- Specialty & Fine Chemicals

- Sodium Acid Pyrophosphate (SAPP) Market

Sodium Acid Pyrophosphate (SAPP) Market Size, Share, and Growth Forecast, 2026 - 2033

Sodium Acid Pyrophosphate (SAPP) Market by Product Type (Food Grade, Industrial Grade), Application (Food & Beverages, Water Treatment, Detergents & Cleaning Products, Pharmaceuticals, Others), End-User (Food Processing Industry, Chemical Industry, Agriculture, Pharmaceutical & Cosmetics, Others), and Regional Analysis for 2026 - 2033

Sodium Acid Pyrophosphate (SAPP) Market Share and Trends Analysis

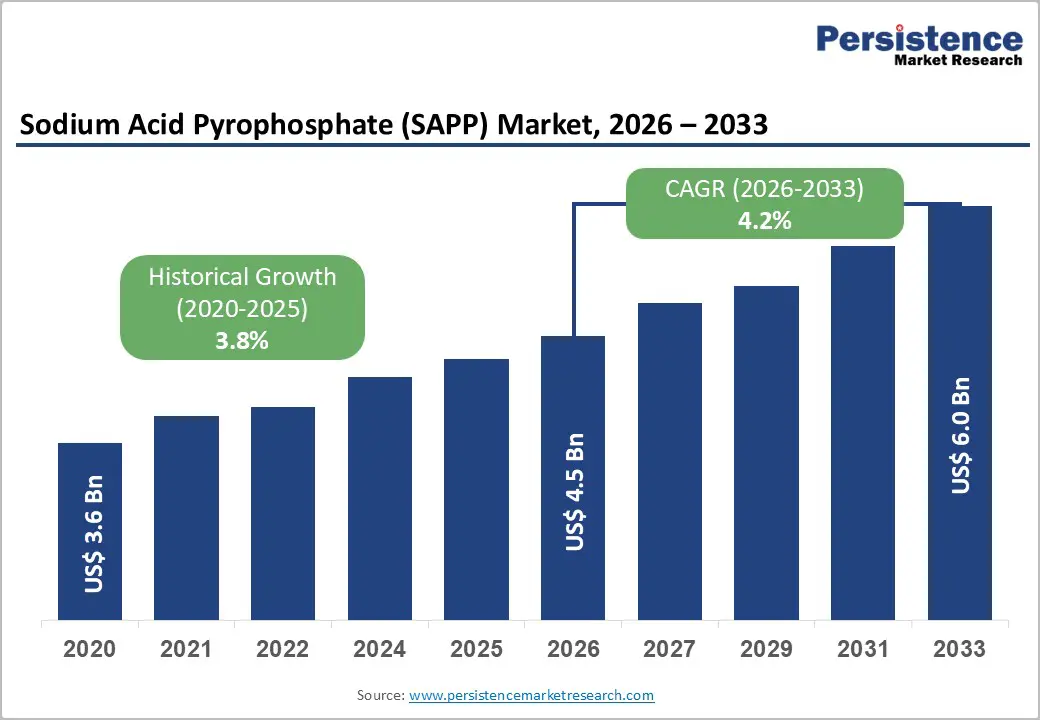

The global sodium acid pyrophosphate (SAPP) market size is likely to be valued at US$ 4.5 billion in 2026, and is projected to reach US$ 6.0 billion by 2033, growing at a CAGR of 4.2% during the forecast period 2026−2033. This steady progression has stemmed from heightened consumption of processed foods, increased investments in water purification systems, and persistent needs for industrial chemicals.

Food-grade SAPP has driven revenue through its essential roles as a leavening agent, buffering compound, and chelating agent in bakery products and meat products. Industrial-grade variants have gained traction via global upgrades to municipal and factory water treatment facilities. This balanced trajectory reflects diversified demand across resilient sectors, where SAPP delivers unmatched consistency in high-volume operations. Companies prioritizing scalability will benefit from its versatility, as urban expansion and regulatory pushes amplify uptake in both food and non-food arenas. Organizations can future-proof portfolios by exploring hybrid applications that blend SAPP with clean-label alternatives, ensuring compliance while capturing margins in premium segments.

