- Specialty & Fine Chemicals

- Synthetic Tartaric Acid Market

Synthetic Tartaric Acid Market Size, Share, and Growth Forecast 2026 - 2033

Synthetic Tartaric Acid Market by Grade (Food Grade, Pharmaceutical Grade, Industrial Grade, and Cosmetic Grade), Form (Anhydrous Powder, Crystalline Powder, Granules, and Liquid), Purity (≥99.5%, 99.0-99.4%, 95.0-98.9%,and <95%), End-user (Food & Beverages, Pharmaceuticals, Cosmetics & Personal Care, Chemical Intermediates, Detergents & Cleaners), and Regional Analysis, 2026 - 2033

Synthetic Tartaric Acid Market Size and Trend Analysis

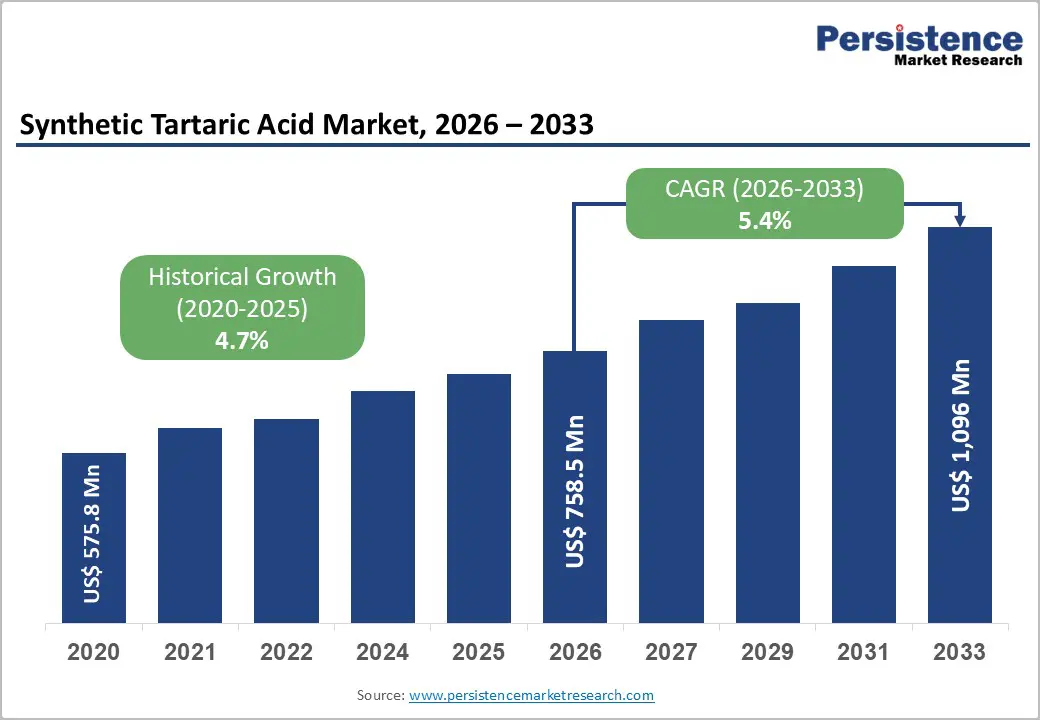

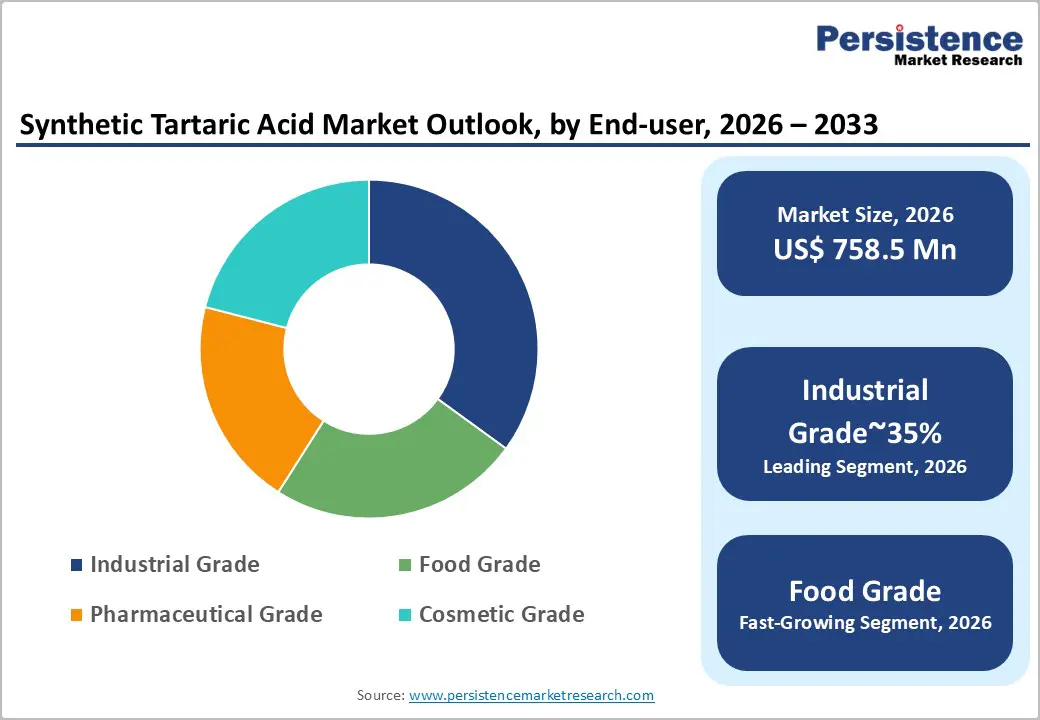

The global synthetic tartaric acid market size is likely to be valued at US$ 758.5 million in 2026 and is expected to reach US$ 1,096.1 million by 2033, growing at a CAGR of 5.4% during the forecast period between 2026 and 2033.

The market trajectory is fundamentally underpinned by the structural shift in global supply chains away from agricultural dependence toward chemically stable alternatives.

Key Industry Highlights:

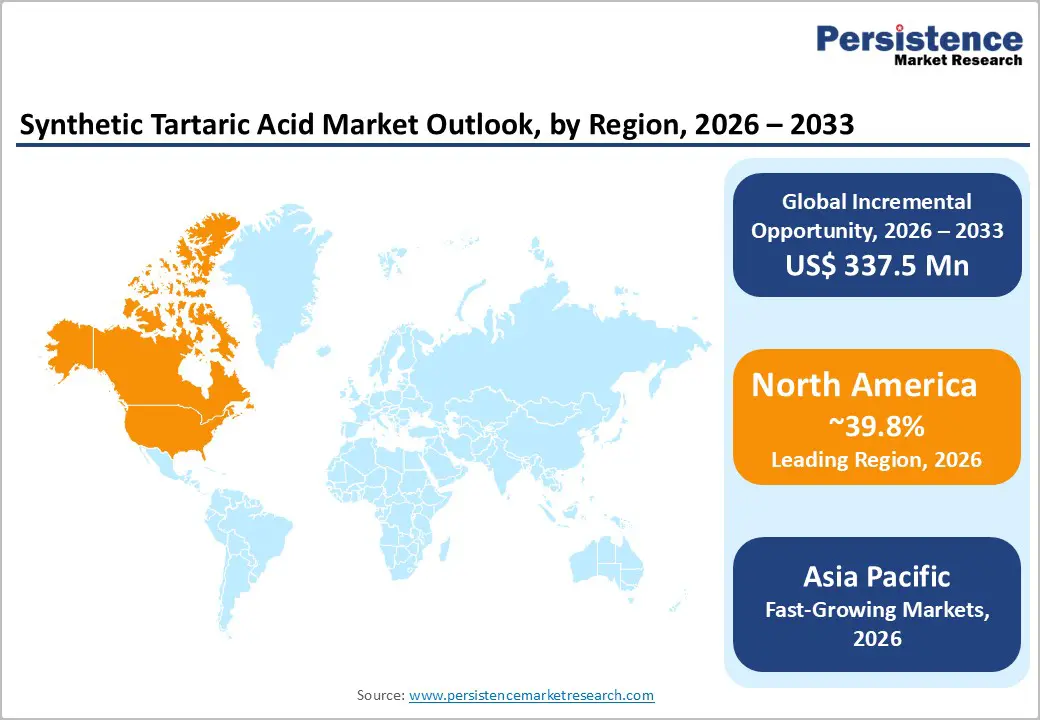

- Leading Region: North America dominates the market, having 39.8% share, due to demand from the construction and pharmaceutical industries, with the United States being the largest consumer in the region.

- Fastest Growing Region: Asia Pacific is projected to witness the highest growth rate of around 7.6%, driven by urbanization and booming pharmaceutical sectors.

- Dominant Segment: Food & Beverages remains the largest end-user segment holding 35% share, utilizing tartaric acid for acidity regulation and preservation.

- Fastest Growing Segment: Industrial Grade is the fastest-growing application with rising CAGR of 6.4%, fueled by the demand for retardants in gypsum and cement.

- Key Market Opportunity: Biochemo-enzymatic synthesis offers a sustainable, cost-effective route to produce high-purity L(+)-tartaric acid.

| Key Insights | Details |

|---|---|

| Synthetic Tartaric Acid Market Size (2026E) | US$ 758.5 Million |

| Market Value Forecast (2033F) | US$ 1,096.1 Million |

| Projected Growth CAGR (2026 - 2033) | 5.4% |

| Historical Market Growth (2020 - 2025) | 4.7% |

Market Dynamics

Drivers - Rising Infrastructure Development Accelerates Synthetic Tartaric Acid Demand in Gypsum and Cement-Based Construction Applications

The rapid expansion of the global construction and building materials industry is a key driver for synthetic tartaric acid demand, particularly due to its effective role as a setting-time retarder in gypsum- and cement-based products. In modern construction practices such as self-leveling floor screeds, molding plaster, and drywall systems, precise control over setting time is essential to ensure smooth application, improved workability, and long-term structural strength.

Synthetic DL-tartaric acid functions as a chelating agent that binds calcium ions, slowing gypsum hydration and preventing premature hardening. This functionality is especially valuable in fast-paced urban infrastructure projects across emerging economies, where speed, efficiency, and material optimization are critical. Industry data consistently shows a strong link between urbanization rates and rising demand for chemical admixtures. As construction companies seek cost-effective and reliable alternatives to natural retardants, synthetic tartaric acid stands out due to its lower cost, consistent ≥99.5% purity, and stable performance. This has resulted in strong volume-driven growth independent of food-related demand.

