- Specialty & Fine Chemicals

- Geosynthetics Market

Geosynthetics Market Size, Trends, Share, and Growth Forecast 2026 - 2033

Geosynthetics Market by Product Type (Geotextiles, Geomembranes, Geofoam, Geogrids, and Geonets), Application (Waste Management, Water Management, Transportation Infrastructure, Construction, and Others), and Regional Analysis for 2026 - 2033

Geosynthetics Market Size and Share Analysis

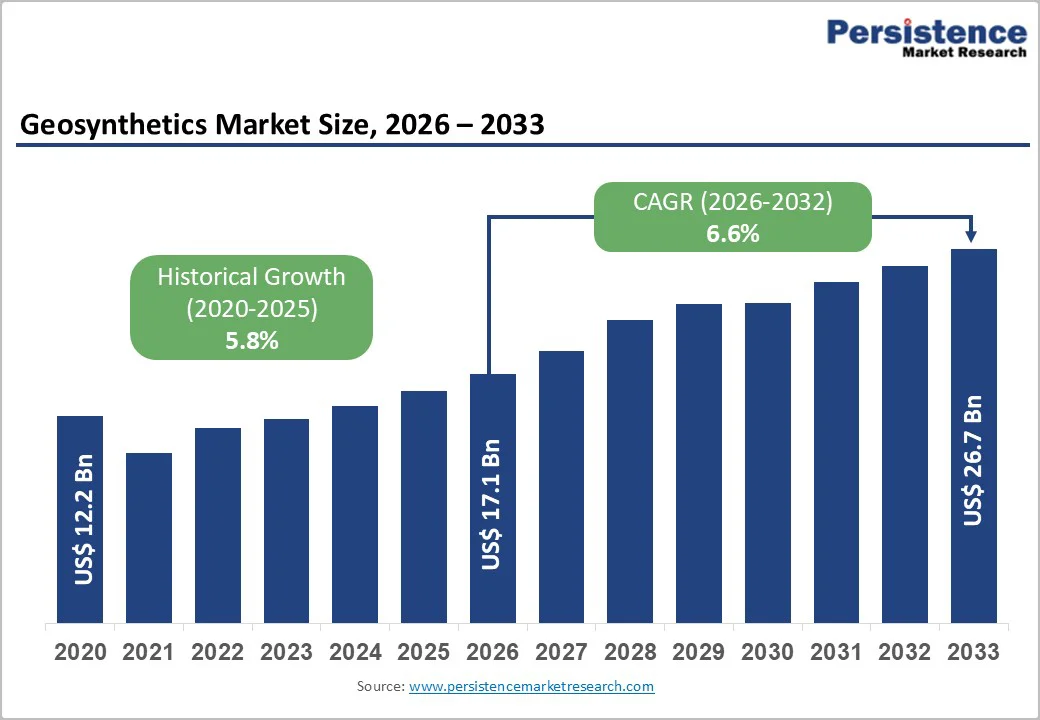

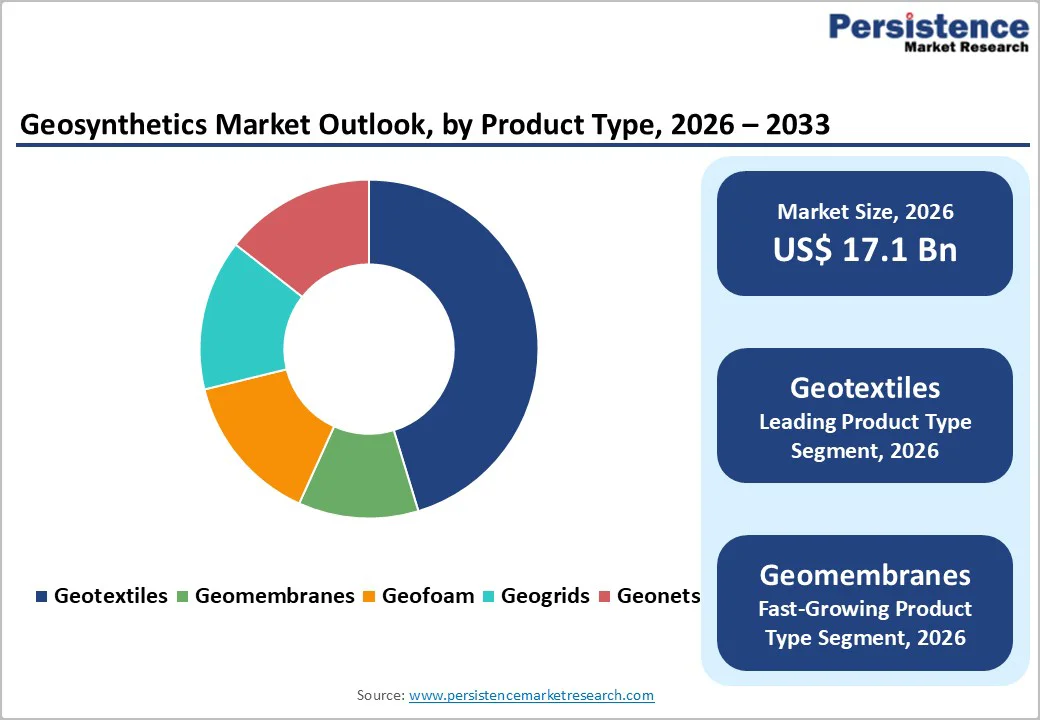

The global geosynthetics market size is valued at US$ 17.1 billion in 2026 and is projected to reach US$ 26.7 billion by 2033, growing at a CAGR of 6.6% between 2026 and 2033.

The market is experiencing sustained growth driven by the escalating infrastructure investments and urbanization across developing economies, which are generating unprecedented demand for soil reinforcement, stabilization, and erosion control solutions, and increasing environmental regulations. Sustainability consciousness is compelling governments and industries to adopt geosynthetic alternatives that reduce carbon emissions.

