- Specialty & Fine Chemicals

- Synthetic Magnesium Silicate Market

Synthetic Magnesium Silicate Market Size, Share, and Growth Forecast, 2026 - 2033

Synthetic Magnesium Silicate by Product Type (Powder, Granule, Dispersion), Grade (Pharmaceutical Grade, Food Grade, Industrial Grade), End-user (Cosmetics, Medicines, Industrial Products), Application (Personal Care, Others), and Regional Analysis 2026–2033

Synthetic Magnesium Silicate Market Size and Trends Analysis

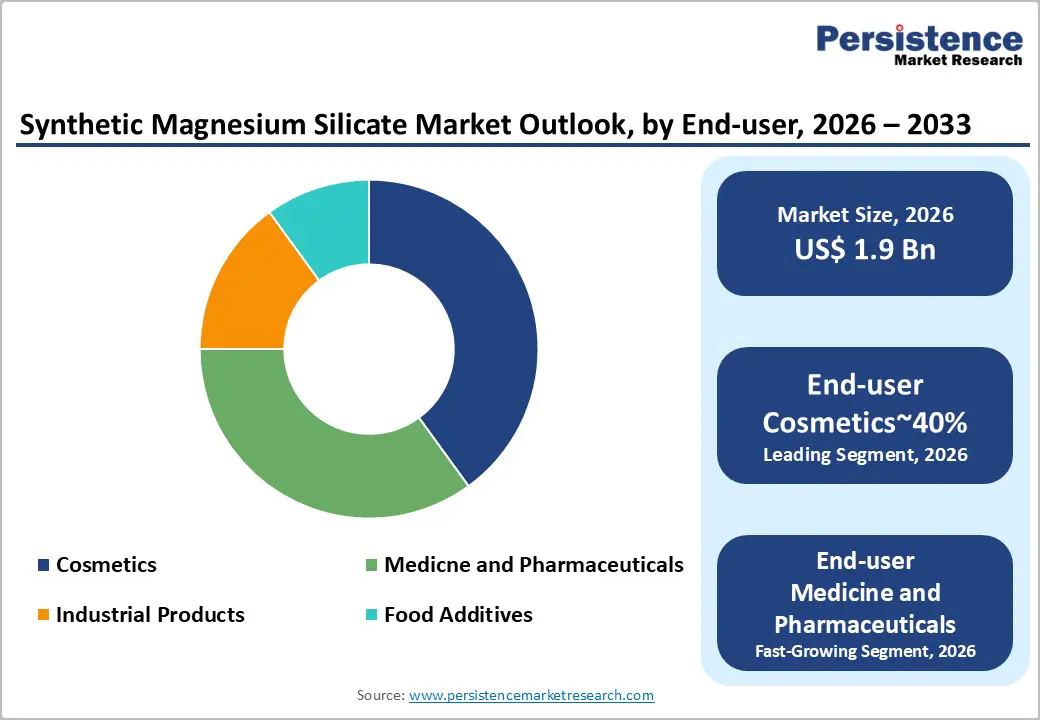

The global synthetic magnesium silicate market size is likely to be valued at US$1.9 billion in 2026 and is expected to reach US$3.1 billion by 2033, growing at a CAGR of 6.7% during the forecast period between 2026 and 2033, driven by increasing demand from the pharmaceuticals and food additives sectors, where its anti-caking and clarifying properties are highly valued. The rising need for high-efficiency adsorbents in renewable fuel refining and premium skincare formulations is providing significant momentum for manufacturers in the synthetic magnesium silicate market.

