- Agrochemicals

- Phosphate Fertilizers Market

Phosphate Fertilizers Market Size, Share, and Growth Forecast 2026 - 2033

Phosphate Fertilizers Market by Product Type (Monoammonium Phosphate (MAP), Diammonium Phosphate (DAP), Single Superphosphate (SSP), Triple Superphosphate (TSP), Others), Application (Cereals and Grains, Oilseeds, Fruits and Vegetables, Others), and Regional Analysis, 2026–2033

Phosphate Fertilizers Market Size and Trend Analysis

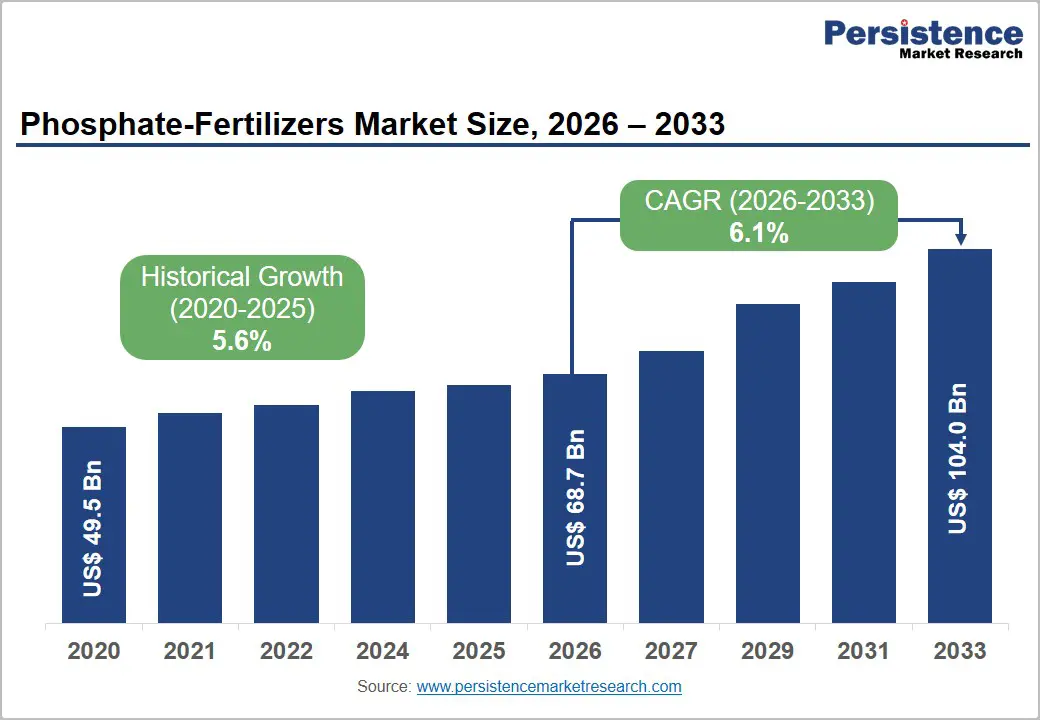

The global phosphate fertilizers market size is expected to be valued at US$ 68.7 billion in 2026 and projected to reach US$ 104.0 billion by 2033, growing at a CAGR of 6.1% between 2026 and 2033. This robust growth is driven by the critical and irreplaceable role of phosphate fertilizers in global food security, rising population-driven food demand, and intensifying agricultural productivity requirements across major crop-producing economies.

The Food and Agriculture Organization of the United Nations (FAO) projects global food demand will increase by approximately 50% by 2050 relative to 2012 levels, compelling consistent expansion in fertilizer application across cereal, oilseed, and horticultural crop systems.

