- Animal Health

- Veterinary Parasiticides Market

Veterinary Parasiticides Market Size, Trends, Share, and Growth Forecast, 2026 - 2033

Veterinary Parasiticides Market by Product Type (Ectoparasiticides, Endoparasiticides, Endectocides), Route of Administration (Oral, Injectable, Topical), Animal Type (Companion, Livestock), and Regional Analysis for 2026 - 2033

Veterinary Parasiticides Market Share and Trends Analysis

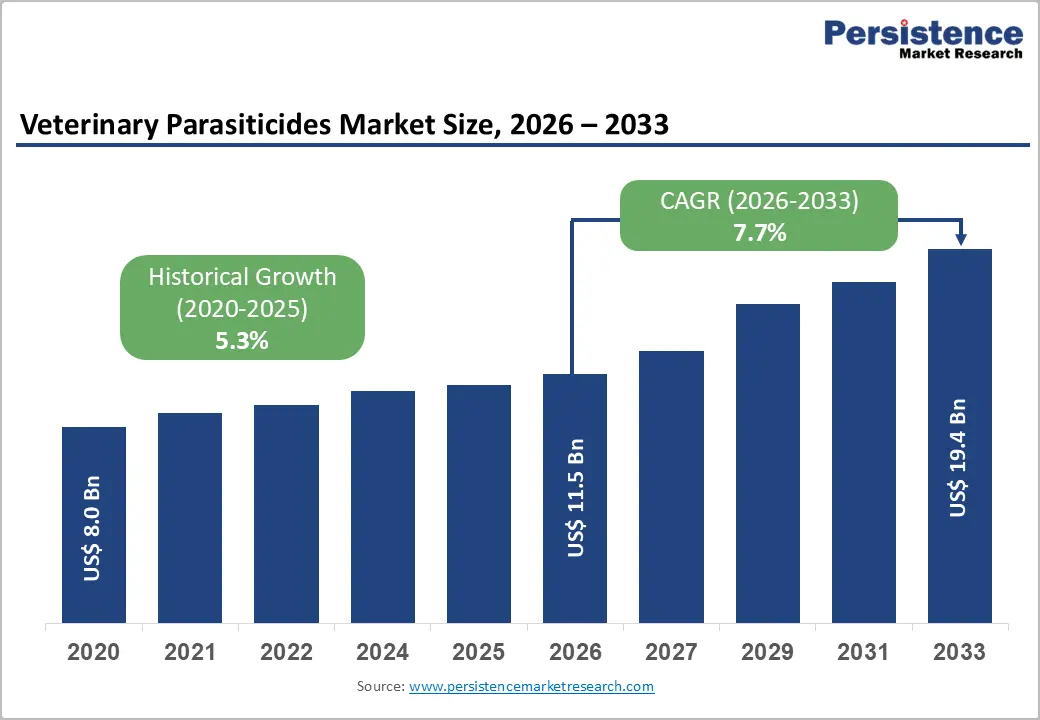

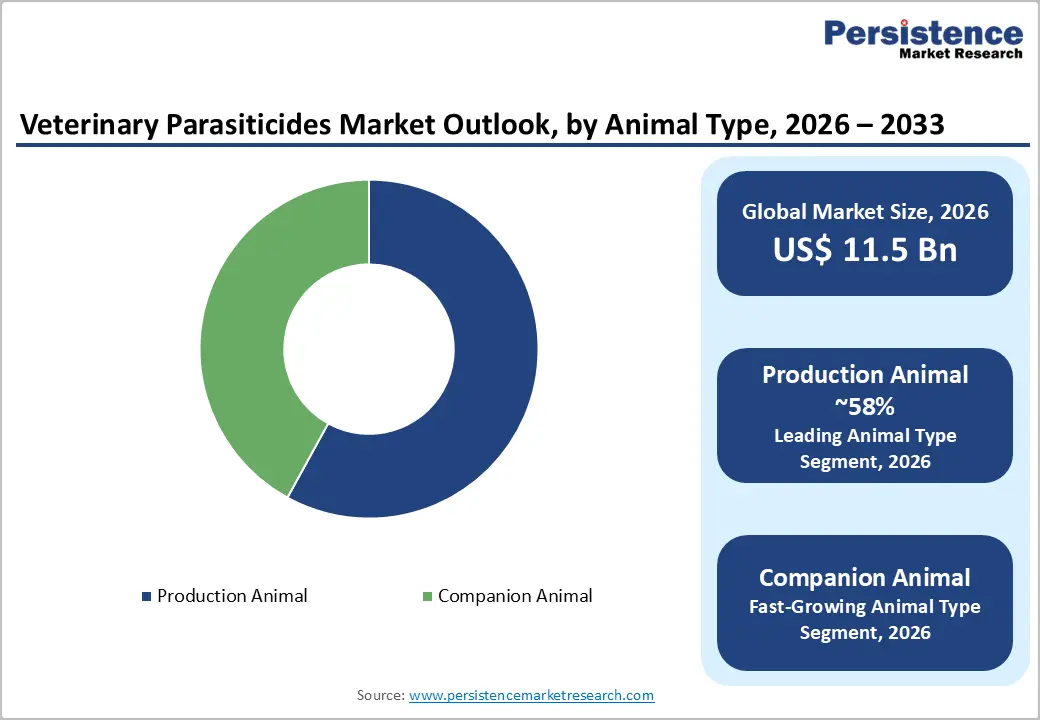

The global veterinary parasiticides market size is likely to be valued at US$ 11.5 billion in 2026, and is projected to reach US$ 19.4 billion by 2033, growing at a CAGR of 7.7% during the forecast period 2026−2033.

