- Testing, Inspection, & Certification

- Physical Intrusion Detection and Prevention Systems Market

Physical Intrusion Detection and Prevention Systems Market Size, Share, and Growth Forecast, 2026-2033

Physical Intrusion Detection and Prevention Systems Market by Component (Hardware, Software, Service), System Type (Keypad, Biometrics, Smart Card, Video Surveillance, Perimeter Intrusion Detection & Prevention, Security Scanning, Imaging & Metal Detection, Others), End-User (Critical Infrastructure, BFSI, Industrial, Government, Educational Institutes, Enterprise), and Regional Analysis for 2026-2033

Physical Intrusion Detection and Prevention Systems Market Share and Trends Analysis

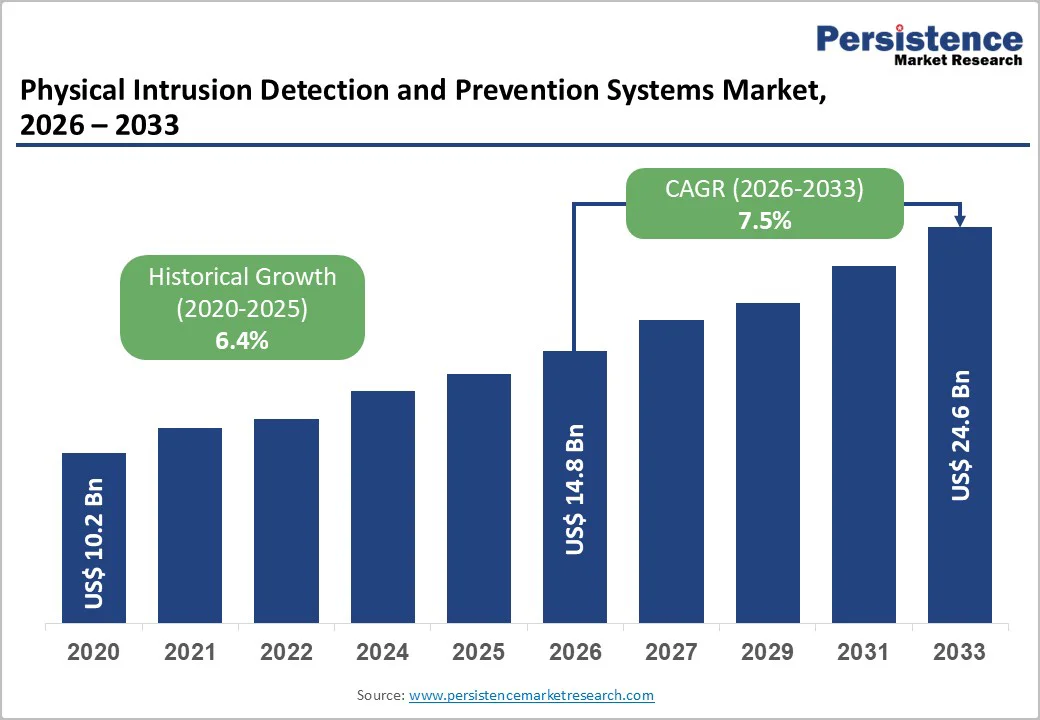

The global physical intrusion detection and prevention systems market size is likely to be valued at US$ 14.8?billion in 2026 and is projected to reach US$ 24.6?billion by 2033, growing at a CAGR of 7.5% during the forecast period 2026-2033. This growth is supported by heightened security concerns across critical sectors, the accelerating adoption of integrated intrusion detection technologies, and rising compliance with stringent regulatory safety standards worldwide. Strong demand for advanced video surveillance, biometric access control, and perimeter intrusion systems is expanding use cases across industrial, government, and enterprise environments. Incorporation of AI, IoT, and real?time analytics are improving threat detection accuracy and lowering operational risks, driving market expansion across mature and emerging regions.

Key Industry Highlights

- Leading Components: Hardware is expected to lead with a 55% share in 2026, while services are likely to be the fastest-growing at an estimated CAGR of 9.5% through 2033, driven by integration requirements and managed security solutions.

