- Plastics, Polymers & Resins

- Synthetic Leather Market

Synthetic Leather Market Size, Share, and Growth Forecast 2026 - 2033

Synthetic Leather Market by Product Type (Polyurethane (PU), Polyvinyl Chloride (PVC), Silicone, Bio-based PU), Application (Footwear, Automotive, Furnishing, Clothing, Fashion Accessories, Other), and Regional Analysis for 2026 - 2033

Synthetic Leather Market Size and Trend Analysis

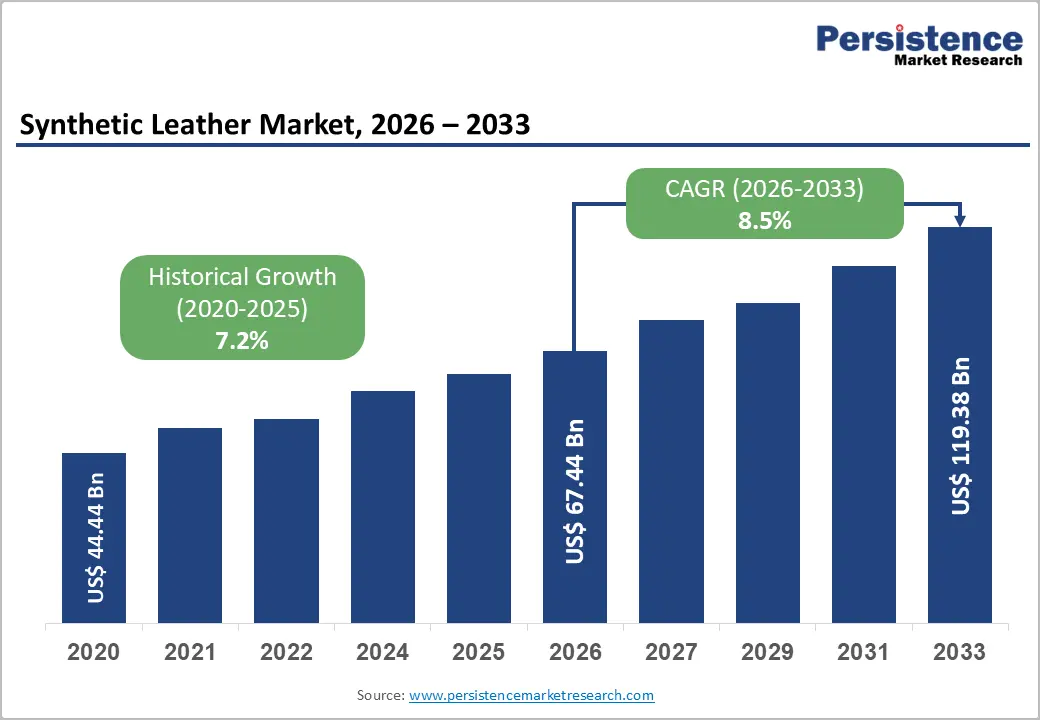

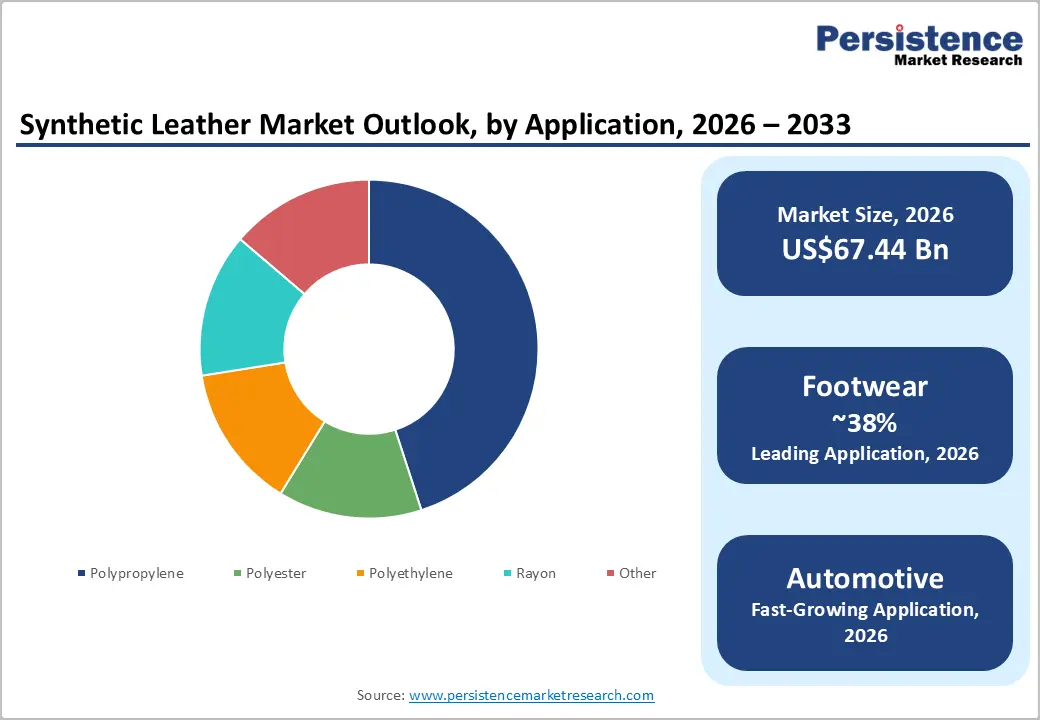

The global Synthetic Leather Market size is supposed to be valued at US$ 67.4 Bn in 2026 and is projected to reach US$ 119.4 Bn by 2033, growing at a CAGR of 8.5% between 2026 and 2033.

This robust expansion is primarily driven by the automotive industry's accelerating shift toward sustainable interior materials, with synthetic leather accounting for 45% of automotive applications in 2024, coupled with rising consumer preference for cruelty-free alternatives as the vegan fashion movement gains momentum. Additionally, technological breakthroughs such as BASF's Haptex 4.0, which achieves 100% recyclability and reduces greenhouse gas emissions by 52% relative to conventional solvent-based polyurethane leather, are fundamentally transforming manufacturing processes while addressing stringent environmental regulations across major markets.