The growth trajectory of the market is underpinned by the escalating global burden of parasitic infestations in both companion and livestock animals, rising pet ownership rates across developed and emerging economies, and the growing regulatory emphasis on food safety and zoonotic disease prevention. Technological innovation in drug delivery systems, the advancement of combination parasiticide products, and the expanding availability of novel active pharmaceutical ingredients continue to redefine the competitive landscape.

Key Industry Highlights

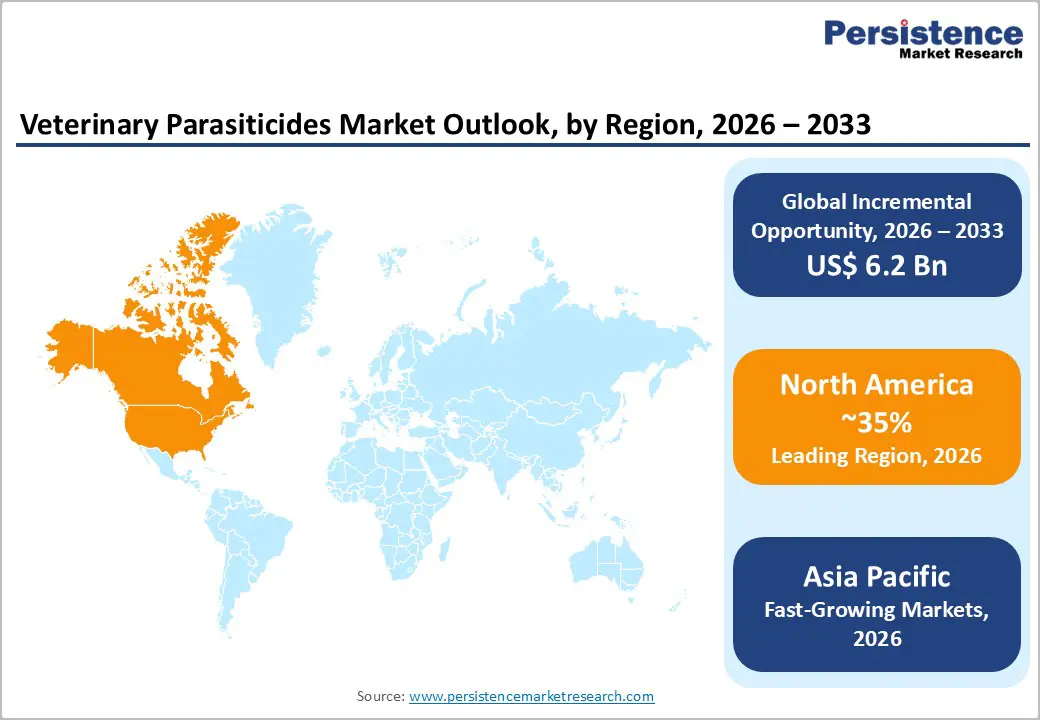

- Dominant Region: North America is expected to command about 38% market share in 2026, supported by strong awareness of animal health and a well-developed veterinary care system.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing from 2026 to 2033, powered by rising pet adoption rates, increasing disposable income, and the growing livestock industry.