Maleic Anhydride-Based Synthetic Production Ensures Year-Round Supply Stability and Reduces Agricultural Dependency Risks

The increasing shift toward maleic anhydride-based synthetic production represents a major structural growth driver by reducing supply risks associated with agriculture-dependent raw materials. Natural tartaric acid production relies heavily on wine output, making it vulnerable to climate variability, poor grape harvests, and supply shortages that often cause price volatility. In contrast, synthetic tartaric acid is produced using maleic anhydride, a petrochemical derivative that allows continuous, scalable, and year-round manufacturing.

Recent advancements, including biochemo-enzymatic technologies developed by players such as Hangzhou Bioking, have further strengthened this production route by enabling high-purity L(+)-tartaric acid with optical quality comparable to natural sources. This reliability appeals strongly to multinational food and pharmaceutical companies that require consistent supply, long-term contracts, and predictable operating costs. By eliminating seasonal constraints and improving supply stability, synthetic producers gain a logistical and commercial advantage, steadily capturing market share from traditional natural tartaric acid suppliers.

Restraint - Stricter EU Food Additive Regulations Increase Compliance Costs and Slow Synthetic Tartaric Acid Adoption in Premium Markets

One of the most significant restraints affecting the synthetic tartaric acid market is the tightening regulatory framework in the European Union. Commission Regulation (EU) 2024/1451, introduced in May 2024, revised usage conditions for tartaric acid (E334) and tartrates by removing their “quantum satis” status across several food categories and imposing strict numerical limits. Following EFSA’s re-evaluation, a group Acceptable Daily Intake (ADI) of 240 mg/kg body weight was established, forcing food manufacturers to reformulate products to remain compliant.

