- Specialty & Fine Chemicals

- Dibasic Ester Market

Dibasic Ester Market Size, Share, and Growth Forecast, 2026 – 2033

Dibasic Ester Market by Product Type (DBE-2, DBE-3, DBE-4, DBE-5, Others), Application (Paint Stripper, Resin, Solvent, Others), End-user (Paints & Coatings, Chemical, Textile, Others), and Regional Analysis for 2026 – 2033

Dibasic Ester Market Size and Trends Analysis

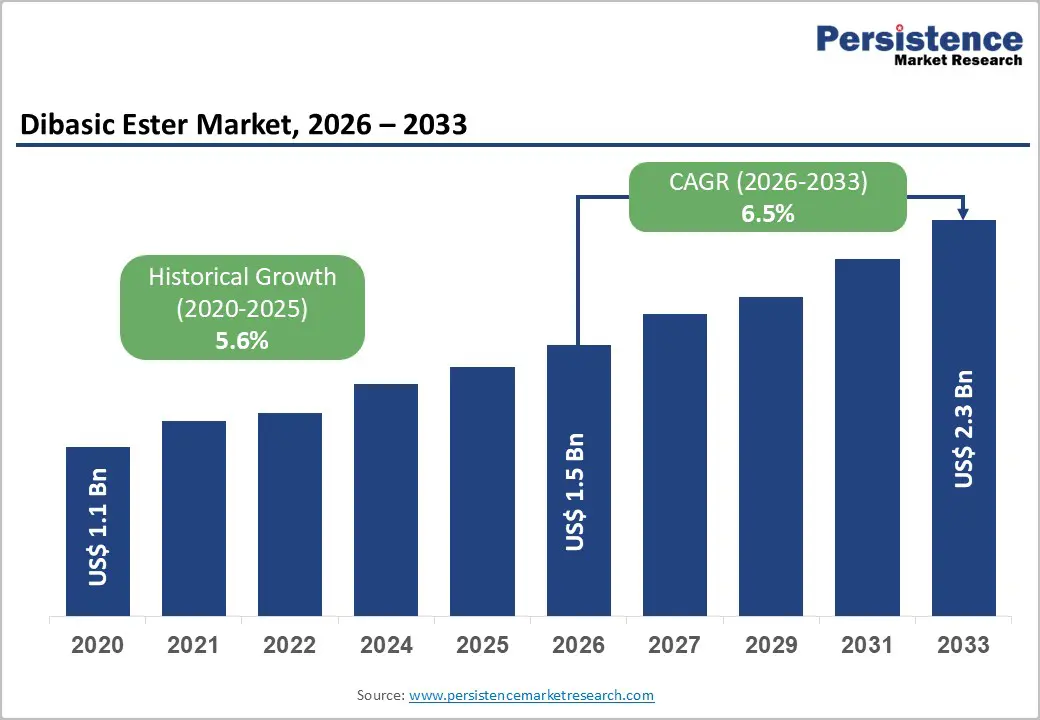

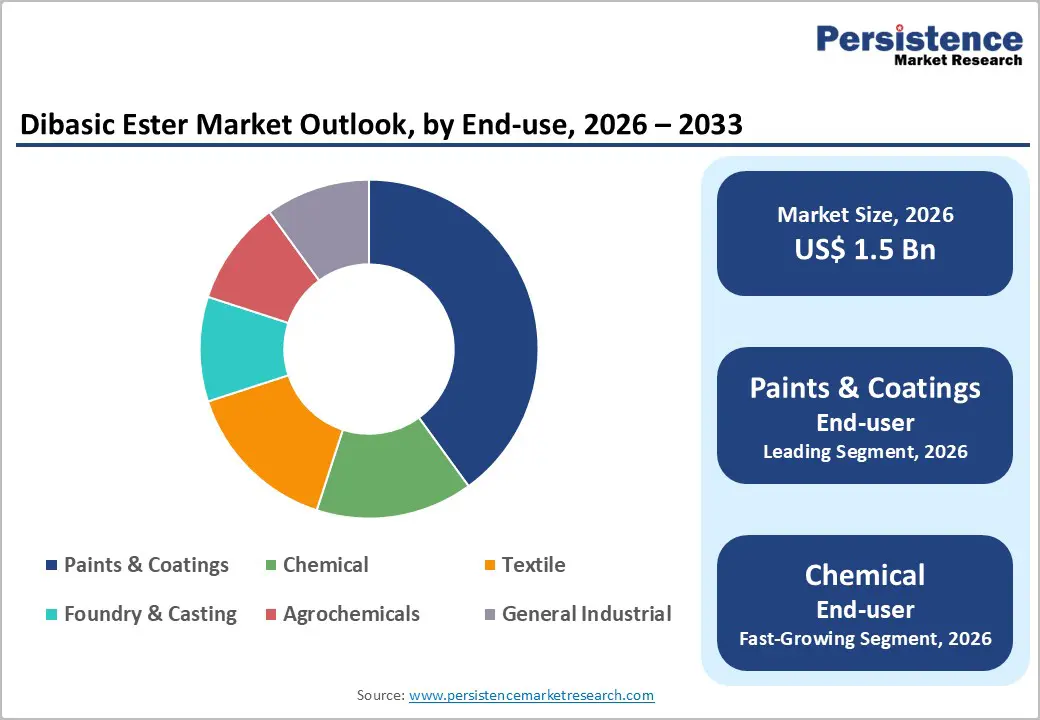

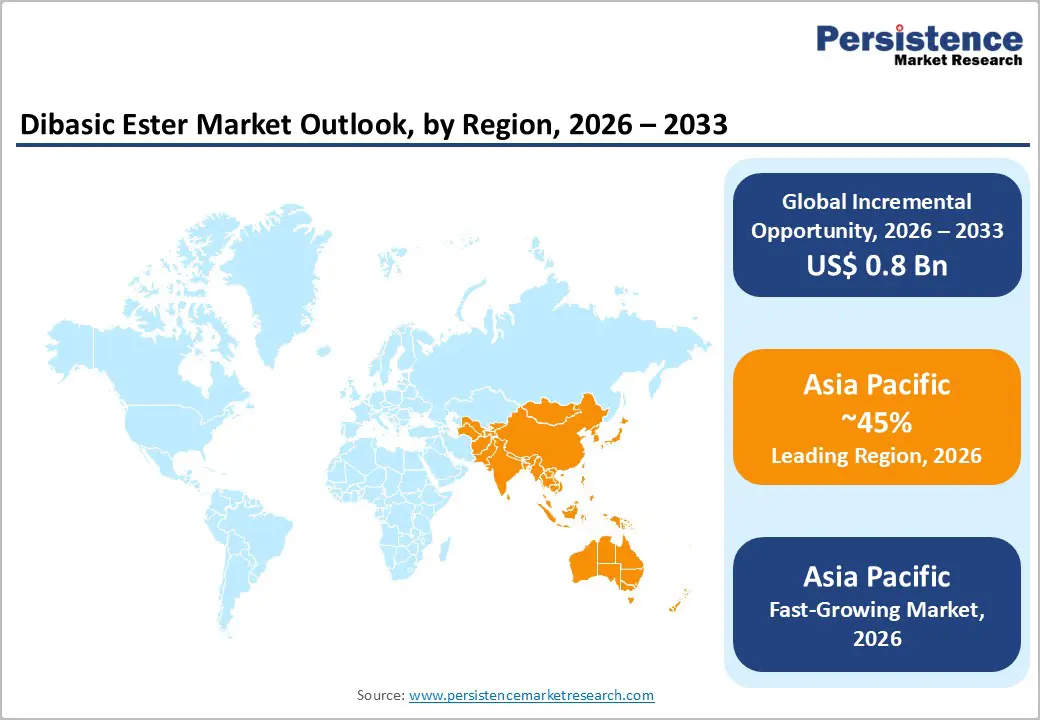

The global dibasic ester market size is likely to be valued at US$1.5 billion in 2026, and is expected to reach US$2.3 billion by 2033, growing at a CAGR of 6.5% during the forecast period from 2026 to 2033, driven by the increasing prevalence of eco-friendly solvents, rising demand for low-VOC alternatives in paints & coatings, and advancements in the formulation of blended dibasic esters.

Growing demand for versatile, biodegradable dibasic esters, especially in paint strippers and resin applications, is accelerating adoption across end-uses. Advances in DBE-4 and DBE-5 mixtures are further boosting uptake by offering superior solvency and safety. The growing recognition of dibasic esters as critical for sustainable industrial cleaning in emerging markets remains a key driver of market growth.

Key Industry Highlights:

- Leading Region: Asia Pacific, anticipated to account for a 45% market share in 2026, driven by rapid industrialization, high coatings production, and strong demand in China and India.

