- Pharmaceuticals

- Respiratory Distress Syndrome (RDS) Market

Respiratory Distress Syndrome (RDS) Market Size, Share, and Growth Forecast, 2026 - 2033

Respiratory Distress Syndrome (RDS) Market by Condition Type (Neonatal Respiratory Distress Syndrome (NRDS), Acute Respiratory Distress Syndrome (ARDS)), Route of Administration (Oral, Injectable, Nasal), End-User (Hospitals, Specialty Clinics, Others), and Regional Analysis for 2026 - 2033

Respiratory Distress Syndrome (RDS) Market Share and Trends Analysis

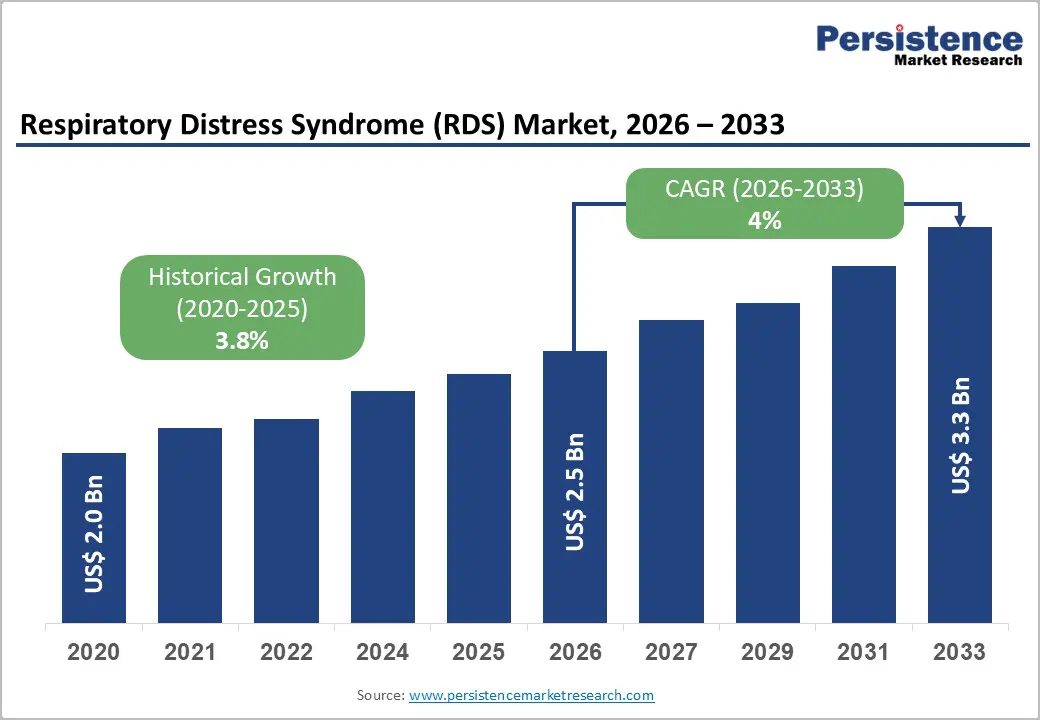

The global respiratory distress syndrome (RDS) market size is likely to be valued at US$ 2.5 billion in 2026, and is projected to reach US$ 3.3 billion by 2033, growing at a CAGR of 4.0% during the forecast period 2026−2033. The market demonstrates steady and structurally resilient growth, supported by the persistent global burden of acute and neonatal respiratory disorders, expanding critical care infrastructure, and continuous clinical innovation in respiratory therapeutics.

Rising preterm birth incidence, increasing intensive care unit (ICU) admissions, and higher survival rates among critically ill patients are strengthening the long-term demand for RDS management solutions. Healthcare systems globally are prioritizing early diagnosis, standardized treatment protocols, and improved drug delivery methods, reinforcing consistent adoption across hospital settings.

