- Bulk Chemicals

- Synthetic Rope Market

Synthetic Rope Market Size, Share, and Growth Forecast 2026 - 2033

Synthetic Rope Market by Material Type (Polyethylene, Polypropylene, Polyester, Specialty Fiber, Polyamide), by Rope Design (Braided, Twisted, Plaited), by Application (Marine & Fishing, Oil & Gas, Construction, Cranes, Others), by Regional Analysis, 2026 - 2033

Synthetic Rope Market Size and Trend Analysis

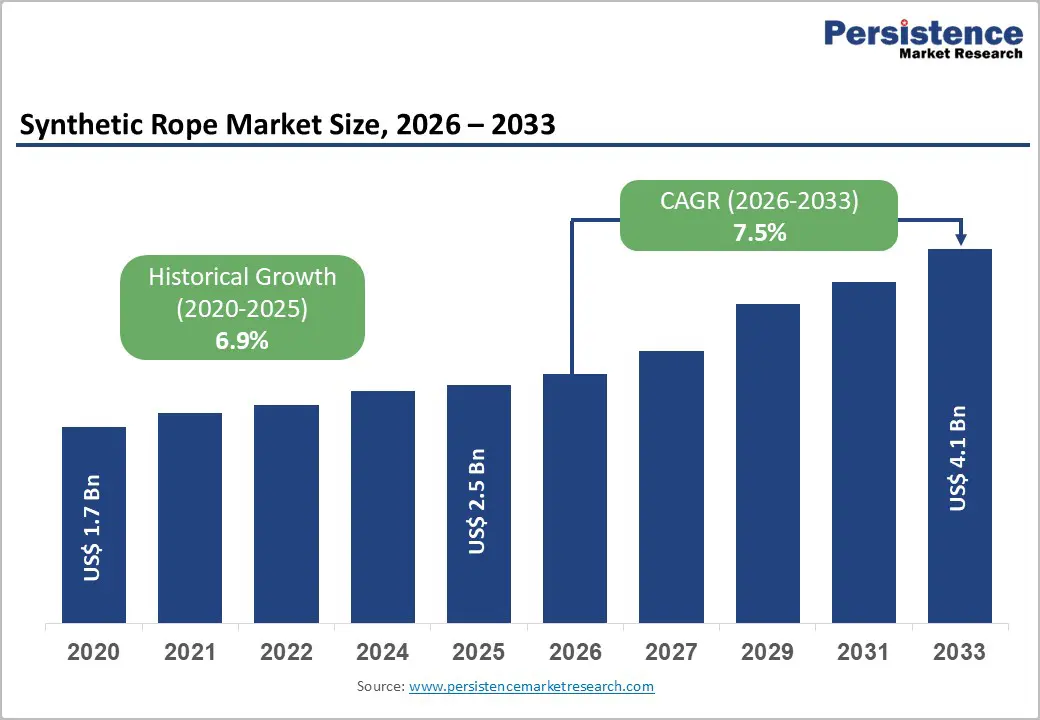

The global synthetic rope market size is expected to be valued at US$ 2.5 billion in 2026 and projected to reach US$ 4.1 billion by 2033, growing at a CAGR of 7.5% between 2026 and 2033.

The market is experiencing robust growth driven by rising demand for lightweight, high-strength materials across the marine, oil and gas, and infrastructure sectors. Synthetic ropes demonstrate superior strength-to-weight ratios compared to traditional steel wire ropes, providing approximately 85% weight reduction while maintaining equivalent tensile strength. The global maritime fleet has expanded at approximately 2.5% annually, creating sustained demand for durable mooring and rigging solutions capable of withstanding harsh marine environments.

Key Industry Highlights:

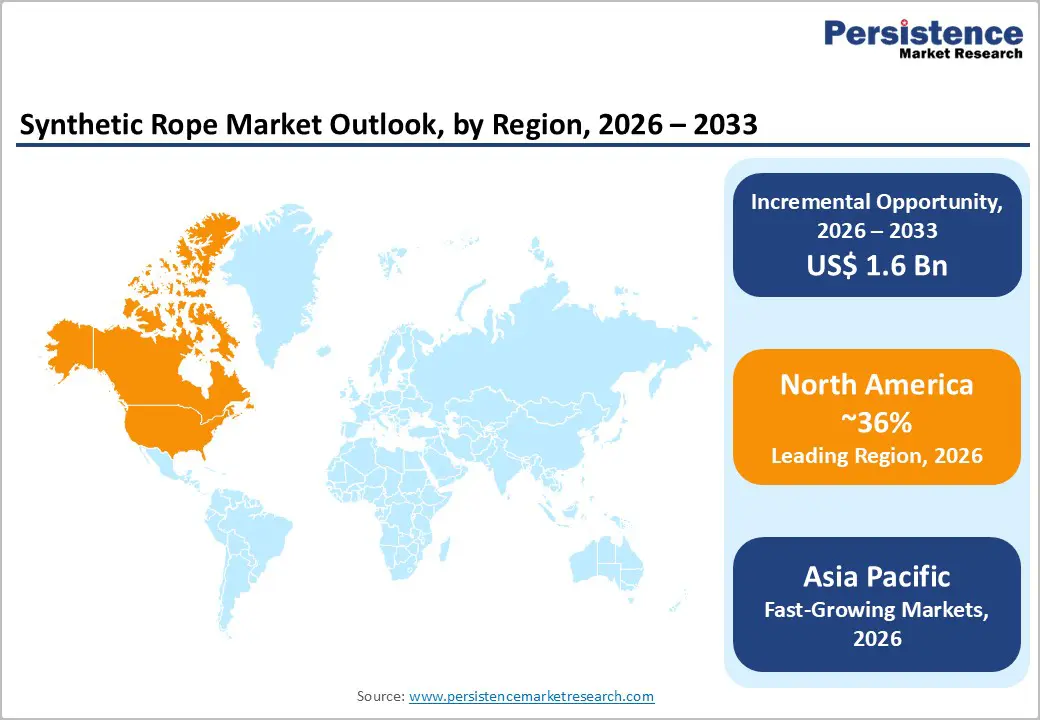

- Leading Region: North America dominates the global synthetic rope market, commanding approximately 36% of market value in 2025, supported by mature offshore oil and gas operations, advanced manufacturing capabilities, and established professional end-user networks.

- Emerging Region: Asia Pacific is the fastest-growing regional market, expanding at approximately 9.5% CAGR through 2032, driven by accelerated infrastructure development, port modernization initiatives, and emerging manufacturing hubs.

