- Semiconductor Materials & Components

- Tantalum Capacitors Market

Tantalum Capacitors Market Size, Share, and Growth Forecast, 2025 - 2032

Tantalum Capacitors Market by Product (Solid Tantalum Capacitors, Wet Tantalum Capacitors, Polymer Tantalum Capacitors), Mounting Type (Surface-Mount, Axial, Radial), Application (IT & Telecommunications, Consumer Electronics, Military and Aerospace, Automotive, Industrial, Medical Devices, Others), and Regional Analysis for 2025 - 2032

Tantalum Capacitors Market Share and Trends Analysis

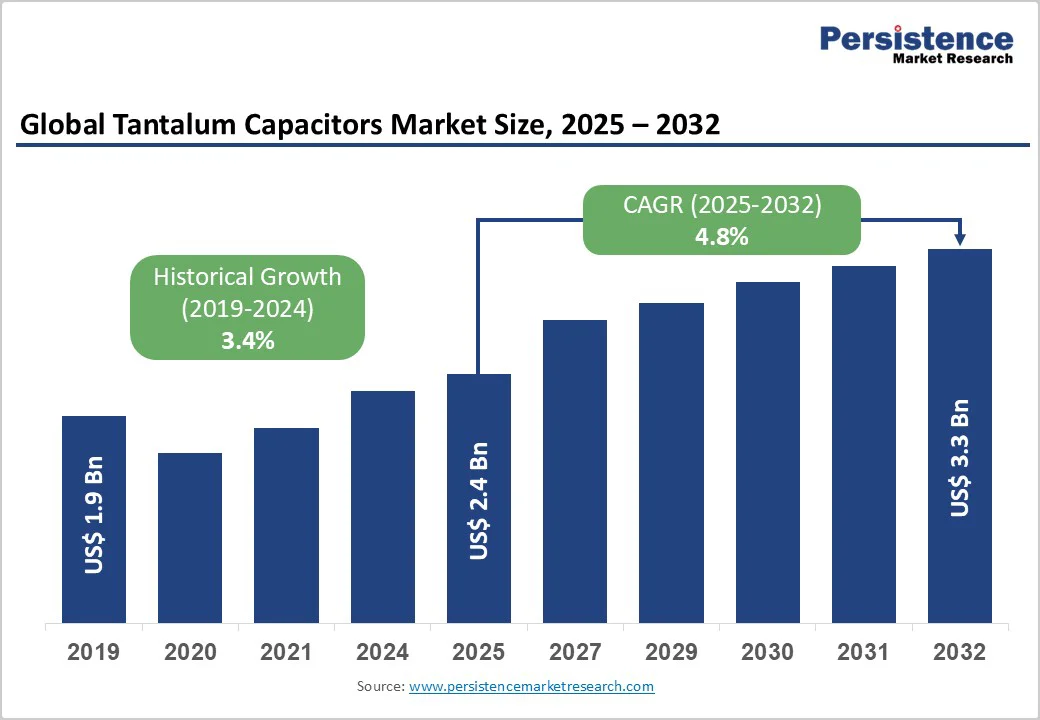

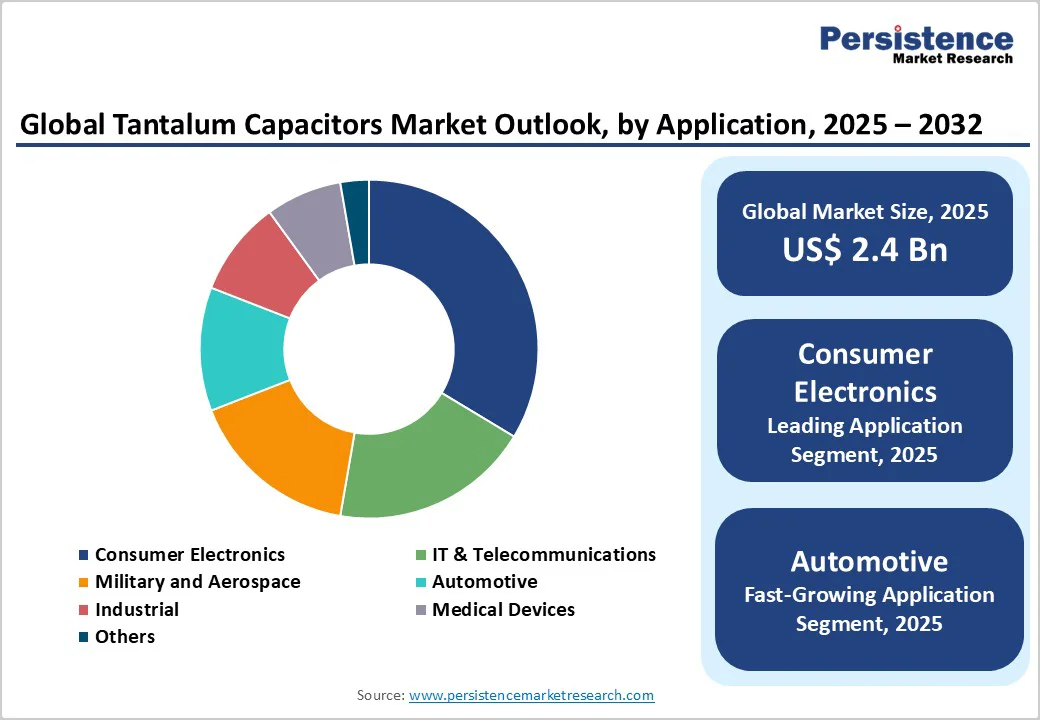

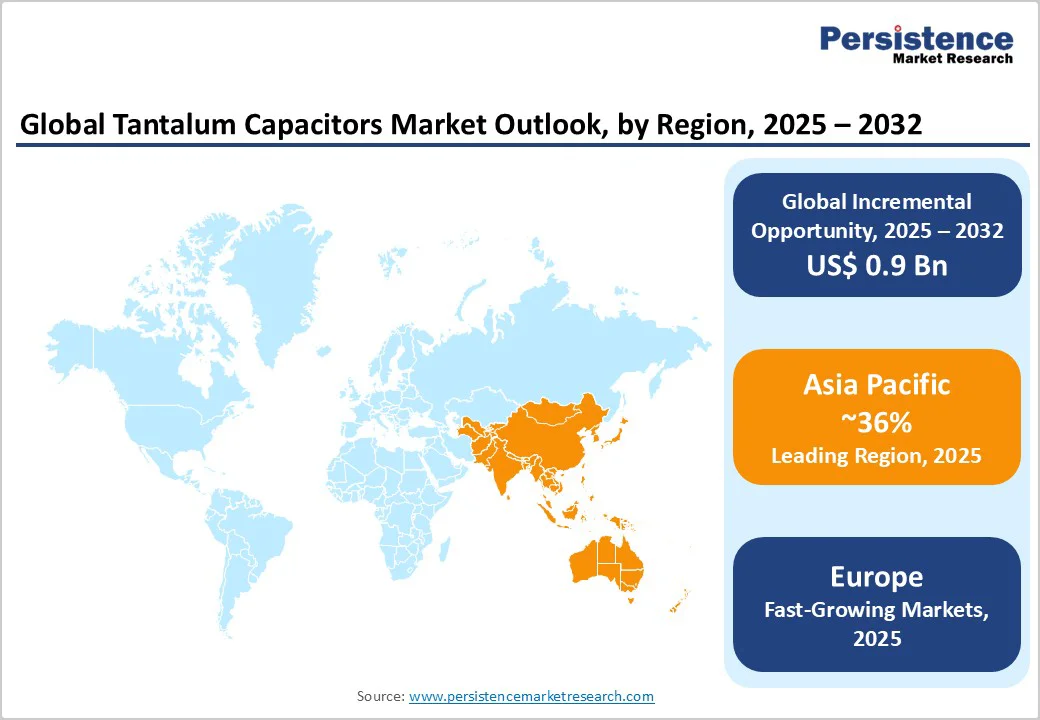

The global tantalum capacitors market size is likely to be valued at US$ 2.4 billion in 2025, and is projected to reach US$ 3.3 billion by 2032, growing at a CAGR of 4.8% during the forecast period 2025-2032. Tantalum capacitors are vital components in modern electronics, offering high volumetric efficiency, superior reliability, and stable performance under extreme conditions. Their demand is rising with technological advancement, device miniaturization, and the need for high-reliability components in sectors such as medical implants, electric vehicles (EVs), 5G infrastructure, and consumer electronics. As industries push for compact, durable, and efficient designs, tantalum capacitors are set to remain critical enablers.

