- Sensors & Controls

- Smart Grid Sensor Market

Smart Grid Sensor Market Size, Share, and Growth Forecast for 2025 - 2032

Smart Grid Sensor Market by Sensor (Voltage/Temperature, Outage Detection, Transformer Monitoring and Dynamic Line Rating and Others), Application (Smart Energy Meters, SCADA, Advanced Metering Infrastructure (AMI) and Others), End-user (Utility, Industrial, Commercial and Residential) and Regional Analysis from 2025 - 2032

Smart Grid Sensor Market Size and Share Analysis

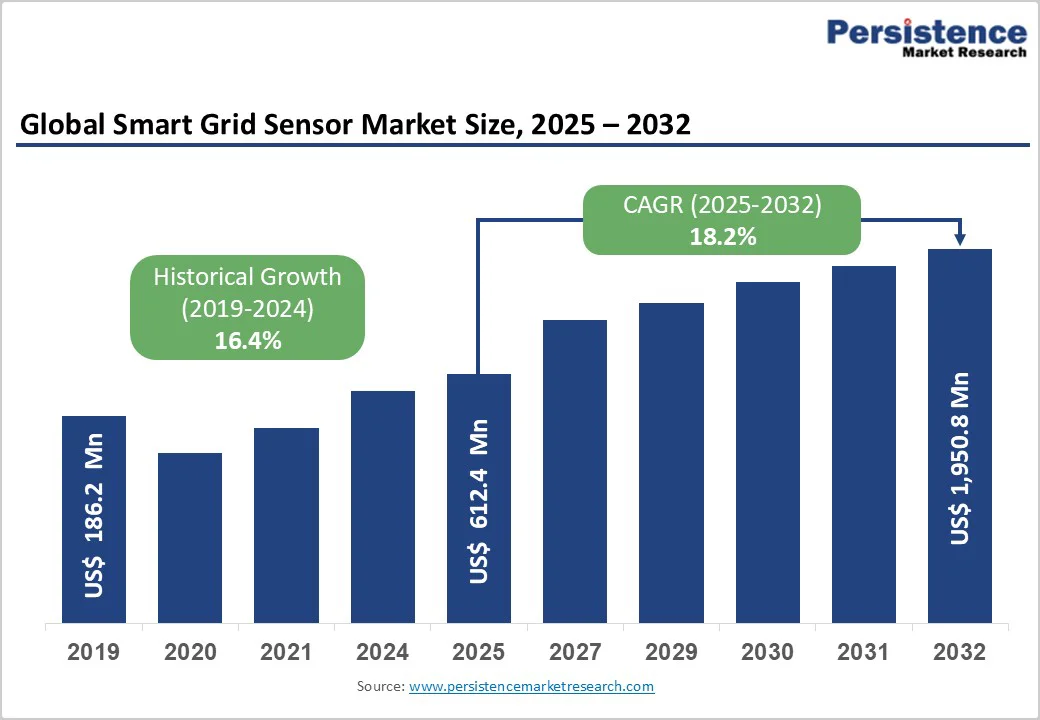

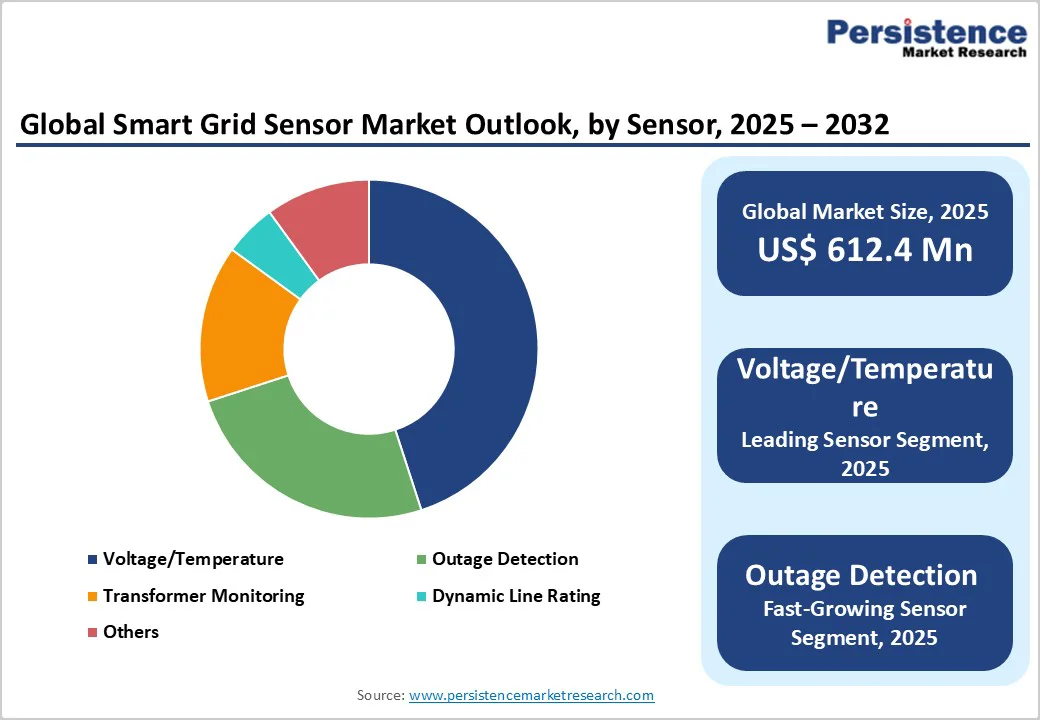

The global smart grid sensor market size was valued at US$ 612.4 million in 2025 and is projected to reach US$ 1,950.8 million, growing at a CAGR of 18.2% between 2025 and 2032. This robust expansion reflects accelerating global investments in electricity grid modernization, increasing renewable energy integration requiring advanced monitoring capabilities, and government mandates for enhanced grid resilience and efficiency.

Key Industry Highlights:

- Leading Component Segment: Voltage and temperature sensors dominate the global smart grid sensors market with a 35.7% share in 2025, serving as foundational components for equipment health and grid performance monitoring. These sensors play a vital role in predictive maintenance and system reliability enhancement across transmission and distribution networks.

- Leading Application Segment: Smart energy meters command a 48.4% market share in 2025, supported by large-scale deployments at consumer endpoints for comprehensive energy data collection and usage analytics. Their integration with digital platforms enables efficient energy distribution and real-time monitoring.

- End-Use Industry Leadership: The utility sector leads with a 54.3% share in 2025, underpinned by extensive adoption of smart sensors across transmission and distribution grids for operational efficiency and network reliability. Meanwhile, commercial End-users represent the fastest-growing segment, expanding at 14% CAGR through enhanced energy optimization and participation in demand response programs.