Key Industry Highlights

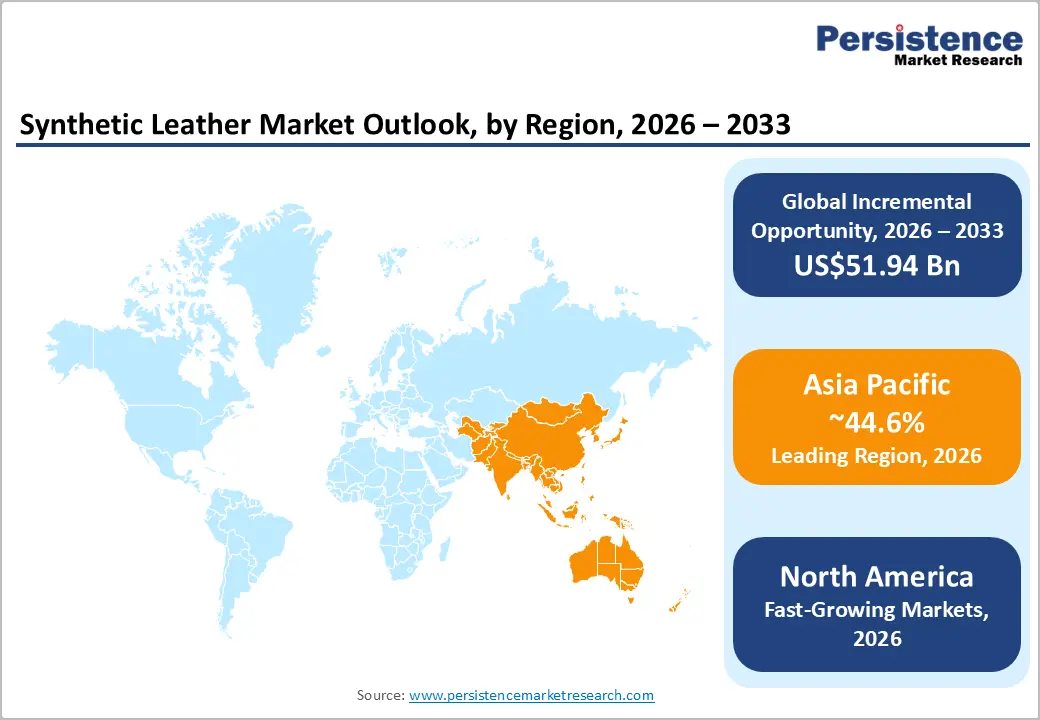

- Regional Leader: Asia Pacific leads the Synthetic Leather Market, commanding over 44.6% share, driven by massive manufacturing capacity in China, producing 1.69 million tons in the first three quarters of 2023, India's expanding footwear and automotive industries, and South Korea's technological leadership.

- Fastest-Growing Segment: North America is the fastest-growing regional market, driven by heightened consumer awareness of animal welfare, robust adoption of the vegan lifestyle, and particularly among millennials and Generation Z.

- Leading Segment: Polyurethane (PU) synthetic leather accounts for approximately 62% of the product type share, driven by superior performance characteristics, including softness, breathability, durability, and aesthetic appeal, that closely replicate those of genuine leather.

- Fastest-Growing Segment: Automotive applications are the fastest-growing segment, as electric-vehicle proliferation and premium interior demand drive synthetic leather adoption, supported by technological advancements in water-based polyurethane formulations that improve material properties.

- Key Market Opportunity: Bio-based synthetic leather innovations represent transformative opportunities as manufacturers develop materials from pineapple leaves, mushroom mycelium, apple waste, and agricultural byproducts.

| Key Insights | Details |

|---|---|

|

Synthetic Leather Market Size (2026E) |

US$ 67.4 Bn |

|

Market Value Forecast (2033F) |

US$ 119.4 Bn |

|

Projected Growth CAGR (2026-2033) |

8.5 % |

|

Historical Market Growth (2020-2025) |

7.2 % |

Market Dynamics

Drivers - Surging Automotive Industry Demand for Sustainable Interior Materials

The automotive sector has become the fastest-growing end-use industry for synthetic leather, as manufacturers increasingly adopt sustainable, high-performance interior materials. Demand is further strengthened by the transition to electric vehicles, with premium EV brands using polyurethane and bio-based alternatives to meet consumer expectations for ethical and durable cabin solutions. Market growth is further supported by the increasing production of SUVs and luxury vehicles that incorporate synthetic leather in multiple interior components.

