- Semiconductor Materials & Components

- Polymer Tantalum Capacitors Market

Polymer Tantalum Capacitors Market Size, Share, and Growth Forecast, 2025 - 2032

Polymer Tantalum Capacitors Market by Product Type (Surface-Mount, Axial, Radial), Application (Medical Devices, Consumer Electronics, Military & Aerospace, Automotive, Industrial, IT & Telecommunications, Others), and Regional Analysis for 2025 - 2032

Polymer Tantalum Capacitors Market Size and Trends Analysis

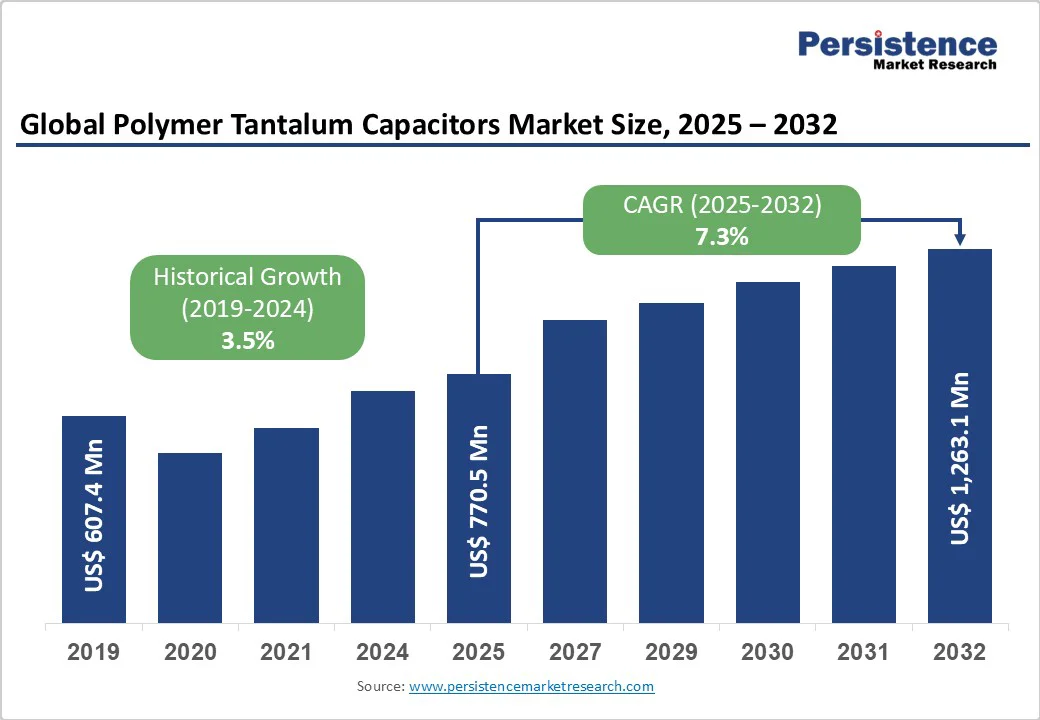

The global polymer tantalum capacitors market size is likely to value US$770.5 Mn in 2025 to US$1,263.1 Mn by 2032, growing at a CAGR of 7.3% during the forecast period from 2025 to 2032, indicating strengthened market momentum driven by expanding applications in electric vehicles, 5G infrastructure, and advanced industrial automation systems.

Key Industry Highlights:

- Leading Product Type: Surface-mount capacitors dominate with an over 60% share in 2025, driven by their compact size, high reliability, low ESR, and compatibility with automated assembly processes.