- Dominant System Types: Video surveillance is anticipated to command 32% in 2026, while biometrics is projected to record the fastest adoption at a CAGR of about 10.2% during 2026–2033, fueled by enhanced security needs in high-risk environments.

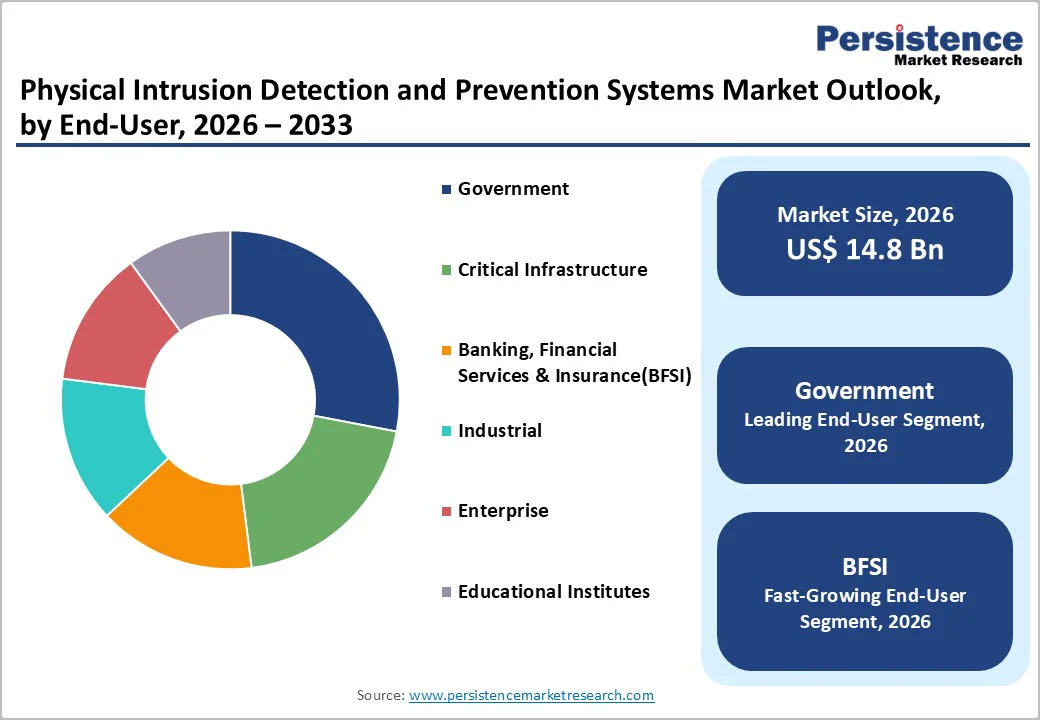

- Primary End-Users: Government is expected to account for an estimated 28% share in 2026, while BFSI is likely to emerge as the fastest-growing end-user segment at a CAGR of 8.8%, reflecting heightened regulatory compliance and asset protection requirements.