Key Industry Highlights:

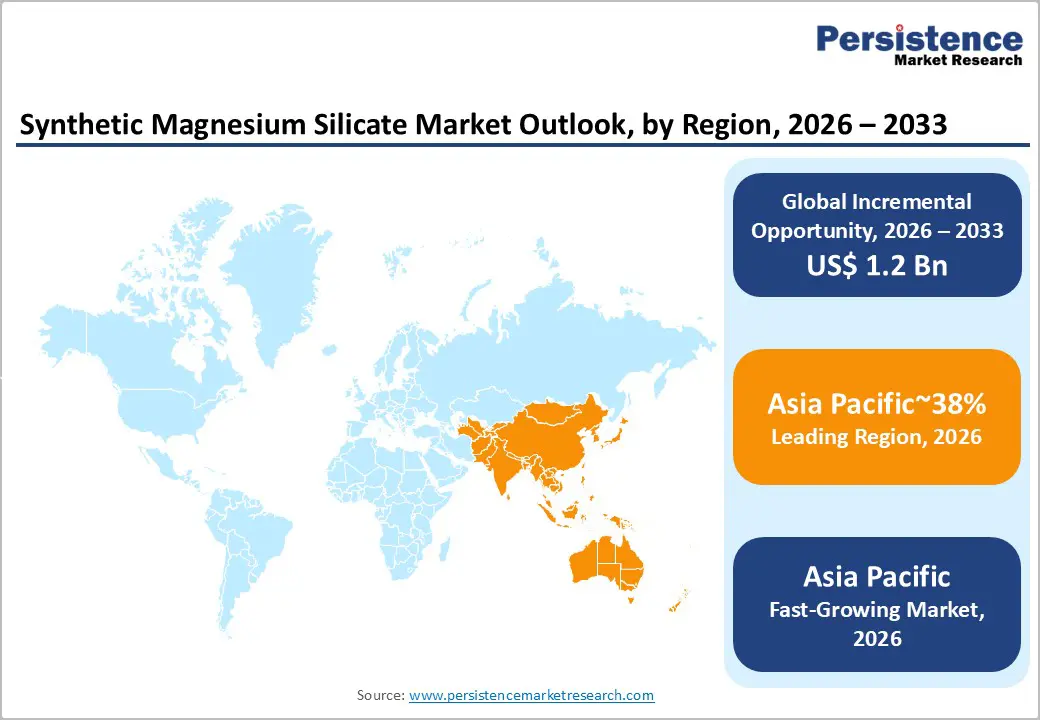

- Leading Region: Asia Pacific is projected to continue being both the largest and the fastest-growing regional market for synthetic magnesium silicate, capturing around 38% of the global market share, driven by the region's extensive pharmaceutical, food processing, and industrial manufacturing sectors.

- Leading Product Type: Powdered synthetic magnesium silicate is anticipated to dominate, accounting for approximately 60% of total demand due to superior adsorption, blending efficiency, and widespread applicability across high-specification end-use industries.

- Leading End-user: The cosmetics segment is expected to remain the leading end-user segment, accounting for approximately 40% of market value, driven by clean-label mandates, talc replacement, and high-purity functional requirements in premium formulations.

- Key Industry Developments: In November 2025, Merck reports Resilient Organic growth fueled by process solutions and pharma manufacturing. Merck’s financial results confirm a 5.2% organic growth rate in its life science sector, driven by strong demand for high-purity chemicals used in drug processing and semiconductor solutions.

| Key Insights | Details |

|---|---|

| Synthetic Magnesium Silicate Market Size (2026E) | US$1.9 Bn |

| Market Value Forecast (2033F) | US$3.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6.7% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Adoption in the "Talc-Free" Cosmetics and Personal Care Movement

The cosmetics and personal care industry is driving market growth through accelerated substitution of natural talc with synthetic magnesium silicate amid heightened contamination risk awareness. Regulatory scrutiny, litigation exposure, and stricter ingredient safety thresholds are compelling formulators to adopt materials with controlled purity and predictable performance. Synthetic magnesium silicate addresses these requirements by delivering consistent particle structure, high oil absorption, and impurity-free composition, directly supporting clean-label and talc-free product positioning across premium and mass-market formulations.