- Fastest-growing Region: Asia Pacific, fueled by construction growth, automotive expansion, and growing investments in green chemicals.

- Dominant Product Type: DBE-4, to hold approximately 35% of the market share, as it provides balanced solvency for coatings.

- Leading Application: Paint stripper, to account for over 30% of the market revenue, due to effective removal and low toxicity.

- Leading End-user: Paints & coatings, to contribute nearly 40% of the market revenue, due to VOC reduction needs.

|

Report Attribute |

Details |

|

Dibasic Ester Market Size (2026E) |

US$1.5 Bn |

|

Market Value Forecast (2033F) |

US$2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.6% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Increasing Demand for Eco-Friendly Solvents

The growing demand for eco-friendly solvents reflects a significant shift in how industries balance performance with environmental responsibility. Manufacturers in sectors like coatings, pharmaceuticals, electronics, and personal care are moving away from traditional petrochemical-based solvents due to their high volatility, toxicity, and disposal challenges. Eco-friendly solvents, sourced from renewable feedstocks or engineered for lower emissions, offer similar solvency while greatly reducing environmental and health risks.

Stricter environmental regulations have accelerated this transition by limiting volatile organic compound (VOC) emissions and promoting safer chemical alternatives. As compliance costs rise, companies are adopting greener solvent systems to ensure long-term regulatory compliance and operational stability. The increasing consumer awareness of sustainability is also encouraging brands to reformulate products using biodegradable, non-toxic solvent solutions. Technological advancements have also improved the efficiency and versatility of eco-friendly solvents, with innovations in bio-based chemistry and process optimization enhancing purity, thermal stability, and compatibility for a wide range of applications.

Limited Awareness and Technical Familiarity

Limited awareness and technical knowledge remain significant barriers in several specialty chemical markets, particularly for alternative and bio-based products. Many end-users, especially small and mid-sized manufacturers, continue to rely on traditional materials simply as they are well understood and have long-established performance benchmarks. In contrast, newer solutions often lack widespread technical exposure, making adoption slower despite clear functional or environmental advantages.

A major challenge lies in the knowledge gap surrounding formulation behavior. Engineers and formulators may be uncertain about how new materials interact with existing ingredients, equipment, or processing conditions. This uncertainty increases the perceived risk of production inefficiencies, product inconsistency, or customer complaints. Companies often delay adoption until extensive internal testing is completed, which adds time and cost.

Training and technical support limitations further reinforce this restraint. Not all suppliers provide detailed application guidance, case studies, or hands-on assistance, making it difficult for users to confidently implement changes. The limited availability of academic and industry literature undermines trust and slows the adoption of eco-friendly solvents. Cost sensitivity is also a significant factor. Without a clear understanding of long-term benefits, such as improved efficiency, regulatory compliance, or lifecycle savings, buyers tend to focus primarily on upfront costs.

Advancements in Low-VOC and Blended Delivery Platforms

Advancements in low-VOC and blended dibasic ester delivery platforms are transforming the global solvent landscape by addressing two major challenges, environmental regulations and performance gaps. Low-VOC platforms are engineered to achieve <1 g/L emissions, reducing reliance on hazardous solvents and enabling compliance in coatings. Innovations, such as optimized ester mixtures, bio-based feedstocks, high-boiling blends, and slow-evaporation designs, significantly improve safety and reduce odor, lowering reformulation costs for brands and sustainability campaigns.

Innovations in blended platforms, such as DBE-4/5 hybrids, custom DBE-9 formulations, multi-functional additives, and synergistic mixes, are enhancing solvency versatility and improving resin compatibility. These innovations overcome the drawbacks of single esters, enhance penetration, and offer flexibility in use without compromise, making them ideal for large-scale paint applications. Emerging technologies such as nano-emulsification, bio-adhesive solvency, and VLP-based blending further elevate their effectiveness and performance.

Category-wise Analysis

Product Type Insights

DBE-4 is anticipated to dominate the market, accounting for approximately 35% of the revenue share in 2026. Its dominance is driven by balanced solvency, low toxicity, and versatility, making it preferred for coatings. DBE-4 provides effective stripping, ensures safety, and contributes to compliance, making it suitable for large-scale paint campaigns. Invista’s DBE™ esters, which include fractionated forms such as DBE-4, are widely marketed as industrial solvent solutions for coatings, paint stripping, and maintenance uses. Invista, a subsidiary of Koch Industries, supplies these DBE esters (mixtures of dimethyl succinate, dimethyl glutarate, and dimethyl adipate) specifically for coatings and paint applications due to their effective solvency, low toxicity, and environmental advantages compared with traditional high-VOC solvents.

