- Animal Health

- Veterinary Arthroscopy Devices Market

Veterinary Arthroscopy Devices Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Veterinary Arthroscopy Devices Market by Product (Arthroscope and Arthroscopic Systems, Arthroscopy Starter Kits, Arthroscopic Handheld Instruments, Consumables, Arthroscopy Cleaning & Sterilization Trays), by Animal (Small Animals, and Large Animals), Procedure, End-user, Regional Analysis, 2025 - 2032

Veterinary Arthroscopy Devices Market Share and Trends Analysis

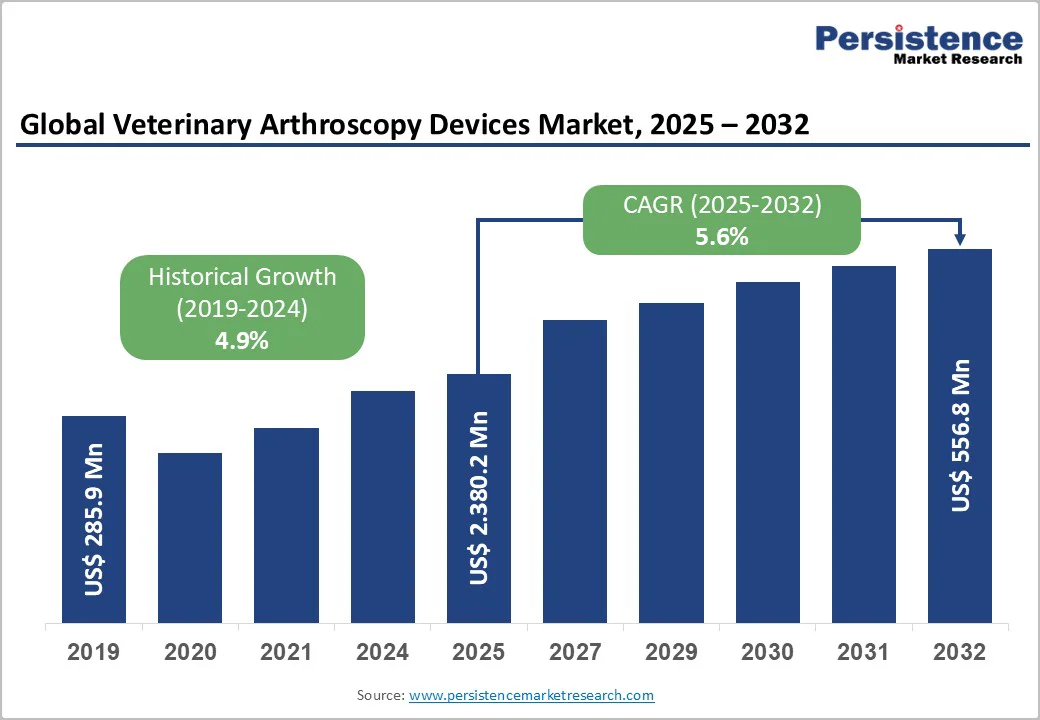

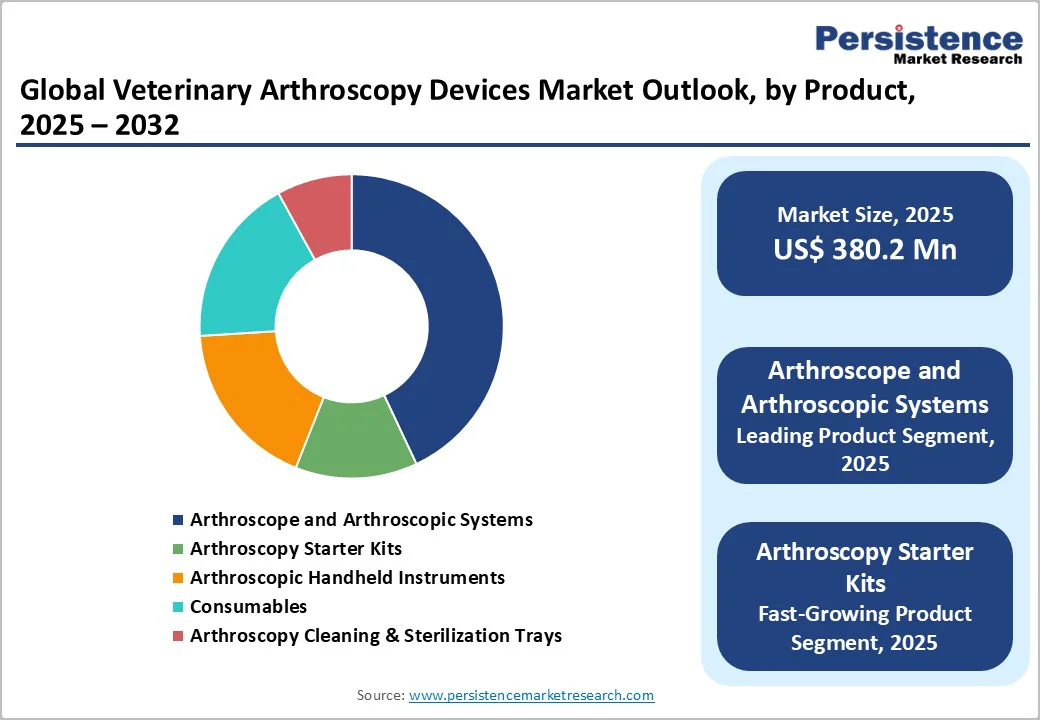

The global veterinary arthroscopy devices market is valued at US$380.2 million in 2025 and is expected to grow to US$556.8 million, representing a CAGR of 5.6% from 2025 to 2032.

The rising prevalence of degenerative joint diseases in companion animals. Conditions such as lameness, joint swelling, muscle atrophy, pericapsular fibrosis, and crepitus in dogs and cats are driving the demand for minimally invasive diagnostic and therapeutic procedures. Veterinary arthroscopy is increasingly preferred over traditional arthrotomy because it provides precise visualization and treatment of joint issues, particularly in animals with smaller joints, resulting in faster recovery and reduced surgical trauma.