Key Industry Highlights

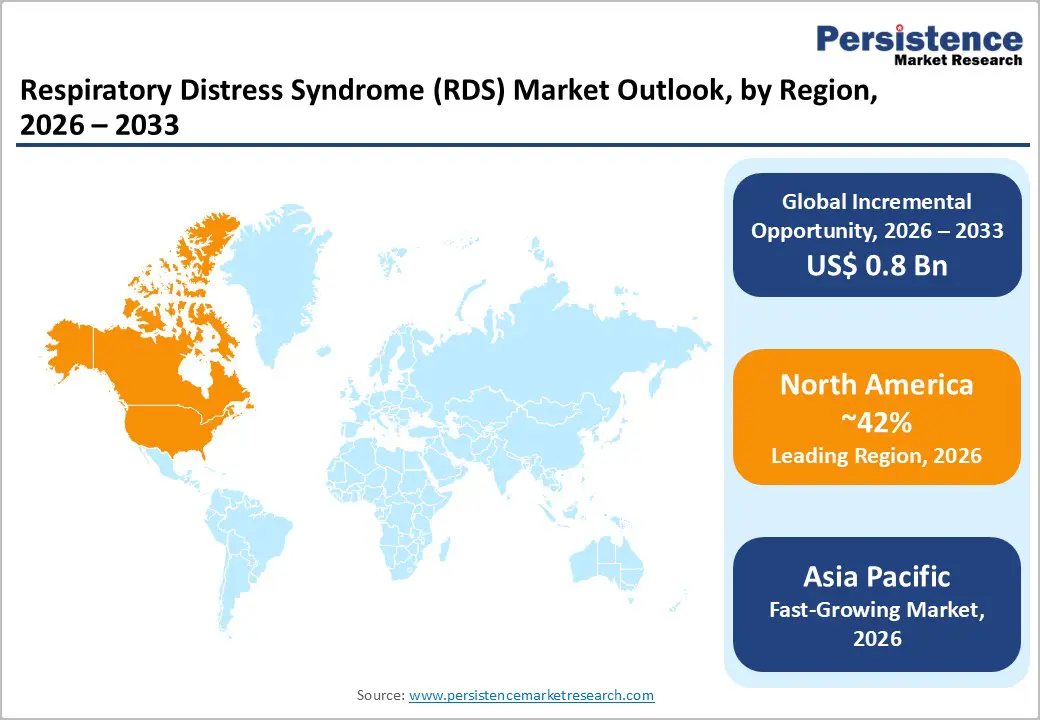

- Dominant Region: North America is predicted to hold a 42% market share in 2026, powered by advanced healthcare infrastructure and rapid adoption of innovative respiratory therapies.

- Fastest-growing Regional Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, driven by expanding neonatal and critical care infrastructure.

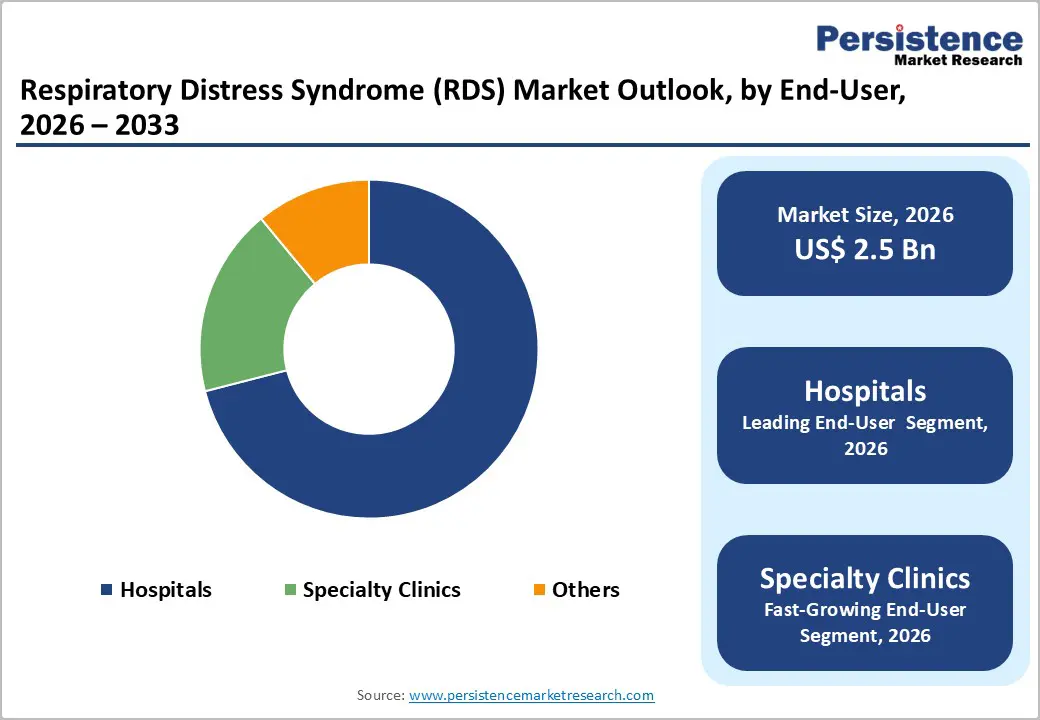

- Leading End-User: Hospitals are likely to lead with about 71% market share in 2026 due to ICU-focused care, advanced diagnostics, and high patient acuity.