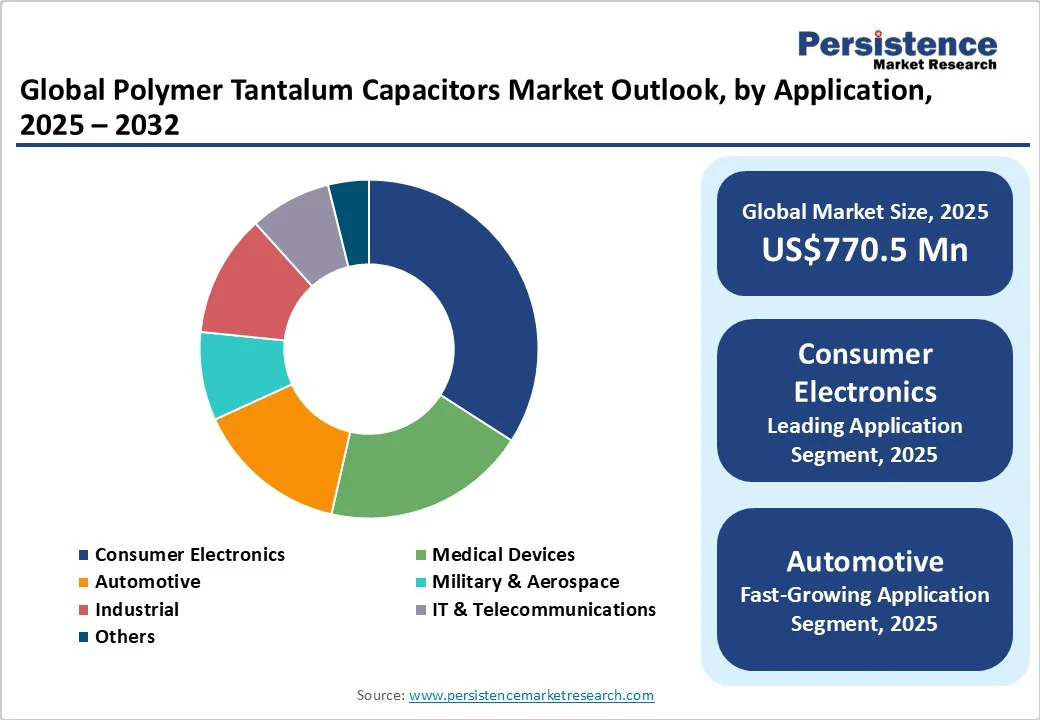

- Leading Application: Consumer electronics are expected to account for more than a 23% share in 2025, driven by increasing demand for energy-efficient, miniaturized devices that require high capacitance. Automotive is the fastest-growing application, fueled by EV adoption, ADAS integration, and electrification, with polymer tantalum capacitors critical for powertrain control, battery management, and infotainment systems.