Key Industry Highlights

- Leading Product: Solid tantalum capacitors are poised to dominate with over 40% share in 2025, offering compact design, reliability, and temperature stability essential for mission-critical electronics.

- Leading Mounting Type: Surface-mount is expected to hold more than 58% of the tantalum capacitors market revenue share in 2025 due to high-density circuit design advantages and compatibility with automated assembly lines.

- Leading Application: Consumer electronics is set to lead with over 26% share in 2025, driven by miniaturized power-efficient devices and 5G-enabled products.

- Dominant Region: Asia Pacific is predicted to dominate with over 36% share by 2025, led by China’s 3.8 million 5G base stations and robust electronics production.

- Regional Dynamics: North America demonstrates strong growth driven by rising semiconductor investments under the CHIPS Act, expanding data center capacity to support AI workloads.

- Key Market Driver: Expanding 5G infrastructure and IoT ecosystem is projected to drive the demand for high-capacitance, stable tantalum capacitors in communication and edge computing systems.

| Key Insights | Details |

|---|---|

|

Tantalum Capacitors Market Size (2025E) |

US$ 2.4 Bn |

|

Market Value Forecast (2032F) |

US$ 3.3 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.8% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Electronics Miniaturization and High-Reliability Needs to Boost Adoption

Tantalum capacitors are increasingly adopted in modern compact electronics such as smartphones, wearables, medical implants, and automotive systems due to their superior volumetric efficiency, thermal resilience, and long operational lifespan compared to aluminum or ceramic types. The miniaturization trend and growing demand for reliable, biocompatible components in wearable health and implantable devices further accelerate adoption, especially amid aging populations in advanced economies. With the global smartphone market undergoing exponential expansion, the demand for high-performance tantalum capacitors is expected to accelerate globally.

Simultaneously, the global deployment of 5G networks, reaching 2.25 billion connections in 2024 and expected to rise to 8.3 billion by 2029, is fueling the need for high-frequency, stable capacitors vital to next-generation communication systems. For example, the U.S. Federal Communications Commission (FCC)’s 5G FAST Plan aims for nationwide deployment by 2025. Tantalum capacitors, known for their high capacitance, reliability, and stability, are increasingly used in 5G base stations and edge computing. The surge in IoT devices is further reinforcing the demand for these components.

Supply Chain Vulnerabilities and Conflict Minerals Compliance Challenges

The tantalum capacitors market growth faces major supply chain risks due to the metal’s limited availability and concentration in politically unstable African regions. Over 50% of global tantalum originates from the Democratic Republic of the Congo (DRC) and nearby nations, where artisanal mining often involves conflict-related human rights abuses. Under Section 1502 of the 2010 Dodd-Frank Act, manufacturers must audit and report conflict-mineral use. The resurgence of M23 militants in eastern DRC in early 2025 drove tantalite prices up ~8% to US$ 80–88/lb, intensifying raw-material scarcity and production instability for aerospace, medical, and consumer electronics capacitors.

Fluctuating tantalum prices and limited availability continue to disrupt the stable supply of tantalum capacitors, with Western smelters paying 10–20% premiums for conflict-free material from Burundi, Mozambique, and Ethiopia to meet environment, social, & governance (ESG) norms. The heavy regional concentration of tantalum mining exposes supply chains to geopolitical risks, as rebel activity often halts recently signed supply agreements. Component manufacturers face raw material shortages and stringent mining regulations, leading to a shift toward ceramic and aluminum electrolytic alternatives.

Expansion in Renewable Energy Storage Systems and Smart Grid Applications

The global transition toward renewable energy and smart grid systems is creating strong growth prospects for the tantalum capacitors market. Supported by federal subsidies and electric mobility programs, demand is rising for high-reliability capacitors in advanced energy storage systems across residential, public, and industrial sectors. The stability offered by tantalum capacitors across temperature ranges and long lifecycles make them ideal for power management in renewable and grid-stabilizing applications. According to the International Energy Agency (IEA)’s World Energy Investment 2025, global energy investment is expected to rise by 2% in real terms to US$ 3.3 trillion, with US$ 2.2 trillion flowing into renewables, grids, storage, and electrification.

