- Semiconductor Materials & Components

- Mobile Phone and Smart Phone Market

Mobile Phone and Smart Phone Market Size, Share, and Growth Forecast, 2025 - 2032

Mobile Phone and Smart Phone Market by Operating System Type (Android, IOS, Others), Price (Entry-level, Mid-range, Premium), Distribution Channel (Operator/Carrier Stores, Brand-Owned Retail, Multi-brand Physical Retail, Online Direct-to-Consumer), and Regional Analysis for 2025 - 2032

Mobile Phone and Smart Phone Market Size and Trends Analysis

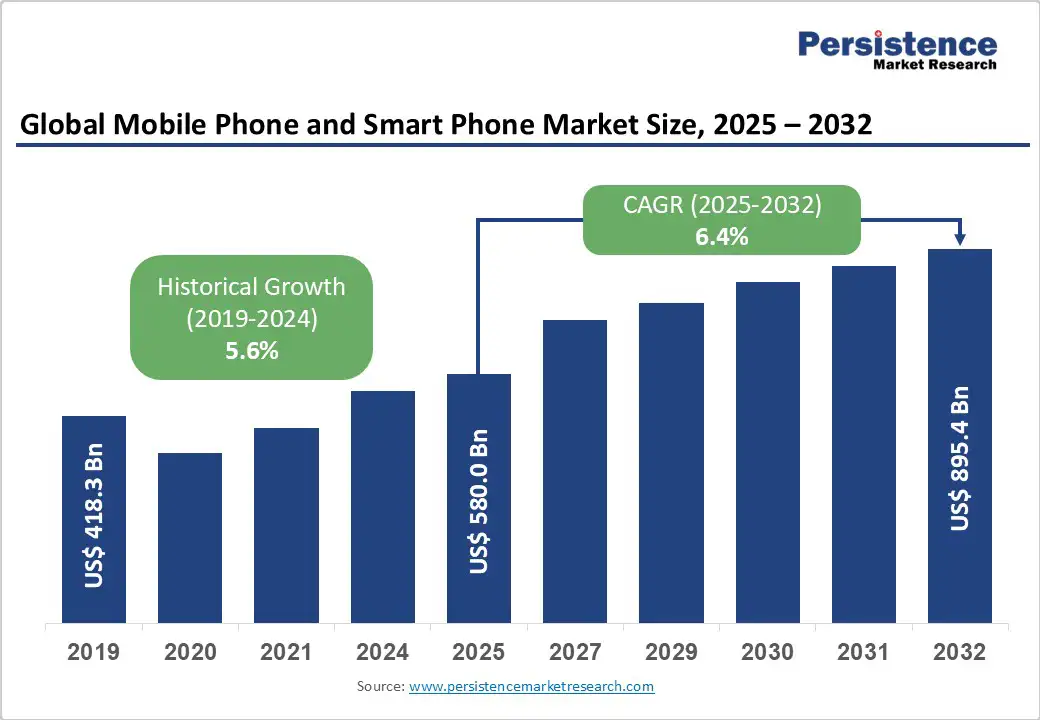

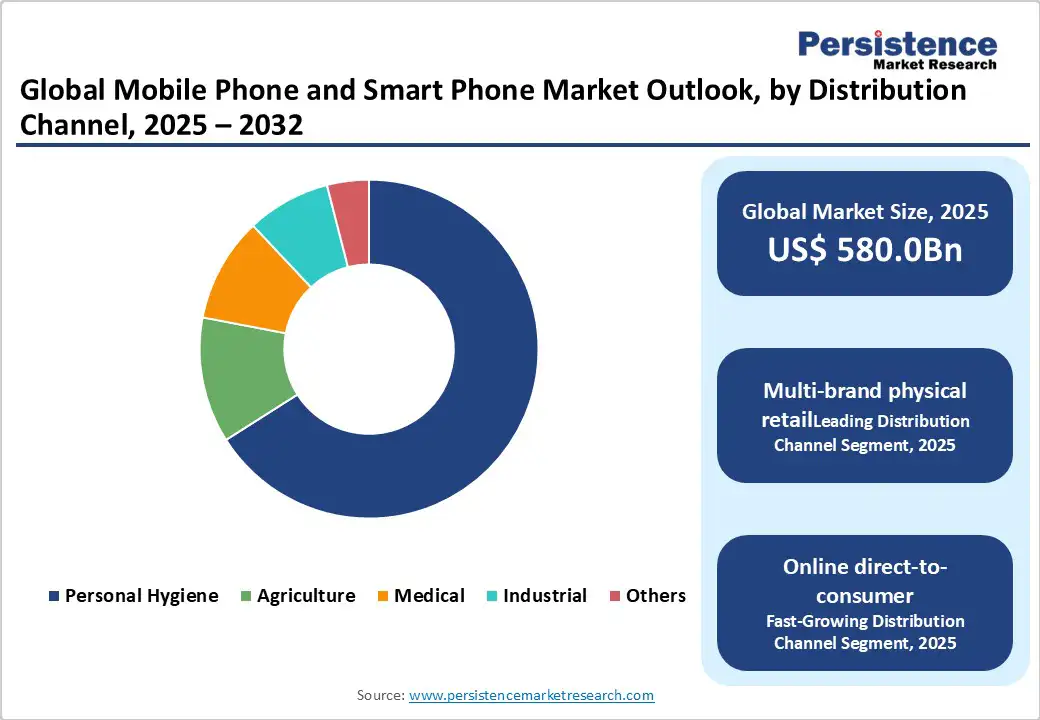

The global mobile phone and smart phone market size is likely to be valued at US$580.0 Billion in 2025 and expected to reach US$895.4 Billion by 2032, registering a robust CAGR of 6.4% during the forecast period from 2025 to 2032, fueled by the increasing demand for high-speed wireless communication solutions, advancements in smartphone technologies, and a global push toward enhancing network infrastructure and connectivity.

The industry’s expansion is further supported by efforts to enhance data transmission efficiency, foster 5G deployment, and improve connectivity for remote and urban areas.

Key Industry Highlights:

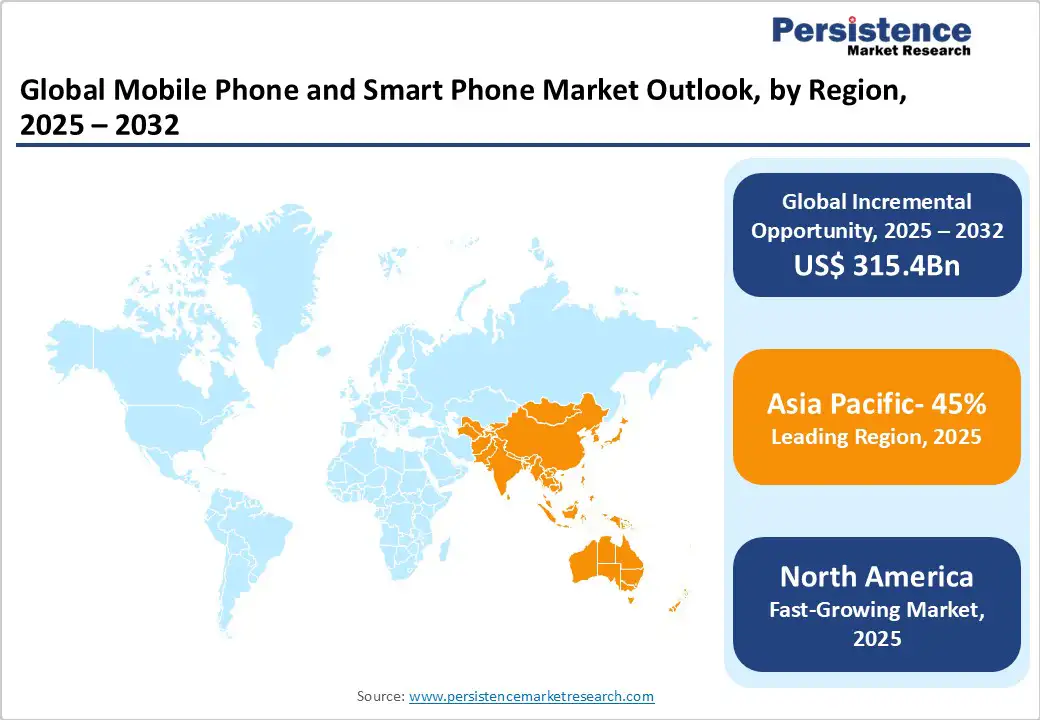

- Leading Region: Asia Pacific holds a 45% market share in 2025, driven by advanced telecommunications infrastructure, widespread adoption of innovative smartphones, and significant investments in network research.

- Fastest-growing Region: North America, propelled by the increasing prevalence of digital transformation, urbanization, and expanding telecom access in countries such as the United States and Canada.

- Dominant Operating System Type: Android accounts for approximately 81% of the global mobile phone and smartphone market share in 2025, owing to its critical role in versatile device compatibility and advancements in open-source ecosystems.

- Popular Price segment: Mid-range with a 40% share, reflecting its critical role in balancing features and affordability for mass adoption.

| Key Insights | Details |

|---|---|

|

Mobile Phone and Smart Phone Market Size (2025E) |

US$580.0 Bn |

|

Market Value Forecast (2032F) |

US$895.4 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

6.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

5.6% |

Market Dynamics

Driver - Rising Demand for High-Speed Wireless Connectivity amid Increasing 5G Deployment

The global surge in demand for high-speed wireless connectivity is a primary driver of the mobile phone and smartphone market. According to the GSMA, 5G connections are expected to exceed 2 billion worldwide by the end of 2025, with the technology enabling ultra-reliable, low-latency communications essential for IoT ecosystems and smart city initiatives. This alarming prevalence is exacerbated by an increasing data consumption rate, with global mobile data traffic expected to grow rapidly in the coming years, and rising lifestyle-related digital dependencies, as wireless networks become a leading global connectivity burden.

In response, governments and telecom operators are investing heavily in backhaul infrastructure, with the United States leading in the adoption of 5G-enabled smartphones for densification to support end-stage urban coverage gaps. In Europe, where 5G rollout cases are steadily increasing, initiatives such as the EU's Digital Decade program highlight the growing focus on spectrum-efficient wireless treatments.

Furthermore, the telecommunications sector, which accounts for a substantial portion of global connectivity expenditure, is increasingly relying on advanced smartphones to mitigate the impacts of bandwidth constraints in fiber-scarce regions. The burden of data-intensive applications is projected to increase significantly in terms of prevalence, latency requirements, and quality-of-service metrics over the coming decades.

In the Asia Pacific, young demographics are also increasingly affected, driving demand for reliable solutions such as Android-based mid-range devices. Growing investments in research focused on AI-integrated mobile challenges further boost the mobile phone and smartphone market by promoting advanced features. Overall, these factors are expected to sustain market growth, with emerging economies leading adoption through public-private partnerships and technology transfers.

Restraint - High Costs of Production and Stringent Regulatory Compliance

The high costs associated with producing advanced smartphones continue to be a significant restraint on market growth. Cutting-edge components, such as high-resolution displays, AI-enabled processors, and advanced camera modules, require sophisticated manufacturing techniques, which substantially increase production expenses compared to those of standard devices. These elevated costs pose challenges for manufacturers seeking to maintain competitive pricing while incorporating the latest technological innovations.

Regulatory compliance further adds to these financial pressures. Meeting stringent standards set by authorities such as the FCC in the United States and regulatory bodies in the European Union requires extensive testing and certification for electromagnetic emissions, data privacy, and device safety. These processes are time-intensive, which delays product launches and increases overall operational costs.

