- Semiconductor Materials & Components

- Global SiC Diodes Market

Global SiC Diodes Market Size, Share, and Growth Forecast 2026 – 2033

SiC Diodes Market by Forward Current (2 to 5 A, 6 to 10 A, 11 to 20 A, 21 to 40 A, and Above 40 A), Reverse Current (650 V, 1200 V, 1700 V, and 3300 V), Application (Automotive, Medical Imaging, Communication, Data Centers, Defense, Photovoltaic Solutions, and Others), and Regional Analysis

SiC Diodes Market Size and Share Analysis

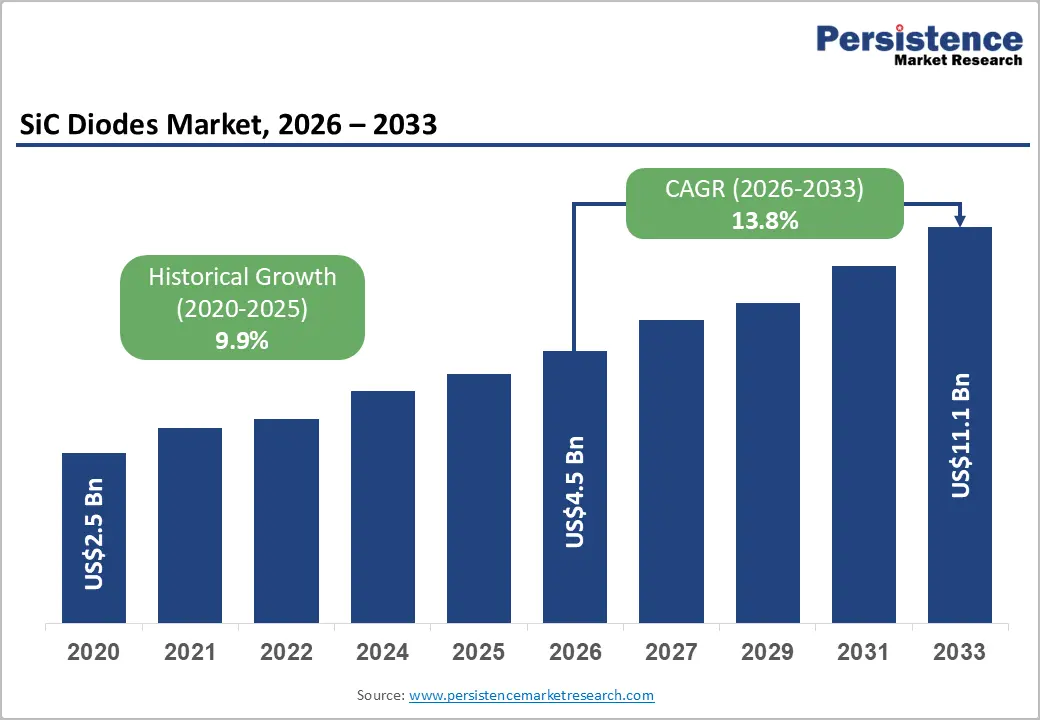

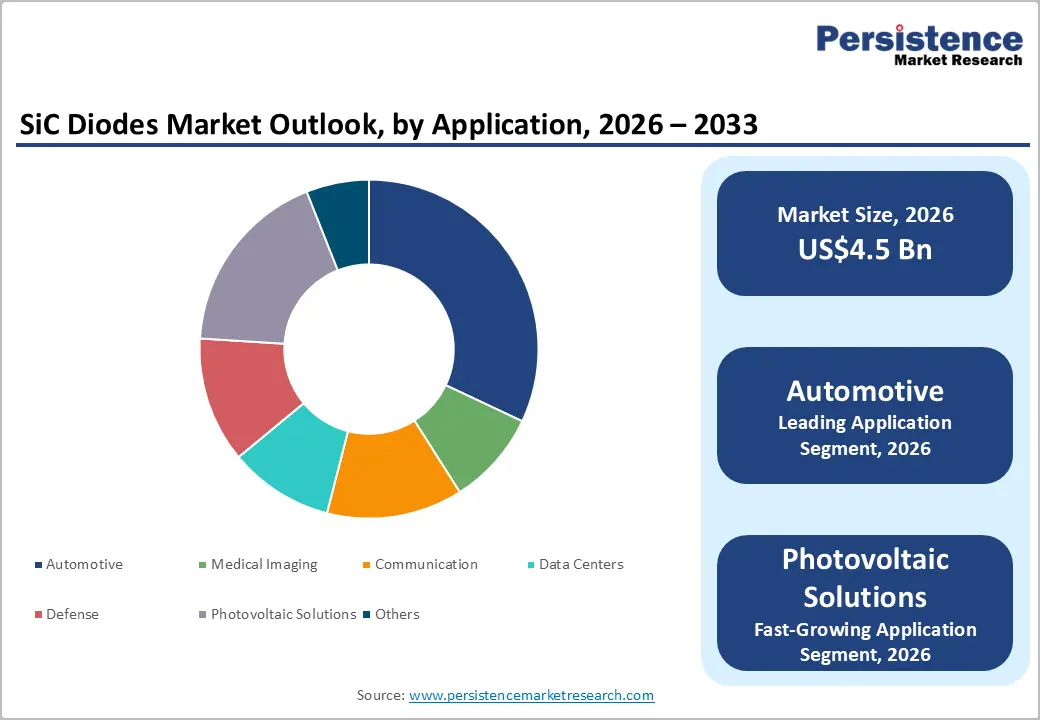

The global SiC Diodes market size was valued at US$ 4.5 Bn in 2026 and is projected to reach US$ 11.1 Bn by 2033, growing at a CAGR of 13.8% between 2026 and 2033. The SiC diodes market is experiencing rapid expansion driven by three primary factors, such as the accelerating electrification of transportation systems with electric vehicles requiring efficient power conversion, the exponential growth of renewable energy infrastructure demanding high-efficiency inverter solutions, and the proliferation of data centers powered by artificial intelligence requiring advanced power management technologies.