- Dominant Product Type: Ectoparasiticides are anticipated to dominate by commanding approximately 48% of the revenue share in 2026, owing to their widespread use against fleas, ticks, and mites in both companion and livestock animals.

- Fastest-growing Product Type: Endectocides are likely to be the fastest-growing segment during the 2026-2033 forecast period, as they offer a comprehensive approach to parasite control within a single treatment.

- Market Opportunities: Emerging markets in Asia Pacific and Latin America offer growth through livestock modernization and urban pet adoption, supported by rising incomes.

| Key Insights | Details |

|---|---|

|

Veterinary Parasiticides Market Size (2026E) |

US$ 11.5 Bn |

|

Market Value Forecast (2033F) |

US$ 19.4 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

7.7% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

DRO Analysis

Rising Global Pet Ownership and Increased Companion Animal Healthcare Spending

The exceptional rise in companion animal ownership worldwide is fundamentally reshaping the veterinary parasiticides market growth. Pet-keeping is no longer a niche activity it is now a mainstream lifestyle choice across many countries, especially in North America, Europe, and Asia Pacific. As more households bring dogs and cats into their homes, demand for regular healthcare services grows, and parasite prevention moves from an occasional need to a routine requirement. Owners increasingly treat pets as family members, which means they are less willing to accept discomfort or illness from fleas, ticks, or intestinal worms. This mindset shift is pushing veterinary clinics and retailers to offer a broader range of reliable, easy-to-use parasiticides that fit into everyday pet-care routines.

As pet humanization continues to deepen, owners are actively choosing higher-quality products rather than basic or low-cost options. They prefer prescription-grade treatments and premium-quality over-the-counter (OTC) formulations that promise better safety, longer protection, and fewer side effects. This demand for premium products is encouraging manufacturers to invest in innovative delivery formats, such as flavored chewables, long-acting spot-ons, and combined parasite-control regimens. These products do not only control common pests but also simplify dosing and reduce the risk of missed treatments. The market is evolving from a volume-driven, low-margin segment into a value-driven space where brands, trust, and clinical evidence matter more than simple price. This structural change is expanding the total addressable market for veterinary parasiticides and creating new opportunities for differentiated, science-backed solutions.

Growing Livestock Population and Food Safety Imperatives

Expanding global demand for animal-derived proteins is pushing farmers to manage larger and more intensive livestock operations, which in turn increases reliance on antiparasitic treatments in food-producing animals. As meat, milk, and egg consumption grow, producers are under constant pressure to maintain healthy herds and flocks while maximizing productivity. Parasites that affect the digestive tract, skin, or blood can significantly reduce feed efficiency, weight gain, and milk yield, so routine use of parasiticides becomes a necessary part of modern farm management. This shift is turning parasiticides from a reactive treatment into a core component of herd-health and biosecurity protocols on commercial units.

Regulatory bodies are tightening oversight of veterinary medicines, which is shaping how parasiticides enter the market and how farmers use them. Frameworks such as the European Union Veterinary Medicinal Products Regulation (EU VMPR) and the United States Food and Drug Administration Center for Veterinary Medicine (FDA CVM) guidelines emphasize approved, evidence-based use of parasiticides, especially in species that contribute to the food supply. These rules require safer residue profiles, clear withdrawal periods, and responsible use to minimize the risk of resistance and environmental impact. As a result, the market is moving toward compliant, registered products rather than informal or off-label treatments, which expands the formal, regulated commercial space for veterinary parasiticides and encourages innovation in safer, more targeted antiparasitic solutions.

Growing Antiparasitic Resistance and Regulatory Stringency

Antiparasitic resistance is becoming a major challenge for animal health systems worldwide, and international organizations such as the World Health Organization (WHO) and the World Organization for Animal Health (WOAH) are actively monitoring the problem. Evidence of reduced sensitivity to macrocyclic lactones in gastrointestinal nematodes of sheep and cattle is now appearing in major livestock-producing regions, including parts of Australia, South America, and Europe. When resistance spreads, standard treatments lose effectiveness, which forces farmers to repeat doses, switch products, or combine different actives. This pattern not only reduces the practical lifespan of existing parasiticides but also increases the risk of long-term control failures and economic losses across entire production systems.