Consumer-led demand for transparency and mineral purity is reinforcing this transition, particularly within developed personal care markets. Brands are responding by embedding synthetic silicates into long-term sourcing strategies to ensure compliance resilience and formulation stability. This structural shift is expanding addressable demand, as synthetic variants enable manufacturers to maintain sensory quality while mitigating regulatory and reputational risk. As talc-free positioning becomes standardized rather than differentiated, synthetic magnesium silicate is emerging as a core growth catalyst within the personal care value chain.

Raw Material Price Volatility

Volatility in magnesium oxide pricing is acting as a structural restraint on market expansion by directly compressing producer margins and disrupting cost predictability. Input cost escalation is intensifying due to constrained mining output, regulatory limitations, and export concentration across key Asian supply hubs. Producers reliant on industrial-grade volumes face heightened exposure, as limited pricing pass-through capacity restricts their ability to offset raw material inflation while maintaining competitive positioning across downstream applications.

Supply-side instability is also raising operational risk by complicating procurement planning and inventory management. Margin pressure is forcing manufacturers to reassess capacity utilization, delay scale-up decisions, and prioritize higher-value grades over volume-driven segments. Without upstream diversification or feedstock substitution, sustained cost volatility threatens to slow industrial-grade adoption and weaken growth momentum, particularly in price-sensitive end-use markets where material economics remain a primary purchasing determinant.

Technological Convergence with Nanotechnology for Drug Delivery

Technological convergence between synthetic magnesium silicates and nanotechnology is opening a high-value growth pathway within advanced drug delivery systems. Nano-structured silicates are gaining traction for their ability to enhance dissolution rates, improve bioavailability, and enable controlled release for poorly soluble BCS Class II and IV drugs. This capability aligns with pharmaceutical pipelines increasingly constrained by solubility limitations, positioning modified silicates as functional excipients rather than inert additives. By leveraging surface engineering and ion-doping techniques, manufacturers can transition from volume-driven supply models toward innovation-led partnerships with biotech and specialty pharma developers.

In January 2025, researchers successfully synthesized magnesium-ion-doped silica nanosheets for pH-Responsive drug delivery. This breakthrough validates commercial feasibility by demonstrating improved degradability and bioavailability in polyphenol-based compounds, including curcumin. Such advancements reinforce premium pricing potential and accelerate value-chain migration toward specialty pharmaceutical applications, particularly in regulation-intensive markets with strong translational research ecosystems.

Category–wise Analysis

Product Type Insights

The powder segment is anticipated to lead the synthetic magnesium silicate market, accounting for approximately 60% of overall demand. This leadership is most likely to persist due to the powder form’s high surface-area-to-volume ratio, which supports superior adsorption, blending efficiency, and functional versatility across pharmaceuticals, food processing, cosmetics, and oil purification. In pharmaceutical formulations, powder-grade synthetic magnesium silicate is widely relied upon as a glidant to improve tablet flow and weight uniformity, while in food and edible oil applications, it remains the preferred anti-caking and filtration aid.

Manufacturers are increasingly adopting AI-assisted synthesis controls to maintain consistent particle size and purity, reinforcing suitability for high-specification uses. Ongoing shifts away from natural talc, driven by purity assurance and performance consistency, are expected to further anchor the powder segment’s dominant position across mature and emerging end-use industries.

The granule segment is expected to emerge as the fastest-growing product type as the market transitions toward performance-engineered, automation-compatible materials. Demand is being propelled by the need for dust-free handling, predictable flow behavior, and improved occupational safety in high-throughput pharmaceutical, food, and industrial processing environments.

Granules are increasingly favored in continuous manufacturing systems, advanced oil purification setups, and solid cosmetic formats where controlled adsorption and volumetric efficiency are critical. Rising adoption of bio-derived silica sources, hybrid silicate formulations, and smart packaging inserts is further supporting uptake. As production lines prioritize efficiency, safety, and material stability, granulated synthetic magnesium silicate is likely to gain accelerated traction despite the continued dominance of powder forms.