Key Industry Highlights

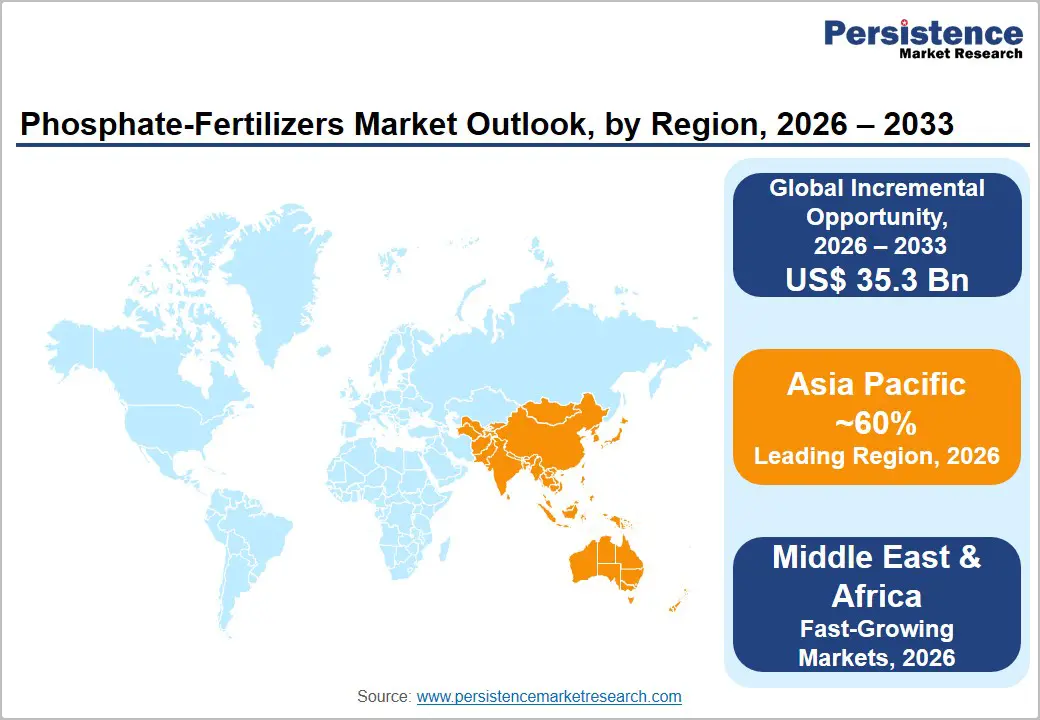

- Leading Region: Asia Pacific dominates the global phosphate fertilizers market with 60% market share in 2026, anchored by China’s role as the world’s largest producer and consumer, India’s government-subsidized DAP/MAP procurement, and Southeast Asia’s expanding tropical crop fertilization programs.

- Fastest Growing Region: Middle East & Africa is projected to register the highest CAGR during 2026–2033, driven by Saudi Arabia’s Vision 2030 agricultural expansion, Egypt’s New Delta reclamation project, and AfDB-supported fertilizer access programs targeting a 50% increase in smallholder application rates across 11 African countries.

