- Medical Devices

- Respiratory Anesthesia Consumables Market

Respiratory Anesthesia Consumables Market Size, Share, and Growth Forecast, 2026 - 2033

Respiratory Anesthesia Consumables Market by Product Type (Anesthesia Masks, Ventilation Circuits, Others), Application (General Surgery, Cardiac Surgery, Others), End-user (Ambulatory Surgery Center, Others), and Regional Analysis for 2026 – 2033

Respiratory Anesthesia Consumables Market Size and Trends Analysis

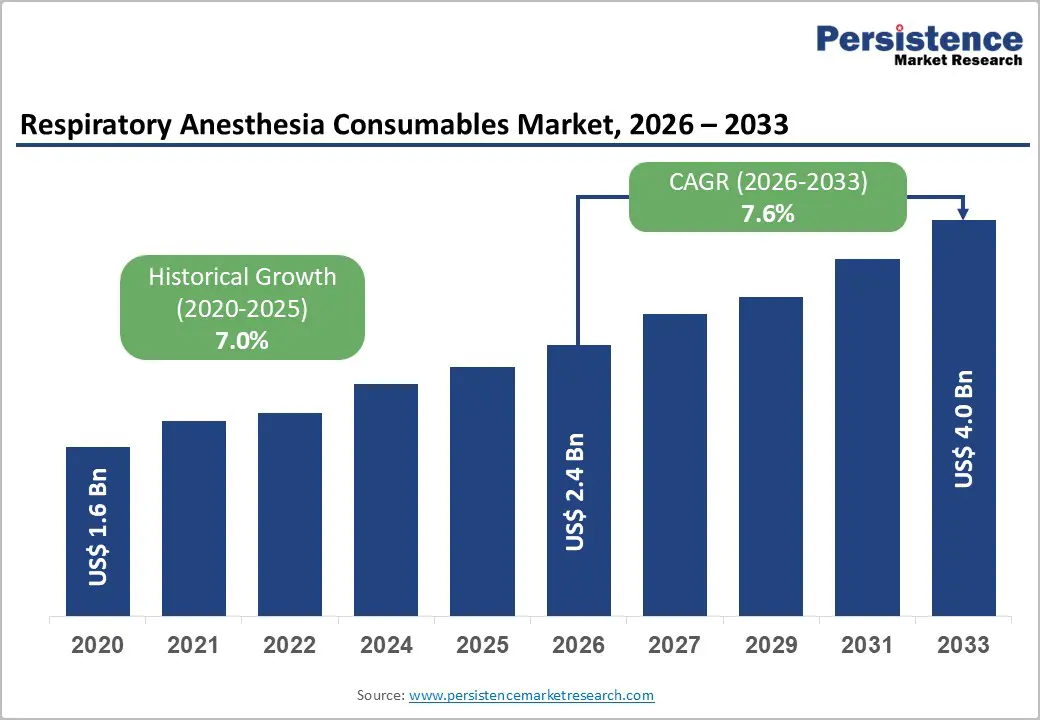

The global respiratory anesthesia consumables market size is lFikely to be valued at US$2.4 billion in 2026, and is expected to reach US$4.0 billion by 2033, growing at a CAGR of 7.6% during the forecast period from 2026 to 2033, driven by the increasing prevalence of surgical procedures, rising number of ambulatory surgery centers, and growing demand for single-use, infection-control respiratory anesthesia consumables.

Growing demand for high-quality, disposable endotracheal tubes and laryngeal masks, especially in hospitals and ASCs, is accelerating adoption across end-use settings. Advances in cuff pressure monitoring and anti-microbial coatings are further boosting uptake by offering better patient safety and reduced ventilator-associated pneumonia risk. Increasing recognition of respiratory anesthesia consumables as critical for airway management, infection prevention, and procedural efficiency in emerging surgical volume markets remains a major driver of market growth.