End-user Insights

The cosmetics segment is anticipated to hold a leading 40% share of the end-user landscape, driven by value rather than volume. High-purity cosmetic grades of synthetic magnesium silicate (SMS) are expected to remain the industry standard, replacing variable natural minerals in premium formulations. Recent industrial updates include the completion of the "Talc-to-Synthetic" transition by major global brands, the launch of ultra-micronized aerosolized powders for sprayable sunscreens and setting products, and the introduction of smart, selective adsorbents that remove oxidized sebum while preserving natural skin moisture.

The market is driven by heightened consumer safety awareness following asbestos litigation. The global trends toward translucent "Glass Skin" aesthetics and waterless formulation mandates, where SMS (Spent Mushroom Substrate) acts as a stabilizing bulking agent. Leading brands in this segment are Spectrum Chemical, Kyowa Chemical, Evonik Industries, and Neelkanth Finechem, emphasizing consistent purity, multifunctionality, and regulatory compliance for premium cosmetic applications.

The medicine and pharmaceutical segment is expected to be the fastest-growing application area for SMS, supported by a systemic shift toward lab-controlled minerals in drug manufacturing. This growth is likely influenced by the "Talc-to-Synthetic" mandate, the rise of continuous manufacturing lines requiring uniform particle distribution, and expansion in generic drug production across India and China. Industrial updates include AI-monitored precipitation for identical porosity, co-processed excipients for improved tablet flow, and SMS stabilization of biologics in dry-powder formulations.

Drivers include growth in gastrointestinal therapeutics, clean-label medicine trends, and integration into nutraceuticals. Regulatory updates such as EMA Annex 1 revisions, USP/NF heavy metal limits, and FDA Inactive Ingredient Database listings are expected to further boost SMS adoption. Leading suppliers include Spectrum Chemical, U.S. Silica (Pharma Division), Biosynth, Lumen Pharmachem, and PQ Corporation, providing high-purity, application-specific SMS to meet the stringent quality standards of the pharmaceutical industry.

Regional Insights

Asia Pacific Synthetic Magnesium Silicate Market Trends

Asia Pacific is expected represent both the leading and fastest-growing region, accounting for around 38% of global market share, positioning the region as the fastest-growing market over the forecast period. Growth is anchored in China and Japan, supported by large-scale pharmaceutical, food processing, and industrial manufacturing ecosystems, while India and ASEAN economies contribute incremental expansion through capacity additions and export-oriented production.

Cost advantages relative to Western markets continue to attract global sourcing activity, reinforcing the region’s role as a manufacturing hub for industrial-grade materials, alongside rising domestic demand. The regulatory environment is transitioning from relatively permissive frameworks toward tighter GMP-aligned standards, reshaping competitive dynamics and elevating quality benchmarks. Government-led industrial policies and targeted foreign direct investment are strengthening infrastructure depth and production sophistication, particularly in pharmaceuticals and specialty chemicals.

While the competitive landscape remains fragmented, scale-driven players and regional leaders are consolidating share through capacity expansion and compliance upgrading. These structural factors collectively sustain Asia Pacific’s growth momentum while gradually improving margin quality and regulatory resilience.

North America Synthetic Magnesium Silicate Market Trends

Market growth in North America is supported by its mature regulatory environment, advanced pharmaceutical manufacturing base, and high compliance intensity. The U.S. anchors regional performance through strong demand from regulated drug production, cosmetics, and oil purification applications, where purity assurance and traceability are decisive. Regulatory oversight from federal agencies continues to elevate entry barriers, reinforcing demand for synthetic and specialty-grade materials while sustaining pricing discipline across the value chain.

Growth prospects are further reinforced by a dense innovation ecosystem and well-developed industrial infrastructure. Sustained investment in research funding, formulation science, and specialty chemical automation is strengthening regional capabilities, particularly in sustainability-aligned and bio-based grades. Consolidation among established suppliers is improving scale efficiencies and compliance readiness. These structural advantages position North America as a high-value, innovation-led market, characterized by moderate growth but strong margin resilience and long-term demand stability.