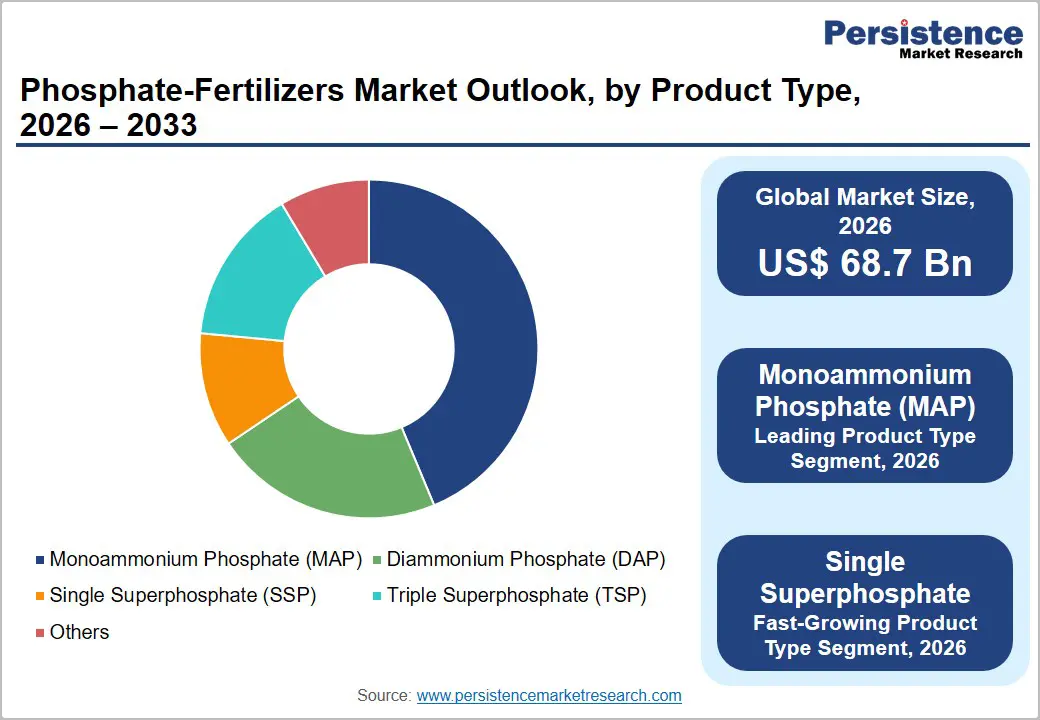

- Dominant Segment: Monoammonium Phosphate (MAP) leads the product type category with 34% market share in 2026, driven by its high phosphorus content (52% P?O?), versatility across broadcast, band, and fertigation applications, and broad compatibility as a component in customized NPK blend formulations globally.

- Fastest Growing Segment: Single Superphosphate (SSP) is the fastest growing product type at 7% CAGR over 2026–2033, driven by its dual phosphorus-sulfur nutrition benefit in sulfur-deficient tropical soils, cost-effectiveness in price-sensitive emerging markets, and local production feasibility using lower-grade phosphate rock in Africa and South Asia.

- Key Market Opportunity: The rapid agricultural expansion across Middle East & Africa, supported by OCP Group’s US$ 13 billion regional investment and AfDB fertilizer access programs, combined with MEA’s phosphate rock reserve proximity, represents a US$ 35.3 billion incremental opportunity between 2026 and 2033.

DRO Analysis

Drivers - Rising Global Food Demand and Expanding Cultivated Arable Land

The accelerating global population growth trajectory, with the United Nations projecting world population reaching 9.7 billion by 2050, is generating structurally increasing food demand that can only be met through sustained intensification of agricultural production. Phosphorus is a non-substitutable macronutrient essential for root development, energy transfer, and crop yield formation, making phosphate fertilizer application non-discretionary in modern crop production systems.

The FAO reports that global cereal production must increase by approximately 1 billion tons annually by 2050 from current levels to meet demand. In parallel, the expansion of cultivated land in Sub-Saharan Africa, Latin America, and Southeast Asia, regions with significant soil phosphorus deficits, is generating incremental fertilizer application demand that directly benefits phosphate fertilizer manufacturers through the forecast period.

Government Agricultural Subsidy Programs Supporting Fertilizer Affordability and Adoption

Government-administered fertilizer subsidy programs across major agricultural economies are sustaining high phosphate fertilizer application rates by ensuring product affordability for smallholders and commercial farmers. India’s fertilizer subsidy scheme, one of the world’s largest, allocated approximately INR 1.75 trillion (US$ ~21 billion) in fertilizer subsidies in fiscal year 2023–24 per Ministry of Chemicals and Fertilizers data, covering DAP and other phosphatic fertilizers under the Nutrient-Based Subsidy (NBS) scheme.

Similarly, China’s agricultural support policies, Brazil’s PRONAF program, and EU Common Agricultural Policy (CAP) frameworks sustain baseline fertilizer consumption levels across the world’s largest agricultural producing nations, providing stable procurement volumes that underpin phosphate fertilizer market revenue growth.

Restraints - Concentration of Global Phosphate Rock Reserves Creating Supply Chain Vulnerability

Approximately 70% of global phosphate rock reserves are concentrated in Morocco and Western Sahara (controlled by OCP Group), creating significant supply chain concentration risk for global phosphate fertilizer producers dependent on imported rock. The U.S. Geological Survey (USGS) estimates total global phosphate rock reserves at approximately 71 billion tons, with Morocco holding the largest share by far.

Geopolitical disruptions, export restrictions, or logistics bottlenecks affecting Moroccan supply can cause severe price spikes and production disruptions globally, as demonstrated during the 2021–2022 fertilizer price crisis when DAP prices tripled within 12 months, creating significant market volatility.