Are regulatory authorities tightening approval and post-market requirements for veterinary medicines, which is intensifying pressure on manufacturers. Under frameworks such as the EU VMPR, companies must now submit more detailed data on safety, resistance risk, and environmental impact, and they often face longer review timelines before a product can enter the market. These higher standards raise the cost of research and development and make it harder for smaller and mid-tier players to bring new antiparasitic solutions to scale. The global veterinary parasiticides industry is moving toward a more consolidated, innovation-driven structure, where investment in novel modes of action, resistance-monitoring tools, and integrated parasite-management strategies becomes essential for long-term competitiveness.

High Product Development Costs and Pricing Pressures

Bringing a new veterinary parasiticide to market is a long and capital-intensive process that spans many stages, from early discovery through extensive safety and efficacy testing to final regulatory approval. This prolonged timeline and high cost structure mean that only firms with strong financial backing and established research infrastructure can regularly launch innovative antiparasitic products. The pipeline of genuinely new actives remains limited, and manufacturers often focus on reformulating or reforming existing chemistries to extend product life cycles and maintain competitive positioning. In many emerging-market regions such as parts of Asia Pacific and Latin America, economic conditions and purchasing power place strong downward pressure on prices.

Generic competition and parallel imports of lower-cost alternatives are expanding rapidly, which limits the ability of branded manufacturers to sustain premium pricing for advanced formulations. Retail consolidation in key markets and the growing role of e-commerce platforms are intensifying price competition, as online channels and large distributors push for volume-based deals and lower margins. This dynamic squeezes profitability for full-portfolio players and can slow the introduction of cutting-edge parasiticides into lower-income markets, where affordable, basic products still dominate. Is the sector likely to differentiate more sharply between high-value, innovation-driven brands and low-cost, generic-style offerings, with access to advanced formulations varying significantly by region and income level.

Biologics and Vaccine-Based Parasite Prevention

The development of anti-parasite vaccines and veterinary biologics is opening a new frontier in the animal health sector, one that complements traditional chemical parasiticides. Scientists are advancing research on vaccines against key parasitic threats such as Leishmania, heartworm, and a range of tick-borne pathogens, often supported by public-funded research programs and academic-industry partnerships. These emerging biologics aim to provide animals with longer-lasting, immune-based protection, reducing the need for repeated chemical treatments and offering a more sustainable approach to parasite control. Although the number of commercially available products in this space is still limited, several candidates are progressing through clinical development and regulatory review, signaling that the segment is moving from proof of concept toward real-world application.

Regulatory frameworks such as those of the United States Department of Agriculture Animal and Plant Health Inspection Service (USDA APHIS) and the European Medicines Agency (EMA) are increasingly supportive of veterinary biologics, offering specialized pathways and incentives that help de-risk innovation. These mechanisms encourage companies to invest in complex vaccine platforms, recombinant technologies, and antigen-discovery programs that could yield new classes of anti-parasite interventions. First-mover organizations that successfully bring an effective anti-tick or anti-helminth biologic to market are likely to gain significant competitive differentiation, as they can position their products as premium, long-term solutions in high-value livestock and companion-animal segments.

Increasing Adoption of Companion Animals

The growing emotional bond between pet owners and their animals is transforming how households approach veterinary care. In many developed regions such as North America and Europe, pets are increasingly viewed as family members rather than simply household animals. This shift is leading owners to spend more on regular checkups, diagnostic tests, and preventive treatments, including products that protect against fleas, ticks, and internal parasites. As pet-centric lifestyles become more common, demand is rising for safer, easier-to-use, and more reliable parasiticides that fit into daily routines and reduce stress for both pets and owners. This change in mindset is turning parasite control into a core part of pet-care spending, rather than an occasional or reactive expense.

Awareness about the health risks linked to untreated parasite infestations is spreading quickly among pet owners, veterinarians, and online communities. Veterinarians are emphasizing the importance of year-round preventive programs, and digital platforms are making it easier for owners to access information and reorder treatments on a schedule. The market is also seeing a steady flow of advanced parasiticide formats, such as flavored chewables, long-acting spot-ons, and combination products that protect against multiple parasites in one dose. These innovations improve compliance and support higher price points, creating attractive growth opportunities for manufacturers that focus on quality, convenience, and trusted clinical evidence.