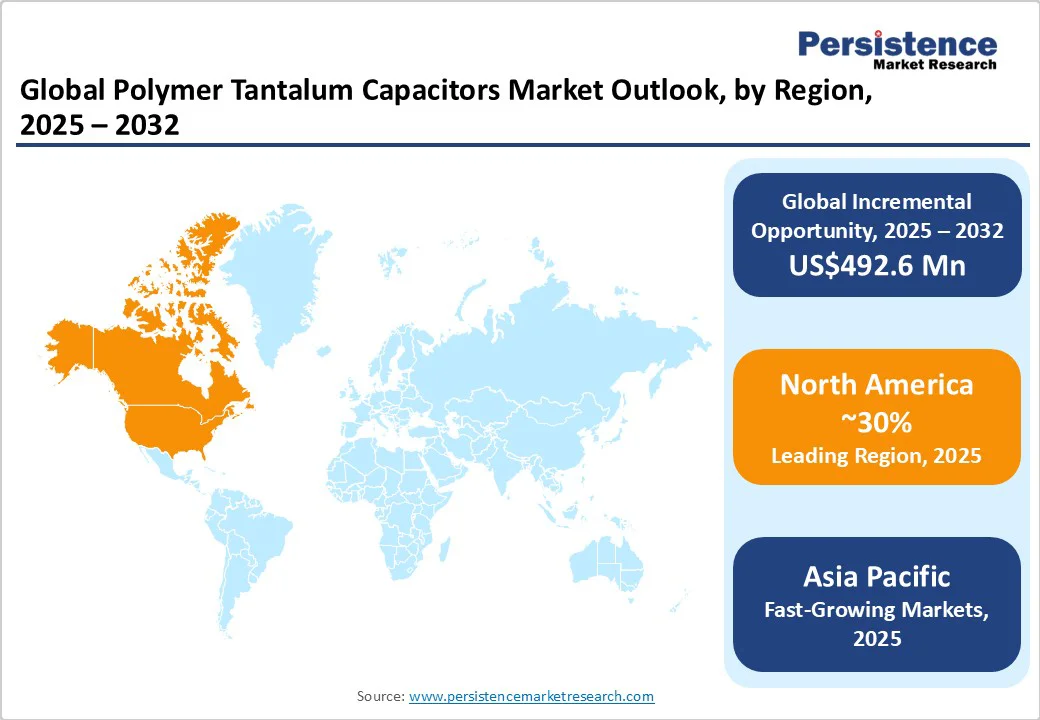

- Leading Region: North America accounts for over 30% share in 2025, supported by advanced semiconductor manufacturing, EV adoption, and defense/aerospace applications. Asia-Pacific is the fastest-growing region, led by China’s EV market.

- Key Opportunity: Integration in renewable energy systems and ADAS/automotive electronics drives growth. Polymer tantalum capacitors enhance efficiency and reliability in power converters, inverters, and energy storage, while supporting advanced automotive safety features.

| Key Insights | Details |

|---|---|

|

Polymer Tantalum Capacitors Market Size (2025E) |

US$770.5 Mn |

|

Market Value Forecast (2032F) |

US$1,263.1 Mn |

|

Projected Growth (CAGR 2025 to 2032) |

7.3% |

|

Historical Market Growth (CAGR 2019 to 2024) |

3.5% |

Market Dynamics

Driver - 5G Infrastructure Deployment and IoT Expansion

The rapid expansion of the telecommunications sector is driving demand for high-frequency, stable capacitors. Global 5G connections reached 2.25 billion in 2024, expanding at four times the rate of 4G LTE adoption, with projections indicating 8.3 billion 5G connections by 2029. The IoT ecosystem expanded to 18.8 billion connected devices in 2024, with enterprise IoT adoption showing that 51% of companies plan budget increases. The convergence of 5G and IoT technologies demands capacitors with superior frequency response and environmental stability, positioning polymer tantalum capacitors as critical components in network infrastructure, edge computing, and next-generation communication systems.

Medical Device Technology Advancement and Regulatory Requirements

The increasing adoption of connected medical devices, remote monitoring systems, and portable diagnostic equipment requires compact, reliable capacitors with extended operational lifespans and consistent performance in critical applications. Tantalum capacitors' biocompatibility makes them ideal for use in medical implants and surgical instruments, supporting market growth driven by aging populations and advancements in healthcare. The stringent regulatory standards for medical devices drive the market toward materials offering reliability and safety, positioning tantalum capacitors favorably.

Growing Need for Enhanced Durability and Efficiency in Industrial Automation and Robotics

Industrial automation and robotics are experiencing rapid growth as industries strive to enhance productivity, streamline operations, and minimize manual intervention. Polymer tantalum capacitors are increasingly preferred in these applications due to their robust construction and ability to endure harsh environments characterized by temperature fluctuations, vibrations, and electromagnetic interference. Their durability ensures reliable performance over extended periods, minimizing downtime and reducing maintenance costs, making them a critical component for manufacturers and system integrators in demanding industrial settings.

Restraint - Tantalum Supply Chain Vulnerabilities

Significant supply chain risks affect polymer tantalum capacitors due to the geographic concentration of tantalum mining. The Democratic Republic of Congo and Rwanda together account for 58% of global tantalum production, representing approximately 1,230 metric tons in 2024. Political instability in these regions has resulted in 30-35% production capacity becoming inaccessible, with the M23 rebel offensive since January 2024 disrupting traditional mining operations. This concentration creates price volatility, with tantalum ore prices experiencing 8% decrease to US$190 per kilogram in 2023 despite supply constraints, indicating complex market dynamics affected by stockpile adjustments and demand fluctuations.

Voltage and Performance Limitations

Polymer tantalum capacitors offer superior ESR characteristics, but they face inherent voltage limitations compared to traditional tantalum capacitors. The maximum voltage ratings typically range from 35V to 75V, restricting their application in high-voltage systems. The temperature coefficient and aging characteristics of polymer materials significantly impact long-term performance stability in extreme operating conditions, necessitating careful application design and derating considerations.