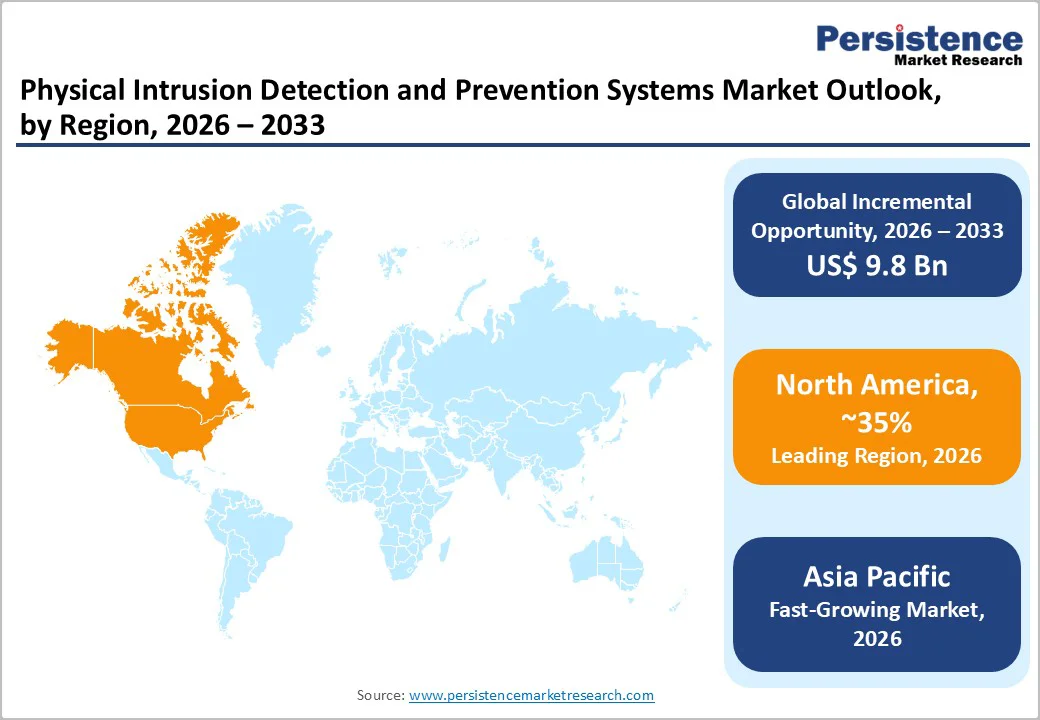

- Regional Leadership: North America is poised to dominate with an approximate share of 35% in 2026, while the Asia Pacific market is projected to expand the fastest at a CAGR of 11% through 2033.

- Competitive Environment: Strategic developments include technology partnerships, AI-based product launches, and mergers, enhancing real-time security capabilities and market reach across key geographies.

- March 2025: Honeywell launched the 50 Series CCTV cameras, its first security products designed and manufactured in India under the “Design in India, Make in India” initiative.

| Key Insights | Details |

|---|---|

| Physical Intrusion Detection and Prevention Systems Market Size (2026E) | US$ 14.8 Bn |

| Market Value Forecast (2033F) | US$ 24.6 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.4% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Escalating Security Risks Reinforced by Technology and Regulation

The rising incidence of physical security breaches, including unauthorized access, vandalism, and asset theft, has elevated physical intrusion risk management to a strategic priority for organizations. Growing exposure of critical infrastructure, commercial facilities, and public spaces has driven governments and enterprises to expand investments in integrated security frameworks that combine perimeter protection, video surveillance, and access control. This transition reflects a broader shift from reactive incident response toward proactive risk mitigation, supporting sustained demand for comprehensive intrusion detection and prevention systems designed to safeguard assets, operations, and public safety.

Technological advances in AI, IoT, cloud connectivity, and analytics are reinforcing this trend by improving detection accuracy, lowering false alarms, and enabling real-time monitoring across distributed environments. For instance, in June 2025, Teledyne FLIR introduced the PT-Series AI SR camera, integrating thermal and 4K visible imaging with edge-based AI analytics for precise perimeter detection and continuous target tracking across wide areas. Such innovations are complemented by stricter regulatory and compliance mandates requiring enhanced physical security in sensitive environments. Together, regulatory enforcement and technology maturity are expanding baseline security budgets and accelerating adoption of intelligent, compliant, and integrated physical security systems.

Cost-Heavy Deployments and Integration Challenges

The deployment of physical intrusion detection and prevention systems involves significant upfront investment, which limits adoption across cost-sensitive organizations. Hardware-intensive components such as high-resolution surveillance cameras, perimeter sensors, biometric access devices, and centralized control panels substantially increase capital expenditure. In large-scale environments, such as transportation hubs or multi-building industrial campuses, deployments often require hundreds of networked devices and redundant systems. These projects commonly entail total implementation costs in the range of US$3–6 million, depending on security complexity and redundancy requirements. Additional expenses related to system design, installation, and commissioning further elevate the total cost of ownership.

