- Specialty & Fine Chemicals

- Desiccants Market

Desiccants Market Size, Share, and Growth Forecast, 2026 - 2033

Desiccants Market by Product Type (Silica Gel, Zeolite, Activated Alumina, Activated Charcoal, Calcium Chloride, Clay, Others), Absorption Process (Physical, Chemical), Application (Electronics, Food, Pharmaceutical, Packing, Air & Gas Drying, Others), and Regional Analysis for 2026-2033

Desiccants Market Share and Trends Analysis

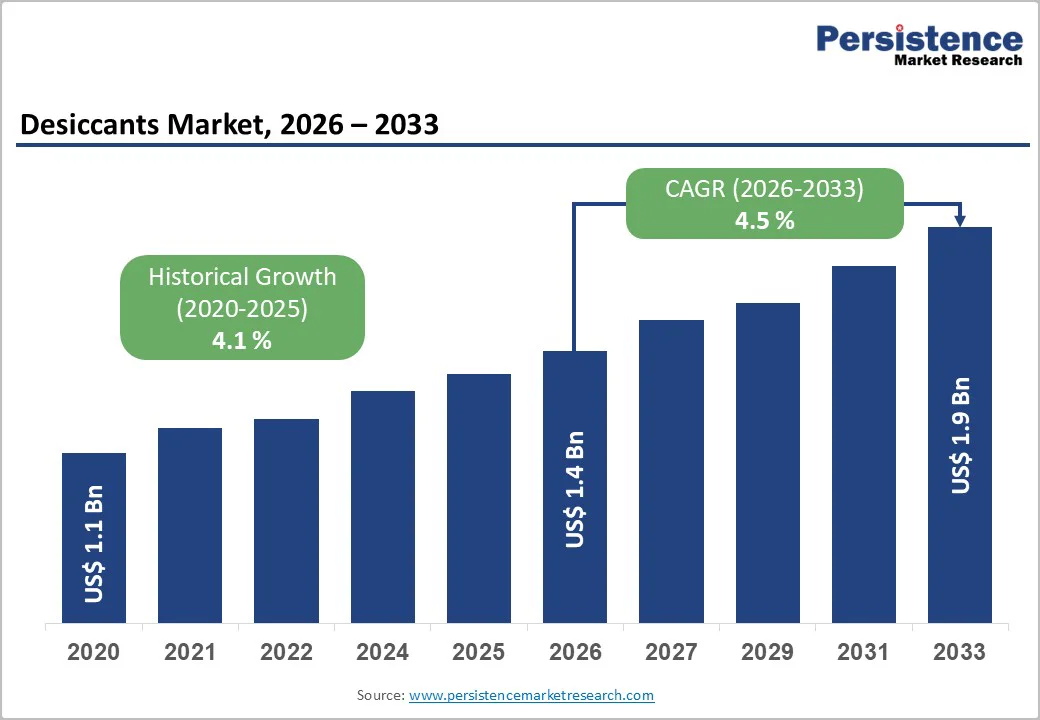

The global desiccants market size is likely to be valued at US$ 1.4 billion in 2026, and is projected to reach US$ 1.9 billion by 2033, growing at a CAGR of 4.5% during the forecast period 2026−2033. Growth is primarily influenced by rising moisture-control requirements across electronics packaging, pharmaceutical stability, and industrial air-drying applications. Regulatory standards on product safety in food and pharma supply chains are strengthening demand for high-efficiency desiccants. Additionally, increased adoption of silica gel and zeolite-based technologies supports the market's structural expansion. Demand in the Asia Pacific continues to scale because of manufacturing concentration and export-oriented operations.

Key Industry Highlights

- Leading Product Type: Silica gel is anticipated to command about 34% of the product category in 2026, supported by its broad industrial usage.

- Fastest-growing Product Type: Zeolites are projected to expand the quickest at 5.8% CAGR through 2033, boosted by increasing deployment in industrial and high-efficiency drying systems.

- Dominant Absorption Process: Physical absorption is likely to remain dominant with a 56% share in 2026, due to its extensive application in packaging and routine moisture-control operations.