BASF’s Haptex technology, showcased at PU TECH 2025, demonstrated significant sustainability advantages, including 52% lower greenhouse gas emissions and notable reductions in energy and water use. China’s automotive leather output exceeded 500 million square feet in 2024, with projected growth of 6-8% in 2025, driven by expanding vehicle manufacturing and increasing demand for premium interiors.

Rising Consumer Preference for Ethical and Cruelty-Free Alternatives

The global shift toward ethical and sustainable consumption is significantly reshaping demand for synthetic leather as consumers increasingly avoid animal-derived materials in favor of cruelty-free alternatives. This trend is especially prominent among millennial and Generation Z consumers, who prioritize sustainability certifications when purchasing footwear, clothing, fashion accessories, and furnishings. The vegan fashion movement continues to expand, with rising demand for animal-free labels and transparency in manufacturing practices.

The microbe-produced bioleather offers substantial environmental benefits, including up to 96.8% lower carbon emissions than polyurethane-coated polyester and 94.3% lower emissions than cotton-based synthetics. Growing demand from emerging markets, particularly China, India, South Korea, Vietnam, and Thailand, further accelerates market expansion. Advances in manufacturing now enable synthetic leather to closely replicate the appearance and durability of genuine leather, thereby mitigating ethical concerns and expanding its consumer appeal.

Restraints - Volatile Raw Material Prices and Petroleum Dependency

The synthetic leather industry faces substantial cost pressures due to volatility in raw material prices, particularly for polyurethane and other petroleum-based inputs essential to conventional production processes. As polyurethane formulations rely heavily on crude oil-derived feedstocks, manufacturers remain vulnerable to global oil price fluctuations driven by geopolitical tensions, supply disruptions, and broader macroeconomic conditions. These cost variations complicate strategic planning, often resulting in compressed margins during periods of elevated raw material prices or customer resistance when producers attempt to adjust prices.