This shift raises compliance costs and creates higher entry barriers for synthetic tartaric acid suppliers targeting the EU food and beverage sector. The regulation also intensifies scrutiny under the clean-label movement, where synthetic additives face consumer resistance. To comply, manufacturers must invest heavily in advanced testing, traceability, and documentation to prove purity and residue compliance, slowing adoption in premium food applications across the region.

Fluctuating Petrochemical Feedstock Prices Challenge Cost Stability and Profit Margins for Synthetic Tartaric Acid Producers

Synthetic tartaric acid production is highly dependent on maleic anhydride, exposing manufacturers to fluctuations in global petrochemical markets. Maleic anhydride is derived from benzene or n-butane, both of which are closely linked to crude oil and natural gas prices. Geopolitical tensions, OPEC+ production decisions, supply chain disruptions, and global energy transitions directly influence feedstock costs. When oil prices rise sharply, production expenses for synthetic tartaric acid increase, narrowing or eliminating its traditional cost advantage over natural tartaric acid.

This volatility poses a major challenge for producers operating in price-sensitive industrial segments. Additionally, stricter environmental regulations related to carbon emissions, particularly in major manufacturing hubs such as China, add further operational and compliance costs. Together, these factors create financial uncertainty and make long-term pricing agreements more difficult, limiting market stability compared to natural tartaric acid sourced from localized wine-producing regions.

Opportunity - Enzymatic Synthesis Innovations Enable Sustainable, High-Purity L(+) Tartaric Acid for Premium Food and Pharmaceutical Markets

Significant growth opportunities emerge based on the expansion of biochemo-enzymatic synthesis technologies, which combine synthetic efficiency with nature-identical positioning. Conventional chemical synthesis typically produces DL-tartaric acid, limiting its use in high-value food and pharmaceutical applications that require the L(+) isomer. However, advanced enzymatic processes-such as those developed by Hangzhou Bioking-use specialized enzymes like cis-epoxysuccinate hydrolase to convert maleic anhydride intermediates into high-purity L(+)-tartaric acid. These methods operate under milder conditions, consume less energy, and generate fewer by-products, aligning with green chemistry principles. This creates opportunities for manufacturers to license or develop similar technologies and offer bio-identical products that meet USP and FCC standards. By positioning enzymatically produced tartaric acid as a sustainable, low-carbon alternative, suppliers can enter premium European and North American markets traditionally dominated by natural tartaric acid producers.

Expanding Pharmaceutical Applications Drive Demand for High-Purity Synthetic Tartaric Acid in Advanced Drug Delivery Systems

The pharmaceutical sector offers strong growth potential for high-purity synthetic tartaric acid, particularly in advanced drug delivery systems and chiral resolution applications. Tartaric acid is widely used to form tartrate salts with active pharmaceutical ingredients, improving solubility, chemical stability, and bioavailability. As drug pipelines increasingly focus on complex molecules and poorly soluble compounds, demand for high-purity, consistent acidulants continues to rise.

Synthetic tartaric acid provides a key advantage through its controlled impurity profile and absence of agricultural contaminants such as pesticides or heavy metals. This makes it especially suitable for injectable and oral formulations. Beyond salt formation, tartaric acid derivatives are gaining traction in biodegradable polymers, hydrogels, and controlled-release drug systems. Manufacturers that comply with GMP standards and provide Drug Master Files can secure long-term partnerships and capture significant value in this high-margin pharmaceutical segment.

Category-wise Analysis

Grade Insights

Industrial-grade synthetic tartaric acid remains the largest volume contributor in the global market due to its widespread use in cost-sensitive, non-food applications. This segment is driven by high demand from construction, textiles, metal treatment, and chemical processing industries, where stereochemical purity is less critical than performance and price. DL-tartaric acid is widely used for chelation, surface treatment, and setting-time control in these sectors.

