- Specialty & Fine Chemicals

- Triethyl Phosphate Market

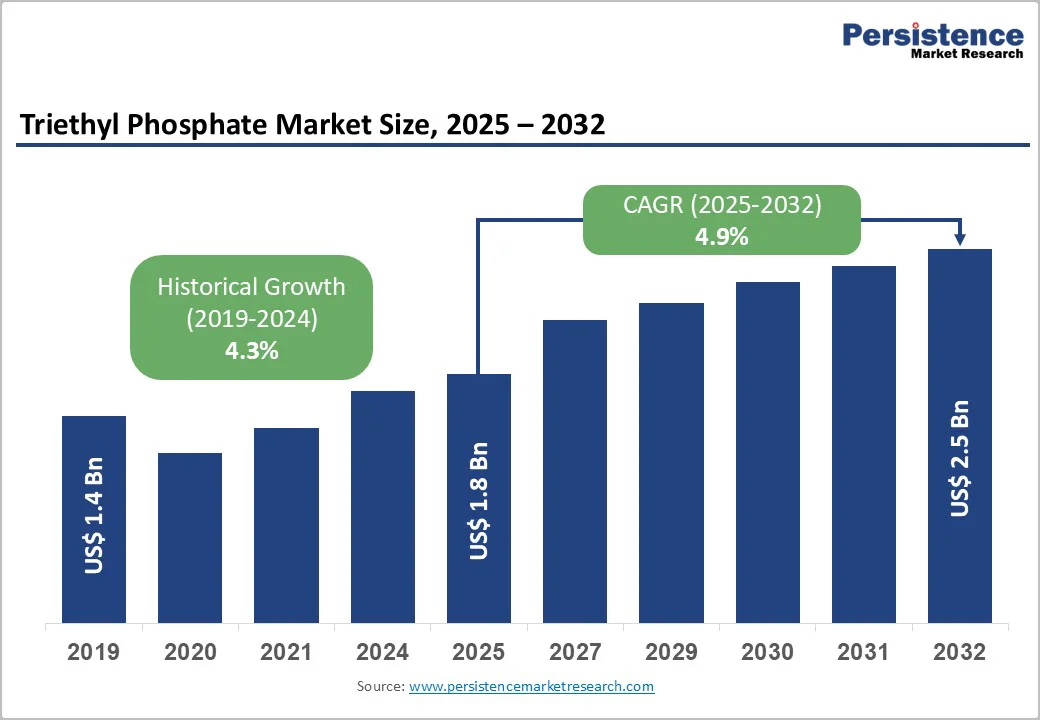

Triethyl Phosphate Market Size, Share, and Growth Forecast, 2025 - 2032

Triethyl phosphate market by Product Grade (Technical Grade, Good Grade, Pharmaceutical Grade), Application (Flame Retardants, Others), Packaging Type (Drums, Totes, Others), End-user (Electronics, Construction, Automotive, Others), and Regional Analysis for 2025 - 2032

Triethyl Phosphate Market Size and Trends Analysis

The global triethyl phosphate market size is likely to be valued at US$1.8 billion in 2025, projected to US$2.5 billion by 2032, growing at a CAGR of 4.9% during the forecast period from 2025 to 2032, driven by the increasing prevalence of flame-retardant applications, rising demand for plasticizers in polymers, and advancements in chemical synthesis.

The demand for triethyl phosphate is rising across industries due to its use as a flame retardant in electronics and as a high-purity intermediate in pharmaceuticals and specialty chemicals. Market growth is driven by innovations in technical and pharmaceutical grades, enhancing versatility and performance in applications ranging from plastics and coatings to food additives and automotive materials.

Key Industry Highlights:

- Leading and Fastest-Growing Region: Asia Pacific, commanding a 39% market share in 2025, driven by massive chemical production, high prevalence of electronics manufacturing, and strong R&D activities in China.