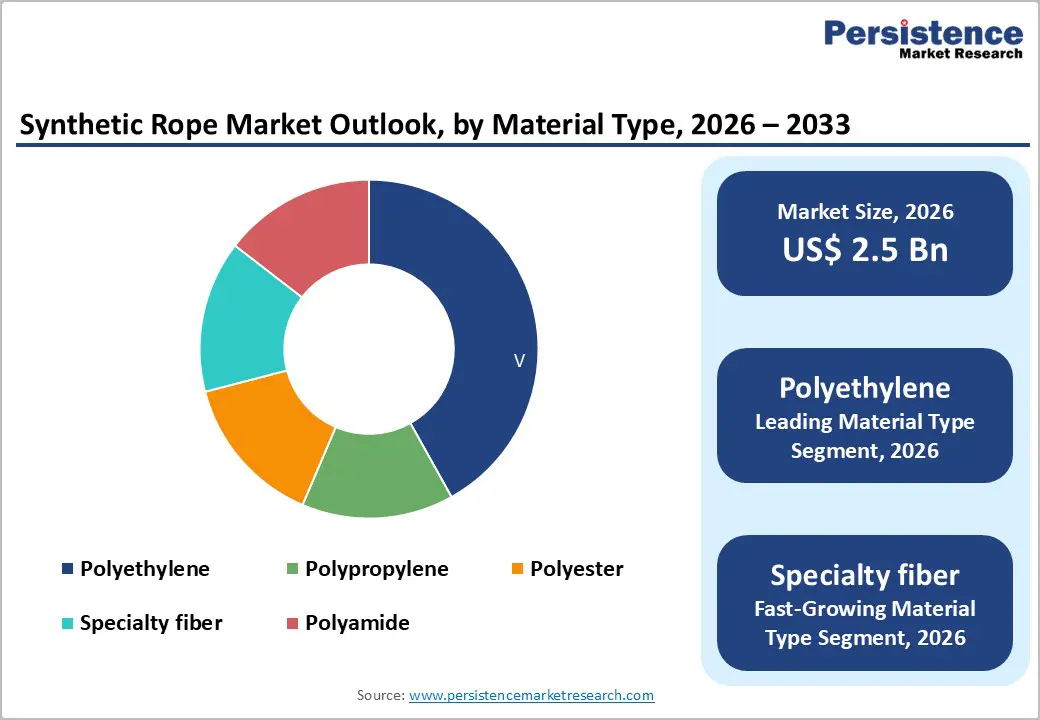

- Dominant Segment: Polypropylene is the dominant material type, commanding approximately 42% of market share in 2025, with its dominance driven by cost-effectiveness, adequate performance characteristics, and a global manufacturing infrastructure.

- Fastest Growing Segment: Braided rope design constitutes the fastest-growing construction segment, expanding at approximately 9.2% CAGR through 2033, reflecting superior performance characteristics and marine industry specification requirements.

- Key Opportunity: Offshore renewable energy infrastructure expansion and emerging market infrastructure development represent principal market opportunities, with offshore wind capacity projected to expand from 35 GW in 2020 to 234 GW by 2030, generating extraordinary specialized rope demand.

| Key Insights | Details |

|---|---|

|

Synthetic Rope Market Size (2026E) |

US$ 2.5 billion |

|

Market Value Forecast (2033F) |

US$ 4.1 billion |

|

Projected Growth CAGR(2026-2033) |

7.5% |

|

Historical Market Growth (2020-2025) |

6.9% |

Market Dynamics

Drivers - Superior Performance Characteristics and Enhanced Operational Safety

Synthetic ropes offer exceptional performance advantages over traditional materials, including superior resistance to abrasion, UV radiation, moisture, and chemical degradation that collectively extend operational lifespan and reduce maintenance costs. Clinical performance data confirms that synthetic ropes exhibit approximately 85% weight reduction compared to equivalent steel wire ropes while maintaining identical tensile strength specifications, fundamentally transforming lifting, rigging, and mooring operations across industrial applications.

The International Maritime Organization (IMO) reports that synthetic rope adoption reduces labor requirements during deployment and installation, substantially improving operational efficiency in demanding maritime environments. Enhanced safety characteristics, including non-corrosive properties, improved grip characteristics, and reduced snapback risks during failure scenarios, position synthetic ropes as mandatory specifications in high-risk applications, including offshore drilling, deepwater exploration, and heavy lifting operations.

Commercial shipping operators have documented that substituting synthetic rope reduces equipment downtime by approximately 30%, improves crew safety metrics, and extends equipment lifespan by reducing corrosive degradation. This documented performance superiority is driving accelerated adoption, particularly among insurance-conscious operators and safety-regulated industries.

Offshore Energy Expansion and Renewable Energy Infrastructure Development

The global transition toward renewable energy infrastructure, particularly the expansion of offshore wind farms, is driving extraordinary demand for specialized synthetic ropes capable of operating in extreme marine environments. Global offshore wind capacity is projected to grow from 35 GW in 2020 to 234 GW by 2030, representing a 568% cumulative increase and establishing unprecedented demand for mooring systems, towing equipment, and lifting solutions. Synthetic ropes manufactured from HMPE (High Modulus Polyethylene) and aramid fibers are essential for floating offshore platform anchoring, tensioning systems, and cable-laying operations where traditional steel solutions prove inadequate.

Additionally, the offshore oil and gas sector, valued at US$ 40 billion globally, continues expanding deepwater exploration activities, with synthetic ropes essential for subsea pipeline operations, production platform mooring, and heavy equipment lifting. Technological advancements in rope design, including 12-strand hollow-braid constructions and hybrid fiber combinations, have expanded performance capabilities while maintaining weight reduction advantages. This convergence of renewable energy demand, continued hydrocarbon exploration, and infrastructure development establishes a multi-decade growth trajectory for synthetic rope consumption.

Restraints - Fluctuating Raw Material Prices and Supply Chain Volatility

Synthetic rope production depends fundamentally on petrochemical feedstocks, including polyethylene, polypropylene, polyester, and specialty fibers, exposing manufacturers to substantial commodity price volatility. Historical petroleum price fluctuations ranging from US$ 40-130 per barrel create unpredictable manufacturing cost structures, constraining profit margins and complicating pricing strategies. Supply chain disruptions following geopolitical instability, trade policy changes, and regional conflicts have created extended lead times for raw material procurement, particularly for specialty fibers including Dyneema and aramid materials.