Supply chain vulnerabilities also restrict market scalability. Sourcing rare materials and high-quality components can be unpredictable due to geopolitical tensions, natural disasters, or production bottlenecks, which may disrupt manufacturing schedules and inflate costs. Smaller manufacturers, in particular, struggle to absorb these expenses, limiting their ability to compete effectively. Collectively, these financial, regulatory, and logistical challenges hinder accessibility, slow adoption in price-sensitive regions, and act as a key barrier to market expansion.

Opportunity - Innovation in Formulations and E-commerce Expansion

Advancements in foldable smartphone designs and AI-driven functionalities present significant opportunities for market growth. Foldable form factors allow manufacturers to offer larger, flexible screens in compact devices, enhancing multitasking, media consumption, and productivity, which appeals to premium and tech-savvy consumers. The integration of on-device generative AI and intelligent assistants further enhances the user experience by enabling faster, context-aware interactions, predictive content suggestions, and personalized applications, creating a competitive advantage for innovative brands.

E-commerce platforms are transforming distribution channels, providing direct-to-consumer access to the latest devices, accessories, and software updates. This approach enhances reach in both urban and semi-urban markets, streamlines device upgrades, and fosters brand loyalty. Strategic partnerships with streaming platforms, gaming services, and content providers amplify the value proposition of high-end smartphones, particularly in emerging markets where digital consumption is rapidly increasing. Collectively, these technological innovations, combined with digital sales channels and ecosystem partnerships, create a robust growth environment, driving the adoption of premium devices and expanding revenue streams for manufacturers worldwide.

Category-wise Analysis

Operating System Type Insights

The global mobile phone and smart phone market is segmented into Android, IOS, and others. Android dominates, holding approximately 81% of market share in 2025, due to its proven efficacy in customization, app availability, and integration into diverse hardware protocols. Android systems are widely used in mid-range and entry-level devices, offering scalability that reduces development costs.

IOS is the fastest-growing segment, driven by increasing demand for premium ecosystems in developed markets. IOS provides seamless integration as ecosystem-locked options, with advancements in privacy features and app optimization making them suitable for long-term use in high-end populations.

Price Insights

The mobile phone and smart phone market is segmented into entry-level, mid-range, and premium. Mid-range dominates, holding approximately 40% of market share in 2025, due to its balance of performance and affordability, feature-rich designs, and integration into emerging market regimens. Mid-range devices are widely used in growing economies, offering value that reduces entry barriers.

Premium is the fastest-growing segment, driven by increasing demand for advanced features such as AI and high-refresh screens. Premium smartphones provide luxury experiences as aspirational options, with advancements in camera tech and build quality making them suitable for long-term use in affluent populations.

Distribution Channel Insights

The mobile phone and smart phone market is segmented into operator/carrier stores, brand-owned retail, multi-brand physical retail, and online direct-to-consumer. Multi-brand physical retail dominates, holding approximately 35% of market share in 2025, due to its proven efficacy in hands-on comparisons, immediate availability, and integration into traditional shopping protocols. Multi-brand stores are widely used in urban areas, offering variety that reduces decision friction.

Online direct-to-consumer is the fastest-growing segment, driven by increasing demand for convenient purchasing in digital-savvy populations. Online channels provide personalized recommendations as virtual options, with advancements in AR try-ons and fast shipping making them suitable for long-term use in remote populations.

Regional Insights

North America Mobile Phone and Smart Phone Market Trends

North America is emerging as the fastest-growing region in the global mobile phone and smartphone market, driven by a well-developed telecommunications infrastructure, substantial investments in network expansion, and a strong cultural emphasis on digital connectivity and technological innovation. The United States serves as the primary growth hub, supported by widespread smartphone adoption and the rapid rollout of 5G networks, which are enhancing mobile internet speeds, reducing latency, and enabling next-generation applications.

Key market drivers include regulatory support for spectrum allocation, which encourages innovation and facilitates high-speed connectivity for consumers and enterprises alike. Rising consumer preference for premium and AI-integrated devices is fueling demand for advanced smartphones, while the growth of e-commerce platforms allows for direct-to-consumer sales, simplified upgrades, and greater reach into urban and semi-urban areas.