- Fastest-growing End-User: Specialty clinics are slated to grow the fastest through 2033, owing to expanded referral networks, outpatient monitoring, and enhanced post-acute respiratory care services.

- January 2025: InflaRx’s GOHIBIC (vilobelimab) received marketing authorization under exceptional circumstances from the European Commission to treat adult patients with COVID?induced ARDS.

| Key Insights | Details |

|---|---|

|

Respiratory Distress Syndrome (RDS) Market Size (2026E) |

US$ 2.5 Bn |

|

Market Value Forecast (2033F) |

US$ 3.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Incidence of Risk Factors and Underlying Conditions

The increasing incidence of key risk factors and underlying health conditions is driving demand significantly as patients with more complex clinical profiles require heightened respiratory support and early intervention. Trends in public health reveal that about 1 in 10 babies worldwide are born prematurely, which translates to a substantial global burden of respiratory complications, including breathing failure and distress immediately after birth. This sustained level of preterm births highlights persistent vulnerability in newborn health despite broader medical advances, and it intensifies reliance on specialized care pathways. In parallel, lifestyle-associated conditions such as metabolic disease, poor maternal health, and environmental stressors elevate risk profiles at all ages, increasing acute episodes that stress acute and critical care infrastructure.

Health systems are adapting to these evolving clinical burdens by prioritizing enhanced diagnostics, ventilatory technology investments, and intensive care capacity expansion. A larger share of patients presenting with chronic conditions such as diabetes, cardiovascular disease, or chronic respiratory illness escalates severity at admission, prompting earlier initiation of advanced therapy and prolonged care cycles. Payers and providers are aligning resources toward models that emphasize improved outcomes through early stabilization, reduced complication rates, and efficient resource utilization.

Clinical Complexity and Risk of Treatment-Related Complications

Clinical complexity and the risk of treatment-related complications restrain expansion as care pathways involve high-stakes interventions delivered in fragile clinical settings. Management relies on precise timing, dose control, and constant physiological monitoring, while patients often present with unstable lung mechanics and systemic vulnerability. Therapies such as surfactant replacement, positive airway pressure, and invasive ventilation require advanced infrastructure and specialized clinicians, raising execution risk when resources or expertise vary across hospitals. This environment elevates exposure to adverse outcomes such as lung overdistension, oxygen toxicity, and infection, reinforcing cautious adoption of advanced therapeutic solutions within healthcare systems focused on risk containment and cost control.

Treatment-related complications influence purchasing decisions and care protocols through their impact on outcomes, length of stay, and liability. Persistent complication rates signal operational and clinical uncertainty despite technological progress. Evidence from the Chinese Neonatal Network shows that in 2025, mortality among preterm infants declined to 4.6%, while serious complications such as bronchopulmonary dysplasia remained at 35.0%, highlighting the enduring burden linked to intensive respiratory interventions. This imbalance between survival gains and complication prevalence sustains conservative clinical behavior, slower protocol standardization, and restrained investment momentum in high-risk treatment modalities.

Expansion of Neonatal Care Infrastructure in Emerging Economies

Steady improvements in neonatal care infrastructure in emerging economies represents a critical opportunity for effective management of respiratory distress syndrome, as it directly addresses long-standing gaps in early-life critical care. Many of these regions face high rates of preterm births combined with historically limited access to advanced neonatal facilities. Strengthening infrastructure improves availability of neonatal intensive care units, respiratory support systems, surfactant administration capabilities, and skilled clinical teams. This shift enables timely diagnosis and standardized treatment pathways, reducing clinical variability and improving outcomes.

Infrastructure expansion also aligns with broader healthcare modernization agendas pursued by governments and private providers in emerging economies. Investments in neonatal care facilities create long-term system value through workforce development, technology adoption, and integration of evidence-based protocols. Improved capacity encourages adoption of advanced respiratory therapies, drives procurement of specialized devices, and supports partnerships with global medical technology providers. These developments transform neonatal care from a reactive service into a structured, high-value clinical domain. For stakeholders, this environment supports sustained demand, predictable utilization, and scalable deployment of RDS-related solutions.

Category-wise Analysis

Condition Type Insights

Neonatal RDS is likely to be the leading segment with a projected 58% of the revenue share in 2026 due to its high treatment dependency, well-established clinical pathways, and universal adoption of standardized surfactant therapy across neonatal intensive care units (NICUs). Immediate intervention requirements drive higher per-patient drug consumption, prolonged hospitalization, and intensive monitoring, resulting in elevated care costs. Consistent incidence of preterm births and strong prioritization of neonatal survival within healthcare systems reinforce sustained utilization. Structured reimbursement frameworks and protocol-driven care further strengthen revenue visibility and segment leadership.