Key Market Highlights

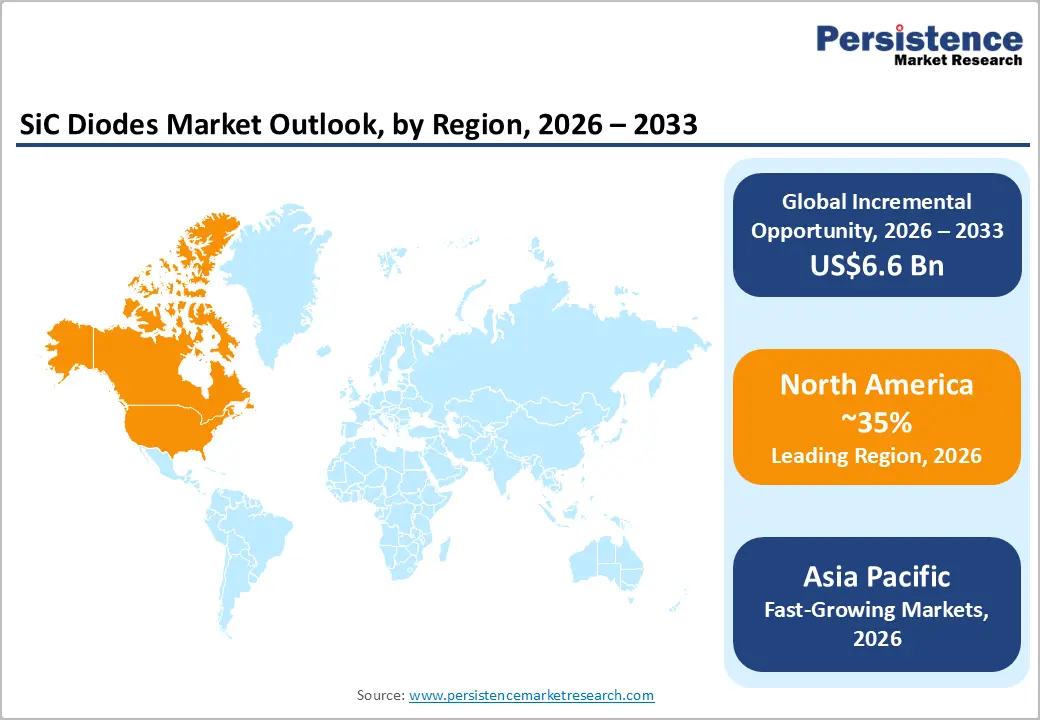

- Leading Region: The North American region maintains the largest market share at 35%, supported by established automotive manufacturing infrastructure, US government EV charging infrastructure investment (US$ 5 billion NEVI allocation), and innovation leadership in power electronics design and manufacturing.

- Fastest Growing Region: The Asia-Pacific region, despite lower current market share, exhibits the fastest growth trajectory at 18.2% CAGR, driven by China's dominant position as the world's largest electric vehicle producer (7.1 million units in 2024) and semiconductor manufacturing hub.

- Dominant Application: The automotive powertrain and EV charging segment dominates category-wise market position with 32% market share, reflecting regulatory mandates for vehicle electrification and strategic focus by major automotive manufacturers on SiC technology integration for performance and efficiency improvements.

- Growing Application: The photovoltaic solutions segment represents the fastest-growing application category at 24% CAGR, driven by renewable energy expansion and grid modernization initiatives across developed and emerging economies.

- Key Market Opportunity: The expansion of ultra-fast EV charging infrastructure and AI data center power architecture transition represents the most significant market opportunity, with 45% of 150kW+ charging stations incorporating SiC technology.

| Key Insights | Details |

|---|---|

|

Global SiC Diodes Market Size (2026E) |

US$ 4.5 Bn |

|

Market Value Forecast (2033F) |

US$ 11.1 Bn |

|

Projected Growth CAGR (2026-2033) |

13.8% |

|

Historical Market Growth (2020-2025) |

9.9% |

Market Dynamics

Market Growth Drivers

Rising Adoption of SiC Diodes in Traction Inverters, Onboard Chargers (OBCs), and DC-DC Converters

The increasing integration of Silicon Carbide (SiC) diodes in traction inverters, onboard chargers (OBCs), and DC-DC converters is a major driver for the global SiC diodes market, particularly within the electric vehicle (EV) ecosystem. In traction inverters, SiC diodes enable high-efficiency DC-to-AC power conversion required to drive electric motors. Their low switching losses, high breakdown voltage, and superior thermal performance reduce energy dissipation and heat generation, directly improving vehicle range and allowing for smaller, lighter inverter and cooling system designs. This is especially critical as automakers transition toward high-voltage EV platforms (400V–800V).

In onboard chargers (OBCs), SiC diodes enhance AC-to-DC conversion efficiency, supporting faster charging speeds, higher power density, and reduced charging losses. Their ability to operate at high frequencies enables compact charger architectures, improving vehicle packaging efficiency while meeting the growing demand for fast and ultra-fast charging compatibility. Similarly, in DC-DC converters, SiC diodes play a vital role in stepping down high-voltage battery power to low-voltage levels for auxiliary vehicle systems. Improved conversion efficiency reduces power losses and thermal stress, extending battery life and improving overall vehicle reliability. Collectively, these performance advantages are accelerating the adoption of SiC diodes across core EV power electronics, driving sustained market growth.

Renewable Energy Transition and Expansion of Solar Photovoltaic Systems

The global transition toward renewable energy, particularly the rapid expansion of solar photovoltaic (PV) systems, is a significant driver for the adoption of Silicon Carbide (SiC) diodes. As governments and utilities worldwide invest heavily in clean energy to meet decarbonization targets and reduce dependence on fossil fuels, demand for high-efficiency power electronics in solar installations continues to rise. SiC diodes are increasingly used in solar inverters, power conditioning units, and energy storage interfaces, where efficient DC-to-AC power conversion and high-voltage handling are critical.