Environmental Regulations Restricting Phosphorus Runoff and Fertilizer Application Rates

Tightening environmental regulations targeting agricultural phosphorus runoff, a leading contributor to freshwater eutrophication and aquatic ecosystem degradation, are constraining fertilizer application rates in environmentally regulated markets.

The European Union’s Nitrates Directive and Water Framework Directive impose strict limits on phosphorus application in designated nitrate-vulnerable zones, directly reducing fertilizer volumes in EU member states' agriculture. U.S. EPA’s Clean Water Act regulations similarly impose watershed-level phosphorus loading limits affecting fertilizer application practices across major agricultural states, moderating market volume growth in these regulatory-active geographies.

Opportunities - Rapid SSP Adoption in Emerging Markets as Cost-Effective Phosphate Solution

Single Superphosphate (SSP) is the fast-growing phosphate fertilizer product type at 7% CAGR driven by its cost-effectiveness in price-sensitive agricultural markets across Sub-Saharan Africa, South Asia, and Southeast Asia. SSP provides the dual benefit of phosphorus and sulfur nutrition, a micronutrient increasingly deficient in tropical and subtropical soils, making it agronomically superior to single-nutrient phosphate products in sulfur-deficient regions.

The International Fertilizer Association (IFA) has documented widespread sulfur deficiency in soils across India, Bangladesh, and large parts of Africa, creating a compelling agronomic case for SSP adoption. Local SSP manufacturing using lower-grade phosphate rock accessible in emerging economies reduces import dependency and production costs, enabling competitive pricing that is accelerating SSP's market penetration.

Middle East & Africa Agricultural Expansion Creating High-Growth Fertilizer Demand

The Middle East & Africa (MEA) region represents the fastest growing phosphate fertilizer market over the forecast period, driven by massive agricultural development initiatives, expanding irrigated crop area, and government food security investment programs. Saudi Arabia’s Vision 2030 agricultural expansion program and Egypt’s New Delta Project targeting 1.5 million feddans of new agricultural land reclamation, are generating substantial new fertilizer application demand.

In Sub-Saharan Africa, African Development Bank (AfDB) programs under the Fertilizer and Soil Health Initiative are supporting fertilizer access for smallholder farmers across 11 countries, targeting a 50% increase in fertilizer use rate. Morocco’s OCP Group and Saudi Arabia’s Ma’aden are strategically positioned to supply this growing MEA demand through integrated phosphate rock-to-fertilizer production complexes at competitive regional cost structures.

Category-wise Analysis

Product Type Insights

Monoammonium Phosphate (MAP) leads the phosphate fertilizers market by product type, accounting for approximately 34% of share in 2026. MAP’s dominance is attributable to its high phosphorus content (52% P?O?), favorable nitrogen-to-phosphorus ratio for diverse crop nutritional programs, and its versatility as a direct application granular fertilizer as well as a component in customized NPK blend formulations.

MAP’s suitability for broadcast, band, and fertigation application methods makes it the preferred phosphate fertilizer across major cereal, oilseed, and specialty crop systems globally. The Mosaic Company, Nutrien Ltd., and PJSC PhosAgro are among the world’s largest MAP producers, collectively supplying most of the North American, European, and Asian MAP demand through integrated mine-to-plant production systems.

Application Insights

Cereals and grains represent the leading application segment in the phosphate fertilizers market in 2026, commanding the dominant share of total phosphate fertilizer consumption globally. Cereal crops, including wheat, rice, maize, and barley, are cultivated on the largest global arable land area and require substantial phosphorus inputs for root system development, tillering, and grain fill processes.

The FAO estimates that cereals and grains account for approximately 50% of global caloric intake, making their yield optimization a food security priority that drives non-discretionary fertilizer expenditure. In major cereal-producing geographies, including China, India, the U.S., and Europe, established fertilizer application recommendations from national agricultural extension services mandate phosphate fertilizer use in cereal production programs, ensuring consistent high-volume demand for MAP, DAP, and SSP products in this application segment through 2033.

Regional Analysis

North America Phosphate Fertilizers Market Trends and Insights

North America is a major phosphate fertilizer-producing and consuming region, with the U.S. operating significant integrated phosphate mining and fertilizer manufacturing operations. The region’s large-scale commercial grain and oilseed production belts generate consistent high-volume MAP and DAP demand, while growing adoption of precision agriculture and variable-rate fertilizer application technologies is improving nutrient use efficiency and sustaining value-based fertilizer procurement.