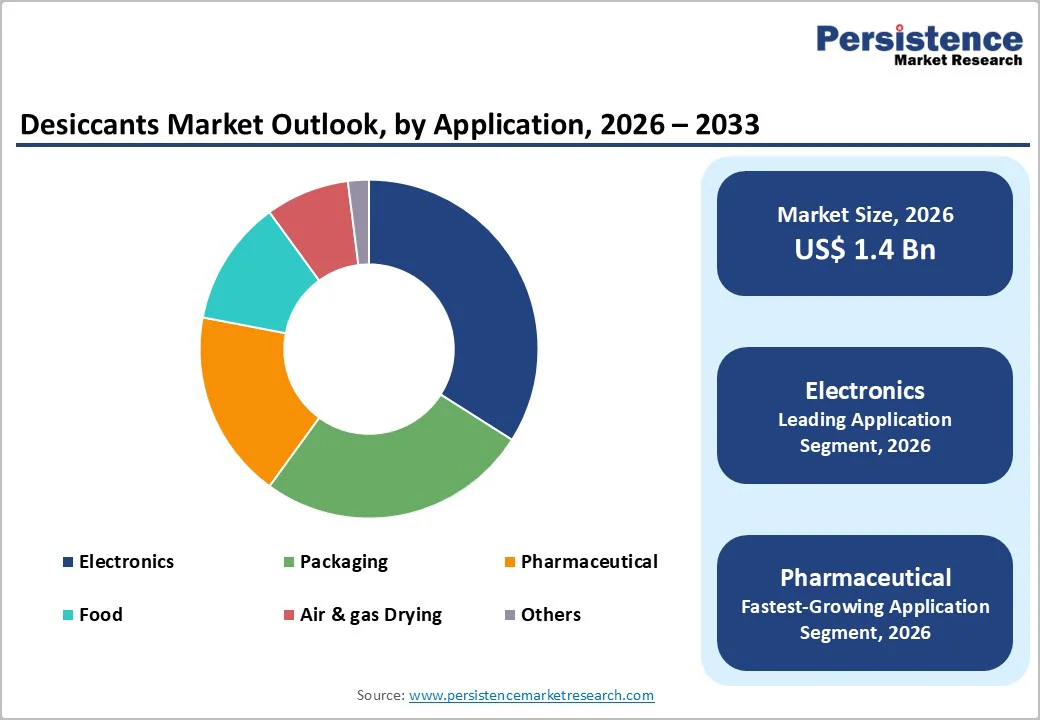

- Dominant Application: Electronics is likely to lead with 34% share in 2026, as moisture-sensitive components increasingly require stringent protective measures.

- Emerging Application: Pharmaceuticals are forecast to record the fastest expansion at 6.5% CAGR through 2033, propelled by intensifying global standards for drug safety and packaging reliability.

