- Medical Devices

- Respiratory Oxygen Delivery Devices Market

Respiratory Oxygen Delivery Devices Market Size, Share, Growth, and Regional Forecast, 2025 - 2032

Respiratory Oxygen Delivery Devices Market by Product (Oxygen Masks, Nasal Cannula, Venturi Masks, Non-rebreather Masks, Others), End-user (Hospitals, Outpatient Facilities, Home Care), and Regional Analysis from 2025 - 2032

Respiratory Oxygen Delivery Devices Market Share and Trends Analysis

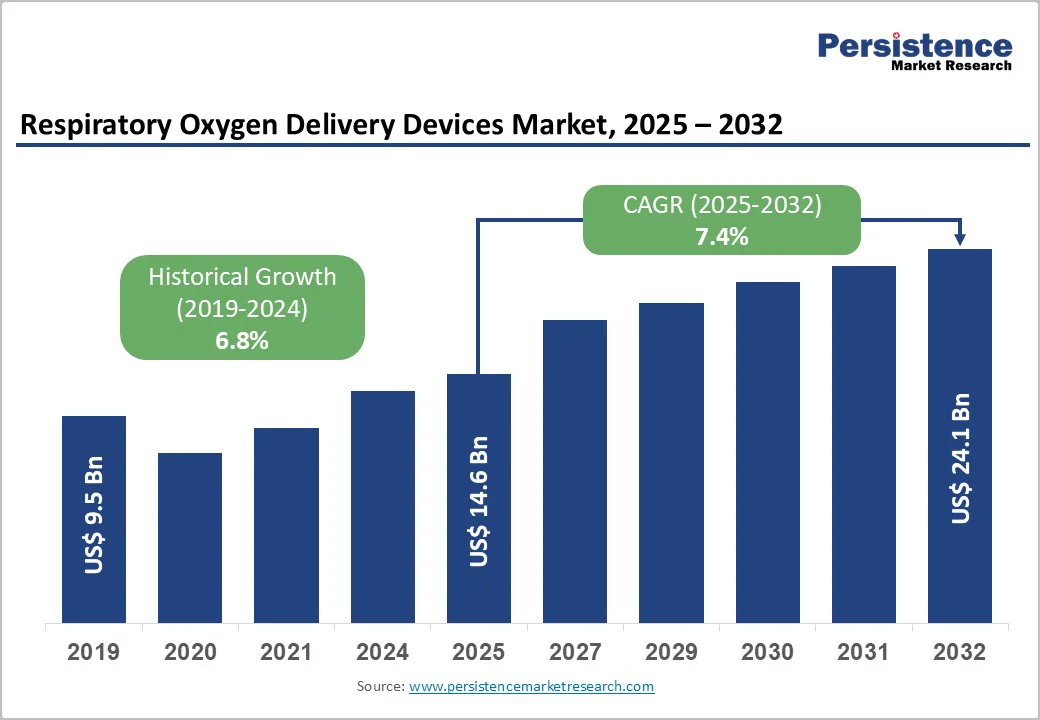

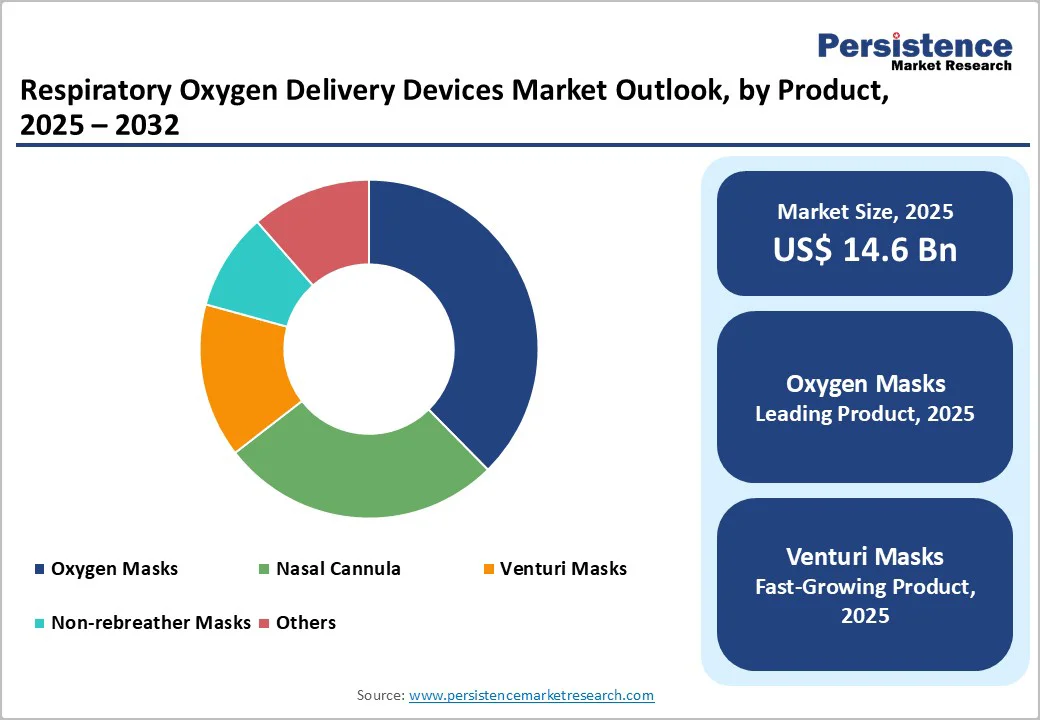

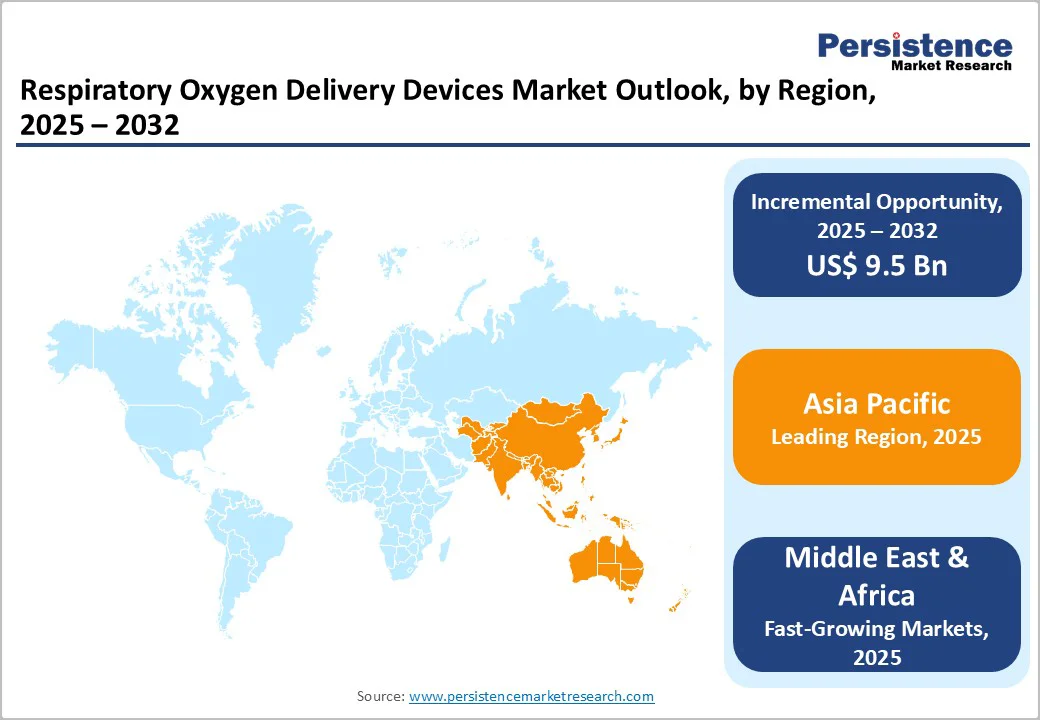

The global respiratory oxygen delivery devices market is valued at US$14.6 billion in 2025 and is projected to reach US$24.1 billion by 2032, growing at a CAGR of 7.4% from 2025 to 2032.

The global market is expanding steadily, fueled by the rising prevalence of chronic respiratory disease, the growing adoption of home healthcare, and innovations in devices such as HFCWO, PEP, and IPV systems. Hospitals, pulmonary clinics, and home care settings are increasing usage. North America leads the market due to awareness and reimbursement, while the Asia Pacific grows fastest with a larger patient base and improving healthcare access.

Key Industry Highlights:

- Leading Region: Asia Pacific, commanding 43.1% market share in 2025, driven by a rising chronic respiratory patient population, expanding healthcare access, growing homecare adoption, and increasing awareness of oxygen therapy devices.

- Fastest-Growing Region: Middle East & Africa, driven by increasing chronic respiratory disease prevalence, expanding healthcare infrastructure, rising adoption of homecare oxygen therapy, and growing awareness of advanced respiratory devices.

- Investment Plans: Europe, emphasizing R&D for innovative, connected, and patient-friendly devices, strategic partnerships, and compliance with EU MDR.