Key Industry Highlights:

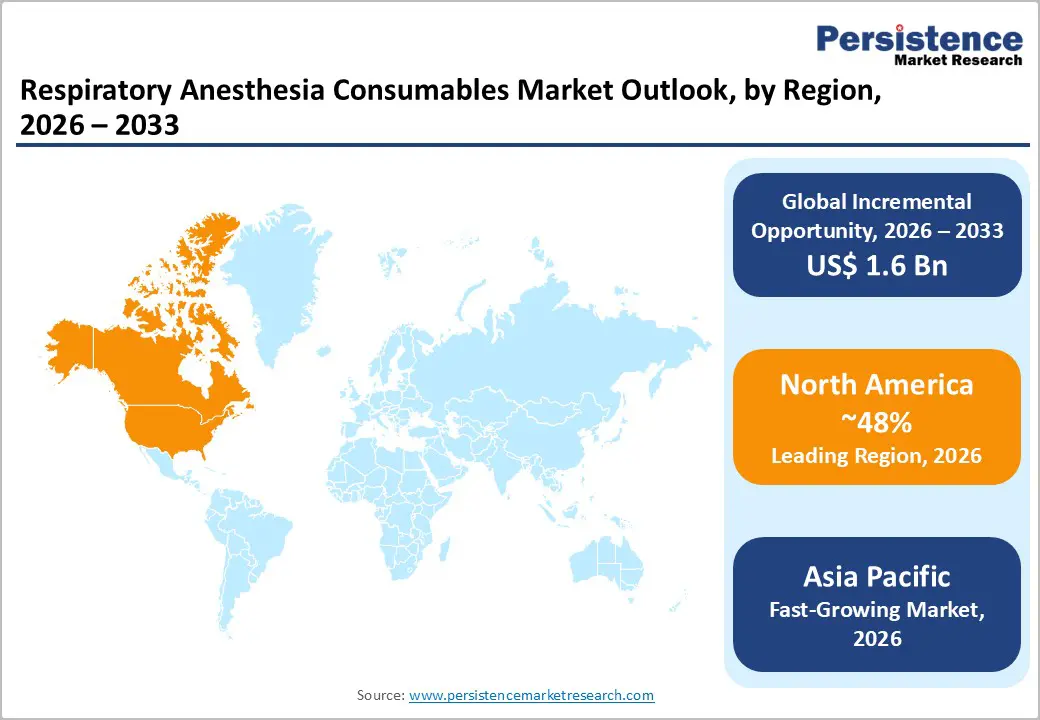

- Leading Region: North America, anticipated to account for a 38% market share in 2026, driven by high surgical volumes, advanced ASC penetration, and strong demand in the U.S.

- Fastest-growing Region: Asia Pacific, fueled by a rapid increase in surgical procedures, expanding healthcare infrastructure, and rising ASC development in China and India.