In solar PV systems, SiC diodes offer lower switching losses, higher breakdown voltages, and superior thermal performance compared with conventional silicon diodes. These characteristics enable higher inverter efficiency, reduce energy losses, and improved system reliability, particularly in large-scale utility solar farms and high-power commercial installations. Their ability to operate at elevated temperatures also reduces cooling requirements, lowering overall system cost and improving operational lifespan.

The growing integration of energy storage systems and smart grids alongside solar PV installations further increases the need for advanced power semiconductor solutions. As solar capacity expands across residential, commercial, and utility-scale applications, the demand for SiC diodes continues to grow, making renewable energy transition a key long-term growth driver for the global SiC diodes market.

Market Restraints

High Manufacturing Costs and Wafer Supply Constraints

Silicon carbide wafer production remains significantly more expensive than silicon wafer manufacturing, with mature manufacturing processes and competitive economies of scale favoring silicon alternatives. SiC device manufacturers face material costs approximately 2-3 times higher than equivalent silicon solutions, which translates to component pricing that deters adoption in cost-sensitive applications.

Global SiC wafer manufacturing capacity constraints persist, with a documented 10% shortage in 2024 creating supply bottlenecks for device manufacturers. While vertical integration efforts by major players like STMicroelectronics, Infineon Technologies, and ON Semiconductor are expanding capacity through new fabrication facilities in Italy (Catania facility operational 2026) and joint ventures in China, near-term supply limitations continue to restrict market growth and price competitiveness.

Technical Complexity and Specialized Design Expertise Requirements

SiC device integration requires fundamentally different circuit design approaches compared to traditional silicon-based power electronics. System designers must address unique challenges including higher switching frequencies, thermal management considerations distinct from silicon devices, and gate drive requirements specific to SiC MOSFET and Schottky diode characteristics. The engineering expertise required for optimal SiC system design is not universally available across all manufacturer segments, particularly in emerging markets.

Integration difficulties arise from compatibility issues with legacy silicon-based component ecosystems, necessitating redesign efforts and extended validation cycles. Concerns regarding long-term reliability in extreme environmental conditions, particularly in aerospace and defense applications, require extensive qualification testing and standardization development, temporarily slowing market adoption in risk-sensitive sectors.

Market Opportunities

Ultra-High-Speed Electric Vehicle Charging and Grid Infrastructure Modernization

The deployment of direct current (DC) ultra-fast charging stations represents a high-growth opportunity for SiC diodes. Current-generation chargers operating at 150 kW and above increasingly incorporate SiC power modules, with market penetration reaching 45% of new ultra-fast charger installations in 2025. These systems require power conversion efficiency above 98% with compact thermal design specifications where SiC technology provides decisive advantages over silicon alternatives.

Grid modernization initiatives including solid-state transformers and flexible AC transmission systems (FACTS) devices incorporate SiC diodes for efficient power routing. The International Energy Agency (IEA) estimates that achieving net-zero emissions scenarios requires investment of US$ 2+ trillion annually in clean energy infrastructure through 2032, of which power conversion semiconductors represent an essential enabling technology. This macroeconomic infrastructure imperative creates sustained demand growth for SiC components across both transportation and energy sectors.

Artificial Intelligence Data Center Power Architecture Transition and Medical Imaging Application Expansion

The explosive growth in artificial intelligence and cloud computing is driving data center power consumption at approximately double the growth rate of general electricity consumption. NVIDIA and other AI infrastructure leaders are adopting 800 VDC direct power architectures, eliminating inefficient intermediate voltage conversions. SiC MOSFET power modules in these systems achieve power loss reduction of 30% compared to silicon alternatives, directly translating to operational cost savings in hyperscale data center operations where power expenditure represents the largest operating expense.