DBE-9 represents the fastest-growing segment, due to its high-boiling point and expanding use in specialty applications. Its slow-evaporation profile makes it ideal for targeted high-temperature, reducing flash-off. Continuous innovations in blending are further strengthening its appeal, driving rapid adoption across North America and Europe, where demand for advanced solvency is accelerating. Formulators at coatings manufacturers often replace more volatile solvents with DBE-9 in coil and can coatings or industrial topcoats to ensure consistent drying and improved surface performance, especially important in North America and Europe, where environmental regulations push for low-VOC, high-performance solvent systems.

Application Insights

Paint stripper is expected to lead, holding approximately 30% of the revenue share in 2026, driven by effective removal needs, large maintenance programs, and strong global demand for safe alternatives. Their dominance continues as industries expand into eco-friendly. Rising adoption of resin solvency and expanded additives campaigns highlight the growing focus on multi-functional benefits. Sunnyside Corporation is a major player in the paint stripper market that has developed benzene-free, low-VOC paint removers aimed at both DIY and professional users. Their formulations are designed to remove coatings effectively without harsh, toxic chemicals, responding directly to global safety and environmental regulations.

Additives represent the fastest-growing segment, due to strong momentum in formulation enhancement and expanding inclusion in plastics. The growing shift toward multifunctional platforms, along with improved compatibility, is accelerating adoption. Advancements in blended additives and the continued progress of specialty mixes entering production trials drive market growth. Clariant expanded its Cangzhou production site specifically to scale up its multifunctional Nylostab™ S-EED™ additive technology. This additive improves color stability, heat resistance, and composite compatibility in nylon plastics, directly enabling broader adoption in demanding applications such as automotive components and high-performance engineering plastics.

End-user Insights

The paints and coatings segment is projected to lead the market, accounting for nearly 40% of the revenue share by 2026. This is primarily due to its continued role as the main hub for low-VOC formulations, large-scale coating projects, and the management of a wide range of products that require safe solvent solutions. Their strong integration, trained chemists, and ability to handle high-volume or eco blends drive higher consumption. Paints & coatings sectors are leading DBE-4 rollouts as well as administering emerging DBE-9 trials.

INVISTA’s DBE® esters are widely supplied to major paints and coatings formulators as high-performance, environmentally friendly solvents. These DBE products, including DBE-4, are specifically used in industrial, decorative, architectural, and automotive coatings to enhance flow, leveling, gloss, and pigment hiding while reducing traditional VOC impacts in solvent-borne systems.

The chemical segment represents the fastest-growing segment, driven by its strong synthesis presence and expanding role in intermediates. They offer convenient, quick, and accessible solvency, attracting users who prefer versatile, low-toxicity settings. Increased outreach programs, industrial focus, and wider availability of routine and premium esters further accelerate uptake, boosting rapid adoption across both urban and semi-urban areas. Eastman’s ester products are leveraged not only as solvents but also as chemical intermediates and building blocks in polymer synthesis, plasticizer production, and specialty solvent blends, attracting formulators who need versatile, low-toxicity chemicals that simplify processing and improve performance in applications from coatings and adhesives to precision cleaning fluids.

Regional Insights

North America Dibasic Ester Market Trends

North America’s growth is driven by the region’s stringent VOC regulations, robust research and development capabilities, and high public awareness of the benefits of eco-friendly solvents. Processing systems in the U.S. and Canada provide strong support for formulation programs, ensuring widespread availability of dibasic esters across industries like paints and coatings, chemicals, and manufacturing. The increasing demand for low-VOC, user-friendly, and easy-to-integrate formats is further accelerating adoption, as these solutions enhance safety and reduce the challenges typically associated with traditional solvents.

Innovations in dibasic ester technology, such as stable blended mixtures, improved high-boiling delivery, and targeted sustainability enhancements, are attracting significant investments from both public and private sectors. Government initiatives and EPA campaigns continue to advocate for their use in reducing hazardous emissions, health risks, and environmental concerns, fostering sustained market demand. The growing focus on specialty chemical grades, especially for applications such as textiles, is expanding the range of potential uses for dibasic ester.

