- Medical Devices

- Molecular Respiratory Panels Market

Molecular Respiratory Panels Market Size, Share, and Growth Forecast, 2026 - 2033

Molecular Respiratory Panels Market by Panel Type (Multiplex, Syndromic, Targeted), Usage (Diagnostic, Research), End-User (Hospital, Diagnostic Centers, Home Healthcare), and Regional Analysis for 2026-2033

Molecular Respiratory Panels Market Share and Trends Analysis

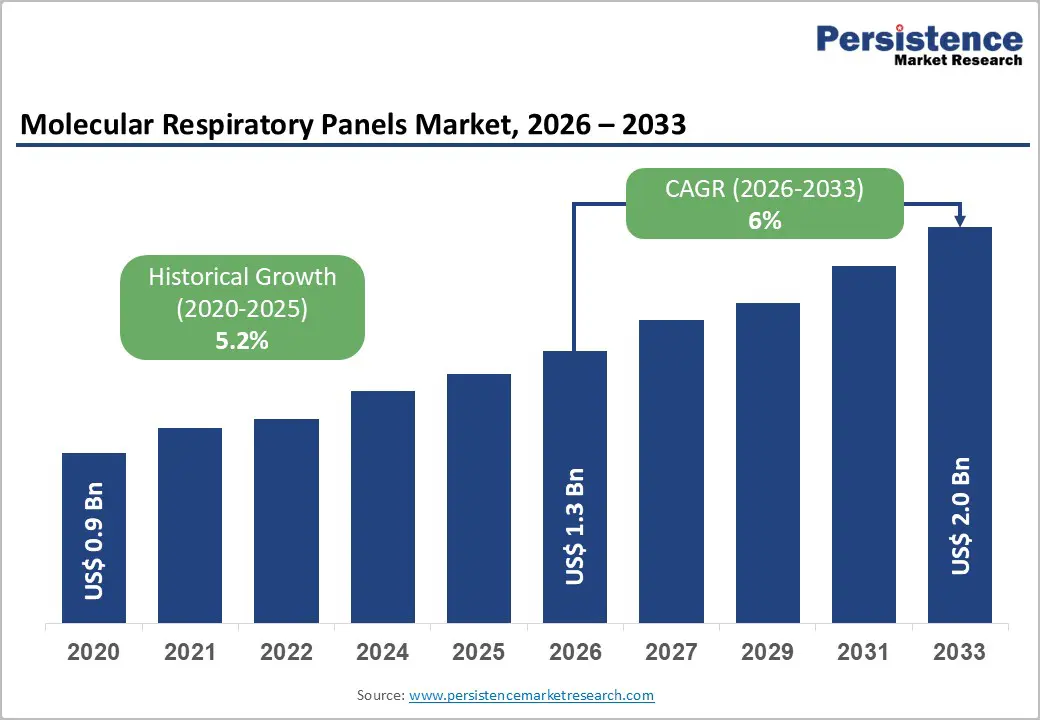

The global molecular respiratory panels market size is likely to be valued at US$ 1.3 billion in 2026, and is projected to reach US$ 2.0 billion by 2033, growing at a CAGR of 6% during the forecast period 2026−2033. Growth is being shaped by the transition of the market from pandemic-driven surges to structurally sustained demand anchored in chronic respiratory disease management and broader adoption of multiplex molecular diagnostics.

Healthcare systems are continuing to integrate respiratory panels into routine clinical workflows for conditions such as influenza, respiratory syncytial virus, and other viral and bacterial infections. Ongoing post-COVID-19 surveillance programs are maintaining elevated testing volumes, while improved laboratory automation is increasing throughput and operational efficiency across hospital and reference laboratory settings. Digital connectivity within healthcare delivery is further amplifying diagnostic reach and decision-making speed. Corporate wellness initiatives are expanding occupational health screening programs, creating incremental demand beyond traditional hospital environments. Artificial intelligence (AI)-enabled digital auscultation tools are improving triage accuracy by reducing false positives and accelerating referral pathways for confirmatory testing. Home-based and decentralized care models are also gaining traction, allowing testing to move closer to patients and easing pressure on centralized facilities.