Key Industry Highlights

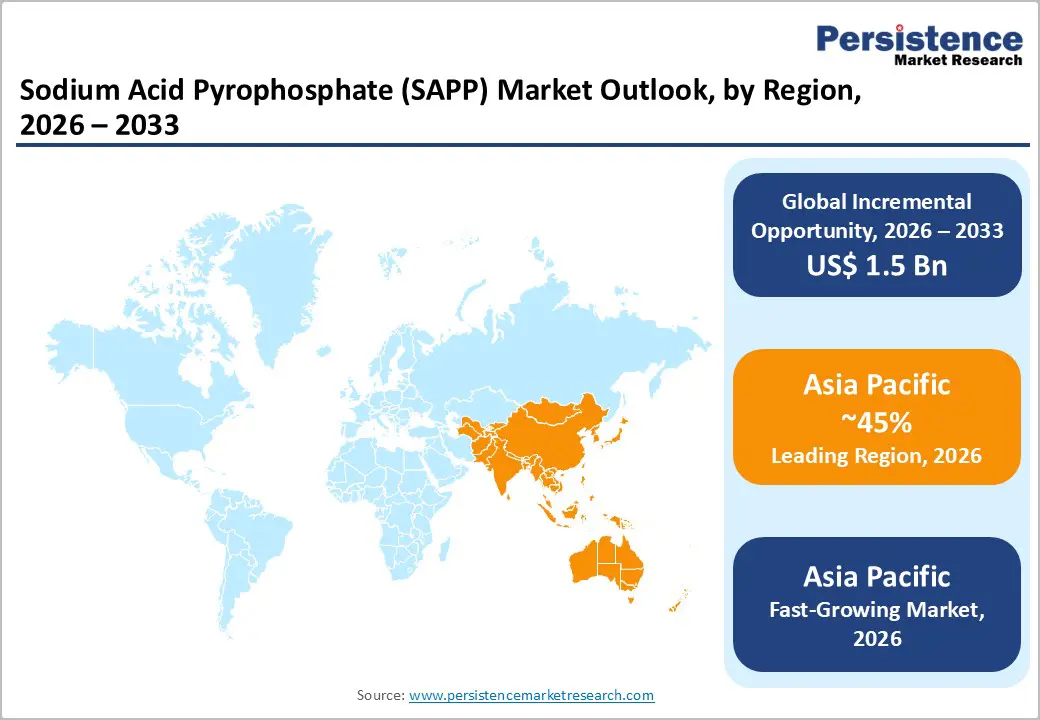

- Dominant Region: Asia Pacific is projected to hold around 45% market share in 2026, driven by skyrocketing demand for processed and convenience foods in urban centers.

- Fastest-growing Market: Asia Pacific is forecasted to be the fastest-growing market from 2026 to 2033, driven by industrial expansion and urban infrastructure development.

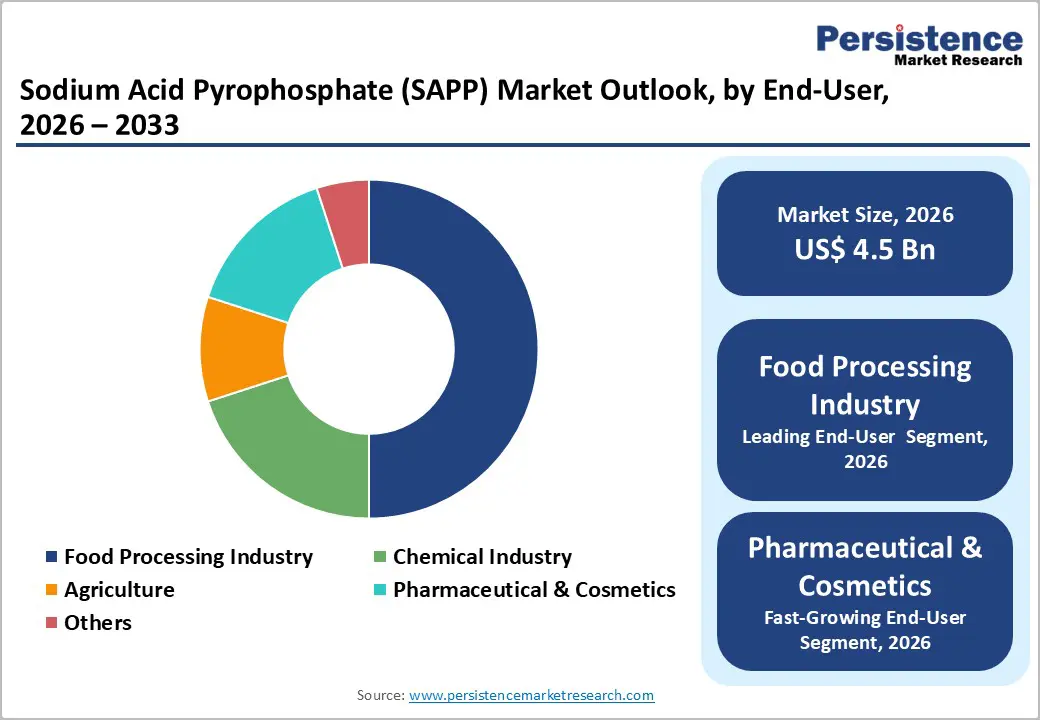

- Leading End-User: The food processing industry is likely to lead with over 50% market share in 2026, driven by scalable production and a heavy reliance on functional ingredients.