Key Market Highlights

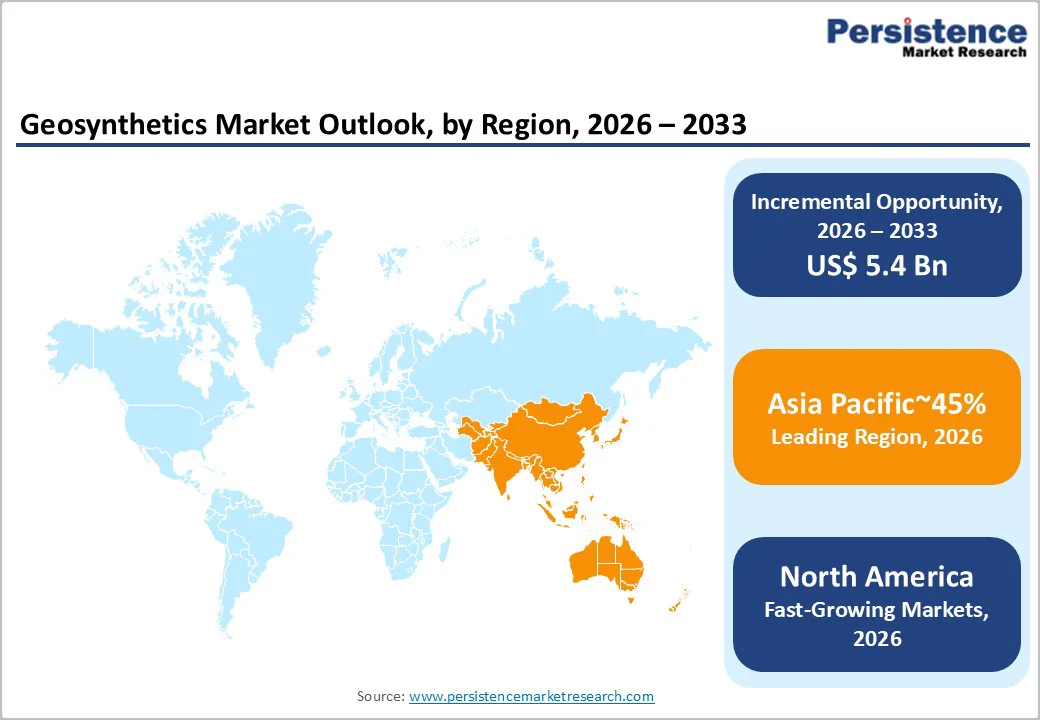

- Leading Region: Asia Pacific commands the largest established geosynthetics market, contributing approximately 45% global market value through mature rapid urbanization, stringent regulatory requirements, and advanced engineering specifications.

- Fastest-Growing Region: North America is the fastest-growing regional market, expanding at approximately 8.2% CAGR driven by extensive infrastructure development, government sustainability initiatives, and massive investments in water management and waste containment.

- Dominant Product Type: Geotextiles dominate the product type segment with approximately 49.1% market share, driven by superior performance characteristics, cost-effectiveness, and widespread deployment.

- Fastest-Growing Application: Waste management is the fastest-growing application segment, with approximately 34.4% market share, driven by stringent environmental regulations mandating geosynthetic-based containment systems and a growing global emphasis on sustainable waste disposal practices and groundwater protection.