System integration challenges also present a structural restraint to market expansion. Organizations frequently operate multi-vendor security environments where access control, surveillance, and analytics platforms rely on different protocols and proprietary architectures. This lack of seamless interoperability complicates data sharing and system orchestration across security layers. Integration challenges increase deployment timelines, raise training and maintenance requirements, and elevate operational risk during system upgrades. Enterprises seeking unified security dashboards or centralized monitoring often face prolonged evaluation and implementation cycles.

Scalable Growth from Emerging Markets and AI-Driven Security Integration

The physical intrusion detection and prevention systems market is set to benefit from accelerating adoption of advanced security solutions in emerging economies, where rapid urbanization, industrial expansion, and infrastructure build-out are heightening exposure to physical security risks. Governments are increasingly embedding intrusion detection, video surveillance, and perimeter protection into transportation hubs, utilities, and public facilities as part of urban safety and infrastructure modernization programs. Expanding investments across energy, telecom, logistics, and smart transportation corridors are extending demand beyond tier-one cities into secondary urban centers and industrial clusters. This geographic expansion is opening large, underpenetrated customer pools, supporting sustained, volume-driven market growth for integrated security solutions.

The convergence of AI, cloud platforms, and advanced analytics is reshaping demand toward intelligent and unified security architectures. Leading vendors are advancing this shift through edge AI, cloud-managed platforms, and converged security capabilities. For example, Hanwha Vision’s showcase at ISC East 2025 highlighted next-generation AI cameras powered by edge-based processing and scalable cloud platforms that enable proactive threat detection and operational intelligence beyond basic monitoring. Similarly, Genetec’s addition of intrusion management to its Security Center SaaS platform demonstrates how unified, cloud-managed environments are becoming central to enterprise security strategies. These developments enable vendors to drive recurring revenues through analytics software, subscriptions, and managed services, reinforcing long-term profitability and customer retention

Category-wise Analysis

Component Insights

Hardware is projected to be the leading component, accounting for an estimated 55% of the physical intrusion detection and prevention systems market revenue share in 2026, due to its fundamental role in physical intrusion detection. Core elements such as surveillance cameras, perimeter sensors, control panels, and biometric readers are mandatory across most security deployments. Government facilities, industrial plants, transportation hubs, and critical infrastructure continue to drive large-scale hardware installations. High unit costs and coverage density requirements further reinforce revenue dominance. Hardware investments are largely non-discretionary in regulated environments. Replacement cycles and technology upgrades sustain recurring demand, keeping hardware as the primary revenue contributor.

Services are expected to represent the fastest-growing component, projected to expand at a CAGR of 9.5% through 2033. Growth is driven by increasing system complexity and the need for continuous performance optimization. Organizations increasingly rely on professional integration, managed monitoring, and maintenance services. Multi-site deployments amplify demand for centralized service models. Managed services reduce operational burden and staffing requirements. Subscription-based contracts improve cost visibility. This shift supports recurring revenue expansion for solution providers.

System Type Insights

Video surveillance systems are expected to capture approximately 32% of the market in 2026. Organizations deploy these solutions extensively for immediate threat monitoring, visible deterrence against unauthorized access, and detailed forensic investigation following security incidents. Commercial properties, manufacturing plants, transportation networks, and city centers represent primary installation sites where high camera densities generate substantial system value. Integration with artificial intelligence-driven analytics improves detection precision by distinguishing genuine threats from routine activities. Regular technology upgrades maintain performance standards and extend operational lifecycles, positioning video surveillance as the foundational component within comprehensive security frameworks.

Biometric systems are poised to emerge as the highest-growth segment, projecting a CAGR of 10.2% through 2033. Enterprises prioritize these technologies for irrefutable identity verification that prevents credential sharing or impersonation attempts. Facial recognition, fingerprint scanning, and iris authentication gain traction in fortified facilities where traditional access methods prove insufficient. Banking operations and server farms lead adoption due to elevated risks surrounding sensitive assets and customer information. Zero-trust architectures mandate continuous authentication throughout user sessions, amplifying biometric requirements across physical and logical access points. Declining hardware costs combined with accuracy improvements exceeding 99% boost enterprise confidence and deployment velocity.