Category-wise Analysis

Product Type Insights

Ectoparasiticides are anticipated to dominate by holding roughly 48% of the veterinary parasiticides market revenue share in 2026. Ectoparasiticides are used to control infections caused by external parasites such as fleas, ticks, and mites in both companion and livestock animals. This segment is expected to grow strongly as ectoparasitic infestations become more common and as owners and veterinarians place greater emphasis on preventive care. Newer formulations such as spot-on treatments and oral chewables are helping to drive demand because they are easy to use and reduce stress for animals. These convenient delivery methods improve compliance among pet owners and farmers, leading to more consistent treatment schedules and better overall parasite control.

Endectocides likely to be the fastest-growing segment during the 2026-2033 forecast period. Endectocides are a distinct class of parasiticides that protect animals against both internal and external parasites. This segment is gaining popularity because it offers a comprehensive approach to parasite control within a single treatment, which simplifies management and improves compliance. Endectocides are especially useful in large livestock herds, where efficient dosing is critical. The introduction of long-acting formulations that provide extended protection is further accelerating demand. Growing interest in integrated parasite-management strategies is encouraging veterinarians and farmers to adopt endectocides as a core component of routine herd-health programs.

Route of Administration Insights

Oral administration is set to capture nearly 42% of the veterinary parasiticides market share in 2026, since it is widely applied across livestock sectors through drenches, boluses, and feed-based additives. In large-herd management, oral products are deeply embedded in routine protocols for cattle, swine, and poultry, where operators can treat many animals quickly and efficiently. These formulations are cost-effective, easy to integrate into feeding systems, and scalable for use on commercial farms. Their compatibility with mass-treatment programs, combined with relatively simple logistics and training requirements, makes them the preferred route for many herd-health and parasite-control strategies in food-producing animals.

Topical formulations are expected to be the fastest-growing segment over the 2026-2033 forecast period, driven by rising demand in companion-animal markets for easy-to-use spot-ons, sprays, and collars that control fleas, ticks, and mites. These products appeal strongly to pet owners because they are convenient, non-invasive, and can be applied at home without the need for injections or complex handling. Many veterinarians also recommend topical treatments as part of routine preventive care, which further accelerates their adoption. Injectable formulations remain important, especially for large-animal and production-animal use, but they are growing at a slower pace than topical products because they are typically reserved for more specialized or clinical settings where trained professionals administer the doses.

Regional Insights

North America Veterinary Parasiticides Market Trends

North America is set to command a significant portion of the veterinary parasiticides market value at approximately 38% in 2026, supported by strong awareness of animal health and a well-developed veterinary care system. In this region, pet owners and livestock producers are highly responsive to preventive care, and many routine veterinary visits now include parasite screening and treatment recommendations. The United States and Canada host a large base of companion-animal households as well as a highly organized livestock sector, which together create consistent demand for effective parasiticides. Regulatory bodies such as the U.S. FDA CVM and national veterinary agencies are also reinforcing standards for product safety and residue control, which pushes the market toward approved, high-quality treatments rather than informal or low-evidence options.

Major Animal-health companies are headquartered or have significant operations in North America, giving them direct access to veterinarians, distributors, and end users. These firms are actively investing in new formulations, combination products, and digital tools that support parasite-management protocols, which strengthens their position in the region. The growing trend of pet ownership, combined with rising awareness of zoonotic and environmentally transmitted parasites, is encouraging more frequent and higher-value purchases of parasiticides. In parallel, the livestock industry is under pressure to maintain high productivity and food-safety standards, which is increasing the use of prophylactic and targeted antiparasitic treatments.

Europe Veterinary Parasiticides Market Trends

Europe is a major and mature market for veterinary parasiticides, anchored by strong awareness of animal health and a dense network of veterinary professionals. Countries such as Germany, France, and the United Kingdom play a central role because they combine high pet-ownership rates with large, technologically advanced livestock sectors. In companion-animal care, veterinarians are increasingly integrating regular parasite screening and preventive treatment into standard checkups, which drives steady demand for flea, tick, and worm control products. Dairy, beef, and poultry producers across the region are under pressure to maintain high productivity and meet strict food-safety requirements, which encourages the routine use of approved parasiticides as part of herd-health programs.