U.S. Phosphate Fertilizers Market Size

The United States accounts for approximately 88% of North American phosphate fertilizer revenues, driven by extensive corn, soybean, and wheat production across the Corn Belt and Great Plains. The Mosaic Company’s Florida and Louisiana operations make the U.S. a significant global MAP and DAP export supplier alongside domestic consumption serving approximately 900 million acres of farmland.

Europe Phosphate Fertilizers Market Trends and Insights

Europe is a significant phosphate fertilizer-consuming region, with demand concentrated in France, Germany, Poland, and Ukraine. EU environmental regulations under the Nitrates Directive and Farm to Fork Strategy are moderating total fertilizer application volumes, while driving adoption of higher-efficiency products and precision application technologies. Yara International ASA and EuroChem are major European phosphate fertilizer suppliers.

Germany Phosphate Fertilizers Market Size

Germany accounts for approximately 18–20% of European phosphate fertilizer revenues, supported by intensive cereal and oilseed production across northern and eastern Germany. EU CAP subsidy frameworks support farmer profitability and maintain fertilizer investment levels, while Germany’s precision agriculture adoption rate is among the highest in Europe, driving MAP and DAP demand through optimized application programs.

U.K. Phosphate Fertilizers Market Size

The U.K. contributes approximately 8–10% of European market revenues, driven by wheat and oilseed rape production across England and Scotland. Post-Brexit agricultural policy through DEFRA’s Environmental Land Management (ELM) scheme is reshaping fertilizer application norms, while the Agriculture and Horticulture Development Board (AHDB) provides nutrient management guidance, maintaining the demand for phosphate fertilizers.

France Phosphate Fertilizers Market Size

France contributes approximately 22% of European phosphate fertilizer revenues, reflecting its position as the EU’s largest agricultural producer with extensive wheat, corn, and sunflower cultivation. France’s Nitrates Action Program (NAP) governs phosphorus application in vulnerable zones, while Yara International and Roullier Group supply specialized phosphate fertilizer products to French farm cooperatives.

Asia Pacific Phosphate Fertilizers Market Trends and Insights

Asia Pacific dominates the global phosphate fertilizers market with 60% share in 2026, anchored by China and India’s massive agricultural sectors. China is simultaneously the world’s largest phosphate fertilizer producer and consumer, with domestic production exceeding 15 million tons of P?O? equivalent annually per China Phosphate & Compound Fertilizer Industry Association data, serving its 120 million hectares of arable land under intensive cultivation.

India Phosphate Fertilizers Market Size

India accounts for approximately 22% of Asia Pacific phosphate fertilizer revenues, driven by the world’s second-largest agricultural sector covering over 170 million hectares of net sown area per Ministry of Agriculture & Farmers’ Welfare data. India’s DAP subsidy under the NBS scheme and Coromandel International Ltd.’s integrated production ensures consistent supply and demand.

Japan Phosphate Fertilizers Market Size

Japan contributes approximately 3–5% of Asia Pacific market revenues, characterized by a mature, precision-oriented agricultural sector with high per-hectare fertilizer efficiency. Japan’s compact but intensive vegetable and rice production systems drive consistent MAP and specialty phosphate fertilizer demand, with JAEA (Japan Atomic Energy Agency) research programs exploring enhanced phosphorus use efficiency technologies.

Southeast Asia Phosphate Fertilizers Market Size

Southeast Asia accounts for approximately 8–10% of Asia Pacific phosphate fertilizer revenues, with Vietnam, Indonesia, Thailand, and Philippines driving demand through rice, palm oil, and rubber cultivation. Expanding tropical crop area and improving smallholder fertilizer access programs under ASEAN food security frameworks are sustaining above-regional-average phosphate fertilizer demand growth.

Competitive Landscape

The global phosphate fertilizers market is moderately consolidated, with integrated phosphate rock-to-fertilizer producers holding significant competitive advantages through control of upstream rock reserves, large-scale production capacity, and established global distribution networks. OCP Group (Morocco), The Mosaic Company, Nutrien Ltd., PJSC PhosAgro, and Ma’aden collectively account for most of the global production capacity.