This supply uncertainty creates competitive disadvantages for manufacturers with limited raw material inventory buffers, particularly affecting smaller regional competitors dependent on just-in-time procurement models. Additionally, competition from low-cost rope alternatives and substitution from traditional steel cables in price-sensitive applications constrains pricing power.

Environmental and Sustainability Concerns Regarding Synthetic Materials

Growing environmental consciousness and regulatory emphasis on sustainable manufacturing practices are creating market headwinds for conventional synthetic rope production. Petroleum-derived synthetic materials are increasingly scrutinized regarding environmental sustainability, with regulatory frameworks in developed economies imposing stricter guidelines on plastic product usage and disposal. Consumer and corporate preferences are shifting toward biodegradable alternatives, eco-friendly materials, and products with recycled content, creating competitive pressure on manufacturers to maintain traditional petrochemical-based production.

The absence of universally standardized recycling infrastructure for end-of-life synthetic ropes limits circular economy participation and creates disposal challenges, particularly in marine applications where rope abandonment contributes to ocean plastic pollution. Insurance companies and environmental compliance agencies increasingly require documentation of sustainable practices, creating operational complexity and requiring investment in the development of alternative materials.

Opportunity - Development of High-Performance Specialty Fibers and Smart Rope Technologies

Advanced fiber technologies, including Dyneema (UHMWPE), Kevlar, and Liquid Crystal Polymer (LCP) offer extraordinary strength-to-weight characteristics exceeding conventional synthetic materials by 5-15x, establishing premium market segments commanding substantial pricing premiums. Manufacturers are investing substantially in smart rope development, incorporating embedded sensors enabling real-time monitoring of tension, load, temperature, and structural integrity. These intelligent systems can provide predictive maintenance alerts and prevent catastrophic failure scenarios in critical applications.

The global smart sensor market for industrial applications is projected to expand at approximately 20.9% annually through 2032, with rope-integrated sensors capturing an increasing share. Companies, including Samson Rope and Cortland, have commercialized advanced fiber systems demonstrating enhanced performance in aerospace, defense, and deep-ocean applications. This technology integration creates differentiation opportunities and justifies premium pricing, particularly among safety-conscious industrial operators and government defense applications.

Expansion into Emerging Markets and Infrastructure Development Acceleration

Emerging economies across Asia Pacific, Latin America, and the Middle East and Africa are experiencing accelerated infrastructure development, port modernization, and industrial expansion, driving extraordinary demand for synthetic rope. India’s infrastructure sector is projected to reach US$ 1.4 trillion by 2025, requiring advanced rigging solutions for skyscraper construction, bridge projects, and offshore development. The Sagarmala initiative, focusing on port modernization and coastal infrastructure expansion, has increased synthetic rope demand by approximately 18% year-over-year in 2023.

China’s vast maritime and construction sectors, combined with expanding offshore oil and gas exploration in the South China Sea, create substantial demand for high-strength synthetic ropes. Southeast Asian countries, including Vietnam and Indonesia, are emerging as manufacturing hubs leveraging regional supply chain efficiencies while generating incremental domestic consumption. Africa’s port expansion initiatives and offshore fishing industry growth create additional demand vectors. Manufacturers establishing regional manufacturing capabilities, localized distribution networks, and country-specific product customization are positioned to capture substantial growth in emerging market, estimated at 8-10% annually, compared to 5-6% in mature markets.

Category-wise Analysis

Material Type Insights

Polypropylene represents the leading synthetic rope material type, commanding approximately 42% of global market share in 2025, with dominance driven by exceptional cost-effectiveness, adequate performance characteristics for general-purpose applications, and established manufacturing infrastructure. Polypropylene ropes demonstrate superior tensile strength compared to polyethylene while maintaining lower costs than specialty fibers, establishing them as preferred materials for construction, general rigging, and agricultural applications.

Polypropylene’s ability to float on water and resist moisture absorption establishes suitability for marine and aquaculture applications where buoyancy characteristics provide operational advantages. The material’s excellent chemical resistance and durability in moderate UV environments position polypropylene as ideal for outdoor industrial applications. Manufacturing capacity for polypropylene rope production is globally distributed with established regional facilities in North America, Europe, and Asia Pacific, ensuring reliable supply and competitive pricing.