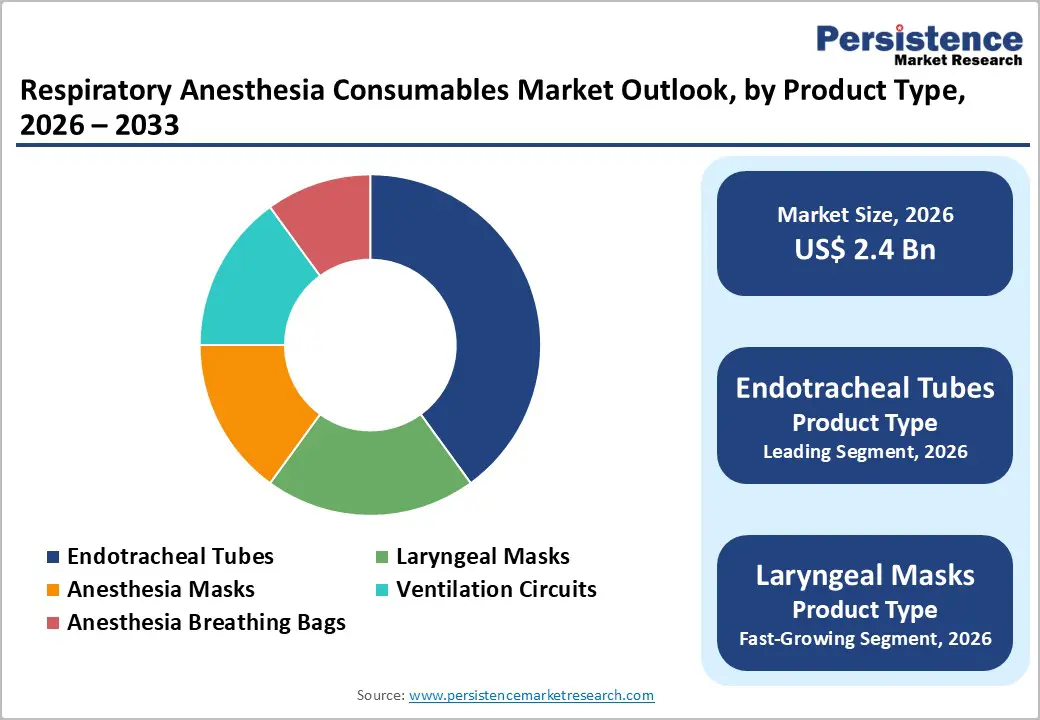

- Dominant Product Type: Endotracheal tubes, to hold approximately 42% of the market share, as they remain the core airway device in general anesthesia.

- Leading Application: General surgery, contributing nearly 48% of the market revenue, due to the highest procedural volume.

- Leading End-user: Hospitals, accounting for over 55% of the market revenue, due to centralized OR infrastructure and high case load.

| Key Insights | Details |

|---|---|

| Respiratory Anesthesia Consumables Market Size (2026E) | US$2.4 Bn |

| Market Value Forecast (2033F) | US$4.0 Bn |

| Projected Growth CAGR (2026-2033) | 7.6% |

| Historical Market Growth (2020-2025) | 7.0% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Growth Analysis – Demand for Surgical Volumes and Ambulatory Surgery Centre Expansion

The growing demand for surgical procedures globally is a key driver for the respiratory anesthesia consumables market. Rising prevalence of chronic diseases, an aging population, and increasing adoption of elective and minimally invasive surgeries are driving higher surgical volumes in both hospitals and specialized facilities. As surgical interventions become more routine, the consumption of anesthesia consumables, including breathing circuits, endotracheal tubes, and face masks, is increasing proportionally. Hospitals are also investing in modern operating rooms and updated anesthesia systems, which require compatible and high-quality consumables to maintain patient safety and procedural efficiency.

The expansion of ambulatory surgery centers (ASCs) is further boosting demand. ASCs are preferred for outpatient procedures due to shorter wait times, lower costs, and patient convenience. These centers often perform a high volume of day surgeries, creating a sustained demand for disposable anesthesia consumables to maintain hygiene and reduce cross-contamination. The rise of outpatient procedures, including orthopedics, ophthalmology, and minor cardiac interventions, has encouraged both established and new ASCs to invest in comprehensive anesthesia infrastructure.

Focus on Single-Use and Infection-Control Products

The emphasis on single-use and infection-control products is shaping the respiratory anesthesia consumables market as healthcare providers prioritize patient safety and regulatory compliance. Single-use products, such as disposable endotracheal tubes, face masks, breathing circuits, and laryngeal masks, are designed to eliminate the risk of cross-contamination between patients. Their adoption has accelerated, particularly in hospitals and ambulatory surgical centers, where hygiene standards are strictly monitored, and infection prevention protocols are enforced.

Infection-control concerns have been further heightened by global health crises and the growing awareness of hospital-acquired infections. Reusable consumables require rigorous sterilization processes that are time-consuming and may carry residual contamination risks if protocols are not strictly followed. By contrast, single-use products ensure sterility for every procedure and reduce operational complexity in high-volume surgical settings.

Barrier Analysis – High Cost of Premium Single-Use Consumables

High costs associated with premium single-use consumables remain a key challenge across healthcare and industrial settings, despite their advantages in safety and performance. These products are typically manufactured using specialized materials, advanced sterilization processes, and strict quality controls to meet regulatory and performance standards. The use of medical-grade polymers, antimicrobial coatings, and precision manufacturing techniques significantly increases production costs compared with reusable or basic disposable alternatives.