- Dominant Product Grade: Technical grade, holding approximately 50% of the market share, due to cost-effectiveness in industrial uses.

- Leading Application: Flame retardants, accounting for over 40% of market revenue, driven by fire safety regulations.

- Leading Packaging Type: Drums, contributing nearly 55% of market revenue, due to standard handling.

- Leading End-user: Electronics, with approximately 30% share, driven by semiconductor needs.

- Key Market Driver: Increasing focus on safety compliance and high-performance polymer processing further accelerates TEP adoption.

- Market Opportunity: Expanding applications in pharma, agrochemicals, and high-performance polymers further open high-value growth avenues.

| Key Insights | Details |

|---|---|

|

Triethyl Phosphate Market Size (2025E) |

US$1.8 Bn |

|

Market Value Forecast (2032F) |

US$2.5 Bn |

|

Projected Growth (CAGR 2025 to 2032) |

4.9% |

|

Historical Market Growth (CAGR 2019 to 2024) |

4.3% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Rising Demand for Triethyl Phosphate in Flame Retardants and Chemical Intermediates

The increasing prevalence of flame-retardant applications globally is a primary driver of the triethyl phosphate market. As fire-safety regulations become more stringent worldwide, manufacturers are increasingly shifting toward halogen-free, phosphorus-based flame retardants, where TEP plays a crucial role due to its high thermal stability and low toxicity. This shift is especially prominent in building insulation, interior materials, wiring systems, and automotive components, where flame resistance is now a mandatory requirement.

TEP is gaining traction as a versatile chemical intermediate, further accelerating market expansion. It is widely used as a catalyst, plasticizer, and solvent in specialty chemical synthesis, agrochemicals, and pharmaceuticals. Its compatibility with multiple chemical processes makes it valuable for producing organophosphates, resins, and performance additives. Industries prefer TEP as it enhances product flexibility, improves process efficiency, and enables compliance with environmental standards.

High Development and Regulatory Costs

The high costs associated with the development and regulatory approval of triethyl phosphate pose a significant restraint on market growth. Developing high-purity TEP for applications such as flame retardants, pharmaceuticals, and specialty chemical synthesis requires advanced production technologies, strict quality control, and continuous R&D investments. These processes often involve complex esterification systems, purification steps, and monitoring equipment, all of which raise operational expenses.

Regulatory compliance adds another major layer of cost. As TEP is classified under various chemical safety frameworks, companies must meet stringent standards related to environmental impact, toxicity, worker safety, and product handling. Compliance with regulations such as REACH in Europe, the EPA guidelines in the U.S., and chemical management laws across Asia requires extensive testing, documentation, and certification. These activities increase administrative and laboratory expenditures and often delay product launches.

Advancements in Bio-Based and Multi-Functional Phosphate Esters

Advances in bio-based and multifunctional phosphate esters are creating significant growth opportunities for the triethyl phosphate market. Derived from renewable feedstocks such as bio-ethanol or vegetable-based alcohols, bio-based phosphate esters offer lower toxicity and enhanced biodegradability. For example, LANXESS has introduced renewable-content phosphate esters in its bio-based plasticizer line for PVC flooring and wall coverings. These products enable manufacturers to meet EU eco-label standards while maintaining effective flame-retardant performance, demonstrating the shift from petroleum-based additives to sustainable, eco-friendly chemical solutions.

Multi-functional phosphate esters also create value by combining several performance properties into one formulation. These esters not only act as flame retardants but also serve as lubricants, anti-wear agents, and plasticizers in high-performance applications. A strong example is their adoption in electric vehicle (EV) battery components, where advanced phosphate esters provide both flame suppression and thermal stability within battery housings and cooling fluids. This dual-function capability enhances EV safety while reducing the number of separate additives required in battery manufacturing.