Europe Synthetic Magnesium Silicate Market Trends

Europe is expected to witness significant growth, positioning the region as a high-value, regulation-led market characterized by policy harmonization and sustainability alignment. Demand is anchored by a well-established pharmaceutical manufacturing base and a premium cosmetics sector, where purity assurance and regulatory conformity drive material selection. Germany leads regional consumption, while the U.K. and France contribute incremental growth through structurally aligned compliance frameworks. Harmonized regulatory oversight under REACH and food safety authorities continues to reduce cross-border compliance friction, reinforcing intra-regional supply efficiency.

Growth dynamics are increasingly shaped by environmental policy integration and industrial upgrading. The European Green Deal is accelerating the adoption of high-efficiency and recyclable material grades, particularly within pharmaceutical and food applications. Regulatory stringency acts as a barrier to low-quality imports, favoring technologically advanced regional producers. Capacity expansions and capital deployment are gradually shifting toward Eastern Europe, reflecting a strategic balance between cost optimization, regulatory continuity, and access to skilled manufacturing infrastructure.

Competitive Analysis

The global synthetic magnesium silicate market is moderately consolidated, with the top five players holding a significant share, led by Imerys and Tokuyama, which exert influence through scale, purity leadership, and supply reliability. PQ Corporation, Merck KGaA, and Tomita Pharmaceutical strengthen competition in high-value pharmaceutical and food-grade segments by emphasizing certified quality and compliance with international pharmacopeia standards. The industrial-grade tier remains fragmented, particularly across China and India, where regional suppliers compete primarily on pricing and proximity to end users.

Competitive strategies center on capacity expansion, technology partnerships, and product innovation, as seen in pharma-grade dispersion launches and nano-technology collaborations. Regionally, consolidation is more pronounced in North America and Europe, while Asia Pacific remains price-competitive but strategically important for capacity growth. Forward dynamics point toward gradual consolidation, driven by demand for high-purity grades, tighter regulations, and closer alignment with end-user supply chains.

Key Industry Developments:

- In October 2024, Huber Advanced Materials implemented global price increases across all product portfolios. The company introduced a price adjustment ranging from 5% to 15% to offset rising costs in feedstocks, packaging, and ocean freight, reflecting inflationary pressures on synthetic mineral production.

- In September 2024, Tomita Pharmaceutical showcased advanced FLORITE silicate excipients at CPHI Milan. The company highlighted the unique porous structure of FLORITE (Calcium Silicate), positioning it as a benchmark for high-performance liquid-to-solid conversion in pharmaceutical tableting.

- In January 2024, PQ Corporation acquired the specialty silicate business of vanBaerle Group. By acquiring the Swiss-based manufacturer, PQ strengthened its portfolio of tailored silicate solutions for industrial welding and construction across Europe and Asia.

Companies Covered in Synthetic Magnesium Silicate Market

- Imerys

- Tokuyama Corp.

- PQ Corporation

- BASF SE

- Huber Engineered Materials

- Tomoe Engineering

- Taurus Chemicals

- Grace & Co

- Evonik Industries

- Clariant

- Cabot Corp.

- Ube Industries

- Kyowa Chemical Industry Co., Ltd.

- Huber Engineered Materials

- SPI Pharma

Frequently Asked Questions

The global synthetic magnesium silicate market is valued at US$1.9 billion in 2026 and is projected to reach US$3.1 billion by 2033.

Demand is increasing due to the global shift toward talc-free formulations, rising pharmaceutical purity requirements, and growing use as an adsorbent in food additives, cosmetics, and renewable fuel refining.

The synthetic magnesium silicate market is expected to grow at a CAGR of 6.7% between 2026 and 2033, supported by pharmaceutical-grade adoption and expanding personal care applications.

Strong opportunities are emerging in biodiesel refining, nanotech-enabled drug delivery systems, and high-purity cosmetic formulations, where performance consistency and regulatory compliance are critical.

Key players include Imerys, Tokuyama Corporation, PQ Corporation, Merck KGaA, BASF SE, Huber Engineered Materials, Evonik Industries, Grace & Co., Clariant, Cabot Corporation, and SPI Pharma.