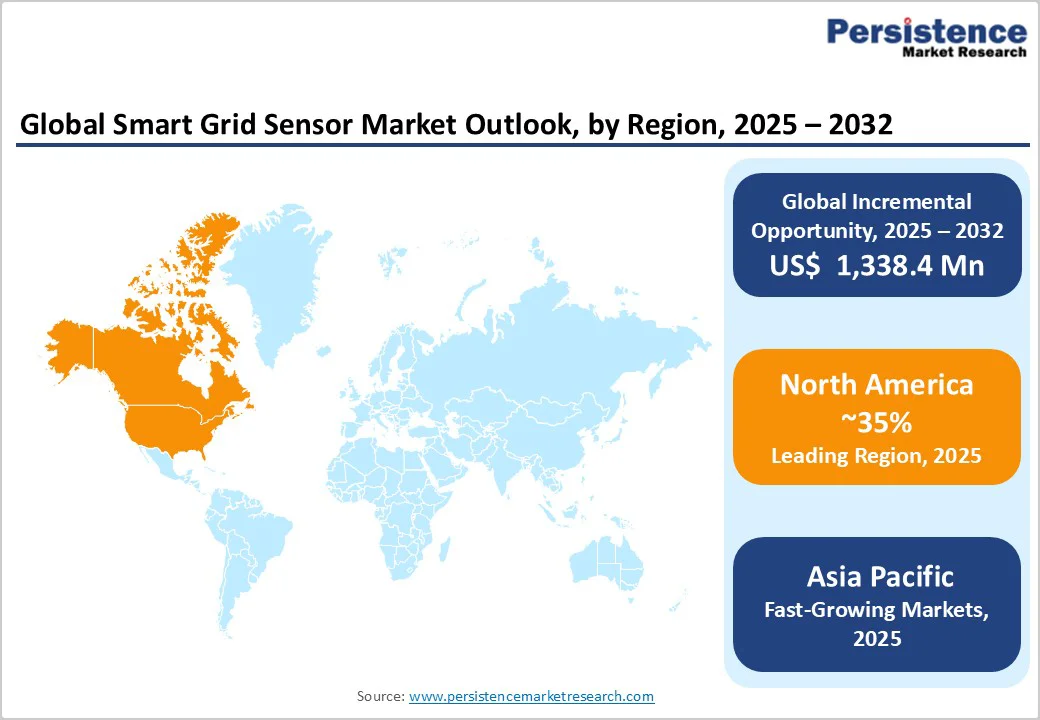

- Regional Leadership: North America dominates the global market with a 28.2% share, reaching US$218.2 million by 2025, driven by large-scale grid modernization and regulatory support for digital infrastructure. Asia Pacific emerges as the fastest-growing region with a 21.5% CAGR, led by China’s grid digitalization initiatives and India’s National Smart Grid Mission.

- Competitive Landscape: Siemens leads the market with estimated annual revenues of US$180–250 million through AI-driven grid management solutions. Key competitors include Schneider Electric, GE, ABB, and Itron, each strengthening portfolios with AI integration and predictive maintenance capabilities.

| Key Insights | Details |

|---|---|

|

Smart Grid Sensor Market Size (2025E) |

US$ 612.4 Mn |

|

Projected Market Value (2032F) |

US$ 1,950.8 Mn |

|

Global Market Growth Rate (CAGR 2025 to 2032) |

18.2% |

|

Historical Market Growth Rate (CAGR 2019 to 2023) |

16.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Innovative Machines Drives North America Smart Grid Sensor Market

Widespread aging electricity infrastructure across North America, Europe, and Asia Pacific creates urgent replacement demand for advanced sensor-based grid monitoring systems capable of delivering real-time performance insights and predictive asset health management. The United States operates electricity grids constructed primarily during the 1970s-1990s, with aging transformers, substations, and transmission lines experiencing increasing failure rates and service disruptions.

American Society of Civil Engineers estimates transmission and distribution systems require $2 trillion investment through 2030 for modernization and expansion, with smart sensors representing critical enabling technology for efficient infrastructure upgrades. The European Union prioritizes digitalization of power grids through €3.6 billion investment allocation specifically earmarked for grid sensor deployment across member states. India's electricity distribution networks, serving 1.4 billion population with historic underinvestment, require comprehensive sensor-based modernization to reduce technical and commercial losses exceeding 25% in many regions.

Renewable Energy Integration and Grid Stability Requirements

Exponential renewable energy adoption worldwide necessitates sophisticated sensor networks providing real-time visibility into distributed generation sources, line losses, frequency fluctuations, and voltage variations requiring continuous monitoring and active management unavailable through traditional infrastructure. Global renewable capacity additions reached 312 gigawatts in 2023, representing 90% of new electricity generation capacity deployed, while renewable penetration targets of 50-80% by 2030 across developed markets require unprecedented grid flexibility and responsive control capability.

Wind and solar energy sources demonstrate variable output requiring constant grid adjustments impossible to manage without dense sensor networks providing millisecond-response data on generation patterns, load distribution, and line conditions. Dynamic Line Rating sensors monitoring conductor temperature, wind speed, and ambient conditions enable utilities to maximize transmission capacity utilization during renewable generation peaks without infrastructure upgrades.