Medical imaging equipment, including MRI systems, CT scanners, and radiotherapy dosimetry devices, increasingly incorporate SiC components for their superior precision, radiation hardness, and high frequency switching capability. SiC's wide bandgap characteristics enable operation at elevated junction temperatures (175°C+), supporting compact thermal designs essential for medical equipment miniaturization. The medical SiC component market will grow more than 20% CAGR through 2033, driven by aging populations in developed economies and healthcare infrastructure expansion in emerging markets.

Category-wise Insights

Forward Current Analysis

The forward current (IF) rating represents the maximum sustained current a diode can conduct in forward bias mode, directly correlating with power handling capability and application class. The market demonstrates distinct demand patterns across current-rating segments, reflecting diverse application requirements ranging from low-power consumer electronics to industrial power distribution systems. The 21 to 40 A segment maintains the highest market share at approximately 28%, driven by prevalence in automotive powertrain applications where traction inverters and on-board battery charging systems operate at power levels requiring current ratings in this range.

This segment's leadership reflects the strategic focus of Volkswagen, Tesla, BMW, and other automotive manufacturers on SiC integration in mainstream vehicle platforms. SiC diodes in the 21-40 A range deliver superior performance in pulse-width modulation (PWM) switching circuits common in EV propulsion systems. The segment's dominance is supported by maturity in manufacturing processes, with STMicroelectronics, Infineon Technologies, and ROHM offering comprehensive product portfolios across multiple voltage ratings and thermal package options specifically optimized for automotive thermal and spatial constraints.

Reverse Current Analysis

The reverse voltage (VRMS) rating specifies the maximum reverse bias voltage a diode can sustain without breakdown, directly determining suitability for specific application voltage levels. The 1200V segment dominates market share at approximately 38%, reflecting its strategic positioning at the intersection of high-performance capability and manufacturing maturity. This voltage rating aligns with modern 400V battery architectures in electric vehicles and 600V DC bus systems in industrial motor drives, where 1200V-rated diodes provide safety margins accommodating voltage transients and surge conditions. The 1200V segment's leadership is reinforced by widespread availability from all major manufacturers including STMicroelectronics, Infineon Technologies, ROHM Semiconductors, ON Semiconductor, and Littlefuse Inc., enabling competitive pricing through supply chain maturity.

The 650V segment, traditionally serving lower-power applications including USB power delivery, charger power factor correction (PFC) circuits, and industrial power supplies, maintains approximately 24% market share but exhibits slower growth reflecting market saturation in mature applications. Conversely, the 1700V and 3300V segments together represent approximately 18% market share but demonstrate accelerating growth at 16% CAGR, driven by expansion in grid-scale energy storage systems, solar inverter topologies, and high-voltage industrial motor drives. These elevated voltage ratings enable system-level efficiency improvements through reduced current levels, subsequently decreasing I²R losses in power distribution networks.

Application Analysis

The automotive application segment, encompassing advanced driver-assistance systems (ADAS), infotainment systems, body electronics, and powertrain/EV charging subsystems, represents the dominant market segment with approximately 32% market share. This leadership reflects regulatory mandates for vehicle electrification, with European Union emissions standards (Euro 7) and United States EPA regulations mandating accelerated transition from internal combustion to electric propulsion. Within the automotive segment, EV charging infrastructure specifically, including on-board chargers (OBC) operating at 3-7 kW and off-board DC fast chargers at 150-350 Kw, drives the most significant SiC diode demand growth. Automotive grade SiC Schottky diodes rated at 1200V demonstrate superior thermal performance, with forward voltage drops of 1.35-1.40 V enabling efficiency improvements of 2-4% in charging systems compared to silicon predecessors.

The medical imaging segment, while smaller at approximately 8% of total market value, exhibits the fastest growth trajectory at 20% CAGR, supported by SiC's inherent radiation hardness and precision enabling applications in radiotherapy dosimetry, MRI power supplies, and CT scanner voltage regulation systems. Communication infrastructure, encompassing 5G telecommunications and satellite communication power systems, represents approximately 6% market share with expansion driven by 5G network rollout across Asia-Pacific and Europe, where high-efficiency power management reduces operational costs in remote base station installations.