In healthcare environments, premium single-use consumables are often designed to reduce infection risks, ensure consistent performance, and eliminate cross-contamination. While these benefits support better patient outcomes, they also lead to higher procurement expenses for hospitals and clinics operating under tight budgets. Cost pressures are further amplified by supply chain dependencies on high-quality raw materials and on compliance with evolving regulatory requirements, which increase overall product pricing. For end users, the recurring nature of single-use products translates into continuous expenditure rather than a one-time investment.

Supply Chain Disruptions and Raw Material Shortages

Supply chain disruptions and raw material shortages have emerged as persistent challenges across manufacturing and healthcare industries, affecting production stability and cost structures. Global supply networks have become increasingly complex, relying on geographically concentrated sources of key materials. Any interruption, such as transportation delays, trade restrictions, geopolitical tensions, or natural disasters, can quickly limit access to essential inputs and disrupt manufacturing operations.

Raw material shortages further intensify these disruptions. Limited availability of specialized polymers, metals, or electronic components forces manufacturers to compete for supply, often at higher prices and with longer lead times. In some cases, production schedules must be adjusted or delayed due to inconsistent material flow, impacting order fulfillment and customer confidence. Smaller suppliers are particularly vulnerable, as they may lack the purchasing power or inventory buffers to absorb sudden shocks. To mitigate these risks, companies are increasingly diversifying supplier bases, increasing safety stock levels, and exploring local or regional sourcing options.

Opportunity Analysis – Expansion in Advanced Airway Management Devices and ASC Penetration

Expansion of advanced airway management devices is strongly supported by the increasing penetration of ambulatory surgery centers (ASCs). As surgical procedures increasingly shift from large hospitals to ASCs, there is a growing demand for airway devices that are compact, easy to use, and capable of maintaining high safety standards in fast-paced clinical environments. Advanced airway management solutions, such as improved supraglottic airway devices, video-assisted intubation tools, and anatomically optimized masks, are designed to support rapid patient turnover while maintaining reliable airway control.

ASCs prioritize efficiency, infection control, and predictable clinical outcomes, which align well with next-generation airway devices that offer enhanced sealing, reduced complication risk, and simplified training requirements. Many of these devices are optimized for single-use or limited reprocessing, helping ASCs minimize cross-contamination and streamline workflows. The increasing volume of minimally invasive and elective procedures performed in ASCs has expanded the need for airway devices suitable for short-duration anesthesia and conscious sedation.

Innovation in Homecare Ventilation

Innovation in homecare ventilation is transforming the management of chronic respiratory conditions by shifting care from hospitals to patients' homes without compromising safety or effectiveness. Modern home ventilation devices are becoming smaller, quieter, and more energy-efficient, making long-term use more comfortable and less intrusive for patients. Advances in sensor technology and smart algorithms now allow devices to automatically adjust airflow, pressure, and oxygen delivery based on real-time patient breathing patterns.

Connectivity has emerged as a key area of innovation. Many homecare ventilators support remote monitoring, enabling clinicians to track patient status, adherence, and device performance without requiring frequent hospital visits. This improves clinical oversight while reducing the burden on the healthcare system and patient inconvenience. User-friendly interfaces and simplified setup processes have also lowered the learning curve for caregivers and patients, supporting broader adoption.

Category-wise Analysis

Product Type Insights

Endotracheal tubes are anticipated to dominate the market, accounting for approximately 42% of the market share in 2026, due to their essential role in securing the airway during surgeries, emergency care, and critical care ventilation. They are widely used across a broad range of procedures requiring general anesthesia and mechanical ventilation, making them a standard clinical requirement in hospitals and ambulatory surgery centers. Continuous improvements in tube materials, cuff design, and safety features have enhanced patient comfort and reduced complication risks. Medtronic plc is one of the leading manufacturers of endotracheal tubes. Shiley™ endotracheal tubes with the TaperGuard™ cuff offer multiple clinical benefits that support safer and more comfortable airway management. The advanced cuff design helps enhance lung protection, reduces pressure on the tracheal wall, and lowers the incidence of postoperative sore throat, contributing to improved patient outcomes. The product is available with or without a preloaded stylet, providing clinicians with flexibility based on procedural needs.