Key competitive differentiators include phosphate rock reserve access, production cost efficiency, product grade and formulation breadth, and proximity to key agricultural consumption markets. Strategic trends include vertical integration expansion, investment in enhanced efficiency fertilizers (EEF), and digital agronomy services bundled with nutrient programs.

Key Developments

- In March 2025, OCP Group announced a US$ 13 billion multi-year investment program to expand phosphate fertilizer production capacity in Morocco and sub-Saharan Africa, targeting growing MEA food security demand and strengthening its dominant global market position.

- In November 2024, Nutrien Ltd. completed the expansion of its Aurora, North Carolina phosphate fertilizer complex, increasing MAP production capacity by approximately 500,000 tons per year to serve growing North American and export market demand.

- In January 2024, Ma’aden (Saudi Arabian Mining Company) commissioned its expanded Wa’ad Al Shamal phosphate complex Phase II, adding significant DAP and MAP production capacity to serve Middle East, South Asian, and African export markets at competitive cost structures.

Global Phosphate Fertilizers Market – Key Insights & Details

| Key Insights | Details |

|---|---|

|

Historical Market Value (2020) |

US$ 49.5 Billion |

|

Current Market Value (2026) |

US$ 68.7 Billion |

|

Projected Market Value (2033) |

US$ 104.0 Billion |

|

CAGR (2026–2033) |

6.1% |

|

Leading Region |

Asia Pacific, 60% market share (2026) |

|

Dominant Product Type (Category-1) |

Monoammonium Phosphate (MAP), 34% market share (2026) |

|

Top-ranking Application (Category-2) |

Cereals and Grains, leading share (2026) |

|

Incremental Opportunity |

US$ 35.3 Billion (2026–2033) |

Companies Covered in Phosphate Fertilizers Market

- Eurochem Group AG

- Israel Chemicals Ltd.

- Coromandel International Ltd.

- Nutrien Ltd.

- Ma'aden

- Agrium Inc.

- PJSC PhosAgro.

- Yara International ASA

- The OCP Group

- JESA

- MIRA Organics and Chemicals PVT LTD

- Potash Corp. of Saskatchewan Inc.

- CF Industries Holdings Inc.

- The Mosaic Co.

- S.A OCP

Frequently Asked Questions

The global phosphate fertilizers market is projected to be valued at US$ 68.7 billion in 2026, driven by structurally growing food demand linked to UN-projected population growth to 9.7 billion by 2050, non-discretionary phosphorus application requirements in cereal and oilseed crop systems, and government fertilizer subsidy programs sustaining affordability and high application rates across Asia Pacific and Latin America.

The primary drivers are the irreplaceable role of phosphorus in crop nutrition, with FAO projecting food demand to increase 50% by 2050, and large-scale government subsidy programs, including India’s INR 1.75 trillion NBS fertilizer scheme and China’s agricultural support policies.

Asia Pacific leads with approximately 60% market share in 2026, driven by China’s position as the world’s largest phosphate fertilizer producer and consumer with annual production exceeding 15 million tons P₂O₅, India’s government-subsidized DAP and MAP procurement program covering 170 million hectares of farmland, and Southeast Asia’s rapidly expanding tropical crop phosphate fertilizer consumption.

The most significant opportunity is the Middle East & Africa’s rapid agricultural expansion, with OCP Group’s US$ 13 billion investment program, Ma’aden’s Wa’ad Al Shamal Phase II expansion, and AfDB’s fertilizer access initiative targeting a 50% increase in smallholder fertilizer use across 11 African countries. SSP’s growing adoption in sulfur-deficient tropical soils at 7% CAGR represents an additional high-growth commercial opportunity.

Key players include The OCP Group (Morocco), The Mosaic Company, Nutrien Ltd., PJSC PhosAgro, Yara International ASA, Ma’aden, Eurochem Group AG, Israel Chemicals Ltd., Coromandel International Ltd., CF Industries Holdings Inc., Potash Corp. of Saskatchewan Inc., Agrium Inc., JESA, MIRA Organics and Chemicals PVT LTD, Groupe Roullier, and Haifa Group, among others.