Regional Insights

North America SiC Diodes Trends

North America maintains regional market leadership with approximately 35% market share, driven by established automotive manufacturing infrastructure, pioneering electric vehicle adoption, and substantial government infrastructure investment. The United States market specifically benefits from the Inflation Reduction Act (IRA), which allocated US$ 5 billion through the National Electric Vehicle Infrastructure (NEVI) Formula Program for charging station deployment across all states. Federal tax credits covering 30% of residential Level 2 charger installation costs and $7,500 incentives for electric vehicle purchases create direct demand stimulation.

Tesla's expansion of the Supercharger network to over 50,000 global charging locations, with North American concentration, accelerates SiC diode adoption in ultra-fast 350 kW charging systems. Major automotive suppliers including Marelli, which introduced an 800-volt SiC inverter platform in July 2022, are standardizing SiC integration across vehicle platforms. The region's technological innovation ecosystem, anchored in Silicon Valley and Detroit automotive clusters, maintains leadership in SiC power module design and application development, supporting premium-segment EV penetration where performance superiority justifies component cost premiums.

Europe SiC Diodes Trends

Europe represents approximately 22% market share, with dominant manufacturing centers in Germany, France, and the United Kingdom where automotive production concentration and stringent emission regulations drive SiC technology adoption. Germany specifically emerges as the leading European market, with growth projections of 28% CAGR through 2032, driven by Volkswagen, BMW, Mercedes-Benz, and Audi's aggressive electrification strategies targeting 100% electric powertrains by 2030-2035. European regulatory frameworks including Euro 7 emission standards and the EU Green Deal mandate vehicle electrification and infrastructure development, directly supporting SiC diode demand in automotive and charging infrastructure.

The United Kingdom market, supported by government initiatives including the ultra-low emission vehicle (ULEV) initiative and charging infrastructure subsidies, demonstrates comparable growth dynamics. France's automotive industry, anchored by Renault and PSA Groupe, alongside the nation's commitment to renewable energy expansion through both wind and solar capacity additions, supports dual-track market growth across both transportation and energy sectors. European market growth also faces temporary constraints from higher material and labor costs relative to Asian manufacturing hubs, necessitating focus on higher-margin applications and performance-differentiated products where SiC technology's efficiency advantages justify cost premiums.

Asia Pacific SiC Diodes Trends

Asia-Pacific represents the largest and fastest-growing regional market with 40-45% market share, anchored by China's dominant position as the world's largest electric vehicle producer and semiconductor manufacturing hub. China produced 7.1 million electric vehicles in 2024, representing 60% of global EV production, creating unparalleled demand for SiC components in traction inverters, battery management systems, and charging infrastructure. The Chinese government's Five-Year Plan targets 800V battery architecture standardization across manufacturers including BYD, Geely-Volvo, and NIO, directly necessitating 1200V-rated SiC diode adoption for power management circuits.

STMicroelectronics' joint venture with Sanan Optoelectronics in Chongqing, involving investment of 30 billion RMB (approximately US$ 3.2 billion), targets production of 480,000 SiC wafers annually by 2028, demonstrating strategic commitment to serving the Chinese market. Japan's automotive industry, represented by Toyota, Honda, Nissan, and Mazda, is integrating SiC technology across passenger and commercial vehicle platforms, with particular emphasis on fuel-cell vehicle power management and battery electric vehicle efficiency optimization. South Korea's semiconductor leadership through Samsung Electronics and SK Hynix, combined with automotive manufacturing through Hyundai-Kia Group, creates integrated ecosystem advantages for SiC technology advancement.