Key Industry Highlights

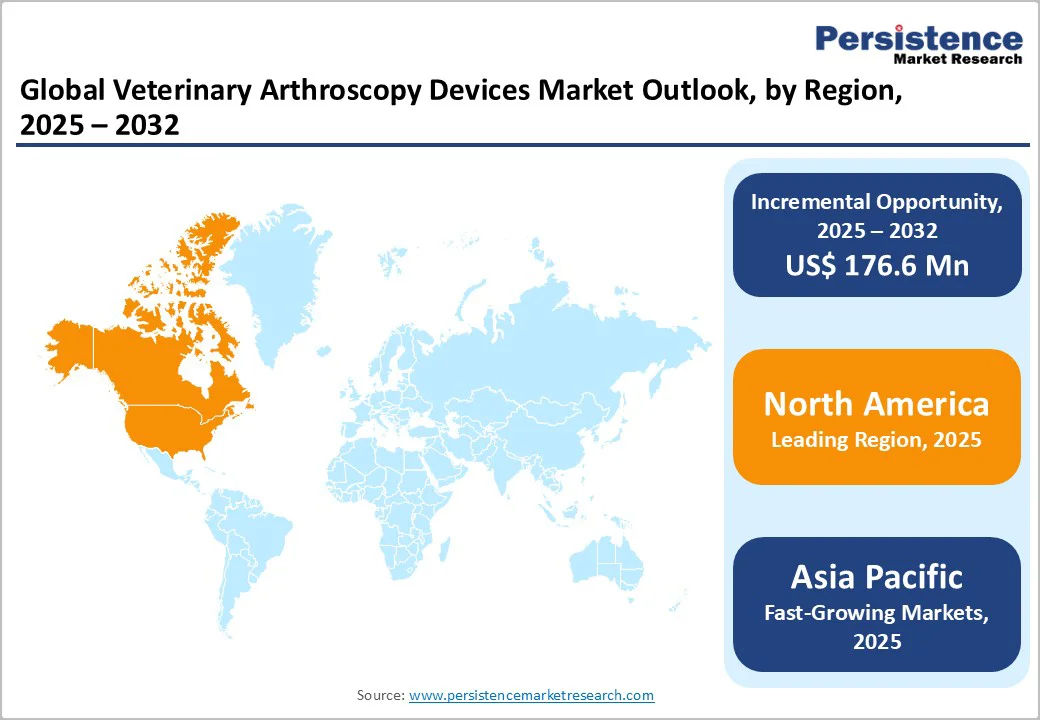

- Leading Region: North America remains the leading region due to advanced healthcare infrastructure and high pet insurance penetration.

- Fastest Growing Region: Asia Pacific is the fastest-growing region, driven by expanding veterinary healthcare and pet ownership.

- Dominant Segment: Arthroscopes and arthroscopic systems dominate the product category with robust adoption across veterinary settings.

- Market Opportunity: Increasing demand for minimally invasive diagnostic procedures offers substantial market growth opportunities.

| Key Insights | Details |

|---|---|

|

Veterinary Arthroscopy Devices Market Size (2025E) |

US$ 380.2 Mn |

|

Market Value Forecast (2032F) |

US$ 556.8 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

5.6% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.9% |

Market Dynamics

Driver - Increasing Pet Ownership and Enhanced Veterinary Care

The global veterinary arthroscopy devices market is driven by rising pet ownership and growing emphasis on enhanced veterinary care. Over recent years, pet adoption has surged across both developed and emerging regions, resulting in a substantial increase in the number of companion animals health requiring medical attention. In the United States alone, data from the American Pet Products Association (APPA) indicates that nearly 70% of households owned a pet in 2023. This trend reflects a broader cultural shift, with pet owners increasingly considering their animals as integral family members. As a result, there is a growing willingness among owners to invest in advanced medical procedures, including minimally invasive surgeries such as arthroscopy, which offer faster recovery times, reduced postoperative pain, and a lower risk of complications.

Simultaneously, the veterinary sector has witnessed an expansion in the number of hospitals, specialty clinics, and diagnostic centers that are incorporating arthroscopy equipment into their practice. This adoption is motivated by the need to provide precise diagnostic capabilities and effective treatment options for musculoskeletal and joint-related conditions in animals. The combined effect of rising pet ownership, increased spending on animal healthcare, and improved veterinary infrastructure continues to propel demand for veterinary arthroscopy devices globally.

Restraints - Strong Pricing Pressure & Product Recalls Can Limit Market Progress

The pet population in the U.S. is rising; however, access to veterinary care remains a cause for concern. The factor of affordability of veterinary health and safety has been a key challenge for both, owners and veterinary professionals. Due to opposition from several key players over inadequate economic and other public means, there is strong pressure to validate, transfer, decentralize, and privatize animal health services in many countries.

Furthermore, manufacturers are aiming to develop innovative designs to set apart their implants, leading them to capitalize on the scanning abilities and developments in the production of orthopaedic devices, which raises their operating costs. Conversely, there is strong pricing pressure in the market. This considerably contracts their profit margins. Rise in arthroscopic device product recalls or retrieving of all defective arthroscopic products from the market is one of the major restraints for market expansion.

There has also been a dearth of resources in the veterinary practice as well as considerable upsurge in demand for veterinary services, evidently since the advocated adoption boom of pandemic pets across the globe. Currently, the shortage of trained veterinary professionals and diagnostic equipment, particularly in emerging countries, is a key factor restraining the use of veterinary arthroscopy devices.