In 2024, the industrial grade segment accounted for a substantial share of global consumption, supported by strong infrastructure development across Asia and the Middle East. Its use as a precursor for chemical intermediates and esters further reinforces demand. Compared to food and pharmaceutical grades, industrial-grade production requires less purification, reducing manufacturing costs and enabling large-scale output. This cost advantage allows suppliers to meet high-volume demand efficiently, securing the segment’s dominance in total market tonnage.

Form Insights

Crystalline powder is the leading form of synthetic tartaric acid in terms of both volume and revenue, as it offers superior handling, storage, and application benefits. This form is preferred across food, pharmaceutical, and industrial applications due to its excellent flowability, uniform particle size, and rapid solubility in water. In food and pharmaceutical manufacturing, precise dosing is critical, and crystalline powder enables accurate measurement and consistent performance.

The form accounts for over 60% of total market share, driven by its extensive use in effervescent salts, baking powders, and beverage formulations. Manufacturers favor crystalline powder because it resists caking under proper storage conditions, ensuring longer shelf life and minimal product loss. Additionally, this form supports high purity levels, typically ≥99.5%, making it suitable for both premium and mass-market applications, reinforcing its dominant position.

Purity Insights

The ≥99.5% purity segment represents the highest-value tier in the synthetic tartaric acid market and dominates overall revenue generation. This purity level is mandatory for food, beverage, and pharmaceutical applications, where strict regulatory compliance is required. Authorities such as the FDA and EFSA enforce rigorous limits on heavy metals, oxalates, and other impurities for food additives classified under E334.

As a result, manufacturers supplying this segment must invest in advanced purification, quality control, and certification processes. Leading producers such as Changmao Biochemical consistently meet these standards, as confirmed by certificates of analysis aligned with BP, USP, and EP specifications. Products below this purity threshold are largely restricted to industrial use and cannot enter the human consumption supply chain. Due to its regulatory necessity and premium pricing, the ≥99.5% purity segment continues to command the largest share of market value.

End-userr Insights

Food and beverages remain the largest end-user segment for synthetic tartaric acid, serving as the primary revenue driver despite competition from natural alternatives. Synthetic L(+) tartaric acid is widely used as an acidulant, flavor enhancer, and pH regulator in soft drinks, bakery products, confectionery, and processed foods. Its distinctive tart taste enhances fruit flavors-particularly grape and citrus-more effectively than citric acid.

The compound is also a key ingredient in baking powders, cream of tartar substitutes, and emulsifiers such as DATEM used in bread production. The segment benefits from stable, year-round demand driven by global processed food consumption. Compared to cyclical industrial applications, food and beverage demand offers greater resilience and predictable volume growth. Cost stability, consistent quality, and functional versatility continue to make this segment the anchor of synthetic tartaric acid demand worldwide.

Regional Insights

North America Synthetic Tartaric Acid Market Trends

The North American synthetic tartaric acid market is driven largely by demand from the construction and pharmaceutical industries, with the United States leading regional consumption. Industrial-grade DL-tartaric acid is extensively used in gypsum wallboard, plaster, and specialty construction materials, where domestic natural production is insufficient in both volume and price competitiveness. As a result, the region relies heavily on imports from Asia, particularly China, to meet demand.

Regulatory clarity from the U.S. FDA has created a clear market divide: natural tartaric acid is reserved for premium wines and organic foods, while synthetic variants dominate industrial and pharmaceutical uses. Trade data shows rising import volumes through major ports such as Los Angeles and Newark. Additionally, North America’s strong innovation ecosystem supports emerging applications in advanced materials, chiral resolution, and pharmaceutical manufacturing, further strengthening regional demand.

Europe Synthetic Tartaric Acid Market Trends

Europe presents a highly regulated but strategically important market for synthetic tartaric acid. The region has a strong natural tartaric acid industry centered in Italy, Spain, and France, supported by wine production. However, regulatory tightening under EU Regulation 2024/1451 has restricted low-quality synthetic imports, particularly for food applications.