Category-wise Analysis

Product Grade Insights

Technical-grade triethyl phosphate is set to dominate the market, capturing 50% share in 2025. Its leadership stems from a balance of cost-effectiveness, adequate purity, and broad industrial applicability, making it the go-to choice for flame-retardant applications. For instance, LANXESS AG’s TEP (marketed as “LEVAGARD TEP-Z”) is widely used in producing polyisocyanurate (PIR) and polyurethane (PUR) foam insulation, as well as thermoset plastics, according to the company’s product-safety documentation. Its consistent performance, high-volume availability, and affordability make technical-grade TEP a preferred solution for manufacturers seeking reliable and economical flame-retardant systems.

Pharmaceutical grade is the fastest-growing segment, driven by medical needs and increasing adoption across pharmaceutical excipients. It offers sterility and high purity, making it especially appealing for drug formulations. For example, according to the U.S. Food and Drug Administration (FDA), when drug formulations involve routes such as injectable, ophthalmic, or inhalational administration, “sterility and a pyrogenicity must be ensured,” and this requirement applies not only to active pharmaceutical ingredients (APIs) but also to excipients used in the formulation. This regulatory emphasis on sterility and safety significantly boosts demand for pharmaceutical-grade materials. A strong focus on GMP-driven innovation and stringent quality standards is accelerating adoption in North America and Europe.

Application Insights

Flame retardants lead the market, holding 40% of the share in 2025, due to their essential role in enhancing polymer and plastic safety. Their strong compatibility with PVC, engineering plastics, and coatings makes them widely adopted across the construction, electronics, and automotive industries. For example, many plastics and foams used in automotive interiors are combustible; hence, manufacturers commonly add flame-retardant chemicals to meet burn-resistance requirements. This regulatory mandate creates a stable, large-volume demand for flame retardants in the automotive sector, supporting the view that flame retardant additives dominate the market share. Growing fire-safety regulations further drive demand, reinforcing their dominant market position.

Plasticizers are the fastest-growing segment, driven by rising demand for flexible, durable PVC materials across construction, automotive, and consumer goods. Their low volatility and strong compatibility with polymers enhance product lifespan and processing efficiency. As industries shift toward high-performance, adaptable materials, triethyl-phosphate-based plasticizers experience rapid adoption and expanding application potential. For example, the United States Environmental Protection Agency (EPA) notes that certain plasticizers, such as Diisononyl phthalate (DINP), are widely used “to make flexible polyvinyl chloride (PVC) and to make building and construction materials; automotive articles; and other commercial and consumer products,” underscoring their widespread industrial application and regulatory acknowledgment of their importance.

Packaging Type Insights

Drums lead the market, accounting for 55% of revenue in 2025, due to their widespread use in bulk packaging and ease of handling for industrial chemicals such as triethyl phosphate. Their durability, leak resistance, and suitability for long-distance transport make them a preferred choice for manufacturers. For instance, the U.S. Environmental Protection Agency (EPA) notes that industrial drums are used to transport a wide range of materials, including chemicals, oils, solvents, resins, acids, paints, and adhesives. This regulatory recognition highlights their reliability and versatility, reinforcing their dominance in storage and transportation.

Totes represent the fastest-growing segment, driven by their efficiency and rising adoption across modern supply chains. Their compatibility with intermediate bulk containers (IBCs) offers superior volume capacity, reduced handling time, and easier integration into automated logistics. For example, IBC tote suppliers note that IBCs offer much greater volume capacity than traditional drums. A single IBC can replace many drums at once, improving logistics efficiency and reducing handling costs. Versatile, reusable, and space-efficient designs make totes increasingly preferred for transporting chemicals such as triethyl phosphate.

End-user Insights

Electronics dominates the market, with a 30% share in 2025, driven by the critical need for circuit protection and fire-resistant components. Triethyl phosphate’s strong flame-retardant properties make it essential in wiring, circuit boards, and casings. As electronic devices become more compact and powerful, demand for safer, heat-stable materials continues to grow, reinforcing this segment’s leadership. For example, flame retardants are an important tool to help reduce fires, injuries, and deaths from fire, and property damage. They are effective in preventing fires from starting and slowing their spread once they start.