Restraints - High Capital Investment and Infrastructure Deployment Costs

Comprehensive smart sensor deployment demands substantial upfront capital investment, with typical municipal or regional utility installations costing $50-200 million depending on service territory size, requiring extended payback periods and constraining adoption in budget-limited jurisdictions. Distribution utility networks serving 1-5 million customers typically require 10,000-50,000 smart sensors across multiple voltage levels, with installed costs of $5,000-15,000 per location including equipment, installation labor, and communication infrastructure.

Developing nation utilities facing chronic capital constraints and limited financing access struggle to justify sensor investments competing with generation and distribution equipment replacement requirements offering more immediate customer service improvements. Legacy infrastructure retrofitting creates higher per-unit costs compared to greenfield deployments due to compatibility requirements, testing protocols, and integration with existing SCADA systems. Extended implementation timelines spanning 5-10 years for comprehensive deployment create budget allocation challenges across multiple fiscal years and political administrations with shifting priorities.

Cybersecurity Vulnerabilities and Data Privacy Concerns

Networked sensor systems create expanded cyber-attack surfaces requiring comprehensive security architecture, encryption protocols, and continuous monitoring imposing significant operational overhead and creating disincentives for rapid deployment adoption among security-conscious utilities. Smart grid sensors transmitting sensitive grid operation data through wireless networks and internet connections present intrusion vectors exploited by nation-states, criminal organizations, and hacktivists targeting critical infrastructure.

Utilities must implement advanced encryption, multi-factor authentication, network segmentation, and 24/7 intrusion detection systems, increasing operational complexity and requiring specialized cybersecurity expertise unavailable in many smaller utility organizations. Consumer privacy concerns regarding granular energy consumption data collected through smart sensors create regulatory compliance obligations and public relations challenges inhibiting marketing support for sensor deployments.

Opportunities - Artificial Intelligence Integration and Predictive Maintenance Applications

AI-powered analytics platforms analyzing real-time sensor data can identify incipient equipment failures, forecast peak demand, optimize energy distribution, and prevent outages days or weeks in advance, creating substantial utility cost savings and customer satisfaction improvements justifying premium pricing for advanced sensor systems. Machine learning algorithms processing voltage fluctuations, temperature variations, and current patterns from millions of sensors simultaneously enable detection of anomalies indicating impending transformer failures, cable insulation degradation, or distribution network imbalances.

Utilities implementing AI-driven predictive maintenance reduce equipment failure rates by 40-60% while extending asset lifespans and improving reliability metrics rewarded through regulatory incentive mechanisms. Schneider Electric's AI partnership with AiDash launched February 2023 delivered grid resilience tools incorporating satellite imagery with sensor data, achieving 85% accuracy in outage prediction and infrastructure threat identification. Market opportunity for AI-powered sensor analytics platforms estimated at $300-500 million by 2032 as utilities increasingly procure integrated solution packages combining sensors with analytics services.

Emerging Market Smart City Development and Digital Infrastructure Expansion

Rapidly urbanizing regions in Asia Pacific, Latin America, and Africa constructing new cities and infrastructure without legacy grid constraints can deploy smart sensors as foundational infrastructure rather than retrofit solutions, creating opportunity for lower-cost standardized implementations serving millions of new customers. Indian government's Smart Cities Mission allocating funding to 100 municipalities prioritizes advanced metering infrastructure and grid modernization with smart sensor deployment as component of integrated urban development strategies.

China's urban area expansion programs incorporating "smart cities" concepts explicitly mandate comprehensive sensor networks for grid management alongside water, traffic, and public safety monitoring systems. Brazil's electrical utility modernization initiatives focus on distribution network digitalization through smart sensors enabling grid losses reduction in developing regions with 15-30% non-technical losses. Market opportunity for emerging market smart sensor deployments estimated at $400-650 million by 2032 as urbanization patterns concentrate population in metropolitan regions requiring modern electricity infrastructure.