Key Industry Highlights

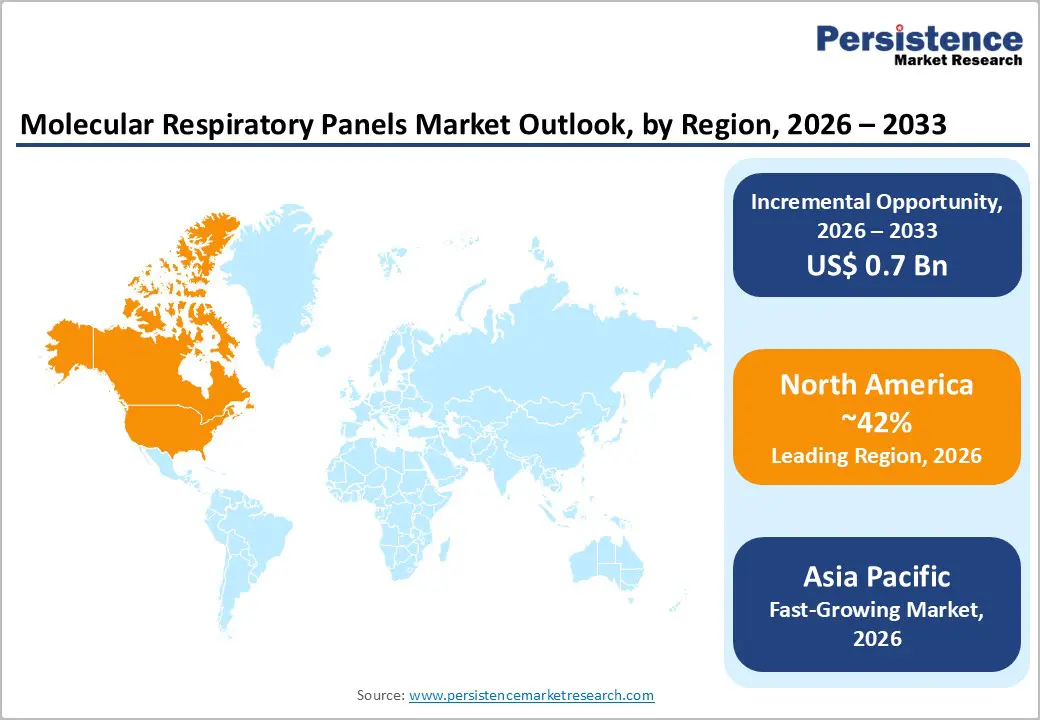

- Dominant Region: North America is expected to command about 42% market share in 2026, supported by the widespread adoption of sophisticated diagnostic technologies.

- Fastest-growing Market: The Asia Pacific market is set to be the fastest-growing through 2033, owing to the healthcare infrastructure modernization.

- Leading & Fastest-growing Panel Type: Multiplex panels are likely to hold around 48.7% of revenue share in 2026, while syndromic panels are likely to be the fastest-growing segment during the 2026-2033 forecast period.