The sector is further exposed to concentration risks, as reflected by the discrete power segment’s 28% share of the automotive semiconductor market in 2024. In addition, PVC-based synthetic leather continues to face scrutiny regarding environmental and chemical safety concerns, driving regulatory pressures that may increase compliance costs or limit usage in regions with stringent environmental standards.

Stringent Environmental Regulations on VOC Emissions

The synthetic leather industry is increasingly challenged by stringent environmental regulations aimed at reducing VOC emissions from solvent-based production processes. These rules require manufacturers to invest substantially in cleaner technologies to maintain market access. Traditional solvent-based polyurethane manufacturing generates high VOC emissions, contributing to air pollution and raising health concerns for workers and nearby communities, thereby intensifying regulatory scrutiny in developed markets.

The European Union Deforestation Regulation has also introduced strict traceability requirements, prompting a parallel examination of the sustainability of synthetic leather manufacturing and its chemical safety. Compliance demands significant capital expenditure on equipment upgrades, emission-control systems, wastewater treatment, and continuous monitoring, posing particular difficulties for smaller firms. Although these pressures are accelerating the transition to water-based and solvent-free formulations, the shift creates competitive disparities and short-term profitability challenges across the industry.

Opportunities - Bio-Based and Circular Economy Innovations

The emergence of bio-based synthetic leather technologies presents a significant opportunity for the industry, as manufacturers develop materials derived from plant waste and agricultural byproducts that meet both sustainability and performance requirements. Innovations using pineapple leaves, mushroom mycelium, and apple waste have proven commercially viable, offering faster biodegradation than petroleum-based alternatives while maintaining mechanical strength and aesthetic appeal.

BASF’s Haptex 4.0, launched in July 2024, delivers 100% recyclable polyurethane synthetic leather by eliminating layer separation during recycling and enabling co-recycling with PET fabrics. This advancement addresses longstanding challenges associated with end-of-life disposal. Kuraray’s Tirrenina technology further enhances sustainability by reducing water use by 70% and CO2 emissions by 35%, while providing broad design flexibility. Growing adoption among premium automotive manufacturers reinforces the strong market potential of durable, high-quality bio-based alternatives.

Customization Capabilities and Emerging Market Expansion

The synthetic leather industry increasingly benefits from advanced customization capabilities that allow manufacturers to tailor color, texture, luster, patterns, and designs to precise customer specifications. This flexibility provides a competitive edge over natural leather, which is constrained by biological variability. Over the past five years, customized synthetic leather has become more prominent in luxury consumer goods, with companies such as Toray offering extensive design options that support brand differentiation and premium positioning.

Demand is particularly strong in fashion accessories, automotive interiors, and furnishings, where personalized aesthetics justify higher price premiums. At the same time, emerging markets offer significant growth potential as rising incomes and urbanization increase the consumption of footwear, automotive products, and furniture. China remains a major production hub, supported by new capacity investments, while the Asia Pacific maintains over 44.6% market share, driven by large-scale manufacturing across China, India, and South Korea.

Category-wise Analysis

Product Type Insights

Polyurethane (PU) synthetic leather dominates the market with an estimated 62% share due to its superior softness, breathability, durability, and aesthetic appeal, which closely replicates genuine leather while offering cost and ethical advantages. PU formulations support a wide range of texture variations, from smooth nappa to pebbled grains, making them suitable for automotive interiors, premium footwear, fashion accessories, and high-end furnishings where visual and tactile quality are essential. The automotive sector particularly favors PU for its abrasion resistance, durability, and low-maintenance properties in high-use environments.

Technological advancements, including the growing adoption of water-based PU, help manufacturers address stringent VOC-emission regulations without compromising performance. BASF’s Haptex technology further strengthens the segment by enabling 100% recyclability, reducing greenhouse gas emissions by 52%, and eliminating wet-line processing. Established infrastructure and mature supply chains create high switching costs, reinforcing PU’s market leadership.