Opportunity - Renewable Energy System Integration

The global renewable energy sector is experiencing unprecedented growth, with investments in clean energy technologies and infrastructure surpassing US$3 trillion in 2024, of which US$2 trillion was allocated to clean energy technologies and infrastructure. This surge is further evidenced by a record US$386 billion invested in renewable energy projects in the first half of 2025, marking a 10% increase from the previous year. Polymer tantalum capacitors play a crucial role in power converters, inverters, and energy storage systems, ensuring efficiency and reliability in these applications. The European Union's Green Deal initiatives continue to promote automation technologies that reduce carbon footprints, creating a favorable regulatory environment for advanced capacitor technologies in renewable energy applications.

Advanced Driver Assistance Systems (ADAS) Integration

The shift toward autonomous driving is significantly boosting demand for high-performance capacitors in automotive electronics. Polymer tantalum capacitors are crucial for ADAS features such as automatic emergency braking, adaptive cruise control, and lane departure warning, due to their high capacitance, low ESR, and stability under extreme conditions. By 2023, 10 out of 14 ADAS functions had achieved a market penetration of over 50%, with five features surpassing 90%, highlighting the rapid adoption of these technologies.

Government safety mandates such as Bharat NCAP further drive the integration of reliable capacitors in vehicles. Increasing consumer demand for advanced safety and sensor technologies underscores the growing market potential for polymer tantalum capacitors in modern vehicles.

Category-wise Analysis

By Product Type, Surface-Mount Capacitors Drives Miniaturization and High-Reliability Electronics

Surface-mount are expected to account for more than 60% share in 2025 due to their compact size, high reliability, and compatibility with automated assembly processes. They meet the growing need for miniaturization in electronics such as smartphones, automotive control units, and aerospace systems. Their low ESR (equivalent series resistance) and stable performance under high temperatures make them ideal for high-density and high-frequency circuit designs.

Radial are expected to grow at the highest rate due to their radial design, which provides superior mechanical stability, higher capacitance per volume, and better heat dissipation ideal for high-vibration and high-temperature environments. Increasing adoption in EV powertrains, telecommunication infrastructure, and energy-efficient systems further drives their growth. Their ease of automated assembly and compact footprint make them highly suitable for modern electronics with space constraints.

By Application, Consumer Electronics Drive Growth Through High-Performance, Compact Devices, 5G, and AI Integration

Consumer electronics are expected to account for more than 23% of the market share in 2025, driven by growing demand for compact, high-performance devices such as smartphones, laptops, wearables, and gaming consoles. Smartphone production is projected to exceed 1.4 billion units annually, and the proliferation of IoT devices is expected to drive consistent demand. These capacitors offer high capacitance, low ESR, and superior stability, making them ideal for power management and miniaturized circuit designs. The rise in 5G-enabled and AI-driven electronics further accelerates the need for reliable, efficient capacitors to ensure performance, energy efficiency, and device longevity.

Automotive is expected to grow rapidly, driven by vehicle electrification and the increasing integration of advanced electronics. Global automotive sales are projected to reach approximately 90 million units in 2025, with Asia accounting for more than half of passenger vehicle sales. It offers superior reliability, high capacitance density, and excellent stability under harsh operating conditions, making it ideal for powertrain control, infotainment, ADAS, and battery management systems. The transition from conventional vehicles to electric and hybrid powertrains significantly increases electronic content per vehicle, with each EV integrating multiple polymer tantalum capacitors in critical power management and control circuits.

Regional Insights

North America Polymer Tantalum Capacitors Market Trends

North America is expected to account for more than 30% share in 2025, characterized by advanced technology adoption and high-value applications. The region's 5G connections reached 289 million in 2024, covering 77% of the population. The region benefits from established semiconductor and electronics manufacturing capabilities, with major companies investing in automation and smart manufacturing technologies. Government initiatives promoting electric vehicle adoption and renewable energy systems create supportive policy frameworks for advanced capacitor technologies.