Acute respiratory distress syndrome is anticipated to be the fastest-growing segment from 2026 to 2033, fueled by increasing intensive care admissions among aging populations and a rising burden of infection-related respiratory failure. Expanding critical care capacity and improved adult survival outcomes encourage broader deployment of advanced respiratory support and pharmacological interventions. Greater clinical awareness and protocol optimization across hospitals support higher diagnosis rates and treatment adoption.

Route of Administration Insights

Injectable therapies are anticipated to secure around 62% of the respiratory distress syndrome market revenue share in 2026, reflecting their critical role in frontline respiratory care where speed, dosing precision, and systemic effectiveness determine clinical outcomes. These therapies integrate seamlessly into intensive care workflows, allowing controlled administration for mechanically ventilated and high-risk patients. Established reimbursement frameworks, clinician familiarity, and broad regulatory acceptance support sustained usage. High reliance on injectable surfactants and supportive agents drives repeat utilization, while extended inpatient treatment durations increase per-case value and reinforce dominance across hospital settings.

Nasal administration is expected to be the fastest-growing segment during the 2026–2033 forecast period, propelled by rising emphasis on non-invasive therapeutic approaches and patient safety within respiratory care. Nasal delivery reduces procedural burden, minimizes ventilation-related complications, and supports earlier intervention protocols. Advances in formulation science and delivery devices improve absorption efficiency and dosing reliability, increasing clinical confidence. Expanding application in early-stage treatment and step-down care environments sustains growth momentum across diverse care settings.

End-User Insights

Hospitals are poised to dominate with a forecasted RDS market share of 71% in 2026, powered by the ICU-centric nature of disease management, advanced diagnostic capabilities, and stringent regulatory compliance requirements. High patient acuity and the need for continuous monitoring concentrate treatment within hospital environments, where multidisciplinary teams and specialized equipment enable rapid intervention. Longer inpatient stays and complex care protocols further reinforce revenue concentration, making hospitals the primary end-user segment for critical RDS therapies and associated clinical services.

Specialty clinics are estimated to be the fastest-growing segment from 2026 to 2033, fueled by expanded referral networks, outpatient respiratory monitoring, and increasing post-acute care services. Clinics are increasingly equipped to manage stable or recovering patients, reducing hospital burden and supporting continuity of care. Investment in specialized respiratory expertise, advanced diagnostic tools, and remote monitoring capabilities enhances service efficiency and supports greater patient throughput across diverse care pathways.

Regional Insights

North America Respiratory Distress Syndrome (RDS) Market Trends

North America is expected to dominate with an estimated 42% of the respiratory distress syndrome market share in 2026, reflecting advanced healthcare infrastructure, concentration of specialized neonatal and adult intensive care units, and strong regulatory support for rapid adoption of innovative respiratory therapies. The regional market benefits from state-of-the-art hospital networks and high clinician expertise, enabling immediate intervention for both neonatal and acute respiratory distress cases. High prevalence of preterm births and chronic respiratory conditions sustains demand for surfactants, ventilators, and non-invasive respiratory support.

Key factors driving North America dominance include robust R&D investments and the presence of major global medical device and pharmaceutical companies focusing on respiratory therapeutics. Clinical expertise in NICUs and adult ICUs facilitates rapid deployment of conventional and emerging treatment modalities. Strategic collaborations among hospitals, research institutions, and technology providers foster continuous innovation in surfactant formulations, ventilation devices, and non-invasive delivery systems. Established patient referral networks and high awareness among healthcare providers support timely diagnosis and intervention across critical care settings.

Europe Respiratory Distress Syndrome (RDS) Market Trends

Europe is predicted to hold a significant position in the RDS market landscape through 2033, supported by well-established healthcare infrastructure, advanced neonatal and adult critical care units, and strong regulatory frameworks that ensure timely access to innovative respiratory therapies. Widespread adoption of standardized treatment protocols, including surfactant therapy and non-invasive ventilation, contributes to consistent market utilization. High awareness among healthcare providers, coupled with structured reimbursement policies across major countries, supports extensive clinical adoption. Continuous investment in hospital capacity, ICU expansion, and staff training reinforces Europe as a stable contributor in the respiratory distress syndrome market expansion.