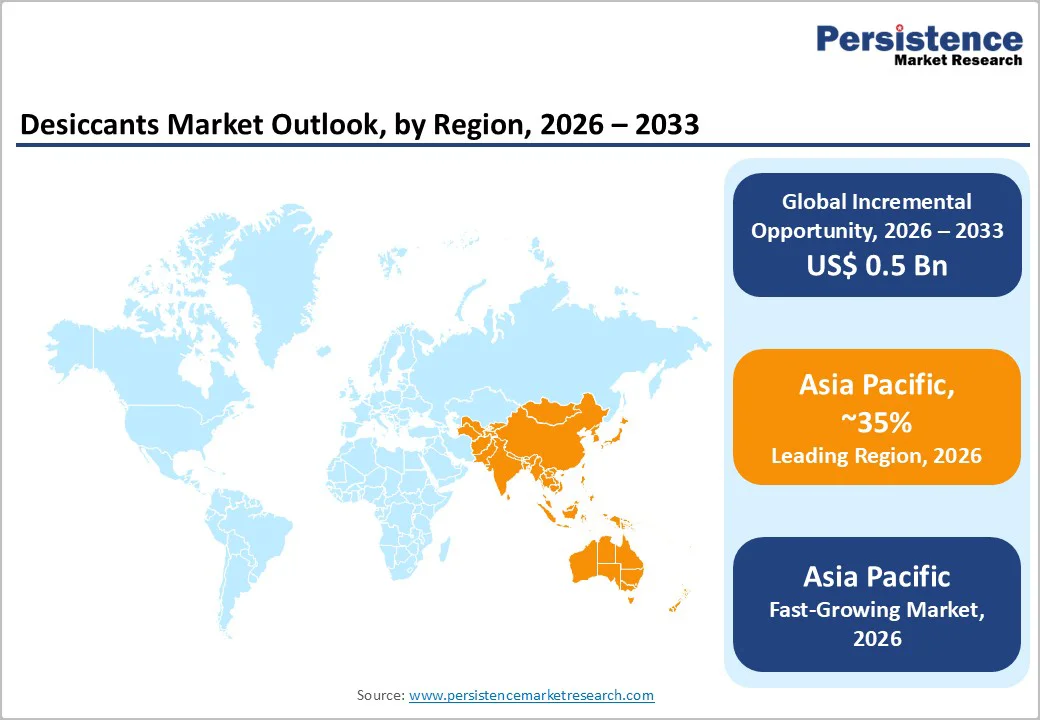

- Regional Leadership: Asia Pacific is estimated to dominate with a 35% share in 2026 and grow the fastest at 5.8% CAGR through 2033, fueled by manufacturing expansion and export-oriented production across China, India, and ASEAN.

- Key Driver: Expansion of semiconductor, 5G, and EV component production is increasing desiccant demand, as ultra-small nodes (5 nm) make devices highly susceptible to moisture-related defects, driving strict humidity-control requirements across manufacturing and logistics.

| Key Insights | Details |

|---|---|

| Desiccants Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 1.9 Bn |

| Projected Growth (CAGR 2026 to 2033) | 4.5% |

| Historical Market Growth (CAGR 2020 to 2025) | 4.1% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Demand for Moisture-Control Solutions across Manufacturing and Logistics

Diversification of operations in moisture-sensitive industries, particularly electronics, pharmaceuticals, and precision manufacturing, has significantly increased the need for reliable humidity-control systems. With the global electronics sector projected to scale new heights over the next decade, moisture protection for sensitive components has become increasingly critical, accelerating the use of desiccants in device packaging and logistics. Regulatory bodies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) require strict moisture standards for drug storage and packaging, strengthening the adoption of desiccant packets and canisters. Similarly, expanding semiconductor and circuit board production requires low-humidity environments to prevent material degradation and maintain product reliability.

Global e-commerce and logistics networks are managing larger volumes of goods that must remain protected during international transport. Cross-border merchandise movement has increased steadily, elevating the need for moisture-control packaging solutions in consumer electronics, pharmaceuticals, textiles, and other sensitive categories. Standards established by international shipping authorities emphasize the importance of cargo protection during extended transit, driving the use of desiccants in freight containers and distribution centers. The growth of industrial air- and gas-drying systems in energy and manufacturing sectors is also expected to support the demand for regenerable desiccant materials, creating a broad and durable foundation for market expansion.

High Production Costs and Environmental Compliance Pressures

Stakeholders in the desiccants industry must navigate intensifying financial risks driven by the volatility of mineral-based inputs. Manufacturers rely on raw materials such as silica gel, zeolites, and activated alumina, yet inconsistent mining yields frequently disrupt supply chains. The energy-intensive refinement process for these minerals further inflates production expenses and severely limits pricing flexibility. These cost dynamics disproportionately impact price-sensitive entities such as original equipment manufacturers (OEMs) in the packaging and electronics sectors. For these buyers, even minor fluctuations in raw material prices can erode competitive advantages. Consequently, suppliers should anticipate that rising input costs will continue to strain relationships with clients who operate on thin profit margins.

Environmental compliance simultaneously presents a formidable operational hurdle for industry incumbents. Chemical absorption products such as calcium chloride require rigorous handling protocols to prevent ecological damage. Authorities are enforcing stricter regulations regarding waste management, which increases the administrative and financial burden on producers. This regulatory landscape forces companies to reevaluate their total cost of ownership (TCO) as disposal fees rise. As industrial consumers increasingly prioritize environmental, social, & governance (ESG) goals, demand shifts toward sustainable and reusable alternatives. Organizations that fail to innovate beyond traditional, single-use chemical solutions risk losing relevance in a market that now views regulatory adherence as a baseline requirement rather than a differentiator.