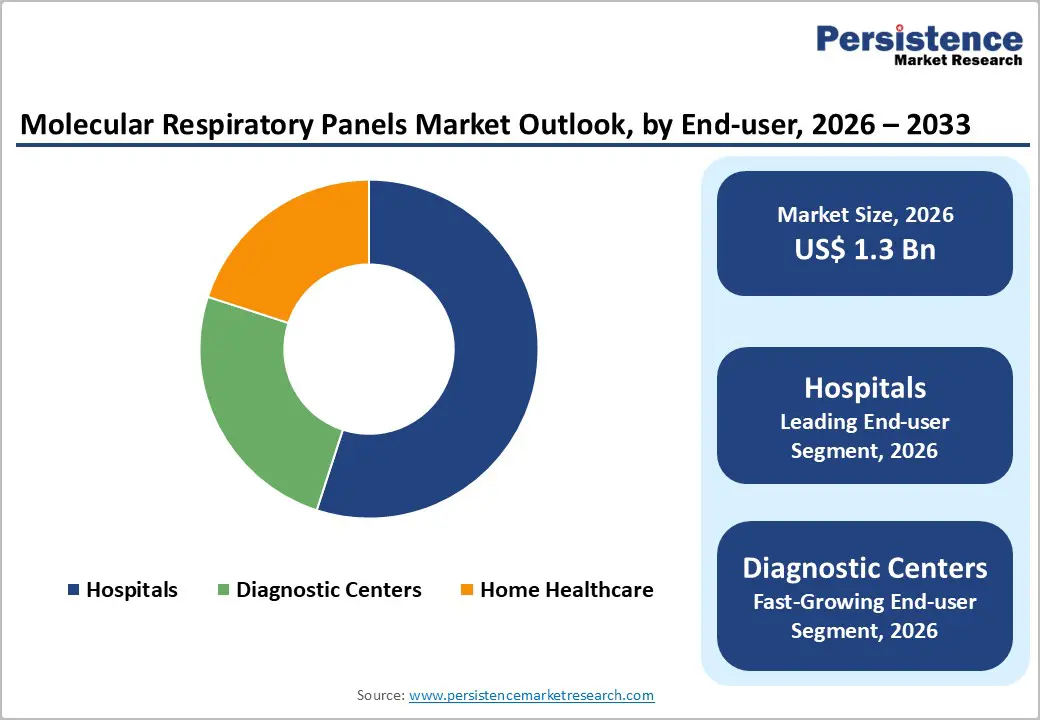

- End-User Dynamics: Hospitals are poised to dominate with an approximate 55% revenue share in 2026, with diagnostic centers recording the highest CAGR from 2026 to 2033.

- January 2026: Cytespace Africa Laboratories tripled its molecular testing capacity by installing multiple Roche cobas® 5800 systems, supporting high-volume automated polymerase chain reaction (PCR) testing.

| Key Insights | Details |

|---|---|

| Molecular Respiratory Panels Market Size (2026E) | US$ 1.3 Bn |

| Market Value Forecast (2033F) | US$ 2.0 Bn |

| Projected Growth (CAGR 2026 to 2033) | 6% |

| Historical Market Growth (CAGR 2020 to 2025) | 5.2% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growing Prevalence of Respiratory Infections Driving Diagnostic Demand

The rising global incidence of respiratory infections is aiding the steady expansion of the molecular respiratory panels market. Healthcare providers are increasingly adopting comprehensive diagnostic platforms to manage diverse viral and bacterial pathogens with greater clinical precision. Public health agencies are reporting sustained case volumes across multiple regions, which is reinforcing demand for rapid and accurate molecular testing systems. Seasonal infection waves are placing additional pressure on hospitals and outpatient facilities, particularly during peak influenza periods. As a result, medical institutions are prioritizing multiplex diagnostic capabilities that can detect multiple pathogens in a single test, enabling faster clinical decisions and more efficient allocation of treatment resources.

The COVID-19 pandemic has permanently transformed respiratory diagnostics by accelerating the establishment of robust surveillance infrastructure worldwide. Health systems have invested significantly in laboratory capacity and digital reporting networks that support simultaneous detection of pathogens such as severe acute respiratory syndrome coronavirus 2 (SARS-CoV-2), influenza, and respiratory syncytial virus (RSV). These systems are continuing to sustain elevated testing volumes beyond the emergency phase by supporting routine surveillance and outbreak preparedness. Clinical laboratories, emergency departments, and outpatient centers are leveraging this infrastructure to strengthen proactive pathogen monitoring and improve patient triage. Strategic integration of multiplex molecular panels is enhancing diagnostic accuracy while optimizing workflow efficiency across diverse care environments.

Regulatory Complexity and Approval Bottlenecks

Molecular respiratory panels are operating within a highly regulated environment across major global markets. Regulatory authorities are enforcing stringent approval requirements that are increasing development timelines and compliance costs. Manufacturers are conducting extensive clinical validation studies to demonstrate analytical accuracy, clinical sensitivity, and specificity across diverse patient populations and specimen types. The United States Food and Drug Administration (FDA), the European Medicines Agency (EMA), and regulatory bodies across Asia Pacific are each applying distinct approval frameworks, documentation standards, and review timelines. This fragmented regulatory landscape is requiring significant investment in regulatory strategy, quality management systems, and post-market surveillance capabilities.

Multi-target molecular panels are facing even greater complexity because each pathogen included in the assay requires independent validation and performance documentation. This requirement is extending development cycles and increasing the cost burden associated with product commercialization. Smaller diagnostic companies are encountering disproportionate challenges due to limited financial resources and regulatory expertise. In contrast, established manufacturers are leveraging prior submission experience, existing compliance infrastructure, and strong regulatory affairs teams to navigate approvals more efficiently. Strategic collaborations with specialized regulatory consultants and contract research organizations are becoming essential for emerging firms seeking to accelerate market entry and compete effectively in a highly regulated diagnostic environment.