Opportunity - Market Players Focusing on Launching Technologically-advanced Veterinary Arthroscopy Products

At present, minimally invasive techniques are attaining widespread acceptance among specialists owing to several advantages of such procedures in comparison to open surgeries. Minimally invasive arthroscopic techniques reduce hospitalization costs and lessen complications related to open repair. In veterinary science, arthroscopy has gained traction over the last few decades and can be understood as the 'gold standard' when it comes to joint evaluation and treatment.

Growing inclination and recognition for minimally invasive and cost-effective surgeries using arthroscopic devices is expected to generate vast opportunities for veterinary arthroscopic device producers. Arthroscopic techniques have become a typical diagnostic and therapeutic preference for canine joint disorders in recent years, which constructs vast opportunities for key players in the veterinary arthroscopy devices landscape.

Arthroscopic surgery in companion animals is the most prominent development in veterinary orthopaedics ever since the institution of diagnostic needle arthroscopy. This is a novel and forthcoming tool in veterinary science. It compromises a minimally invasive tool that can deliver the capacity for present dynamic conception of the animal’s structure, permitting a different tool for diagnosis and procedure of veterinary professional decision-making, and can possibly lessen the time from wound to analysis, surgical or nonsurgical cure, and recovery.

In the same way, improvements in arthroscope technology with micro-electronics have given rise to the advancements in needle arthroscopes for arthroscopy procedures in small animals. Though treatment preferences are growing, conclusive diagnosis of minor to moderate stifle pathology has been limited for a long time, owing to factors such as inadequacy of conventional diagnostic arthroscopy, even though it permits for both, diagnosis and therapy, but calls for general anaesthesia, longer recovery time, and substantial cost.

Like conventional arthroscopy, standing needle arthroscopy has established itself as a safe and dependable process devoid of the risks and costs related to general anaesthesia. This method is a supplementary diagnostic procedure that can be adopted when conventional diagnostic procedures such as radiology and ultrasound have not grasped conclusive diagnosis.

Thus, growing need for more efficient and cost-effective diagnostic arthroscopy is creating opportunities for key players to develop new technologically advanced veterinary arthroscopy products.

Category-wise Analysis

By Product, Arthroscope and Arthroscopic Systems Dominate the Market

The Arthroscope and Arthroscopic Systems segment is the leading product category in the veterinary arthroscopy devices market, capturing around 43% share in 2024. Their prominence is attributed to their essential role in both diagnostic and therapeutic applications, offering veterinarians precise visualization of joints, which is critical for accurate treatment planning and effective surgical intervention. These systems enable minimally invasive procedures, reducing trauma, post-operative pain, and recovery time for animals, making them highly preferred in clinical practice.

Technological advancements have further strengthened the adoption of arthroscopes and arthroscopic systems. Features such as high-resolution imaging, enhanced lighting, and compact, ergonomic designs make the devices more user-friendly and efficient, supporting their widespread use in veterinary hospitals and specialty clinics. Additionally, the increasing trend toward minimally invasive surgeries in companion animal healthcare has accelerated the preference for these systems over conventional surgical methods. Continuous innovation, integration with digital platforms, and improvements in surgical precision ensure that arthroscopes remain central to veterinary orthopedic and soft tissue interventions globally.

By Animal, Small Animals Leads the Market

The Small Animals segment holds a dominant position in the veterinary arthroscopy devices market, accounting for approximately 68% share in 2024. This leadership is largely driven by the increasing population of companion animals, particularly dogs and cats, which constitute the largest patient group in veterinary care worldwide. Rising pet ownership, coupled with pet owners’ willingness to invest in advanced medical procedures, has significantly boosted the demand for minimally invasive surgeries such as arthroscopy. These procedures are preferred for their ability to ensure faster recovery, reduced surgical trauma, and improved clinical outcomes in small animals.

In contrast, the adoption of arthroscopy in large animals, including equines and livestock, remains relatively limited. Factors such as higher procedural costs, the complexity of surgical interventions, and variations in clinical practices contribute to slower uptake in this segment. Nevertheless, as awareness of joint and musculoskeletal disorders in large animals grows, adoption is gradually increasing, though small animals continue to drive the majority of market demand and revenue.