Strong implementation of digital health solutions for patient monitoring and early diagnosis enhances treatment efficiency and clinical outcomes. Partnerships among hospitals, research centers, and medical device manufacturers promote innovation and support deployment of advanced ventilators and respiratory support equipment. Well-developed public health initiatives focusing on neonatal care and adult critical care enable timely intervention and adherence to standardized treatment protocols. Comprehensive access to private and public healthcare services ensures wider coverage and consistent adoption of respiratory therapies across the regional market.

Asia Pacific Respiratory Distress Syndrome (RDS) Market Trends

Asia Pacific is forecasted to be the fastest-growing regional market for respiratory distress syndrome between 2026 and 2033, stimulated by rapid expansion of neonatal and critical care infrastructure and increasing investments in advanced respiratory technologies. Governments across several countries are prioritizing the development of high-dependency care units to address rising preterm birth rates and growing prevalence of infection-related respiratory failure. Private healthcare providers are simultaneously upgrading hospitals with modern ventilators, surfactant therapies, and non-invasive respiratory support devices, enhancing access to timely intervention. Expanding urban healthcare networks and rising affordability due to insurance penetration further support market adoption.

Key factors driving this growth include strategic public-private partnerships aimed at scaling neonatal and adult critical care services and implementation of evidence-based protocols to reduce infant and adult mortality rates. Technological adoption is supported by local manufacturing of surfactants and ventilatory equipment, reducing cost barriers and improving supply chain efficiency. Regional focus on training specialized respiratory care personnel and increasing awareness of early intervention for high-risk neonates and adults contributes to higher treatment uptake.

Competitive Landscape

The global respiratory distress syndrome market structure is moderately consolidated. The top five companies – AbbVie Inc., Pfizer Inc., AstraZeneca, Sanofi, and Novartis AG – account for about 60% of the global revenue. These leaders dominate through proven neonatal surfactant therapies and extensive global distribution networks. Their strong research & development (R&D) capabilities, regulatory expertise, and broad market presence allow them to sustain leadership in both mature and emerging regions. Strategic investments in clinical trials and next-generation formulations help these organizations maintain a competitive edge, ensuring continued adoption of their therapies in diverse healthcare settings.

Mid-sized and inchoate firms contribute to the market by focusing on delivery innovation and regional expansion. These organizations prioritize the development of non-invasive administration methods, advanced dosing systems, and cost-effective solutions to improve patient access in underserved areas. Their efforts to enter new geographies and collaborate with local healthcare providers foster broader market growth and address unmet needs in regions with limited resources. By combining innovative approaches with targeted outreach, these companies play a vital role in advancing treatment options and supporting the overall evolution of respiratory distress syndrome care.

Key Industry Developments

- In December 2025, a retrospective cohort study showed that higher neonatal Sequential Organ Failure Assessment (nSOFA) scores within the first 24?hours of NICU admission were linked to an increased likelihood of prolonged mechanical ventilation in infants with respiratory distress syndrome.

- In September 2025, researchers at the Institute of Science Tokyo discovered that basophils, rare white blood cells comprising 0.5 to 1% of circulating immune cells, promote recovery from acute RDS by releasing interleukin-4 (IL-4), which suppresses inflammatory neutrophils and reduces lung tissue damage. The study found that IL-4 turns off pro-inflammatory genes in neutrophils, suggesting that targeting the basophil–IL-4–neutrophil pathway could offer a new therapeutic approach for ARDS.

- In June 2025, the U.S. Food and Drug Administration (FDA) granted Fast Track designation to BioAegis Therapeutics’ lead candidate recombinant human plasma gelsolin (rhu?pGSN) to accelerate the development of a potential treatment for acute respiratory distress syndrome.

Companies Covered in Respiratory Distress Syndrome (RDS) Market

- AbbVie Inc.

- Pfizer Inc.

- CHIESI ESPAÑA S.A.U

- AstraZeneca

- Sanofi

- Novartis AG

- GSK plc.

- Bayer AG

- Teva Pharmaceutical Industries Ltd

Frequently Asked Questions

The global respiratory distress syndrome (RDS) market is projected to reach US$ 2.5 billion in 2026.

Rising prevalence of preterm births, increasing ICU admissions, and growing adoption of advanced respiratory therapies drive the market.

The market is poised to witness a CAGR of 4% from 2026 to 2033.

Expansion of neonatal and critical care infrastructure in emerging economies and adoption of non-invasive respiratory therapies present key market opportunities.

Key players in the market include AbbVie Inc., Pfizer Inc., CHIESI ESPAÑA S.A.U, AstraZeneca, Sanofi, and Novartis AG.