Laryngeal masks represent the fastest-growing product type, fueled by a reliable, less invasive alternative to traditional endotracheal intubation for airway management in many surgical and emergency scenarios. Their ease of placement, reduced requirement for deep anesthesia, and lower risk of airway trauma make them especially attractive in outpatient, ambulatory, and short-procedure settings. As clinicians look for devices that shorten setup time and improve patient comfort while maintaining effective ventilation, laryngeal masks have seen broader adoption. Ambu AuraOnce Disposable Laryngeal Mask, produced by Ambu A/S, a major global manufacturer of airway management devices. The AuraOnce is a disposable, anatomically curved laryngeal mask airway designed for fast and easy placement with a soft cuff that establishes an effective seal for routine anesthesia and emergency ventilation.

Application Insights

General surgery is expected to dominate the market, contributing nearly 48% of revenue in 2026, supported by the largest volume of procedural demand that requires airway management and ventilation support. General surgical procedures ranging from abdominal operations to routine minimally invasive interventions typically involve controlled anesthesia and airway devices such as endotracheal tubes and laryngeal masks. These devices are used consistently across a wide range of patient populations and hospital settings, driving steady consumption. Medtronic plc’s Portex® endotracheal tubes are extensively used in general surgical procedures, which require controlled airway management under general anesthesia. General surgery, including abdominal, orthopedic, and other routine operations, accounts for the largest application segment of endotracheal tubes because nearly all such surgeries involve securing a patient’s airway to provide ventilation during anesthesia.

Cardiac surgery represents the fastest-growing application, driven by advancements in cardiovascular care that have expanded both the number and complexity of heart procedures performed globally. As populations age and cardiovascular disease prevalence increases, more patients are undergoing surgical interventions such as bypass, valve repair or replacement, and minimally invasive cardiac procedures. These operations often require precise airway and ventilation management, advanced monitoring, and longer perioperative support, driving greater utilization of specialized devices and consumables. According to the National Library of Medicine, most cardiac surgical procedures worldwide are CABG, with approximately 800,000 performed annually. Despite the growing prevalence of high-risk patients, substantial improvements in CABG outcomes have been achieved during the past years. Maquet Cardiovascular’s (a Getinge brand) heart-lung machines and associated airway/ventilation support products during open-heart procedures. Maquet’s systems are widely used in coronary artery bypass grafting (CABG) and heart valve surgeries, which have been increasing in number due to rising cardiovascular disease rates globally. These procedures require complex airway management and cardiopulmonary support, driving increased use of devices such as endotracheal tubes, ventilators, and perfusion equipment.

Regional Insights

North America Respiratory Anesthesia Consumables Market Trends

North America is projected to dominate, accounting for nearly 48% revenue in 2026, driven by the region’s high surgical volumes, strong ASC penetration, and high public awareness of infection-control benefits. Distribution systems in the U.S. and Canada provide extensive support for respiratory consumables programs, ensuring wide accessibility across endotracheal tubes, general surgery, and hospital populations. Increasing demand for single-use, convenient, and easy-to-deploy forms is further accelerating adoption, as these formats improve patient safety and reduce barriers associated with reusable devices.

Innovation in respiratory anesthesia consumables technology, including stable laryngeal masks, improved cuff monitoring delivery, and targeted ASC enhancement, is attracting significant investment from both public and private sectors. Government initiatives and CMS campaigns continue to promote use against infection risks, procedural efficiency concerns, and emerging outpatient threats, creating sustained market demand. The growing focus on cardiac grades and specialty uses, particularly for general surgery and others, is expanding the target applications for respiratory anesthesia consumables.