- Fastest-growing End-User: The pharmaceutical & cosmetics sector is projected to grow the fastest from 2026 to 2033, driven by rising demand for excipients, formulation innovation, and regulatory-driven product diversification.

| Key Insights | Details |

|---|---|

|

Sodium Acid Pyrophosphate (SAPP) Market Size (2026E) |

US$ 4.5 Bn |

|

Market Value Forecast (2033F) |

US$ 6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.2% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.8% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Expansion in the Food and Beverage Processing Industry

The expansion of food and beverage processing has heightened demand for sodium acid pyrophosphate through essential industrial needs for scale, consistency, and speed. Modern facilities have prioritized reliable leavening, precise moisture control, and uniform texture in high-volume production lines. This ingredient has delivered these benefits amid heat exposure, intense mixing, and frozen logistics, integrating seamlessly into automated systems and uniform recipes. Processors' scaling operations have selected it to minimize variability, safeguard yields, and accelerate equipment transitions. As product ranges diversify into bakery items, snacks, and ready-to-eat meals, buyers have increasingly valued its consistent functionality to uphold operational standards and quality benchmarks.

Strategic investments in production infrastructure have strengthened long-term procurement practices and formulation controls, further boosting SAPP adoption. Centralized purchasing teams have favored suppliers offering stability across regions and vendors. The compound has ensured repeatable results from one batch to the next, reducing adjustments during capacity upgrades and product introductions. Contract manufacturers and private-label operations have relied on its strict specifications to fulfill brand commitments. Organizations pursuing exports have emphasized its role in meeting regulatory demands and enhancing shelf life, which will optimize supply chains and curb waste in the years ahead. Forward planners should assess hybrid blends to future-proof formulations against evolving efficiency pressures.

Health Concerns Related to Phosphate Intake

Health concerns about phosphate intake have significantly restrained demand for sodium acid pyrophosphate, as consumer perceptions and regulatory reviews have reshaped ingredient choices. Greater awareness of dietary phosphorus balance has sharpened scrutiny on its presence in processed foods. Manufacturers have encountered demands from health advocates and nutrition-savvy shoppers to curb phosphate levels in recipes. Clean-label strategies and straightforward ingredient lists have prompted developers to reevaluate synthetic aids, heightening risks for those linked to overconsumption. This evolution has curbed SAPP uptake in everyday products such as baked goods and snacks.

Regulatory monitoring and buyer-mandated limits have tightened demand further, with institutional purchasers, retailers, and foodservice providers enforcing phosphate caps to match wellness goals. Reformulation efforts have entailed added expenses, validation trials, and delays, fostering conservative sourcing approaches. Brand managers have balanced its processing advantages against backlash potential, particularly in fitness-focused lines. Future pipelines favor substitutes that deliver efficacy alongside broad appeal. Organizations should audit formulations early and explore natural leaveners to mitigate compliance hurdles and seize cleaner alternatives.

Emerging Applications in Water Treatment and Detergents

Emerging applications in water treatment and detergents have opened substantial growth opportunities for SAPP, as industries have focused on efficiency, regulatory adherence, and performance gains. Water treatment facilities have required agents that prevent scaling, stabilize ions, and boost system reliability in both municipal and industrial setups. This compound has met these needs by ensuring uniform treatment results and shielding equipment from mineral deposits. Urban expansion and industrial water recycling initiatives have heightened the call for reliable chemicals that match operational benchmarks and budget constraints. Formulators will find SAPP particularly suited to these dynamic environments, where consistent efficacy drives long-term adoption.

Detergent producers have offered another promising expansion path, propelled by the need for superior cleaning power and precise blending. Contemporary formulations have stressed water softening, effective stain lifting, and synergy with sophisticated surfactants. SAPP has enhanced these traits by optimizing performance across diverse water qualities. High-concentration and institutional cleaners have relied on robust builders who deliver consistent outcomes while meeting environmental regulations. As hygiene requirements escalate in commercial settings, developers should integrate SAPP strategically to achieve a balance between efficacy and compliance, positioning brands for competitive differentiation in tightening markets.