Competitive Landscape for the SiC Diodes Market

The global SiC diodes market exhibits a moderately consolidated structure with the top five manufacturers controlling approximately 70-75% combined market share. STMicroelectronics maintains regional dominance with 32.6% market share in 2023, reflecting comprehensive product portfolio spanning discrete diodes through integrated power modules and established customer relationships across automotive, industrial, and renewable energy sectors. Infineon Technologies represents the second-largest competitor with significant strength in automotive applications, supported by AEC-Q101 qualification across product lines and strategic focus on electric vehicle and data center power electronics. The competitive landscape demonstrates a clear strategic shift toward vertical integration, with leading manufacturers establishing control over entire value chains from SiC substrate manufacturing through device fabrication to module assembly and packaging.

This integration strategy addresses supply chain vulnerabilities exposed during the 2024 SiC wafer shortage and enables competitive differentiation through proprietary packaging innovations and thermal management solutions. Wolfspeed Inc. maintains critical position as the primary SiC wafer supplier, accounting for significant substrate supply across the industry, though competitors including STMicroelectronics, Infineon, and ROHM are establishing captive wafer production capabilities reducing supplier concentration risk. The market shows emerging competition from Chinese manufacturers including Sanan Optoelectronics (through STMicroelectronics joint venture), signaling potential future competitive intensity as production capacity localization accelerates.

Key Market Developments

- In September 2025, Wolfspeed Announces Commercial Launch of 200mm SiC Materials Portfolio. The commercial release of 200-millimeter silicon carbide wafers represents a significant manufacturing inflection point, enabling transition from 150mm (6-inch) to 200mm (8-inch) wafer technology.

- In December 2025, ROHM Launches SiC MOSFETs in TOLL Package with 39% Thermal Performance Improvement. ROHM's SCT40xxDLL series represents innovation in miniaturized SiC power modules, achieving thermal resistance reduction of 39% compared to conventional TO-263-7L packages while reducing footprint by 26% and profile height to 2.3mm.

- In November 2025, Wolfspeed Launches 1200V SiC Six-Pack Power Modules with 3x Power Cycling Capability. Wolfspeed's latest generation power modules incorporating Gen 4 SiC MOSFET technology achieve significant advancements including 22% on-resistance (RDS(ON)) improvement at 125°C and 60% reduction in turn-on energy (EON).

Companies Covered in Global SiC Diodes Market

- Infineon Technologies

- STMicroelectronics

- ROHM Semiconductors

- Cree, Inc.

- Microchip Technology Inc

- ON Semiconductor

- CALY Technolgies

- WeEn Semiconductors

- Littlefuse, Inc.

- United Silicon Carbide Inc.

Frequently Asked Questions

The global SiC Diodes market size is projected to grow from US$ 4.5 billion in 2026 to US$ 11.1 billion by 2033, representing a compound annual growth rate (CAGR) of 13.8% during the forecast period. This growth trajectory reflects the combined impact of electric vehicle electrification adoption, renewable energy infrastructure expansion, and artificial intelligence data center power management requirements across developed and emerging economies.

The SiC Diodes market is primarily driven by three converging factors, such as accelerating global electric vehicle adoption with governments investing US$ 5+ billion annually in charging infrastructure through programs including the US NEVI Program, EU Green Deal initiatives, and India's PM E-DRIVE scheme.

The automotive powertrain and EV charging segment maintains the largest market share at approximately 32%, driven by regulatory mandates for vehicle electrification across North America (IRA incentives), Europe (Euro 7 standards), and Asia-Pacific (China's mandatory 800V architecture transition).

North America maintains the largest regional market share at approximately 35%, supported by the US Bipartisan Infrastructure Law's US$ 5 billion NEVI allocation for EV charging deployment, Federal tax credits covering 30% of residential charging installation costs, and established automotive manufacturing infrastructure centered in Detroit and peripheral regions.

The most significant emerging opportunities include, ultra-fast EV charging infrastructure expansion, with 45% of 150kW+ chargers incorporating SiC technology and systems achieving 98%+ efficiency supporting accelerated deployment across highway corridors and urban centers.

The market is dominated by STMicroelectronics (32.6% share), Infineon Technologies, ROHM Semiconductors, Wolfspeed Inc., and ON Semiconductor, collectively controlling 70-75% combined market share.