- Key Market Opportunity: Advanced geocomposite solutions incorporating integrated drainage systems, PFAS-remediation capabilities, and smart sensor technologies represent the highest-potential market opportunity.

| Key Insights | Details |

|---|---|

|

Global Geosynthetics Market Size (2026E) |

US 17.1 Bn |

|

Market Value Forecast (2033F) |

US$ 26.7 Bn |

|

Projected Growth CAGR(2026-2033) |

6.6% |

|

Historical Market Growth (2020-2025) |

5.8% |

Market Dynamics

Drivers - Rapid Infrastructure Expansion and Government Investment in Developing Economies

Rapid infrastructure development across emerging markets is a major driver fueling the growth of the global geosynthetics market. Developing economies in Asia, Africa, Latin America, and the Middle East are undertaking large-scale construction projects, including highways, high-speed rail networks, metro systems, airports, industrial corridors, smart cities, and energy projects, to support urbanization, logistics efficiency, and economic modernization. Governments are significantly increasing capital expenditure on public infrastructure, often endorsed by multilateral funding and public-private partnerships, which is creating sustained demand for advanced geotechnical materials.

Geosynthetics, such as geotextiles, geomembranes, geogrids, and geocells, are increasingly integrated into these projects due to their superior performance in soil stabilization, erosion control, drainage, reinforcement, and environmental protection. They enable faster construction, reduce the need for natural aggregates, lower lifecycle costs, and enhance infrastructure durability, which aligns with cost-conscious development strategies. Additionally, regulatory shifts in emerging economies are encouraging the adoption of engineered materials to ensure long-term resilience against climate-related risks such as flooding, landslides, and soil erosion. As a result, the growing pipeline of infrastructure investments in developing regions remains one of the most influential demand-side catalysts for the global geosynthetics market.

Stringent Environmental Regulations and Sustainability-Driven Market Adoption

Environmental consciousness and regulatory mandates are reshaping the utilization of geosynthetics across the waste management and water conservation sectors globally. The European Union Landfill Directive and United States EPA Subtitle D Regulations require geosynthetic-based containment systems in landfill construction, mandating minimum 100-year service lives for geomembrane products in certain German jurisdictions. HDPE geomembranes are experiencing strong demand due to superior chemical resistance and durability characteristics, enabling long-term waste containment.

Growing awareness of PFAS contamination in water resources is driving demand for advanced geocomposite solutions that incorporate active media and ion-exchange resins for contaminated-site remediation. Geosynthetics contribute substantially to carbon-emission reduction objectives, with studies demonstrating a 75% reduction in carbon emissions in reinforced-soil retaining-wall structures compared to traditional concrete alternatives. Sustainability policies and corporate environmental responsibility initiatives are compelling organizations to prioritize geosynthetic adoption, positioning the material category as essential for achieving climate targets and environmental protection objectives.

Restraints - Installation Expertise Requirements and Technical Specification Complexity

Geosynthetic product installation requires specialized expertise and technical knowledge, creating barriers to market adoption in regions with limited engineering capacity. Complex installation procedures, stringent quality control requirements, and performance verification demands necessitate a trained workforce, limiting market expansion in developing regions. Build America, Buy America (BABA) regulations established through the Infrastructure Investment and Jobs Act requirements create compliance challenges for manufacturers, with noncompliance thresholds limited to USD 1 million or 5% of total costs.

These regulatory requirements increase administrative burden and project costs, potentially constraining market growth. Specification complexity and variations in design standards across different geographic regions and application types require manufacturers to maintain diverse product portfolios and technical support capabilities, increasing operational complexity and cost structures.

Raw Material Price Volatility and Supply Chain Disruptions

Geosynthetic manufacturers face significant challenges from fluctuating petrochemical feedstock prices and supply chain disruptions affecting production economics. Polypropylene, widely used in geotextile and geogrid production, is subject to price volatility driven by crude oil market dynamics and geopolitical factors. Supply chain interruptions, transportation cost pressures, and raw material availability constraints directly impact manufacturing profitability and product pricing, particularly affecting smaller manufacturers lacking economies of scale.

The build-back-better supply chains required following pandemic disruptions have increased logistics costs and extended project timelines, creating margin pressures throughout the geosynthetic value chain. Manufacturers struggling with cost inflation are constrained in investment capacity for research and development and facility expansion, limiting innovation potential and competitive positioning. Currency fluctuations affecting international trade and global supply chain coordination create additional uncertainty, impacting pricing strategies and market competitiveness.