Category-wise Analysis

Product Type Insights

The food-grade segment is projected to account for approximately 62% of the sodium acid pyrophosphate market revenue share in 2026, underscoring its vital role in high-volume food production. Bakery operations have depended on it for precise leavening and uniform crumb structure, while meat processors have valued its moisture-binding to maximize yields. Instant meal producers have integrated it for reliable results amid rapid packaging and prolonged shelf life. Regulatory approvals in major regions have facilitated widespread use, as standardized recipes and automated lines demand consistent performance. This reliability has cemented its dominance in scaled food systems pursuing quality control and throughput gains.

Industrial-grade SAPP is set to achieve the fastest growth between 2026 and 2033, driven by expanding needs in water treatment and detergent sectors. Treatment plants have employed it to inhibit scale formation and enhance ion stability, safeguarding equipment and streamlining operations. Detergent formulators have leveraged its water conditioning to boost stain removal across hard water profiles. Infrastructure projects, urbanization, and industrial buildup in developing economies have intensified uptake. Businesses should prioritize this variant for its adaptability and economics, enabling seamless integration into evolving processes that demand robust, compliant solutions.

Application Insights

The food & beverages segment is projected to lead with an estimated 55% of the total consumption in 2026, underscoring its pivotal function in processed and convenience items. Bakery goods have accounted for nearly 30 percent of this uptake, as precise leavening, even crumb formation, and prolonged freshness support mass production demands. Urban growth and shifting eating habits have boosted dependence on ready meals and packaged options. Bulk purchasing, standardized recipes, and robotic lines have prioritized additives to ensure steady results, solidifying this category's position amid rising throughput needs.

Water treatment is expected to register the fastest growth between 2026 and 2033, driven by wastewater modernization at facilities in the Asia Pacific and Middle East, alongside stricter effluent controls. Operators have adopted it to prevent scale, balance ions, and streamline flows, cutting downtime and repair costs. Infrastructure booms and factory proliferation have accelerated integration of industrial-grade variants. Planners should target these dynamics by aligning supply with compliance standards, unlocking efficiencies that will sustain momentum in resource-stressed regions.

End-User Insights

The food processing industry is projected to command over 50% market share in 2026, driven by its expansive operations and reliance on functional additives to ensure uniform quality. High-capacity bakeries, meat operations, and ready-meal facilities have relied on precise rising action, water binding, and structural integrity. Uniform recipes and robotic systems have selected components that yield reliable outcomes. Enduring supplier contracts and group purchasing have enhanced integration, guaranteeing steady supply and smooth workflows across varied categories.

The pharmaceutical and cosmetics sector is poised for the swiftest growth between 2026 and 2033, driven by rising demand for excipients and innovative blending. Drug makers have sought dependable, dissolvable agents with measured responses for tablets, powders, and suspensions. Beauty formulators have employed it to sustain consistency, acidity levels, and durability. Surging trials, range extensions, and approval mandates will propel uptake. Leaders need to align R&D with these sectors to harness formulation edges and regulatory alignment for premium positioning.

Regional Insights

North America Sodium Acid Pyrophosphate (SAPP) Market Trends

North America holds a significant share of the sodium acid pyrophosphate market due to its well-established food processing and industrial sectors. The food and beverage industry drives substantial consumption, particularly in bakery, meat, and convenience foods, where consistent leavening, moisture retention, and texture stability are critical. High standards for quality control, automation, and efficiency in large-scale production facilities make functional ingredients such as this essential for maintaining uniform product performance. Strong regulatory frameworks across the United States and Canada ensure compliance and facilitate steady adoption, while collaborations between ingredient suppliers and major food manufacturers strengthen supply chains and enhance procurement efficiency.

Industrial applications also support market growth in North America, particularly in water treatment, detergents, and cleaning products. Municipal water management projects and stricter environmental regulations for industrial effluents increase reliance on phosphate-based chemicals for scale control and treatment efficiency. Detergent manufacturers and industrial cleaning operations benefit from stable performance and compatibility with varied formulations, driving steady adoption across non-food sectors. Technological advancements in manufacturing and processing, coupled with strong infrastructure development and regulatory oversight, ensure that North America remains a mature and strategically important market.

Europe Sodium Acid Pyrophosphate (SAPP) Market Trends

Europe has established itself as a vital market for SAPP, driven by a sophisticated food processing sector that prioritizes quality, safety, and standards compliance. Bakery enterprises, meat facilities, and convenience meal producers have integrated it for reliable rising action, water retention, and structural uniformity in mass operations. European shoppers have preferred packaged items that deliver superior flavor and extended freshness, sustaining robust consumption patterns. Clear directives from the European Union (EU) on additive approvals have facilitated uniform integration and bolstered enduring sourcing plans among manufacturers.