- Dominant Product: Oxygen masks, leading the market with 37.6% share in 2025, due to their efficiency in delivering controlled oxygen flow, ease of use, and widespread adoption across hospitals, clinics, and home care settings.

| Key Insights | Details |

|---|---|

|

Respiratory Oxygen Delivery Devices Market Size (2025E) |

US$14.6 Bn |

|

Market Value Forecast (2032F) |

US$24.1 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

7.4% |

|

Historical Market Growth (CAGR 2019 to 2024) |

6.8% |

Market Dynamics

Driver - Growing Home Healthcare Adoption

Growing adoption of home healthcare is strongly driving the respiratory oxygen delivery devices market. In the U.S., more than 1.5 million adults use long-term supplemental oxygen therapy at home. In France, patients using home respiratory equipment (including oxygen therapy) increased by 117% from 2006 to 2019, reaching nearly 246,000 individuals, with 139,323 on long-term home oxygen alone in 2019. This shift toward in-home care not only reduces hospital burden but also boosts demand for portable, efficient oxygen systems, making home-based therapy a growing cornerstone of the respiratory device market.

Restraints - Stringent Regulatory Compliance

Stringent regulatory compliance significantly restrains the respiratory oxygen delivery devices market. Under the EU Medical Device Regulation (MDR 2017/745), manufacturers must establish comprehensive post-market surveillance (PMS) systems and continuously conduct post-market clinical follow-up (PMCF) as part of their technical documentation. The MDR also enforces rigorous clinical evaluation of safety and performance, with frequent updates to the clinical evaluation report. Non-compliance has serious consequences: the U.S. FDA issued a warning to a leading oxygen concentrator maker for failing to investigate approximately 10% (2,589 of 25,777) of customer complaints. These regulatory demands, spanning risk management, quality systems, clinical evidence, and vigilant post-market monitoring, raise development costs and delay product launches, particularly burdening smaller or newer companies.

Opportunity - Rising Telehealth and Remote Patient Monitoring

Rising telehealth and remote patient monitoring (RPM) are significant opportunities for the respiratory oxygen delivery devices market. In the U.S., Medicare now reimburses RPM services, allowing connected pulse oximeters and oxygen devices to transmit real-time data to healthcare providers. Between 2019 and 2023, RPM usage grew by over 3,300%, with more than 5.5 million services delivered. Programs like the Mayo Clinic’s RPM initiative, involving over 7,000 COVID-19 patients, reported 78.9% engagement, with low hospitalization (9.4%) and emergency visit (11.4%) rates.

For chronic respiratory patients on home oxygen, RPM enables continuous monitoring of oxygen saturation, early detection of complications, and timely interventions. This integration of telehealth with oxygen therapy devices enhances patient outcomes, reduces hospital visits, and drives demand for smart, connected oxygen delivery systems, making it a key growth avenue for the market.

Category-wise Analysis

By Product, Oxygen Masks dominate the Respiratory Oxygen Delivery Devices Market.

Oxygen masks dominate the market with a 36.7% share in 2025, due to their ability to provide higher and more controlled oxygen concentrations than nasal cannulas. They can deliver up to 60–80% oxygen depending on the type, making them ideal for patients with severe hypoxemia or acute respiratory distress. Masks, including simple, venturi, and non-rebreather types, are widely used in hospitals, emergency rooms, and home care for patients requiring precise oxygen delivery. Their versatility allows use across critical care, surgery, and chronic respiratory management, contributing to broad adoption. Additionally, oxygen masks reduce the risk of inadequate oxygenation in patients compared to low-flow devices, ensuring effective treatment. High demand in institutional settings, combined with ease of use and clinical preference, drives their market dominance over other oxygen delivery products.

By End-user, Hospitals are gaining traction due to high patient demand and advanced infrastructur.e

Hospitals dominate the respiratory oxygen delivery devices market because they treat the largest number of patients requiring continuous, high-flow, or emergency oxygen therapy. In critical care units, emergency departments, and surgical wards, oxygen is routinely administered to manage hypoxemia, respiratory distress, and post-operative recovery. Hospitals have the infrastructure, trained staff, and resources to maintain and operate a wide range of oxygen delivery devices, including masks, nasal cannulas, and high-flow systems.

The high patient turnover and diverse clinical needs create sustained demand for these devices. Additionally, hospitals invest in advanced monitoring and oxygen-delivery technologies to ensure precise treatment, improve patient outcomes, and reduce complications, thereby reinforcing their position as the largest end-user segment in the respiratory oxygen-delivery devices market.

Regional Insights

Asia Pacific Respiratory Oxygen Delivery Devices Market Trends

Asia Pacific dominates the respiratory oxygen delivery devices market, with a 43.1% share in 2025, driven by a large and growing population of patients with chronic respiratory diseases. China alone has nearly 100 million people with COPD, accounting for approximately 25% of global cases. Epidemiological surveys across Asia report a COPD prevalence of around 6.2% in the adult population. Asthma prevalence in the region ranges from 0.7% to 32.8% across countries, further expanding the patient base.