Additionally, research funding from leading institutions promotes the development of foldable designs, advanced AI functionalities, and immersive user experiences. These combined technological, regulatory, and infrastructural factors ensure North America remains at the forefront of smartphone adoption, innovation, and market expansion globally.

Europe Mobile Phone and Smartphone Market Trends

Europe represents a significant portion of the global mobile phone and smartphone market, driven by stringent data privacy regulations, a strong tradition of technological innovation, and increasing consumer demand for sustainable devices. Leading countries such as Germany and the United Kingdom are key contributors to regional growth. The EU’s Digital Markets Act encourages fair competition and supports diverse operating system options in consumer electronics, fostering innovation and broader adoption.

Germany, with its advanced manufacturing base and strong consumer preference for eco-friendly devices, continues to invest heavily in research and development, supporting the production of mid-range Android smartphones for enterprise and personal use. The United Kingdom benefits from streamlined regulatory approvals post-Brexit, facilitating the adoption of premium iOS devices and encouraging growth in mobile-based financial services.

Cross-border collaborations and coordinated supply chains across Europe enhance efficiency and promote the use of sustainable components, reinforcing the region’s emphasis on innovation, consumer protection, and environmental responsibility. These factors collectively position Europe as a stable and growing market for smartphones

Asia Pacific Mobile Phone and Smart Phone Market Trends

Asia Pacific dominates the global mobile phone and smartphone market, expected to account for 45% of market share in 2025, driven by population growth, digital intensification, and shifting attitudes toward connectivity. Leading countries such as China and India are central to this expansion, supported by government-backed digital initiatives that promote network modernization, widespread 5G adoption, and enhanced access to advanced devices. Rising middle-class smartphone ownership is fueling demand across both urban and rural markets, creating opportunities for entry-level, mid-range, and premium devices.

In China, a strong focus on export-quality hardware and innovation is driving growth in the premium smartphone segment, while e-commerce platforms facilitate widespread access and efficient distribution in densely populated urban areas. India’s digital programs and subsidies for affordable smartphones are addressing entry-level needs, particularly in rural and semi-urban regions, expanding the mobile phone and smartphone market base.

Combined with increasing technological literacy, growing mobile internet penetration, and investments in infrastructure, these factors position the Asia Pacific as the most dominant and fastest-growing region in the global smartphone market, offering scalable, cost-efficient solutions to a vast and diverse population.

Competitive Landscape

The global mobile phone and smartphone market is moderately fragmented, comprising a mix of established international brands and emerging regional players. Key companies focus on continuous innovation, including AI integration, foldable designs, and enhanced camera systems, to differentiate their offerings. Strategic mergers, acquisitions, and partnerships facilitate geographic expansion, while investments in supply chains, R&D, and digital sales channels enable the capture of emerging opportunities and address growing consumer demand for connected, high-performance devices worldwide.

Key Developments

- In 2025, Apple Inc. launched a redesigned iPhone SE with 5G and A16 chip, enhancing entry-level offerings.

- January 2024: SAMSUNG announced a partnership with research institutions for advanced AI-integrated foldable screens.

Companies Covered in Mobile Phone and Smart Phone Market

- Apple Inc.

- SAMSUNG

- Oppo

- Huawei Device Co., Ltd.

- OnePlus

- Sony Group Corporation

- Xiaomi

- HTC Corporation

- Google LLC

- ZTE Corporation

Frequently Asked Questions

The mobile phone and smart phone market is projected to reach US$580.0 Bn in 2025.

Rising demand for high-speed connectivity, technological advancements in AI, and government initiatives for 5G are key drivers.

The mobile phone and smart phone market is poised to witness a CAGR of 6.4% from 2025 to 2032.

Innovations in foldable designs and e-commerce expansion, such as AI features, present significant growth opportunities.

Apple Inc., SAMSUNG, Oppo, Huawei Device Co., Ltd., OnePlus, Sony Group Corporation, Xiaomi, HTC Corporation, Google LLC, and ZTE Corporation are among the leading players, known for their innovative smartphone solutions.