Opportunity - Renewable Energy Infrastructure and Climate Resilience Applications

Geosynthetics are emerging as critical enabling materials for renewable energy infrastructure development, with solar and wind energy projects requiring geomembranes and geogrids for site preparation and foundation stabilization. China's offshore wind energy expansion, India's renewable energy targets, and global solar farm development initiatives are creating substantial new geosynthetic demand across foundation engineering, site stabilization, and erosion control applications. The global shift toward renewable energy is expected to generate hundreds of gigawatts of new capacity through 2032, with each megawatt requiring geosynthetic support systems. Climate change adaptation strategies increasingly emphasize coastal protection, flood mitigation, and slope stabilization, where geosynthetics provide cost-effective and proven solutions.

Emerging applications include green infrastructure projects incorporating water-absorbing geocomposites for sustainable stormwater management and vegetation support. Smart geosynthetics incorporating embedded sensors and monitoring capabilities represent a growing opportunity segment, enabling real-time structural health monitoring and safety alerts. Infrastructure resilience initiatives responding to extreme weather events create an accelerating demand for high-performance geosynthetic materials capable of withstanding challenging environmental conditions while maintaining long-term performance.

Advanced Geocomposite Solutions and Specialized Applications for Contaminated Sites

Advanced geocomposite materials combining multiple functions are the fastest-growing product segment, with integrated drainage systems that eliminate traditional drainage layers by combining HDPE geomembranes with geotextile overlays, reducing installation time and overall project costs. Specialized geocomposites incorporating PFAS-remediation capabilities are experiencing accelerating demand as global awareness regarding per- and polyfluoroalkyl substances contamination increases. HUESKER's Tektoseal Active PFAS product, which combines ion-exchange resin and activated carbon layers, exemplifies innovative solutions addressing emerging contamination challenges. Geocomposite canal lining products, sediment capping systems, and oil-spill absorption materials are experiencing growth driven by environmental remediation requirements and industrial application demands. Recycled material-based geosynthetics, including products incorporating recycled polymers and biodegradable materials, are creating growth opportunities aligned with circular economy objectives. Specialized products for heavy-load mining applications, railroad bed stabilization, and advanced bridge systems represent niche opportunities where technical performance requirements drive premium pricing and higher margin potential. Nanotechnology integration, artificial intelligence applications, and smart sensor incorporation into geosynthetic products create emerging innovation frontiers with significant long-term market potential.

Category-wise Analysis

Product Type Insights

Geotextiles dominate the geosynthetics market with approximately 49.1% revenue share in 2026, driven by widespread deployment in separation, filtration, drainage, and erosion control applications across infrastructure and environmental projects. Geotextiles are permeable engineered fabrics manufactured from synthetic fibers, primarily polypropylene and polyester, designed to interact with soil while maintaining filtration and drainage functionality. Superior performance characteristics, including high tensile strength, durability, and cost-effectiveness, position geotextiles as the foundational material category across civil engineering applications.

Geotextile adoption continues expanding in emerging applications, including green infrastructure, water conservation, and sustainable agriculture, supporting steady market growth. Advanced geotextiles incorporating enhanced UV resistance, increased interface friction performance, and specialized filtration capabilities are experiencing accelerated adoption in demanding applications requiring extended service lives and superior performance specifications.

Application Analysis

Waste management holds the largest application segment with approximately 34.4% market share, driven by regulatory mandates requiring geosynthetic-based containment systems in municipal and industrial waste management facilities. Governments worldwide are mandating stringent waste containment practices, compelling landfill operators to implement comprehensive geomembrane liners, leachate collection systems, and gas management infrastructure incorporating geosynthetic components.

Geosynthetic clay liners, combining low permeability with superior chemical resistance, are widely deployed in hazardous waste containment and industrial waste management applications. Geosynthetics reduce the risk of soil and groundwater contamination, providing critical environmental protection while enabling regulatory compliance across jurisdictions. The waste management segment is expected to continue expanding as developed and developing nations prioritize modernizing waste infrastructure and environmental protection.

Regional Insights

North America Geosynthetics Market Trends

North America emerges as the fastest-growing region, with approximately 28% global market share, supported by mature infrastructure networks, extensive regulatory frameworks, and a substantial presence of geosynthetic manufacturers. The United States dominates regional market positioning through strong government infrastructure investment and advanced engineering specifications requiring geosynthetic deployment across transportation and environmental applications.

Government mandates requiring geosynthetic implementation in landfill systems, combined with EPA regulations on waste containment and water protection, drive sustained market growth across environmental applications. North America is expected to expand at a faster CAGR than other developed regions, reflecting infrastructure modernization priorities and regulatory sophistication.