Industrial and non-food uses have further advanced SAPP demand across Europe, with water purification systems employing phosphate agents to curb scaling and balance ions effectively. Detergent creators have enhanced cleaning power and adaptability in fluctuating water profiles. EU environmental policies have promoted eco-conscious practices and wastewater management, generating steady demand for reliable chemicals. Ongoing industrial buildup, city expansions, and upgrades to public utilities will intensify uptake. Strategists should leverage these trends through localized partnerships and compliance innovations to secure sustained growth in this regulated landscape.

Asia Pacific Sodium Acid Pyrophosphate (SAPP) Market Trends

By 2026, Asia Pacific is projected to command an estimated 45% of the sodium acid pyrophosphate market share, fueled by swift urbanization, population surges, and escalating needs for processed and ready-to-eat foods. Large-scale bakery plants, meat operations, and instant meal facilities have selected it for its even rise, water-holding, and structural uniformity. Approval processes in nations such as China and India have streamlined food-grade integration, minimizing hurdles and stabilizing supply networks. Partnerships between additive suppliers and processors have optimized bulk acquisition, fostering enduring regional consumption amid capacity expansions.

The Asia Pacific market is also set to achieve the fastest growth throughout the 2026-2033 period, supported by factory proliferation, city infrastructure projects, and heightened uptake in water purification and cleaning agents. Municipal sewage improvements and rigorous factory discharge controls in countries including India, Vietnam, and Indonesia have boosted phosphate chemical dependence. Industrial hubs and middle-class spending have sparked cross-industry requirements. Developers should channel funds into blending advancements and domestic facilities to deepen penetration, securing leadership in this high-momentum arena.

Competitive Landscape

The global sodium acid pyrophosphate market structure is moderately consolidated, with leading players capturing a significant portion of market share through strong production capabilities, established distribution networks, and broad application expertise. Key players include ICL, Innophos, Grasim Industries Limited and Aditya Birla Chemicals Pvt. Ltd, Prayon, and Chongqing Chuandong Chemical Co., Ltd. These companies maintain leadership by offering high-quality food-grade and industrial-grade products, ensuring regulatory compliance across multiple regions, and leveraging technical expertise to support diverse end-use applications. Strategic investments in manufacturing efficiency, supply chain optimization, and R&D enable these players to meet large-scale industrial and food processing requirements consistently.

Mid-sized and emerging companies contribute by focusing on niche applications, regional penetration, and specialized formulations. These firms prioritize innovation in industrial water treatment, detergent applications, and functional additives for processed foods, enhancing adoption in untapped markets. Partnerships with local distributors, technical support services, and cost-effective solutions allow these companies to expand their presence in developing regions. Emphasis on sustainable production practices and formulation flexibility strengthens competitiveness, supporting overall market growth while complementing the dominance of major SAPP producers across global food and industrial sectors.

Key Industry Developments

- In August 2025, Innophos showcased at the Food Tech Summit & Expo 2025 innovations such as Cal-Rise® (SAPP/SALP alternative with less sodium), VersaCal® Bright (TiO2 replacement), LEVAIR® baking solutions, GLP-1 protein aids, and Optibind™ (STPP alternative boosting poultry yield by 19%).

- In August 2025, research on frankfurters showed that SAPP enhances texture through greater springiness, hardness, and skin formation while cutting oiliness. It also improves flavor by intensifying beef, salt, and smoke notes and toning down fat perception.

- In February 2025, Pet Honesty launched Cat Dental Powder, a mixable supplement with sodium acid pyrophosphate to slow tartar buildup, postbiotics, kelp, and a fresh-breath blend to combat plaque, support gums, and reduce bad breath in cats. It fits seamlessly into meals as part of their expanding feline wellness line.

Companies Covered in Sodium Acid Pyrophosphate (SAPP) Market

- ICL

- Innophos.

- Grasim Industries Limited and Aditya Birla Chemicals Pvt. Ltd

- Prayon

- Chongqing Chuandong Chemical Co., Ltd.

- Haifa Negev technologies LTD

- Hubei xingfa chemicals group co., LTD

- Lianyungang Dongtai Food Ingredients Co., Ltd

- Jost Chemical Co.

Frequently Asked Questions

The global sodium acid pyrophosphate market is projected to reach US$ 4.5 billion in 2026.

Rising demand from food processing, bakery, meat, and convenience food industries drives the market.

The market is poised to witness a CAGR of 4.2% from 2026 to 2033.

Expanding applications in water treatment, detergents, and industrial processes present key market opportunities for SAPP.

Key players in the market include ICL, Innophos, Grasim Industries Limited and Aditya Birla Chemicals Pvt. Ltd, Prayon, and Chongqing Chuandong Chemical Co., Ltd.