Region-wise Insights

North America Veterinary Arthroscopy Devices Market Trends

North America leads the global veterinary arthroscopy devices market, accounting for approximately 38.3% share in 2025, with the U.S. as the dominant contributor. The strong presence of a large pet population, rising adoption rates, and growing awareness among pet owners regarding advanced healthcare interventions are key factors driving market expansion. Pet owners are increasingly willing to invest in minimally invasive procedures that enable faster recovery and reduce postoperative complications.

The region benefits from a well-established veterinary healthcare infrastructure, high pet insurance penetration, and widespread acceptance of arthroscopic procedures over traditional surgical methods. Increasing cases of trauma surgeries, soft tissue injuries, and degenerative joint conditions in companion animals further fuel demand for arthroscopy devices. Regulatory frameworks, particularly by the FDA, ensure device safety while supporting innovation through efficient approval pathways for new and improved technologies.

In addition, North America’s market growth is supported by the presence of key device manufacturers investing heavily in research and development. Companies focus on product enhancements, digital integration, and high-definition imaging systems to improve surgical precision, outcomes, and clinician adoption across veterinary hospitals and specialty clinics.

Asia and Pacific Veterinary Arthroscopy Devices Market Trends

Asia Pacific veterinary arthroscopy devices market is the fastest growing globally, driven by increasing pet ownership in countries such as China, Japan, India, and ASEAN nations. Rising disposable incomes and changing lifestyles have encouraged more households to adopt companion animals, creating demand for advanced veterinary care. Government initiatives to improve animal healthcare, coupled with the expansion of veterinary hospitals and specialty clinics equipped with arthroscopy systems, are supporting market growth.

The region benefits from major production hubs that offer cost advantages for manufacturers, enabling scalable device deployment at competitive prices. Awareness about minimally invasive procedures among pet owners is steadily increasing, while adoption of pet insurance in urban centers further supports the market. Additionally, veterinarians in emerging economies are increasingly integrating advanced diagnostic and surgical procedures to improve treatment outcomes for musculoskeletal and joint-related disorders in animals. These factors make the Asia-Pacific a high-potential market for veterinary arthroscopy devices.

Competitive Landscape

Introduction of new technologies, upgrading existing products, and strategic alliances for the sale and promotion of products are key differential strategies followed by manufacturers of veterinary arthroscopy devices. Companies are also entering into mergers and acquisitions with other medical device manufacturers to expand their product portfolio and market presence across the globe.

Key Industry Developments:

- In December 2021, American medical device company DePuy Synthes (a subsidiary of Johnson & Johnson Services, Inc.) acquired OrthoSpin, an Israeli startup specializing in automated strut systems.

- In April 2021, Trice Medical acquired Tenex Health, enabling portable, cost-efficient diagnostic.

Companies Covered in Veterinary Arthroscopy Devices Market

- Arthrex, Inc.

- Karl Storz SE & Co. KG

- Biovision Veterinary Endoscopy, LLC.

- Eickemeyer

- vetOvation

- KYON Veterinary Surgical Products

- Trice Medical

- GerVetUSA

- Dr. Fritz Endoscopes

- Depuy Synthes

- Integra LifeSciences Corporation

- IMEX Veterinary, Inc.

- ConMed Linvatec

- Novetech Surgery

- Others

Frequently Asked Questions

The global veterinary arthroscopy devices market is projected to be valued at US$ 380.2 Mn in 2025.

Increasing prevalence of animal musculoskeletal disorders and rising demand for minimally invasive veterinary surgeries drive the market.

The global market is poised to witness a CAGR of 5.6% between 2025 and 2032.

Growing pet adoption, technological advancements, and expanding veterinary clinics present significant market growth opportunities.

Leading companies include Arthrex, Inc., Karl Storz SE & Co. KG, Biovision Veterinary Endoscopy, LLC., Eickemeyer, vetOvation, and Others.