Expansion of Advanced, Sustainable, and High-Performance Desiccant Solutions

The strategic focus on sustainability and operational efficiency is accelerating the demand for regenerable desiccant materials. Key players such as Clariant, Multisorb, and Absortech are actively advancing eco-efficient solutions to capture this market momentum. Clariant is driving this shift through Research and Development (R&D) initiatives that enhance their portfolio of environmentally optimized products. Their innovations include reusable silica gel, molecular sieves, and activated alumina designed to minimize waste in air-drying systems. These efforts help industrial clients achieve global environmental goals while ensuring consistent performance. By reducing the overall carbon burden, these manufacturers are redefining industry standards for durability and lifecycle management.

Parallel expansion opportunities are emerging within critical sectors such as healthcare, pharmaceuticals, and advanced electronics. These industries demand precise humidity control to maintain product safety and efficacy. Multisorb is targeting these needs by introducing high-efficiency canisters with reduced plastic content. This strategy reflects a broader transition toward specialized pharmaceutical-grade technologies. Absortech is also innovating with low-carbon dioxide (CO2) variants and programs utilizing recycled content. Such developments are vital for semiconductor and electric vehicle (EV) ecosystems that require ultra-efficient moisture-barrier packaging. These advancements establish advanced desiccants as essential enablers for compliance-driven applications globally.

Category-wise Analysis

Product Type Insights

Silica gel is set to lead in 2026 with an estimated 38% of the desiccants market revenue share, driven by its strong adsorption capacity, chemical stability, and broad usability across packaging, electronics, and pharmaceutical applications. Its regenerability and cost efficiency make it highly suitable for moderate-humidity environments, supporting consistent demand across mass-market and specialized uses. The introduction of new performance-enhanced formats, such as Madhu Silica Pvt. Ltd.’s silica gel breather cartridge launched in March 2025 for high-humidity pharmaceutical packaging, further strengthens its relevance in regulated, moisture-sensitive sectors. Industries value its safe handling, predictable adsorption behavior, and ability to meet stringent quality and compliance needs. These attributes reinforce silica gel’s long-standing dominance, especially as global packaging and electronics shipments continue to expand and diversified format compatibility widens its adoption across end-use industries.

Zeolite, the fastest-growing segment, is projected to expand at 9.5% CAGR between 2026 and 2033, supported by its rising adoption in high-temperature industrial drying, petrochemical processes, and gas-separation systems. Its ability to deliver precise moisture control under demanding operating conditions makes it increasingly attractive for advanced manufacturing. Molecular sieves offer higher efficiency where low residual moisture levels are critical, enabling wider penetration in industrial facilities and chemical processing units. Growth is also driven by increasing investments in energy-efficient drying operations, where zeolite’s enhanced performance provides significant advantages. As industries prioritize durable and specialized desiccants, zeolite’s share will continue to accelerate across global markets.

Absorption Process Insights

Physical absorption is expected to hold the largest share of 56% in 2026, aided by its widespread use in packaging, logistics, electronics, and pharmaceutical storage. Materials such as silica gel, clay, and activated alumina rely on simple yet highly effective adsorption mechanisms that offer consistent moisture control at a competitive cost. These solutions remain indispensable for routine humidity?management needs, particularly in supply chains requiring reliability and minimal handling complexity. Their ease of integration into sachets, packets, and storage systems further strengthens demand across multiple industries. As global shipments rise, physical absorption continues to dominate due to proven versatility.

Chemical absorption is poised to be the fastest-growing segment through 2033, driven by its exceptional moisture-uptake capacity in extreme humidity conditions. Reactive desiccants provide superior performance in industrial cargo, commercial storage, marine transport, and high-exposure logistics environments. Their ability to maintain stability even with high moisture loads makes them valuable for protecting bulk goods and sensitive materials during long-distance movement. As global supply chains become more complex, demand for high-capacity desiccants is increasing, especially in sectors prioritizing reliability under fluctuating environmental conditions. This shift positions chemical absorption as a rapidly expanding process type globally.