Application Insights

Footwear applications account for approximately 38% of the synthetic leather market, driven by strong global demand, supported by population growth, rising disposable incomes, and rapid fashion cycles across casual, athletic, formal, and specialty segments. Emerging markets, particularly China, India, South Korea, Vietnam, and Thailand, continue to drive expansion, reinforcing Asia-Pacific’s leadership in synthetic leather footwear production.

Synthetic leather provides manufacturers with key advantages, including design flexibility for complex patterns and colors, consistent quality suitable for automated production, and cost predictability critical for mass-market development. Its water resistance, ease of cleaning, and durability under repeated flexing meet performance needs in athletic and casual footwear, while aesthetic improvements have increased adoption in formal and fashion-focused categories. Growing interest in cruelty-free and sustainable products further supports demand, with major brands offering dedicated vegan footwear lines.

Regional Insights

North America Synthetic Leather Market Trends

North America demonstrates strong market performance driven by increasing consumer awareness of animal welfare, growing adoption of vegan lifestyles, and regulatory frameworks that support sustainable manufacturing practices. The U.S. leads regional demand, supported by a mature consumer base that values transparency in sourcing and environmental impact, particularly among millennials and Generation Z, who are willing to pay premiums for ethically aligned products. Major automotive manufacturers in the region specify synthetic leather for interiors due to its cost predictability, design flexibility, and consistent performance.

Innovation ecosystems across North America further advance next-generation bio-based and solvent-free technologies, strengthening the region’s competitive position. Growing adoption in fashion and accessories, supported by vegan product lines and wider retail availability, continues to elevate synthetic leather’s premium perception, despite moderate headwinds from economic sensitivity.

Europe Synthetic Leather Market Trends

Europe’s synthetic leather market is shaped by stringent environmental regulations, strong animal-welfare advocacy, and advanced manufacturing capabilities concentrated in Germany, Italy, France, and Spain. These factors establish high global standards for technology and quality. The European Union Deforestation Regulation has introduced strict traceability requirements for traditional leather, indirectly benefiting synthetic alternatives that avoid deforestation concerns and allow more controlled, compliant production.

Germany’s chemical industry, led by BASF, continues to advance polyurethane formulations and sustainable coating technologies. Kuraray Europe further highlights regional innovation through its Tirrenina water-borne synthetic leather, which reduces water usage by 70% and CO2 emissions by 35%. Fashion hubs such as Milan, Paris, and London increasingly feature synthetic leather in premium collections, while German automotive manufacturers specify it to balance sustainability with performance, influencing broader market adoption.

Asia Pacific Synthetic Leather Market Trends

Asia-Pacific maintains market leadership with a share exceeding 44.6%, driven by extensive manufacturing capacity across China, India, South Korea, and Southeast Asian nations, which serve both domestic demand and global export markets. China remains the dominant producer, manufacturing 1.69 million tons of synthetic leather in the first three quarters of 2023 despite an 11% year-on-year decline, and continues to expand through 32 new projects supporting green supply chains and regional diversification.

Automotive leather output exceeded 500 million square feet in 2024, with projected growth of 6–8% in 2025. India is experiencing rapid expansion, supported by a growing middle class, urbanization, and a strong footwear and automotive sectors. Japan and South Korea contribute technological leadership, while Southeast Asian countries attract investment through competitive labor costs and improved infrastructure, reinforcing Asia Pacific’s position as the global synthetic leather production hub.

Competitive Landscape

The Synthetic Leather Market is moderately fragmented, with global chemical companies, specialized synthetic leather manufacturers, and textile producers competing across diverse technologies, applications, and regions. Leading players such as BASF, Toray Industries Inc., Kuraray Co. Ltd., and Dow leverage strong R&D capabilities, chemical engineering expertise, and established customer relationships in automotive, footwear, and furnishing sectors to maintain competitive differentiation. Competition increasingly centers on sustainability performance, customization capabilities, and technical support, alongside strategic initiatives such as capacity expansion, bio-based material development, and vertical integration.