Supporting this demand is a robust regulatory and policy environment that emphasizes animal welfare, product safety, and environmental protection. The European Union veterinary medicines framework, administered in part through the European Medicines Agency (EMA), sets clear standards for the approval and use of veterinary parasiticides, including data requirements for efficacy, resistance risk, and environmental impact. These rules encourage manufacturers to invest in higher-quality, evidence-based products rather than low-evidence or off-label options. Major Animal-health companies also maintain significant research, registration, and commercial operations in Europe, which helps them tailor parasite-control solutions to regional disease patterns and regulatory expectations.

Asia Pacific Veterinary Parasiticides Market Trends

Asia Pacific is anticipated to emerge as the fastest-growing market for veterinary parasiticides between 2026 and 2033. Rising pet adoption is particularly visible in urban centers across countries such as China, India, and Japan, where young professionals and middle-income households are increasingly choosing dogs and cats as part of their lifestyle. As disposable income grows, pet owners are more willing to spend on preventive care, including year-round flea, tick, and worm control products that offer convenience and perceived safety. Veterinarians and pet-care clinics in major cities are promoting standardized parasite-management protocols, which further strengthens demand for branded and higher-quality parasiticides.

The livestock industry across Asia Pacific is undergoing significant modernization, with governments and private investors pushing for more efficient and integrated farming systems. Dairy, poultry, and swine producers are expanding herd sizes and adopting more professional herd-health practices, including routine parasite control to protect productivity and meet evolving food-safety expectations. Regulatory bodies in several countries are also tightening standards for veterinary medicines, which is encouraging the use of approved, registered parasiticides rather than informal or low-evidence treatments. As animal-health awareness spreads and consumers increasingly demand high-quality meat, milk, and eggs, the Asia Pacific region is becoming a strategic growth hub for both local and global veterinary parasiticides manufacturers.

Competitive Landscape

The global veterinary parasiticides market structure is moderately consolidated, dominated by leading players such as Zoetis Inc., Boehringer Ingelheim Animal Health, Virbac S.A., Vetoquinol S.A., and Dechra Pharmaceuticals. These players collectively capture 60-65% of the market share. The market features a dynamic competitive landscape with several major multinational companies alongside smaller regional players. Large firms lead through extensive research and development efforts that yield innovative products with enhanced efficacy and safety.

Companies are also channeling significant resources into advancing pharmaceutical formulations to meet rising demand for reliable parasite control across livestock and companion animals. Strategic moves such as collaborations, mergers, and acquisitions are common as players seek to broaden their product offerings and enter new geographic areas. These initiatives help firms strengthen market positions and respond to evolving customer needs in a highly competitive environment.

Key Industry Developments

- In October 2025, Health Canada approved BRAVECTO® QUANTUM (fluralaner extended-release injectable suspension) from Merck Animal Health, offering dogs and puppies aged 6 months and older up to 12 months of protection against fleas and key ticks like black-legged, American dog, and brown dog ticks, or 8 months against lone star ticks.

Companies Covered in Veterinary Parasiticides Market

- Zoetis Inc.

- Boehringer Ingelheim Animal Health

- Merck Animal Health (MSD)

- Elanco Animal Health

- Virbac S.A.

- Vetoquinol S.A.

- Ceva Santé Animale

- Dechra Pharmaceuticals

- Chanelle Pharma Group

- Phibro Animal Health Corp.

- Norbrook Laboratories

- Huvepharma

- Indian Immunologicals Ltd.

- Bimeda Inc.

Frequently Asked Questions

The global veterinary parasiticides market is projected to reach US$ 11.5 billion in 2026.

Market growth is being driven by rising companion animal ownership and livestock intensification, which are increasing the demand for preventive parasite control.

The market is poised to witness a CAGR of 7.7% from 2026 to 2033.

Major opportunities lie in Innovation in biologics, vaccines, and integrated management tools will create new high-value segments beyond traditional chemical parasiticides.

Zoetis Inc., Boehringer Ingelheim Animal Health, Virbac S.A., Vetoquinol S.A., and Dechra Pharmaceuticals are some of the key players in the market.