Application Insights

The electronics segment is expected to lead with an estimated 34% share in 2026, driven by the need for strict moisture control in device packaging, semiconductor storage, and protection of sensitive circuitry. Even small humidity fluctuations can cause component degradation, making desiccants essential in preventing failures. The growth of global electronics supply chains, particularly in East Asia, further increases the requirement for reliable drying solutions. High-value components, such as sensors and microchips, depend heavily on moisture-stable environments. As electronic exports and manufacturing volumes rise, the demand for precision desiccants remains strong.

The pharmaceutical segment is projected to grow at approximately 10.2% CAGR from 2026 to 2033, due to stringent stability guidelines and increasing production of moisture-sensitive formulations. Desiccants are vital in protecting tablets, capsules, and diagnostic products throughout storage and global distribution. Expanding temperature-controlled logistics networks support wider adoption of advanced humidity-control materials. As regulatory bodies emphasize packaging integrity, manufacturers increasingly rely on high-purity desiccant solutions. Growing investments in biopharmaceuticals and emerging-market healthcare distribution further accelerate demand. This positions pharmaceuticals as the most dynamic application category in the forecast period.

Regional Insights

North America Desiccants Market Trends

North America is projected to capture approximately 28% of the desiccants market share by 2026. This dominant position stems from robust demand within the pharmaceutical, electronics, and industrial manufacturing sectors. The United States drives regional consumption through advanced production capabilities and stringent safety regulations. Manufacturers in this region increasingly adopt specialized moisture-control solutions to protect high-purity healthcare packaging and semiconductor components. The rise of automation in warehouses and logistics networks further amplifies the need for reliable humidity management. A stable regulatory environment encourages quality compliance, prompting organizations to integrate performance-driven materials into their operations. This systemic focus on precision ensures that the region remains a pivotal hub for high-value applications.

Innovation-driven suppliers are essential to this market development as they invest heavily in recyclable packaging and regenerable technologies. The expansion of e-commerce, medical supply chains, and precision component manufacturing reinforces continuous demand for efficient industrial drying systems. Facilities are upgrading their infrastructure, which heightens the necessity for effective moisture-barrier protections across the entire value chain. Simultaneously, the adoption of environmentally responsible inputs aligns with tightening sustainability mandates. These factors collectively solidify North America’s status as a primary contributor to global revenue streams, positioning the region at the forefront of sustainable and technological advancement.

Europe Desiccants Market Trends

Europe is poised to secure approximately 25% of the global market share in 2026. This robust positioning stems from mature manufacturing sectors and rigorous quality assurance standards. Economic powerhouses such as Germany, France, and the United Kingdom are driving this regional momentum through their advanced automotive, chemical, and pharmaceutical industries. Strict European Union (EU) regulations regarding product safety compel organizations to adopt superior desiccant solutions. Consequently, the sector is witnessing a distinct shift toward recyclable and low-toxicity materials. These inputs are becoming critical for stakeholders who manage risks within food safety and medical supply chains. By utilizing precision moisture-control systems, high-value manufacturers strengthen their operational resilience against environmental variables.

A structured policy framework is simultaneously encouraging the adoption of sustainable and regenerable technologies. Manufacturers are responding to these incentives by increasing their investments in clean materials and energy-efficient drying systems. This regulatory pressure fosters a competitive environment that drives continuous innovation in performance and design. Suppliers are actively integrating circular economy principles into their waste-management strategies to meet these evolving expectations. Such initiatives allow companies to align their product development cycles with broader environmental mandates. Ultimately, these factors support a consistent expansion trajectory that balances industrial output with ecological responsibility.

Asia Pacific Desiccants Market Trends

Asia Pacific is forecast to capture approximately 35% of the desiccants market share by 2026, establishing the region as the global leader. This dominance is fueled by large-scale manufacturing activities in China, Japan, India, and ASEAN countries. The region’s export-driven industries, including electronics, pharmaceuticals, automotive components, and chemicals, require reliable, high-performance desiccants to protect moisture-sensitive products. Innovations such as those demonstrated by Multisorb Technologies at CPHI & PMEC India 2025 highlight the region’s commitment to adopting advanced moisture-control solutions, particularly in pharmaceutical and nutraceutical sectors. China’s electronics manufacturing ecosystem remains a key consumption driver, with widespread use of silica gel, clay, and molecular sieves. Expansion in food processing and pharmaceutical production further accelerates desiccant adoption, while cost advantages in manufacturing bolster regional supply chain competitiveness.