Key Market Developments

- January 2026: San Fang Chemical and NicheTech Advanced Materials announced the signing of a strategic cooperation agreement with BASF. This partnership combines San Fang and NicheTech’s expertise in material processing and application knowledge within the footwear supply chain with BASF's leading-edge innovation in material science, accelerating the transition to a more sustainable and circular economy in the sporting footwear & garment industry

- April 2025: BASF SE highlighted innovations such as Haptex, a synthetic leather solution that significantly reduces environmental impact and improves sustainability at PU TECH 2025. Haptex offers 52% lower greenhouse gas emissions, over 20% energy savings, and 30% less water usage compared to traditional solvent-based polyurethane leather production, achieved by eliminating the wet line process.

- June 2024: Germany's DITF and FILK developed a sustainable synthetic leather using bio-based polybutylene succinate (PBS) for both the fiber substrate and coating. This uniform material composition facilitates efficient recycling, addressing challenges associated with traditional synthetic leathers that combine different, non-biodegradable materials.

Top Companies in Synthetic Leather Market

BASF (Ludwigshafen, Germany) operates as a global chemical industry leader with comprehensive polyurethane systems expertise supporting synthetic leather manufacturing through innovative formulations, including the Haptex technology platform, achieving 100 % recyclability and substantial environmental performance improvements. The company's Performance Materials division serves automotive, footwear, furnishing, and fashion industries with customized polyurethane solutions addressing sustainability requirements, regulatory compliance, and performance specifications while maintaining cost competitiveness essential for mass market applications.

Toray Industries Inc. (Tokyo, Japan) leverages advanced materials science and fiber technology expertise to produce premium synthetic leather offerings serving automotive, fashion, and industrial applications requiring superior performance characteristics. The company responds to market customization trends through wide-ranging options encompassing pattern, design, luster, texture, and prints supporting brand differentiation strategies, while maintaining manufacturing quality consistency and supply reliability valued by multinational customers operating global supply chains.

Kuraray Co. Ltd. (Tokyo, Japan) specializes in microfiber-based synthetic leather technologies exemplified by the Clarino and Tirrenina product families, offering environmental advantages through water-borne manufacturing processes, reducing resource consumption while delivering design flexibility across numerous shades, thicknesses, and surface treatments. The company's positioning emphasizes sustainability credentials, technical performance, and application versatility, appealing to European and global customers prioritizing environmental responsibility alongside material functionality.

Companies Covered in Synthetic Leather Market

- TORAY INDUSTRIES, INC.

- Kuraray Co. Ltd.

- San Fang Chemical Industry Co., Ltd.

- BASF

- NAN YA PLASTICS CORPORATION

- Mayur Uniquoters Limited

- H.R. Polycoats Pvt. Ltd.

- Dow

- Teijin Ltd.

- Zhejiang Hexin New Material Co., Ltd.

- Yantai Wanhua Huayi Polyurethane Products Co., Ltd.

- Alfatex

- FILWEL Co., Ltd.

- Kolon Industries, Inc.

Frequently Asked Questions

The global Synthetic Leather Market is valued at US$ 67.4 Bn in 2026 and projected to reach US$ 119.4 Bn by 2033, growing at a CAGR of 8.5 % during the forecast period.

The market is primarily driven by the automotive industry, with accelerating electric vehicle adoption requiring sustainable interior materials, coupled with rising consumer preference for cruelty-free alternatives as vegan fashion gains momentum.

Polyurethane (PU) synthetic leather dominates with approximately 62 % market share, driven by superior performance characteristics including softness, breathability, durability, and aesthetic appeal that closely replicates genuine leather.

Asia Pacific leads the market with over 44.6 % share, driven by massive manufacturing capacity in China, producing 1.69 million tons in the first three quarters of 2023, automotive leather production exceeding 500 million square feet in 2024, India's expanding industries, and South Korea's technological capabilities.

Transformative opportunities emerge from bio-based synthetic leather innovations utilizing pineapple leaves, mushroom mycelium, and agricultural waste, achieving faster biodegradation than petroleum alternatives, with Kuraray's Tirrenina demonstrating 70 % water usage reduction and 35 % carbon dioxide emission decrease, while BASF's Haptex 4.0 offers 100 % recyclability, supporting circular economy principles and premium positioning as sustainable alternatives.