End-User Insights

The government sector is anticipated to lead the market, commanding approximately 28% of the market revenues in 2026. National security imperatives and public safety obligations drive sustained procurement across critical infrastructure, including international borders, airports, railway stations, seaports, and government facilities. Governments allocate budgets through policy mandates rather than purely commercial considerations, making this spending relatively insulated from economic downturns and market volatility. Regulatory compliance frameworks require continuous investment in surveillance and perimeter protection technologies, ensuring predictable revenue streams for system providers. Large-scale centralized monitoring programs further reinforce government dominance as the primary revenue contributor. From a strategic perspective, vendors serving this segment benefit from long-term contracts, standardized procurement processes, and opportunities to scale deployments across multiple jurisdictions.

The BFSI sector is likely to represent the fastest-expanding end-user segment, with projected CAGR of 8.8% between 2026 and 2033. Financial institutions confront escalating physical security threats targeting cash repositories, automated teller machines (ATMs), data centers housing customer information, and branch locations, while simultaneously managing stringent regulatory oversight regarding asset protection and privacy safeguards. Banks increasingly integrate biometric access control systems and advanced video surveillance networks featuring analytics capabilities to detect suspicious behavior patterns in real time. Geographic expansion strategies involving multi-branch networks amplify deployment requirements across urban and suburban locations. Concurrent digital transformation initiatives elevate security standards as institutions recognize that physical intrusion prevention must complement cybersecurity protocols to protect hybrid infrastructure.

Regional Insights

North America Physical Intrusion Detection and Prevention Systems Market Trends

North America is projected to account for approximately 35% of the physical intrusion detection and prevention systems market share in 2026, driven primarily by the United States. Strong security infrastructure, mature enterprise adoption, and high public-sector spending support sustained demand. Federal and state compliance requirements mandate deployment of advanced intrusion detection across critical facilities. Enterprises continue to invest in integrated access control, perimeter protection, and AI-enabled surveillance systems. High awareness of physical risk and asset protection reinforces long-term adoption. The regional market also benefits from early technology adoption and standardized security practices.

The North America market is expected to grow at a steady CAGR through 2033, supported by expansion of intrusion detection solutions into smart city infrastructures, healthcare, and industrial environments. Organizations increasingly favor cloud-connected platforms and analytics-driven monitoring. The competitive landscape is defined by innovation-led offerings and strong service ecosystems. Government contracts and long-term service agreements provide revenue stability. Continuous modernization of aging infrastructure sustains upgrade cycles. The region remains a priority market for both domestic and international vendors.

Europe Physical Intrusion Detection and Prevention Systems Market Trends

Europe is expected to remain a stable and well-regulated market, supported by strong regulatory alignment across member states and a sustained focus on public safety. Countries such as Germany, the U.K., France, and Spain are anticipated to continue leading deployments across transportation networks, industrial facilities, and government buildings. Enterprises are likely to prioritize compliance-ready security architectures that integrate surveillance, access control, and perimeter protection. Investment activity is expected to remain closely linked to infrastructure modernization and urban safety programs. Harmonized regulatory frameworks are projected to support consistent adoption across the region. This environment is likely to ensure steady and predictable demand.

The Europe market is foreseen to expand steadily over the forecast period, supported by ongoing smart city development and wider adoption of analytics-enabled surveillance systems. Organizations are likely to favor scalable and interoperable solutions to manage security across multiple sites efficiently. The competitive landscape is expected to continue reflecting a mix of global vendors and specialized regional players. Solution customization and service quality are anticipated to remain key differentiators. Compliance expertise is likely to play a decisive role in vendor selection.

Asia Pacific Physical Intrusion Detection and Prevention Systems Market Trends

Asia Pacific is expected to be the fastest-growing regional market, expected to register a CAGR of approximately 11% through 2033, driven by rapid urbanization and infrastructure expansion. The region is projected to hold approximately 28% market share in 2026, led by China, India, and ASEAN economies. Governments are investing heavily in public safety, transportation, and industrial security. Rising threat awareness is accelerating adoption across commercial and manufacturing sectors. Large population centers increase demand for scalable security systems. Growth extends beyond tier-one cities into emerging urban zones.