The Asia Pacific desiccants market is also projected to grow at a CAGR of 9.8%, making it the fastest-growing regional market for the 2026-2033 forecast period. Stricter compliance standards for drug quality, food safety, and export certification are accelerating the uptake of advanced desiccant technologies. Japan’s precision manufacturing and India’s expanding pharmaceutical sector are critical growth engines. Investments in logistics, warehousing, and automation are increasing demand for desiccants across industrial and packaging applications. Continuous improvements in industrial infrastructure and regulatory frameworks further elevate the region’s global standing. The integration of innovative, high-efficiency desiccants is expected to sustain strong market momentum through 2033, reinforcing Asia Pacific’s leadership in the desiccants industry.

Competitive Landscape

The global desiccants market structure remains moderately fragmented, and large suppliers such as Clariant, Multisorb Technologies, Evonik, BASF, and W. R. Grace capture a meaningful portion of industry revenue. These companies compete through broad product ranges, resilient international distribution, and steady investment in high-purity adsorbent materials that meet regulatory expectations. They also strengthen differentiation by prioritizing sustainability and performance in demanding end uses, such as pharmaceuticals, electronics, and protective packaging.

At the same time, regional and niche manufacturers such as Sorbead India, OhE Chemicals, Trockenmittel Deutschland, and Desicca Chemicals continue to win business with cost-effective manufacturing and tailored solutions for specific operating conditions. Their local supply networks, customization capabilities, and strong position in use cases such as cargo protection, industrial drying, and food packaging help them compete effectively against multinational brands. Entry barriers remain moderate because new entrants must meet compliance obligations and prove material-processing consistency, especially where safety, traceability, and validation matter. However, technology-led differentiation is creating a clearer opening for new challengers, particularly those that combine desiccants with digital moisture-monitoring and smart packaging features.

Key Industry Developments

- In December 2025, Multisorb Technologies participated in MJBizCon 2025 at the Las Vegas Convention Center. The company showcased specialized moisture and oxygen control products for cannabis and niche packaging. The exhibition emphasized product innovation for high-value, sensitive goods. It strengthened Multisorb’s visibility in emerging and specialized packaging markets.

- In September 2025, the National Renewable Energy Laboratory (NREL) and Blue Frontier developed the Energy Storing and Efficient Air Conditioner (ESEAC) system, which leverages liquid desiccants to decouple dehumidification from cooling and reduce peak power demand by more than 90%. This solution significantly lowers electricity costs by storing energy in salt-based fluids for use during high-rate periods.

- In May 2025, Clariant was honored with the Strive 35 – Sustainability Award by ADM for outstanding supplier performance. The recognition highlighted excellence in environmental sustainability and economic delivery. It underscores Clariant’s commitment to responsible and eco-friendly desiccant production.

Companies Covered in Desiccants Market

- Clariant AG

- Multisorb Technologies

- Sanner GmbH

- W.R. Grace & Co.

- Protech Plastics

- Capitol Scientific

- Brownell Ltd

- Absortech AB

- Oker-Chemie GmbH

- Desicca Chemicals

- GeeJay Chemicals

- Trockenmittel GmbH

- CILICANT

- Drytech Industries

- Sorbead India

Frequently Asked Questions

The global desiccants market is projected to reach US$ 1.4 billion in 2026.

Increasing production of moisture-sensitive goods, stricter regulatory standards in pharmaceuticals and food packaging, and rising demand from global logistics networks that require humidity-control systems are driving the market.

Major opportunities include the expansion of sustainable and regenerable desiccant technologies, increasing adoption in pharmaceutical supply chains, and advancements in high-performance electronic packaging across Asia Pacific, North America, and Europe.

Key market participants include Clariant, Multisorb Technologies, Evonik, BASF, W. R. Grace, and Sorbead India.