Rope Design Insights

Braided rope design represents the fastest-growing construction methodology, expanding at approximately 9.2% CAGR through 2032, substantially outpacing twisted and plaited design segments. Braided construction allows sustained heavy loads without kinking or unraveling, providing superior performance in marine, climbing, rescue, and industrial applications requiring exceptional reliability. Braided ropes made from polypropylene or polyester exhibit enhanced handling, improved knot security, and a longer operational lifespan compared to alternative designs.

The International Maritime Organization (IMO) and professional rescue organizations increasingly specify braided rope configurations for critical safety applications, thereby establishing regulatory preference that is driving market expansion. Manufacturers including Marlow Ropes, WireCo WorldGroup, and Samson Rope have invested substantially in braided rope product development, introducing advanced constructions including 12-strand hollow-braid designs achieving 85% weight reduction compared to steel equivalents.

Application Analysis

Marine and fishing applications represent the leading end-use segment, commanding approximately 42% of the global synthetic rope market value in 2025, with dominance driven by mandatory specification requirements in maritime operations and commercial fishing. The global maritime fleet's approximately 2.5% annual expansion, combined with aging vessel replacement cycles, sustains demand for high-performance mooring and rigging solutions.

Commercial fishing operations extensively use synthetic ropes for net rigging, mooring systems, and vessel equipment, with regional fishing industry expansion particularly pronounced in the Asia-Pacific region, supporting emerging aquaculture initiatives. Marine applications benefit from synthetic ropes’ exceptional resistance to saltwater corrosion, UV degradation, and harsh environmental conditions inherent in ocean operations.

Regional Insights

North America Synthetic Rope Market Trends and Insights

North America maintains commanding market dominance, accounting for approximately 36% of the global synthetic rope market value in 2025, with the United States establishing market leadership through technological innovation, advanced manufacturing capabilities, and substantial offshore oil and gas operations. Established manufacturers, including WireCo WorldGroup, Samson Rope Technologies, and Yale Cordage, have maintained regional market dominance through continuous product innovation, extensive distribution networks, and professional recommendation influence among industrial end-users.

The U.S. offshore oil and gas sector, valued at US$ 40 billion globally, continues generating substantial demand for high-performance synthetic ropes in drilling, production, and subsea operations. However, the expansion of renewable energy infrastructure, particularly offshore wind farm development in coastal regions, is establishing emerging growth vectors. Canada’s maritime and fisheries sectors, combined with expanding infrastructure projects, maintain consistent demand.

Regional regulatory emphasis on worker safety and operational efficiency continues driving synthetic rope adoption specifications in industrial applications. The region benefits from advanced manufacturing technology, extensive research and development capabilities, and strategic partnerships between rope manufacturers and end-use industries.

Europe Synthetic Rope Market Trends and Insights

Europe collectively represents a significant share of the global synthetic rope market value in 2025, with the region characterized by stringent quality standards, advanced manufacturing capabilities, and a strong emphasis on sustainable and eco-friendly rope production. Germany, the United Kingdom, France, and Spain represent primary European markets, with Germany maintaining technological leadership and a product innovation focus. European manufacturers, including Marlow Ropes, Teufelberger, and English Braids, have established market presence through specialization in premium product segments and sustainability-driven product development.

The region’s extraordinary emphasis on renewable energy infrastructure, particularly offshore wind farm expansion, is generating unprecedented demand for specialized synthetic ropes capable of functioning in extreme marine environments. European offshore wind capacity expansion, combined with regulatory frameworks promoting decarbonization, is establishing a strong market growth trajectory. Regulatory harmonization through European Union standards and professional recommendation guidelines facilitates cross-border market integration.

The region’s mature industrial infrastructure, established safety standards, and emphasis on product quality maintain competitive positioning. Environmental consciousness and sustainability requirements are driving innovation in biodegradable alternatives and in the development of products with recycled content.

Asia Pacific Synthetic Rope Market Trends and Insights

Asia Pacific has emerged as the fastest-growing regional market, expanding at approximately 9.5% CAGR through 2033, substantially outpacing global average growth rates and representing the principal incremental demand opportunity. China dominates the regional market with approximately 45% of production volume and represents the world’s largest rope manufacturing center, leveraging extensive manufacturing infrastructure, cost advantages, and technological capabilities.