Europe Dibasic Ester Market Trends

Europe is boosting awareness of sustainability benefits through strong regulatory frameworks and government-led green initiatives. Countries like Germany, France, and the U.K. have well-established chemical regulations that facilitate the routine use of eco-friendly solutions, encouraging the adoption of innovative ester delivery methods, including dibasic esters. These sustainable formulations are particularly attractive to the paints and coatings industry, regulation-conscious operators, and industrial users, as they improve compliance and enhance coverage rates.

Technological advancements in dibasic ester development, such as low-VOC blends, application-specific delivery methods, and improved biodegradable grades, are further expanding market potential. European authorities are increasingly backing research and trials for esters to address both general and specialized needs, which is strengthening market confidence. The growing focus on convenient, safe alternatives aligns with the region’s priorities on preventive health and emission reduction. Public awareness campaigns and promotional efforts are broadening the reach in both urban and rural areas, while suppliers continue to invest in production and new variants to enhance efficacy.

Asia Pacific Dibasic Ester Market Trends

Asia Pacific is the dominant and fastest-growing region, expected to account for 45% of the market share by 2026. This growth is driven by increased industrial awareness, expanding government initiatives, and the broadening of application programs across the region. Countries like India, China, Japan, and those in Southeast Asia are actively promoting ester-based solutions to support manufacturing growth and meet the emerging demands of coatings. Dibasic ester is particularly appealing in these regions due to its cost-effectiveness, scalability, and suitability for large-scale industrial applications, benefiting both urban and rural populations.

Technological innovations are advancing the development of stable, efficient, and easy-to-process dibasic esters, capable of withstanding challenging production conditions while reducing dependency on toxic substances. These advancements are crucial for reaching remote facilities and improving solvency coverage overall. The growing demand in sectors such as paints and coatings, chemicals, and textiles is driving market expansion. Public-private partnerships, growing industrial investments, and increased funding for ester research and manufacturing capacities are further accelerating growth. The convenience of dibasic ester delivery, along with enhanced safety and reduced hazard risks, positions it as a preferred solution.

Competitive Landscape

The global dibasic ester market features competition between established chemical leaders and emerging specialty suppliers. In North America and Europe, Solvay SA and Merck KGaA lead through strong R&D, distribution networks, and industry ties, bolstered by innovative grades and solvent programs. In Asia Pacific, Shandong Yuanli Science and Technology Co., Ltd. advances with localized solutions, enhancing accessibility. Blended delivery boosts versatility, cuts VOC risks, and enables mass integrations across regions. Strategic partnerships, collaborations, and acquisitions merge expertise, expand capacities, and speed commercialization. Sustainable formulations solve regulatory issues, aiding penetration in green-focused areas.

Key Industry Developments

- In October 2025, BASF started up a new production line dedicated to dispersions for architectural coatings and construction materials at its facility in Dilovas?, Türkiye. The expansion has significantly increased production capacity at the Dilovas? site, allowing BASF to meet the rising demand for dispersions in Türkiye, the Middle East, and Northwest Africa. It also extends the regional product portfolio, which can now cover a shift in local customer needs and drive innovation.

- In February 2025, Thyssenkrupp Uhde GmbH, in partnership with Novonesis Group (Lyngby, Denmark), announced the launch of their joint offering, Uhde Enzymatic Esterification. This new technology bears the potential to revolutionize ester production by significantly reducing energy consumption and enhancing product quality through environmentally friendly biocatalysis, at a competitive cost-in-use of the enzyme.

Companies Covered in Dibasic Ester Market

- Solvay SA

- Merck KGaA

- INVISTA

- Prasol Chemicals Pvt. Ltd.

- Banner Chemicals Limited

- Shandong Yuanli Science and Technology Co., Ltd.

- T&J Chemicals Pte Ltd

- Comet Chemical Company Ltd.

- Redox Pty Ltd

- Santa Cruz Biotechnology, Inc.

- Carl Roth GmbH + Co KG

- PT Lautan Luas Tbk

- Acar Chemicals Inc.

Frequently Asked Questions

The global dibasic ester market is projected to reach US$1.5 billion in 2026.

The rising prevalence of eco-friendly solvents and demand for low-VOC alternatives are the key drivers.

The dibasic ester market is poised to witness a CAGR of 6.5% from 2026 to 2033.

Advancements in low-VOC and blended delivery platforms represent key opportunities.

Solvay SA, Merck KGaA, INVISTA, Prasol Chemicals Pvt. Ltd., and Shandong Yuanli Science and Technology Co., Ltd. are the key players.