Integration of AI for Enhanced Diagnostic Accuracy

AI and machine learning (ML) are increasingly being integrated into molecular respiratory panel platforms, unlocking measurable diagnostic improvements. These technologies are analyzing amplification curves with high precision and are detecting subtle signal variations that may indicate co-infections or emerging viral mutations. AI-driven systems are correlating pathogen detection results with patient demographics, presenting symptoms, and medical history to generate structured clinical decision support. This approach is reducing false positives associated with contamination or cross-reactivity and is improving overall test specificity. Algorithm-based signal interpretation is further enhancing sensitivity in samples with low viral loads, enabling earlier therapeutic intervention and better infection control management.

Cloud-enabled analytics platforms are extending these capabilities across distributed healthcare networks and multi-site laboratory environments. Automated quality control systems are increasing throughput and reducing manual review burdens, while integration with electronic medical records (EMR) is strengthening data continuity and traceability. This connectivity is supporting population health surveillance programs and predictive outbreak modeling by aggregating real-time diagnostic data. Remote result validation and centralized oversight are accelerating clinical workflows and improving turnaround times. Secure data-sharing frameworks are facilitating multi-center research collaborations and strengthening public health coordination. For diagnostic manufacturers and healthcare providers, AI-enabled respiratory panels are creating competitive advantages through higher analytical performance, streamlined operations, and improved patient outcome management across varied care settings.

Category-wise Analysis

Panel Type Insights

Multiplex panels are poised to dominate in 2026, commanding approximately 48.7% of the total market revenue, on account of their comprehensive pathogen coverage and operational efficiency. The segment benefits from strong adoption in hospital laboratories and emergency departments where comprehensive pathogen identification supports infection control decisions and antimicrobial stewardship programs. The research indicates multiplex testing is gaining momentum in point-of-care settings as technology miniaturization enables compact, user-friendly platforms suitable for urgent care and outpatient offices.

Syndromic panels are likely to be the fastest-growing segment during the 2026-2033 forecast period. Syndromic panels focus on symptom clusters rather than individual pathogens. They test comprehensive arrays tailored to clinical presentations such as acute respiratory distress, enabling rapid differentiation of bacterial versus viral etiologies. This approach accelerates triage decisions, curtails unnecessary antibiotic prescriptions, and enhances infection control in crowded facilities. Growth accelerates due to regulatory endorsements from bodies like the U.S. Centers for Disease Control and Prevention (CDC) and European Centre for Disease Prevention and Control (ECDC), which promote syndromic testing for outbreak surveillance.

Usage Insights

Diagnostic use is likely to represent the dominant application segment, capturing approximately 65% of the molecular respiratory panels market revenue share in 2026, driven by routine deployment in hospitals, clinical laboratories, and healthcare facilities for patient care. Clinical diagnostics encompass emergency department testing, inpatient monitoring, outpatient evaluation, and infection control surveillance. This segment benefits from established reimbursement frameworks, integration with electronic health records, and clinical pathways mandating rapid pathogen identification. The COVID-19 pandemic permanently elevated respiratory testing capacity, with healthcare systems maintaining enhanced diagnostic infrastructure for ongoing surveillance programs.

Research use is expected to be the fastest-growing application area for molecular respiratory panels over the 2026-2033 forecast period, supported by expanding public health initiatives and epidemiological monitoring programs. Government agencies including the CDC operate integrated surveillance frameworks merging SARS-CoV-2, influenza, and RSV tracking, requiring consistent molecular assay supply for wastewater analytics and sentinel site monitoring. Academic research institutions utilize molecular respiratory panels for studying pathogen evolution, antimicrobial resistance patterns, and vaccine effectiveness. Pharmaceutical companies employ these panels in clinical trials evaluating therapeutic interventions.

End-user Insights

The hospital segment is anticipated to lead with an approximate 55% of the molecular respiratory panels market share in 2026. Large hospital systems and medical centers possess the necessary infrastructure, technical expertise, and patient volumes to support high-throughput molecular testing platforms. Emergency departments prioritize rapid diagnostic capabilities for triage decisions, while intensive care units require comprehensive pathogen panels for managing critically ill patients with complex respiratory presentations. Outpatient clinics increasingly adopt compact, CLIA-waived systems enabling same-visit diagnosis and treatment decisions. Hospitals also benefit from integrated laboratory operations, established supply chains, and favorable reimbursement rates that offset higher per-test costs.