The growing adoption of advanced recycling technologies, such as microwave-assisted selective carbothermal reduction, which achieves 97% purity in tantalum carbide recovery from end-of-life capacitors, presents a major sustainability and supply resilience opportunity in the tantalum capacitor market. With 20–30% of global tantalum consumption already met through recycling, manufacturers are expanding closed-loop systems to minimize dependency on conflict-region mining. Supported by governmental e-waste regulations and ESG-driven investments, companies adopting circular economy models lower raw material costs and enhance supply chain security, a critical advantage amid rising demand from high-tech sectors such as electronics, defense, and telecommunications.

Category-wise Analysis

Product Insights

Solid tantalum capacitors are expected to account for more than 40% share in 2025 on account of their superior volumetric efficiency, long-term reliability, and stable capacitance across temperature ranges. The growing need for compact, high-performance electronic components in smartphones, automotive electronics, medical devices, and defense systems drives their dominance. Their ability to deliver high capacitance in small packages and withstand harsh operating conditions makes them essential for miniaturized and mission-critical applications.

Polymer tantalum capacitors are projected to witness the fastest growth, driven by a soaring demand for compact, high-performance components in smartphones, EVs, data centers, and 5G infrastructure. Their low equivalent series resistance (ESR) and high root mean square (RMS) ensure superior power efficiency and thermal stability for high-frequency, high-current applications. The introduction of MIL-PRF-32700 qualified variants further underscores their adoption in military and aerospace systems, reflecting strong market momentum across advanced electronics and automation sectors.

Mounting Type Insights

Surface-mount is anticipated to account for over 58% of the tantalum capacitors market revenue share in 2025, attributable to the rising need for compact, high-capacitance components that enable space-efficient circuit designs. Their superior volumetric efficiency, ease of automated assembly, and stable performance under temperature and voltage variations make them ideal for modern miniaturized electronics. The demand for high-density, reliable, and long-lasting solutions further strengthens their market leadership. Recent product launches, including Panasonic's commercialization of 50TQT33M and 63TQT22M models with ultrahigh withstand voltage and high capacitance in the industry's lowest profile of 3mm, demonstrate ongoing innovation supporting USB Power Delivery 3.1 applications up to 240W.

Radial tantalum capacitors are projected to grow at the highest rate through 20232 because of their superior mechanical reliability, through-hole mounting suitability, and stable performance in harsh environments. Advancements in polymer technology have improved their low ESR and power efficiency, aligning with next-generation electronic needs. Enhanced lead frame designs and materials further strengthen thermal management and reliability, driving renewed adoption in aerospace, defense, and industrial applications.

Application Insights

Consumer electronics are set to command more than 26% revenue share in 2025 due to a strong demand for compact, high-performance components in smartphones, tablets, laptops, and wearable devices. These products require capacitors offering high capacitance density and reliability to support miniaturized, power-efficient designs. The growing adoption of 5G-enabled devices, advanced processors, and high-speed power management systems further drives usage. The integration of AI capabilities, enhanced camera systems, and high-speed connectivity in modern devices continues to increase component density, sustaining demand for high-reliability tantalum capacitors.

Automotive sector will grow at a significant rate from 2025 to 2032, driven by the increasing integration of advanced driver assistance, electrified powertrains, and in-vehicle infotainment systems. Tantalum capacitors are increasingly favored in automotive electronics for their stability under extreme conditions, compact size, and high reliability, making them ideal for mission-critical applications in safety, powertrain, and communication modules. Global automotive sales are projected to reach over 86 million units in 2025, creating substantial volume opportunities as the shift toward electric and hybrid vehicles amplifies electronic content per vehicle.

Regional Insights

North America Tantalum Capacitors Market Trends

The North America tantalum capacitors market is driven by strong demand from aerospace, defense, and medical electronics requiring high-reliability components, along with the rapid expansion of AI workloads and data centers. The U.S. Department of Energy’s 2024 review highlights data-center loads tripling over the past decade and expected to double–triple again by 2028, boosting power-system component demand. Semiconductor investments under CHIPS-era incentives and new fabs announced by the U.S. Department of Commerce and Intel in 2024–2025 further stimulate local use of these capacitors in power management. In Canada, federal Zero-Emission Vehicle (ZEV) infrastructure programs have elevated the demand for EV power-electronic components.