Contributing factors include widespread air pollution, high smoking rates, and occupational exposures, which increase respiratory disease incidence. Rapid urbanization, improved healthcare infrastructure, and expanding access to primary and specialty care boost device adoption. Governments and healthcare providers are increasingly supporting home care and portable oxygen solutions. The combination of a large patient population, rising disease prevalence, and expanding healthcare access establishes Asia Pacific as the leading market for respiratory oxygen delivery devices.

North America Respiratory Oxygen Delivery Devices Market Trends

North America is one of the fastest-growing regions in the respiratory oxygen delivery devices market, driven by the high prevalence of chronic respiratory diseases and a well-developed healthcare system. In the United States, over 15 million adults are diagnosed with COPD, and chronic lower respiratory diseases cause more than 145,000 deaths annually. Additionally, more than 1.5 million Americans use long-term supplemental oxygen, reflecting sustained demand for respiratory devices.

The region benefits from advanced hospital infrastructure, widespread adoption of home healthcare, and favorable reimbursement policies for durable medical equipment, including oxygen delivery systems. High awareness among patients and healthcare providers, coupled with strong investment in healthcare technology, supports rapid adoption of portable, efficient, and connected oxygen devices, driving North America’s position as a fast-growing market in this sector.

Europe Respiratory Oxygen Delivery Devices Market Trends

Europe is an important region in the respiratory oxygen delivery devices market due to its high burden of chronic respiratory diseases. About 81.7 million people in the WHO European Region live with conditions such as COPD and asthma, representing a major public health concern. Environmental risk factors, including air pollution and occupational exposures, contribute to over 35% of CRD-related deaths in the region. The economic impact is also substantial: the European Union spends approximately €38.6 billion annually on COPD alone, accounting for more than half of total respiratory disease costs. This combination of high disease prevalence, preventable risk factors, and significant economic burden drives demand for oxygen therapy and makes Europe a strategically important market for respiratory oxygen delivery devices.

Competitive Landscape

The global respiratory oxygen delivery devices market is growing steadily, driven by rising cases of COPD, asthma, and cystic fibrosis and an increasing preference for noninvasive therapies. Hospitals and home care settings are adopting oxygen masks, nasal cannulas, and high-flow systems for improved patient outcomes. North America leads the market with a strong healthcare infrastructure, while the Asia Pacific region grows fastest due to pollution, expanding healthcare access, and rising affordability.

Key Industry Developments:

- In October 2025, Medtronic Cardiac Surgery launched the VitalFlow™ Extracorporeal Membrane Oxygenation (ECMO) system in Europe, enhancing treatment options for critically ill patients. The new system provided advanced life-support capabilities, helping hospitals manage severe cardiac and respiratory failure cases more effectively.

- In May 2025, GE HealthCare and Raydiant Oximetry accelerated innovation in fetal oxygen saturation technology, unveiling advancements to improve monitoring accuracy and maternal-fetal outcomes. The companies focused on developing noninvasive solutions to more accurately track fetal oxygen levels during pregnancy, thereby enhancing early detection of hypoxia and related complications.

- In May 2025, Medtronic received the FDA’s Safer Technologies Program (STeP) designation for its investigational Nellcor™ pulse oximetry technology, recognizing its potential to improve patient safety. The designation allowed Medtronic to expedite development and regulatory review, aiming to bring advanced oxygen monitoring solutions to clinical settings more quickly.

Companies Covered in Respiratory Oxygen Delivery Devices Market

- GE Healthcare

- Koninklijke Philips N.V.

- ICU Medical (Smiths Medical)

- Invacare Corporation

- Medtronic

- Fisher & Paykel Healthcare

- ResMed

- Linde

- Mindray

- Chart Industries

- Drägerwerk AG & Co. KGaA

- DeVilbiss Healthcare

- Others

Frequently Asked Questions

The global respiratory oxygen delivery devices market is projected to be valued at US$ 14.6 Bn in 2025.

Rising chronic respiratory diseases, growing homecare adoption, technological advancements, increasing patient awareness, and expanding hospital and clinical infrastructure drive market growth.

The global respiratory oxygen delivery devices market is poised to witness a CAGR of 7.4% between 2025 and 2032.

Expanding homecare, telehealth integration, aging population, emerging markets, and development of smart, portable, and patient-friendly oxygen delivery devices offer key opportunities.

GE Healthcare, Koninklijke Philips N.V., ICU Medical (Smiths Medical), Invacare Corporation, Medtronic, Fisher & Paykel Healthcare.