Europe Geosynthetics Market Trends

Europe represents a mature, well-established market characterized by stringent environmental regulations and sustainability-driven product specifications. Germany dominates European geosynthetic markets and is expected to be the fastest-growing country segment, driven by robust construction activity, strict regulatory compliance requirements, and strong environmental consciousness.

The European Union Landfill Directive and harmonized quality standards established through LAGA (the German waste management standards body) create uniform technical requirements across member states, benefiting manufacturers that provide compliant solutions. Geomembranes account for approximately 32.7% of material preferences across Europe, valued for their superior durability and long-term performance, which meet stringent regulatory specifications.

Asia Pacific Geosynthetics Market Trends

Asia Pacific commands approximately 45% of the global geosynthetics market in 2026, making it the largest regional market. This dominance is driven by unprecedented infrastructure development, rapid urbanization, and large-scale government investments in transportation, energy, and environmental engineering projects. Countries such as China, India, Indonesia, and Vietnam are heavily investing in highways, rail networks, airports, metro systems, industrial corridors, and coastal protection works, each of which requires significant use of geotextiles, geomembranes, geogrids, and drainage composites.

The region’s construction sector also benefits from supportive policy frameworks promoting sustainable materials, efficient land management, and climate-resilient infrastructure. Additionally, rising environmental regulations on waste management and water conservation are driving the deployment of geosynthetics in landfill liners, wastewater treatment, and irrigation systems. Local manufacturing expansion, cost-effective production capabilities, and technological advancements further reinforce the Asia Pacific’s leadership position.

Competitive Landscape

The global geosynthetics market exhibits a moderately fragmented competitive structure with SOLMAX holding approximately 8-10% market share following strategic acquisitions of Propex and TenCate Geosynthetics, establishing the company as the world's largest geosynthetics provider. The top five companies, SOLMAX, NAUE GmbH, Berry Global, Koninklijke Ten Cate, and GSE Environmental, collectively control approximately 25-28% of global market value.

Leading companies pursue aggressive expansion strategies through acquisition initiatives, geographic market penetration, product portfolio diversification, and research and development investments targeting sustainable and specialized solutions. Emerging business models include subscription-based material leasing arrangements, direct-to-customer digital platforms, and circular economy initiatives emphasizing product recyclability and material reuse.

Key Market Developments:

- In November 2023, HUESKER Inc. introduced the Tektoseal Active PFAS advanced geocomposite featuring dual-layer geotextile construction with integrated ion exchange resin and activated carbon, specifically engineered to remediate PFAS-contaminated sites while providing customizable treatment for project-specific contaminant concentrations.

- In October 2023, AGRU America unveiled its innovative Integrated Drainage System (IDS), combining structured geomembrane with geotextile overlay, effectively replacing traditional soil and aggregate drainage layers while reducing installation time, material requirements, and project costs through advanced composite engineering.

- In June 2023, SOLMAX completed the acquisition of Propex, one of the largest U.S. geosynthetics manufacturers established in 1910, significantly expanding SOLMAX's global product portfolio, geographic reach, and market leadership position across construction, transportation, mining, and environmental containment sectors.

Companies Covered in Geosynthetics Market

- SOLMAX

- NAUE GmbH

- Berry Global

- Koninklijke Ten Cate N.V.

- GSE Environmental

- Officine Maccaferri S.p.A.

- Low & Bonar

- Propex Operating Company, LLC

- Fibertex Nonwovens A/S

- TENAX Group

- AGRU America, Inc.

- HUESKER Group

- TYPAR Geosynthetics

- Global Synthetics

- CTM Geosynthetics

Frequently Asked Questions

The global geosynthetics market was valued at US$ 17.1 Bn in 2026 and is projected to reach US$ 26.7 Bn by 2032, growing at a CAGR of 6.6% during the forecast period.

Infrastructure development across emerging economies, environmental regulations mandating geosynthetic deployment in waste management, and government initiatives promote geosynthetic utilization as sustainable alternatives represent primary growth drivers.

Geotextiles dominate with approximately 49.1% market share, valued for separation, filtration, drainage, and erosion control capabilities across infrastructure and environmental applications.

Asia Pacific maintains the largest established geosynthetics market with approximately 45% global share, supported by mature infrastructure networks, stringent regulatory requirements, and government funding programs.

Advanced geocomposite solutions incorporating integrated drainage systems, PFAS-remediation capabilities, and emerging smart sensor technologies represent the highest-growth opportunities.