Asia Pacific Tantalum Capacitors Market Trends

Asia Pacific is projected to hold over 36% of the tantalum capacitors market share in 2025, supported by strong supply chains, cost-effective production, and rapid technology adoption. China, producing roughly 1.67 billion mobile phones in 2024, including about 1.25 billion smartphones, and operating 3.8 million 5G base stations by May 2024, leads regional demand through smartphones, telecom, and server applications. Japan’s focus on high-reliability automotive and industrial electronics, South Korea’s semiconductor and electronics export cycles, and Taiwan’s record US$475 billion ICT-led exports in 2024 reinforce steady component consumption. India’s PLI and Electronics Component Manufacturing Scheme accelerate local capacitor production and stoke the demand for EV electronics.

Europe Tantalum Capacitors Market Trends

The demand for tantalum capacitors in Europe is growing on the back of rapid automotive electrification, AI-enabled industrial expansion, and widespread 5G deployment. Germany recorded a 53.5% rise in BEV registrations in April 2025 with 45,535 units and an 18.8% market share, while EU-wide BEV registrations reached 1.13 million units with a 15.8% share between January and August 2025, as reported by the European Automobile Manufacturers’ Association. The European Union (EU) 5G Observatory noted 94.3% household 5G coverage by end-2024, driving hardware upgrades across telecom and edge networks. Rising data center capacity and renewable power projects across Europe are further accelerating demand for high-reliability tantalum capacitors used in inverters, converters, and power management modules.

Competitive Landscape

The global tantalum capacitors market structure shows moderate concentration, with leading manufacturers accounting for more than half of the total market share. Manufacturers are actively focusing on product innovation, miniaturization, and reliability enhancement to meet the demanding performance requirements of modern electronics. They are also adopting vertical integration strategies to secure a stable raw material supply amid global tantalum sourcing challenges. Companies are forming strategic partnerships with original equipment manufacturers (OEMs) to strengthen their market position, enhance supply chain resilience, and ensure long-term growth.

Key Industry Developments

- In October 2025, tantalum prices surged significantly, reaching around US$ 96 per pound for tantalum pentoxide containing 25% tantalite, marking a 22% increase so far in the year and over 60% since early 2021. This price rise is bolstered by Chinese smelters increasing inventory and Australian producers redirecting shipments to markets such as the US, Japan, and Mexico. Western Australia’s lithium miners, including Pilbara Minerals, Mineral Resources, Liontown Resources, and IGO, benefit from rising tantalum as a valuable by-product amid lithium market challenges.

- In September 2025, Panasonic Industry Co., Ltd. announced the upcoming mass production (starting December 2025) of its new conductive polymer tantalum solid capacitors (POSCAP) models, 50TQT33M and 63TQT22M. Designed for laptops and tablets, these capacitors feature ultra-high voltage tolerance, high capacitance, and the industry’s lowest 3 mm profile, supporting USB Power Delivery (PD) 3.1 up to 240 W.

- In June 2025, Patriot Battery Metals began work programs to unlock tantalum as a high-value by-product opportunity at its Shaakichiuwaanaan property in Quebec, Canada, one of the top five global tantalum pegmatite resources by grade and tonnage. The project holds significant lithium, caesium, tantalum, and gallium mineralization, with preliminary test programs producing promising tantalite concentrate.

Companies Covered in Tantalum Capacitors Market

- KEMET Corporation

- AVX Corporation

- Vishay Intertechnology, Inc.

- Nichicon

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- ROHM Co., Ltd.

- Samsung Electro-Mechanics

- NIC Components Corp.

- Hitachi AIC

- Exxelia

- Panasonic

- Xiangyee

Frequently Asked Questions

The global tantalum capacitors market is projected to reach US$2.4 billion in 2025.

The growing demand for compact, high-reliability electronic components is a key driver of the market.

The market is poised to witness a CAGR of 4.8% from 2025 to 2032.

Developing high-voltage and automotive-grade tantalum capacitors, as well as expanding recycling initiatives to ensure sustainability, is creating strong growth opportunities.

KEMET Corporation, AVX Corporation, Vishay Intertechnology, Inc., and Nichicon are among the leading market players.