Market expansion is supported by localized manufacturing, competitive pricing, and strong government incentives. Biometric access control and AI-enabled surveillance adoption is increasing rapidly. Enterprises are upgrading legacy systems to meet rising security expectations. International vendors are forming partnerships to strengthen regional presence. Digital transformation initiatives amplify demand for integrated platforms. Asia Pacific remains the most attractive growth market over the forecast period.

Competitive Landscape

The global physical intrusion detection and prevention systems market structure is moderately consolidated, with leading vendors such as Honeywell, Johnson Controls, Bosch Security Systems, Axis Communications, and Hikvision accounting for a substantial portion of total market revenue. These players benefit from strong enterprise and government relationships, broad product portfolios spanning hardware, software, and services, and deep expertise in regulatory compliance. Continuous investment in R&D enables them to maintain leadership in AI-enabled surveillance, advanced access control, and integrated security platforms. Their ability to deliver end-to-end solutions positions them favorably for large-scale and mission-critical deployments.

Regional and specialized vendors focus on niche applications such as perimeter intrusion detection, biometric authentication, and analytics-driven monitoring. Barriers to entry remain high due to stringent compliance requirements, complex system integration, and the need for long-term service capabilities. However, increasing adoption of cloud-based platforms and open architectures is allowing software-centric firms to participate through analytics, monitoring, and platform integration. Over time, gradual market consolidation is expected as leading vendors pursue acquisitions and strategic partnerships to strengthen geographic reach, expand technology capabilities, and enhance service offerings.

Key Industry Developments

- In December 2025, the Louvre issued a €57 million public tender to overhaul its security infrastructure following a high-profile theft that exposed critical system gaps. The program focuses on upgrading CCTV networks, access control, intrusion and artwork detection, and centralized video management. It also includes deployment of digital safety management and cybersecurity platforms. The initiative underscores rising security investment priorities for high-risk cultural and public institutions.

- In September 2025, KEENFINITY Group officially launched Radionix, its dedicated brand for intrusion alarm and integrated monitoring systems, at the GSX conference in New Orleans. The flagship Radionix G Series unifies intrusion detection, access control, and fire alarms into a single platform. The launch followed KEENFINITY’s spin-off from Bosch in July 2025, marking a strategic repositioning. Radionix reflects renewed focus on platform-based security architectures under KEENFINITY’s independent operations.

- In April 2025, the Security Industry Association announced the winners of the New Products and Solutions (NPS) Awards at ISC West in Las Vegas. Vaidio emerged as the most prominent winner, securing the Best New Product Award for its Vaidio 9.0 AI Vision Platform, alongside multiple category honors. Intrusion detection categories also recognized innovations from Spot AI and Hexagon, highlighting advances in remote monitoring and lidar-based vision systems. The awards reflect the industry’s accelerating transition toward AI-centric physical intrusion detection platforms.

Companies Covered in Physical Intrusion Detection and Prevention Systems Market

- Honeywell International Inc.

- Johnson Controls International plc

- Bosch Security Systems

- Axis Communications AB

- ADT Security Services

- Dahua Technology

- Hikvision

- Senstar Corp.

- Genetec

- Tyco International

- FLIR Systems

- Siemens AG

- Hanwha Techwin

- Avigilon

Frequently Asked Questions

The global physical intrusion detection and prevention systems market is projected to reach US$ 14.8 billion in 2026.

Rising number of physical security threats, increasing protection of critical infrastructure, regulatory compliance mandates, and growing adoption of AI-enabled surveillance and access control technologies are driving market growth.

The market is poised to witness a CAGR of 7.5% from 2026 to 2033.

Convergence of physical and digital security platforms, increasing adoption of AI-driven predictive threat detection, and growing demand for managed security services are key market opportunities.

Honeywell International Inc., Johnson Controls International plc, Bosch Security Systems, Axis Communications, and Hikvision are some of the key players in the market.