China’s vast maritime and construction sectors, combined with expanding offshore oil and gas exploration in the South China Sea, generate extraordinary synthetic rope demand. Regional manufacturers, including Taizhou Shengfeng Rope, are innovating with UHMWPE technologies serving domestic infrastructure projects and export markets.

India is the region’s fastest-expanding individual market, driven by port modernization initiatives, the expansion of the shipping industry, and growth in the construction sector. The Sagarmala initiative, which focuses on port infrastructure development, has substantially increased the adoption of synthetic rope. India’s growing coastal economy and the expansion of its fishing industry create incremental demand vectors. Japan maintains a strong market position, with preferences for high-quality products and brand loyalty toward Panasonic and international manufacturers.

Southeast Asian nations, including Vietnam, Indonesia, and Thailand are experiencing market development with manufacturing expansion and fishing industry growth. Regional market expansion is supported by rising disposable incomes, accelerated infrastructure investment, and the proliferation of e-commerce platforms, enabling market access previously restricted to traditional distribution channels.

Competitive Landscape

The global synthetic rope market reflects a moderately consolidated competitive structure, with a small group of multinational producers holding a significant share while numerous regional manufacturers compete in specialized niches. Market leaders strengthen competitive positioning through technological advancements in high-performance fibers, process innovations that enhance tensile durability and fatigue resistance, and expansion of distribution networks in offshore energy, maritime logistics, and heavy industrial sectors.

Competitive strategies increasingly prioritize sustainability, including recyclable polymer development and circular economy integration, aligning with customer procurement requirements in offshore wind, port operations, and defense applications. Regional players are gaining share by offering customized solutions, faster delivery cycles, and competitive pricing supported by localized production and direct sales models.

Strategic mergers and acquisitions continue to reshape market concentration, enabling scale advantages in R&D and global after-sales service capabilities. The long-term competitive trajectory favors manufacturers investing in smart rope technologies and embedded sensor monitoring systems that support predictive maintenance and safety compliance.

Key Market Developments

- September 2023 – BRADEN launched TRS Synthetic Rope engineered for TR Series Recovery Winches (12,000–30,000 lb pulls). Four times lighter than steel cable, it features UHMPE/urethane coating, Vectran core, and eye splices for enhanced durability, easy handling, and safety in demanding applications.

- January 2023 – Verlinde launched the EUROBLOC VF synthetic rope electric hoists for loads up to 20,000 kg, featuring Dyneema® ropes, 15 patented innovations, and advanced rope angle management functions.

- November 2025 – Samson introduced CALIBRE™ synthetic rope for superyachts, featuring high-modulus polyethylene core and polyester braided cover for exceptional tensile strength, lightweight flexibility, superior abrasion resistance, minimal stretch, and customizable options enhancing docking, towing, and marine durability.

- January 2025 – Samson enhanced its global service offering with advanced testing capabilities in France via Corderie Lancelin's Ernée facility for up to 600-ton destructive testing, complemented by US advanced testing, residual strength testing, and digital asset management.

Companies Covered in Synthetic Rope Market

- WireCo WorldGroup Inc

- Samson Rope Technologies Inc.

- Cortland Limited

- Teufelberger Holding AG

- Lanex AS

- Touwfabriek Langman BV

- English Braids Limited

- Axiom Cordages Ltd

- Yale Cordage Inc.

- Unirope Ltd.

- Dong Yang Rope Mfg. Co., Ltd.

- Bexco NV-SA

- Atlantic Braids Ltd.

- Marlow Ropes

- Magento Inc.

- New England Ropes

- Southern Ropes

- Cox Group

Frequently Asked Questions

The global synthetic rope market is projected to reach US$ 2.5 billion in 2026.

Growth is driven by lightweight, high-strength performance offering up to 85% weight reduction versus steel and rising offshore renewable energy demand.

North America leads with 32–36% market share, while Asia Pacific grows fastest at 8.5–9.5% CAGR through 2032.

Offshore renewable energy infrastructure expansion and adoption of advanced high-performance fibers create major growth opportunities.

WireCo WorldGroup, Samson Rope Technologies, Cortland Limited, and Teufelberger are leading companies in synthetic rope market.