Europe Respiratory Anesthesia Consumables Market Trends

Europe is increasing awareness of single-use infection-control benefits, strong regulatory systems, and government-led outpatient surgery programs. Countries such as Germany, France, the U.K., and Spain have well-established healthcare frameworks that support routine respiratory consumables use and encourage the adoption of innovative airway delivery methods, including laryngeal masks and cuffed tubes. These high-safety formulations are particularly appealing for general surgery populations, regulation-conscious hospitals, and ASC users, improving outcomes and coverage rates.

Technological advancements in respiratory anesthesia consumables development, such as enhanced anti-microbial, application-targeted delivery, and improved laryngeal mask grades, are further boosting market potential. European authorities are increasingly supporting research and trials for consumables against both routine and specialized needs, strengthening market confidence. The growing emphasis on convenient, single-use options is aligned with the region’s focus on preventive HAI reduction and day-surgery expansion. Public awareness campaigns and promotion drives are expanding reach in both hospital and ASC segments, while suppliers are investing in production and novel variants to increase efficacy.

Asia Pacific Respiratory Anesthesia Consumables Market Trends

Asia Pacific is likely to be the fastest-growing market for respiratory anesthesia consumables in 2026, driven by rising surgical awareness, increasing government initiatives, and expanding application programs across the region. Countries such as China, India, Japan, and South Korea are actively promoting consumables campaigns to address surgical growth and emerging infection-control needs. Respiratory anesthesia consumables are particularly attractive in these regions due to their scalable administration, ease of adoption, and suitability for large-scale hospital and ASC drives in both urban and rural populations.

Technological advancements are supporting the development of stable, effective, and easy-to-deploy respiratory consumables, which can withstand challenging sterilization conditions and minimize infection dependence. These innovations are critical for reaching domestic hospitals and improving overall surgical coverage. Growing demand for endotracheal tubes, general surgery, and hospitals applications is contributing to market expansion. Public-private partnerships, increased healthcare expenditure, and rising investment in consumables research and production capacity are further accelerating growth. The convenience of consumables delivery, combined with improved safety and reduced risk of complications, positions it as a preferred choice.

Competitive Landscape

The global respiratory anesthesia consumables market features competition between established medical device leaders and emerging airway specialists. In North America and Europe, Medtronic and Ambu lead through strong R&D, distribution networks, and hospital ties, bolstered by innovative endotracheal tube and laryngeal mask programs. In Asia Pacific, local players advance with cost-competitive solutions, enhancing accessibility. Single-use delivery boosts infection control, cuts cross-contamination risks, and enables mass integrations across ORs. Strategic partnerships, collaborations, and acquisitions merge expertise, expand portfolios, and speed commercialization. Antimicrobial formulations solve VAP issues, aiding penetration in high-risk procedures.

Key Industry Developments

- In April 2025, Dräger, a global leader in medical and safety technology, announced the launch of the Atlan® A100 anesthesia workstation in India. The innovative anesthesia workstation was engineered to enhance patient care and optimize workflows in the operating room. The Atlan® A100 system was equipped with advanced lung-protective ventilation, low-flow anesthesia capabilities, and infection-prevention measures, providing medical professionals with tools designed to optimize patient outcomes and improve efficiency across perioperative settings.

Companies Covered in Respiratory Anesthesia Consumables Market

- Medtronic

- Boston Scientific Corporation

- Koninklijke Philips N.V.

- Westmed, Inc.

- Armstrong Medical

- Teleflex Incorporated

- Smiths Group plc

- Airways Corporation

- Allied Healthcare Products, Inc.

- Bard Medical

Frequently Asked Questions

The global respiratory anesthesia consumables market is projected to reach US$2.4 billion in 2026.

Growing focus on infection control and patient safety is accelerating the adoption of single-use and advanced airway consumables, helping healthcare facilities reduce cross-contamination risks and improve clinical outcomes.

The respiratory anesthesia consumables market is poised to witness a CAGR of 7.6% from 2026 to 2033.

Expansion of ambulatory surgery centers (ASCs) and outpatient procedures is creating strong demand for compact, easy-to-use, and single-use respiratory anesthesia consumables that support faster patient turnover and efficient clinical workflows.

Medtronic, Ambu, Teleflex Incorporated, Smiths Group plc, and BD are the key players.