Water Quality and Wastewater System Monitoring Integration

Utilities managing integrated water-electricity infrastructure increasingly deploy sensor platforms spanning multiple utilities enabling cross-infrastructure optimization, asset management efficiency improvements, and operational cost reductions creating new procurement opportunities beyond traditional electricity grid applications. Smart sensors monitoring water distribution system pressure, flow, and quality characteristics interface with electricity grid sensors enabling coordinated management of water pumping loads optimized for renewable generation patterns and electricity pricing signals.

Integrated utility management platforms incorporating electricity, water, and gas system sensors provide consolidated visibility enabling single utility organization to optimize operations across infrastructure domains, reducing overall operational costs by 20-30%. Market opportunity for water-integrated sensor systems estimated at $100-200 million by 2032 as municipal utilities recognize cross-infrastructure optimization benefits.

Segmentation Analysis

Sensor Type Analysis

Voltage and temperature sensors dominate the smart grid sensor market with a 35.7% share, providing essential monitoring for voltage fluctuations, equipment stress, and thermal performance across transformers, cables, and switchgear. These sensors enable predictive maintenance and prevent failures through real-time data and dynamic line rating adjustments. Hybrid voltage-temperature sensor packages, such as those from Eaton and Sumitomo Electric, enhance cost efficiency and have achieved over 90% adoption in advanced utilities.

Outage detection sensors, growing at 18.2% CAGR through 2032, enable rapid fault identification and customer notification using AI and IoT-based systems. Smart meters with advanced algorithms detect anomalies and outages with 90%+ accuracy, reducing response times by up to 60% and improving overall grid reliability and customer satisfaction.

Application Analysis

Smart energy meters hold a 48.4% market share, serving as key utility endpoints for real-time data collection and two-way communication with control centers to enable demand management, time-of-use pricing, and load profiling. Integrated with voltage, current, and power quality sensors, smart meters provide visibility into distribution network conditions from the end-user perspective, transforming them from billing tools into active grid monitoring nodes.

Advanced metering infrastructure (AMI) is the fastest-growing segment, expanding at 16–18% CAGR as utilities adopt two-way communication for dynamic pricing, demand response, and energy efficiency optimization. AMI systems enhance grid reliability, detect faults and energy theft, and improve loss reduction by 8–12%, while global smart meter installations are projected to surpass 1 billion units by 2025.

End-User Analysis

Utility companies dominate the smart grid sensor market with a 54.3% share, as they operate extensive transmission and distribution networks requiring continuous monitoring for reliability and efficiency. Vertically integrated utilities deploy sensor networks across all voltage levels to balance supply and demand in real time, while municipal and cooperative utilities expand adoption through government grants, EU modernization funds, and joint procurement programs to reduce deployment costs.

The commercial and industrial sector is the fastest-growing end-user segment, expanding at 12–14% CAGR, driven by energy cost reduction goals and participation in demand response programs. Large facilities use smart sensors for real-time energy monitoring, peak load management, and automated building controls, achieving 15–25% energy savings and supporting ESG and sustainability initiatives through verified energy efficiency tracking.

Regional Market Insights

North America Smart Grid Sensor Market Trends

North America accounts for a market value of US$218.2 million in 2025, growing at a 12.8% CAGR through 2032, positioning the region as a mature and innovation-driven smart grid sensor market. The United States leads regional growth through the Grid Resilience Innovative Partnership (GRIP) Program, allocating US$10.5 billion for grid modernization and smart sensor integration across transmission and distribution networks. Major utilities such as Duke Energy, American Electric Power, and Southern Company have deployed over 150 million smart meters with integrated sensors, forming the backbone for outage management, demand response, and grid optimization.

Federal initiatives like the Infrastructure Investment and Jobs Act and renewable energy integration targets further accelerate adoption. In Canada, utilities benefit from US$100 million in Smart Grid Program funding, driving modernization projects across Ontario, British Columbia, and Alberta focused on enhancing distribution grid efficiency and stability.