Military and aerospace applications represent significant value segments, with defense contractors requiring components meeting stringent MIL-SPEC standards. The introduction of MIL-PRF-32700/2 qualified polymer tantalum capacitors demonstrates industry commitment to serving these demanding markets with documented reliability and performance characteristics. The convergence of AI, IoT, and manufacturing automation creates sustained demand for capacitors with superior frequency response and environmental stability.

Asia Pacific Polymer Tantalum Capacitors Market Trends

Asia-Pacific is the fastest-growing market for polymer tantalum capacitors, driven by rapid EV adoption, expanding consumer electronics production, and massive telecom infrastructure investments, including China’s ~4.5 million 5G base stations. Established semiconductor and electronics industries in Japan, South Korea, and Taiwan, combined with manufacturing cost advantages and skilled labor, support regional dominance.

Industrial automation, smart factories, and renewable energy projects in China, Japan, and India increase demand, as these capacitors are essential in power management, control systems, and energy storage due to their efficiency, durability, and thermal stability. According to IEA, China’s EV market leadership, with over 11 million vehicles sold in 2024, with global EV sales reaching 17 million units, further fuels regional demand, while the concentration of major electronics brands and contract manufacturers creates synergistic ecosystems driving innovation and cost optimization.

Europe Polymer Tantalum Capacitors Market Trends

Europe’s polymer tantalum capacitor demand is driven by its leadership in automotive electronics, including EVs and autonomous driving, and supportive EU regulations such as the Green Deal, promoting energy-efficient technologies. Key markets such as Germany, UK, France, and Spain show strong adoption of industrial automation and smart factory solutions, aligning with capacitors’ reliability and precision. Renewable energy investments in wind and solar, along with advanced grid management, further boost demand for high-performance, long-life capacitors.

Germany leads EU car production at 20%, followed by Spain, Czechia, France, and Slovakia, reinforcing consistent market growth across automotive and industrial sectors. The EU’s cautiously optimistic GDP growth of 1.1% in 2025 supports sustained industrial and technological expansion.

Competitive Landscape

The global polymer tantalum capacitors market demonstrates a consolidated structure with several established players maintaining significant market positions through technological innovation, manufacturing scale, and application expertise. Leading companies control approximately 70 - 80% of the global share, with the remainder distributed among specialized regional manufacturers and emerging technology providers. Companies are competing on performance parameters including ESR characteristics, voltage ratings, temperature stability, and reliability metrics.

Key Industry Developments:

- In September 2025, Panasonic Industry Co., Ltd. announced the upcoming mass production of its new conductive polymer tantalum solid capacitors models 50TQT33M and 63TQT22M, offering ultra-high withstand voltage, high capacitance, and an industry-low 3 mm profile.

- In March 2024, KEMET launched the industry’s first T581 SMD polymer tantalum capacitors qualified under the new MIL-PRF-32700/2 military specification. These 35V-rated capacitors deliver ultra-low ESR, high reliability, and superior performance for aerospace and defense power management applications. KEMET plans to expand its military-grade portfolio with additional CV ratings and the upcoming T580 series.

Companies Covered in Polymer Tantalum Capacitors Market

- YAGEO Corporation (Kemet)

- Kyocera AVX Corporation

- Panasonic Holdings Corporation

- Vishay Intertechnology, Inc.

- Hitachi AIC

- Samsung Electro Mechanics

- Matsuo Electric Co.,Ltd.

- Hunan Xiangyee Electronic Technology Co. Ltd

- Others

Frequently Asked Questions

The global polymer tantalum capacitor market is likely to value at US$770.5 Mn in 2025.

The growing demand for compact, high-reliability capacitors where efficiency, durability, and stable performance are critical.

The market is poised to witness a CAGR of 7.3% from 2025 to 2032.

Growing adoption of electric vehicles, advanced driver assistance systems (ADAS) creates strong growth opportunities.

YAGEO Corporation (Kemet), Kyocera AVX Corporation, Panasonic Holdings Corporation, Vishay Intertechnology, Inc., Hitachi AIC are among the leading key players.