Despite this, Europe remains a significant importer of synthetic tartaric acid for non-food uses, including textiles, chemicals, and industrial processing in countries such as Germany and the U.K. A notable trend is growing acceptance of enzymatically produced synthetic L(+) tartaric acid as a “nature-identical” alternative when it meets European Pharmacopoeia standards. Regional producers, including Spain-based companies, are increasingly diversifying into high-grade synthetic products to offset grape harvest volatility, blending traditional sourcing with industrial efficiency to maintain supply stability.

Asia Pacific Synthetic Tartaric Acid Market Trends

Asia Pacific is the fastest-growing and largest production hub for synthetic tartaric acid, with China and India dominating global supply. The region benefits from well-developed petrochemical infrastructure, enabling large-scale, cost-efficient maleic anhydride-based production. Chinese manufacturers such as Hangzhou Bioking and Changmao Biochemical lead global exports, leveraging advanced enzymatic technologies to deliver high-quality L(+) tartaric acid at competitive prices.

A key regional trend is strong domestic consumption growth, driven by rising demand for processed foods, bakery products, and pharmaceuticals across China, India, and Southeast Asia. Expanding middle-class populations are absorbing a growing share of local production. Government support for integrated chemical industrial parks further reduces production costs by linking upstream and downstream operations. These structural advantages position Asia Pacific as both the manufacturing backbone and a rapidly expanding consumption market.

Competitive Landscape

The global synthetic tartaric acid market exhibits a fragmented to semi-consolidated structure, heavily dominated by Asian manufacturers. Chinese producers control the majority of global capacity, benefiting from scale, vertical integration, and secure access to maleic anhydride feedstocks. Market leaders such as Hangzhou Bioking and Changmao Biochemical differentiate themselves through proprietary enzymatic technologies that enable bio-identical L(+) tartaric acid production, essential for entry into Western food and pharmaceutical markets.

Strategic partnerships with international distributors help these companies navigate regulatory requirements in North America and Europe. Meanwhile, smaller regional players focus on niche applications or localized supply. Traditional natural tartaric acid producers are increasingly adopting hybrid sourcing models or supplementing supply with synthetic grades to mitigate grape harvest risks. This evolving competitive landscape reflects a gradual shift toward technology-driven, reliability-focused market leadership.

Key Market Developments:

- In July 2023, Alvinesa has acquired Genosa, a company that specializes in grape-based ingredients, to enhance its portfolio of naturally sourced ingredients, which also includes olive extract. Based in Spain, Genosa focuses on transforming agricultural by-products from the wine industry into natural ingredients for the beauty and personal care, nutraceutical, and food and beverage sectors.

Companies Covered in Synthetic Tartaric Acid Market

- Tártaros Gonzalo Castelló S.L

- Sagar Chemicals

- American International Chemicals LLC

- Ninghai Organic Chemical Factory

- Yantai Taroke Bio-engineering Co., Ltd

- Hangzhou Bioking Biochemical Engineering Co., Ltd

- Hangzhou Regin Bio-tech Co., Ltd.

- Changmao Biochemical Engineering Company Limited

- Brenn-O-Kem (Pty) Ltd

- Omkar Speciality Chemical Limited

- Shanhong Chemical Co, Ltd

- PAHI, S.L.

Frequently Asked Questions

The global synthetic tartaric acid market size is projected to be valued at US$ 758.5 Million in 2026.

Key demand drivers include the growing construction industry requiring gypsum retardants and the shift towards stable, non-agricultural supply chains for industrial applications.

The Industrial Grade segment commands the largest volume share, while the Food Grade segment leads in value due to purity requirements.

Asia Pacific is expected to remain the leading region, supported by extensive manufacturing infrastructure in China and rising domestic consumption.

Adopting biochemo-enzymatic synthesis technologies to produce high-purity L(+)-tartaric acid presents a significant opportunity to capture premium market segments.

Major players include Hangzhou Bioking Biochemical Engineering Co., Ltd, Changmao Biochemical Engineering Company Limited, Sagar Chemicals, and Yantai Taroke Bio-engineering Co., Ltd.