Recognizing the distinct obstacles encountered by veterinarians, they develop software that not only satisfies regulatory mandates but also attends to the routine operational necessities of hospitals and clinics.

Key Recent Developments

New Product

In October 2022, LifeLearn Animal Health, an online veterinary software provider, announced the full integration of ClientEd, a client education resource that increases pet owner compliance and saves practices time, into Shepherd's veterinary practice management software.

Market Impact: The October 2022 implementation of ClientEd by LifeLearn Animal Health into the veterinary practice management software of Shepherd represents a significant development in the worldwide veterinary software industry. This advancement improves the operational capabilities of veterinary practice management systems through the integration of an all-encompassing client education resource, thereby encouraging greater adherence from pet owners. By means of easily accessible and educational resources, the integration not only streamlines the productivity of veterinary practices, but also demonstrates the industry's dedication to improving the quality of pet healthcare as a whole.

Veterinary Software Market Research Segmentation

By Product:

- Practice Management Software

- Imaging Software

By Delivery Mode:

- On-premise

- Cloud/Web-based

By Practice Type:

- Small Animals

- Mixed Animals

- Equine

- Food-producing Animals

- Others

By End Use:

- Hospitals/Clinics

- Reference Laboratories

By Region:

- North America

- Europe

- East Asia

- South Asia & Oceania

- Latin America

- Middle East & Africa

Companies Covered in Veterinary Software Market

- IDEXX Laboratories, Inc.

- Hippo Manager Software, Inc.

- Antech Diagnostics, Inc. (Mars, Inc.)

- Esaote SpA

- Henry Schein, Inc.

- Patterson Companies, Inc.

- ClienTrax

- Digitail Inc

- Vetspire LLC (Thrive Pet Healthcare)

- DaySmart Software

Frequently Asked Questions

The market is anticipated to grow at a CAGR of 7.2% during the projected period.

The Veterinary Software market size will be valued at USD 1.6 billion in 2025.

The United States will held the largest market share in 2025.

The prominent players in the market are IDEXX Laboratories, Inc., Hippo Manager Software, Inc., Antech Diagnostics, Inc. (Mars, Inc.), Esaote SpA, and Henry Schein, Inc., among others.

The reference laboratories segment is expected to grow at the fastest growth during the forecast period.