Diagnostic centers is projected to be the fastest-growing segment during the 2026-2033 forecast period. These facilities process high test volumes from multiple healthcare providers, requiring scalable platforms with batch processing capabilities. Reference laboratories serve as essential partners for community hospitals lacking in-house molecular testing capacity, providing comprehensive panel options and specialized pathogen identification. The segment is experiencing steady growth as laboratories expand syndromic testing menus and adopt automation solutions to improve operational efficiency.

Regional Insights

North America Molecular Respiratory Panels Market Trends

North America is set to command a significant portion of the molecular respiratory panel market share at an estimated 42% in 2026. The market here benefits from an advanced healthcare infrastructure that is supporting broad adoption of multiplex molecular diagnostics across hospitals, reference laboratories, and integrated delivery networks. Utilization rates are remaining high due to routine respiratory screening protocols and strong reimbursement coverage. The United States is driving regional leadership through sustained investments in research and development, public health surveillance, and laboratory modernization. Healthcare providers are prioritizing comprehensive pathogen detection to refine patient management pathways and reduce inappropriate antibiotic use. The U.S. Centers for Disease Control and Prevention (CDC) actively promotes antimicrobial stewardship programs, which is reinforcing demand for precise and rapid pathogen identification.

Regulatory authorities are facilitating innovation by maintaining structured review pathways for novel diagnostic panels. The U.S. FDA has been clearing advanced respiratory assays with increasing frequency, which is enabling timely commercialization of next-generation platforms. Leading manufacturers such as F. Hoffmann-La Roche Ltd., bioMérieux SA, Becton, Dickinson and Company, Thermo Fisher Scientific Inc., and QIAGEN N.V. are leveraging established distribution networks and strong clinical partnerships to maintain competitive positioning. Expansion of point-of-care testing is creating new demand across ambulatory care centers, urgent care facilities, and retail clinics. Companies are investing in portable and user-friendly platforms that are supporting decentralized testing models and improving access to rapid diagnostics across diverse healthcare settings.

Europe Molecular Respiratory Panels Market Trends

Europe is slated to hold the second-largest share of the market for molecular respiratory panels in 2026, supported by mature healthcare systems and structured public health frameworks. Countries such as Germany, the U.K., France, and Spain are driving regional demand through coordinated respiratory surveillance programs and standardized diagnostic pathways. Universal healthcare coverage across most member states is ensuring broad patient access to molecular testing services. Centralized laboratory networks are enabling efficient deployment of multiplex panels across hospitals, community clinics, and specialized centers. Demographic trends are further strengthening demand, as aging populations are requiring proactive monitoring for respiratory infections and associated complications. Seasonal virus circulation and occupational health mandates are sustaining routine testing volumes, particularly among healthcare workers and high-risk populations.

The European Union (EU) In Vitro Diagnostic Regulation (IVDR) is harmonizing regulatory standards across member states and is reinforcing quality, safety, and performance requirements for diagnostic assays. This regulatory alignment is enabling smoother cross-border commercialization for compliant manufacturers while raising entry barriers for smaller competitors. Established companies such as bioMérieux SA and QIAGEN N.V. are maintaining strong competitive positions through regional manufacturing presence and extensive clinical partnerships. The National Health Service (NHS) in the U.K. is investing in laboratory modernization and digital integration, while Germany is advancing hospital network upgrades and research collaborations. France and Spain are expanding molecular testing capacity to address rising respiratory disease burdens. Opportunities are emerging in decentralized testing platforms, laboratory automation technologies, and enhanced data-driven public health monitoring systems that are supporting early outbreak detection and resource planning.

Asia Pacific Molecular Respiratory Panels Market Trends

Asia Pacific is expected to stand as the fastest-growing regional market for molecular respiratory panels through 2033, as healthcare systems here are accelerating modernization and expanding diagnostic capacity. Governments across China, India, Japan, South Korea, and members of the ASEAN are prioritizing comprehensive pathogen surveillance programs to strengthen outbreak preparedness and routine respiratory disease management. Rising incidence of respiratory infections and increasing awareness of early detection are driving higher testing volumes across urban and semi-urban areas. Expanding healthcare budgets are supporting laboratory network development, automation upgrades, and broader point-of-care deployment. Japan is facing sustained demand due to its aging population and higher vulnerability to respiratory illnesses, while South Korea is maintaining elevated diagnostic readiness following prior epidemic experiences. Rapid urbanization and air quality challenges in China are further reinforcing the need for continuous respiratory monitoring.