Europe Smart Grid Sensor Market Trends

Europe is valued at US$156.8 million in 2025, expanding at a CAGR of 8.2% through 2032, driven by regulatory harmonization, renewable energy integration, and premium adoption of advanced sensor technologies. Germany leads the region with a mandatory smart meter rollout targeting full penetration by 2032, supporting advanced grid stability measures as wind and solar contribute over 65% of electricity generation. The United Kingdom accelerates deployment through regulatory mandates and modernization investments enabling intelligent grid management and renewable integration. France and Spain incorporate grid sensors into national energy transition strategies, backed by EU funding for technology transfer and standardization.

The European Union’s unified technical standards facilitate cross-border procurement and supply chain efficiency, lowering costs. Meanwhile, Nordic countries such as Sweden and Norway operate highly sophisticated sensor networks supporting 99% renewable generation periods and millisecond-level grid response capabilities for real-time stability management.

Asia Pacific Smart Grid Sensor Market Trends

Asia Pacific is the fastest-growing region, projected to reach a market value of US$548.9 million by 2032, expanding at a robust 21.5% CAGR. Growth is driven by rapid urbanization, ambitious renewable energy targets, and large-scale government infrastructure investments. China leads the regional market with a comprehensive grid modernization strategy aimed at 100% smart meter penetration and advanced sensor deployment across all voltage levels, supporting 1,200 GW of renewable capacity by 2032. India’s National Smart Grid Mission drives sensor implementation across major distribution networks with US$129.9 million in public funding, fostering scalable private utility models.

Addressing 25%+ distribution losses, India leverages smart sensors to reduce losses by 8–12%, achieving payback within 5–7 years. Meanwhile, Japan sustains technological leadership through government-backed innovation in advanced grid monitoring systems and the export of smart sensor technologies across regional markets.

Competitive Landscape

The smart grid sensor market exhibits moderate-to-high consolidation with leading players commanding approximately 35-40% combined market share, while specialized regional manufacturers and emerging innovators capture growing segments requiring niche expertise and localized support. Siemens AG emerges as market leader with estimated annual smart grid sensor revenue of US$180-250 million from global operations, leveraging comprehensive automation technology portfolio and software platforms enabling integrated grid solutions.

Recent Industry Developments

- In April 2024, Accurant International, LLC, has acquired Sentient Energy from Koch Engineered Solutions. Sentient Energy, a leader in electric grid transformation, offers intelligent sensors and analytics for fault detection and grid safety. This acquisition supports grid modernization and Net Zero goals.

- In November 2023, Schneider Electric, a leader in energy management and automation, called on energy decision makers to prioritize digital upgrades for sustainable, resilient, efficient, and flexible grids at COP28 and Enlit Europe 2023. Their experts highlighted the potential benefits of these upgrades, including increased network automation to drive the energy transition.

Companies Covered in Smart Grid Sensor Market

- ABB Ltd.

- Aclara Technologies LLC

- General Electric Company

- Honeywell International Inc.

- Eaton

- Toshiba Corporation

- QinetiQ Group PLC

- Torino Power Solutions Inc.

- Sentient Energy, Inc.

- ARTECHE

- Siemens AG

- Ingenu Inc.

- Other Market Players

Frequently Asked Questions

The Smart Grid Sensor market is estimated to be valued at US$ 612.4 Mn in 2025.

The key demand driver for the Smart Grid Sensor Market is the growing need for real-time monitoring, automation, and reliability in power distribution networks.

In 2025, the North America region will dominate the market with an exceeding 35% revenue share in the global Smart Grid Sensor market.

Among the Pressure Range, 4200 bar hold the highest preference, capturing beyond 55.2% of the market revenue share in 2025, surpassing other products.

The key players in the Smart Grid Sensor market are ABB Ltd., Aclara Technologies LLC, General Electric Company, Honeywell International Inc. and Eaton.