The regional market is also benefiting from cost advantages and integrated supply chains that are positioning Asia Pacific as both a major consumption hub and a manufacturing center for molecular diagnostics. Regulatory frameworks are gradually aligning with international quality standards, which is improving product credibility and facilitating regional distribution. Streamlined approval pathways in several countries are reducing time to market for innovative platforms. Multinational companies such as Thermo Fisher Scientific are establishing or expanding local operations to capture long-term growth potential and optimize cost structures. Strategic opportunities are concentrating on affordable testing solutions for resource-constrained settings, mobile laboratory systems that extend access to rural populations, and public-private partnerships that are strengthening nationwide surveillance infrastructure. For manufacturers and investors, Asia Pacific is presenting a compelling growth environment supported by demographic shifts, infrastructure investment, and regulatory evolution.

Competitive Landscape

The global molecular respiratory panels market is exhibiting a moderately concentrated structure, with F. Hoffmann-La Roche, bioMérieux SA, Becton, Dickinson and Company (BD), Thermo Fisher Scientific, and QIAGEN collectively accounting for approximately two-fifths of total market share. These firms are leveraging established brand credibility, extensive distribution networks, and long-standing clinical relationships to maintain competitive leadership. The current market phase is reflecting increasing consolidation, which is placing mounting pressure on mid-sized manufacturers. To remain competitive, these companies are pursuing strategic acquisitions, forming technology alliances, or focusing on specialized clinical niches where differentiation is achievable and margins remain defensible.

Competitive positioning is increasingly depending on integrated service ecosystems rather than standalone diagnostic instruments. Leading players are combining molecular platforms with reagent supply contracts, laboratory information system integration, and embedded clinical decision support tools. Investments in automation technologies are improving laboratory throughput and reducing manual intervention, which is enhancing operational efficiency for healthcare providers. The integration of artificial intelligence (AI) is further strengthening analytical performance and workflow optimization. Companies that offer comprehensive multi-pathogen detection panels are achieving stronger premium positioning compared to single-technology competitors. In the current market scenario, sustained success requires platform scalability, digital integration capabilities, and the ability to deliver end-to-end diagnostic solutions that support both clinical accuracy and operational efficiency.

Key Industry Developments

- In December 2025, BD expanded its BD MAX™ System menu in Europe with In Vitro Diagnostic Medical Device Regulation (IVDR) certification for two VIASURE assays developed by Certest Biotec. The VIASURE Respiratory Virus Extended Mix Real Time PCR Detection Kit detects multiple respiratory viruses.

- In October 2025, Hologic received U.S. FDA 510(k) clearance and EU Conformité Européenne (CE) marking under the IVDR for its Panther Fusion Gastrointestinal (GI) Bacterial and Expanded Bacterial Assays. These molecular tests rapidly detect common bacterial pathogens causing infectious gastroenteritis.

- In August 2025, Roche received U.S. FDA 510(k) clearance for its cobas® Respiratory 4-flex assay, the first respiratory test using the company's innovative Temperature-Activated Generation of Signal (TAGS) technology.

Companies Covered in Molecular Respiratory Panels Market

- F. Hoffmann-La Roche Ltd

- bioMérieux SA

- Becton, Dickinson and Company (BD)

- Thermo Fisher Scientific Inc.

- QIAGEN N.V.

- Abbott Laboratories

- Hologic Inc.

- Seegene, Inc.

- DiaSorin S.p.A.

- Bio-Rad Laboratories, Inc.

- Illumina Inc.

- GenMark Diagnostics (Roche)

- Cepheid (Danaher)

- Altona Diagnostics GmbH

- CerTest Biotec S.L.

Frequently Asked Questions

The global molecular respiratory panels market is projected to reach US$ 1.3 billion in 2026.

The market is driven by rising global respiratory infections and post-COVID-19 surveillance infrastructure sustain demand for multiplex molecular diagnostics.

The market is poised to witness a CAGR of 6% from 2026 to 2033.

AI integration and point-of-care expansion are unlocking efficiency gains across decentralized care networks.

F. Hoffmann-La Roche, bioMérieux SA, BD, Thermo Fisher Scientific and QIAGEN N.V are some of the key players in the market.