The construction segment is the fastest-growing, fueled by stringent building codes and rising adoption of flame-retardant coatings. Triethyl phosphate enhances fire resistance and durability in paints, insulation, and interior materials. Its ability to meet safety standards while maintaining long-term performance drives rapid adoption, making construction a key growth area in the TEP market. For example, foam plastic insulation (e.g., polyurethane, polyisocyanurate, other plastics/foams used in walls, ceilings, and insulation panels) is widely used in construction, but as foam plastics are combustible, they are generally treated with flame retardants to satisfy code-mandated flammability and fire resistance standards.

Regional Insights

North America Triethyl Phosphate Market Trends

North America is projected to account for nearly 24% of the share in 2025, driven primarily by demand from the flame-retardant, specialty chemical, and electronics sectors. One of the major growth drivers is the implementation of stringent fire-safety regulations in construction, automotive, and electronics industries, which is accelerating the adoption of halogen-free, phosphorus-based flame retardants such as TEP. The use of TEP as a catalyst, solvent, and chemical intermediate in specialty chemicals and pharmaceutical manufacturing is also further supporting market expansion.

Rising demand for high-purity or premium-grade TEP in advanced applications, such as battery electrolytes and electronic components, is driving manufacturers to expand production of specialized formulations. Sustainability is also shaping the market, with companies developing bio-based and low-toxicity phosphate esters to comply with environmental regulations and cater to consumer preferences for greener chemicals. Supply dynamics, including dependence on imports due to limited domestic production, continue to influence market strategies and logistics planning.

Europe Triethyl Phosphate Market Trends

Europe is driven by a strong demand for halogen-free, environmentally compliant flame-retardant solutions. Europe’s stringent regulatory framework, including REACH and advanced fire-safety standards, continues to push manufacturers toward safer, low-toxicity additives, positioning TEP as a preferred option in electronics, automotive components, construction materials, and coatings. The region is also witnessing a rising adoption of high-purity TEP grades used in specialty chemical synthesis, pharmaceuticals, and agrochemicals, reflecting the continent’s growing emphasis on precision manufacturing and high-performance intermediates.

Sustainability trends are shaping market direction, as European producers increasingly focus on greener, bio-based phosphate esters to meet environmental and circular-economy goals. While regulatory compliance and production qualification processes add cost and complexity, they simultaneously encourage innovation in advanced, safer formulations. Regulatory guidance from the European Medicines Agency (EMA) similarly requires that excipients used in medicinal products meet defined quality standards, and any use of novel excipients (or excipients via new administration routes) must be clearly evaluated before approval.

Asia Pacific Triethyl Phosphate Market Trends

Asia Pacific is the dominant market, accounting for 39% of the share in 2025, due to the rising demand from key end-use industries such as flame retardants, agrochemicals, plastics, and pharmaceuticals. Countries such as China, India, Japan, and South Korea are expanding their chemical manufacturing capacities, which drives large-scale consumption of TEP as both a flame-retardant additive and a solvent. Rapid industrialization and growing construction activities in China and Southeast Asia are increasing the need for fire-safety materials, strengthening TEP demand in flame-retardant applications.

The region is also a global hub for agrochemical production, and TEP is frequently used as an intermediate in pesticide formulations, further accelerating market expansion. Supportive government initiatives promoting chemical manufacturing, along with rising investments in specialty chemicals and export-oriented production, position Asia Pacific as the fastest-growing regional market. The growing pharmaceutical and textile sectors, which use TEP as a plasticizer and catalyst, are contributing to continuous demand growth.

Competitive Landscape

The global triethyl phosphate (TEP) market is highly competitive, comprising multinational chemical giants and specialized producers targeting niche applications. In mature regions such as North America and Europe, companies such as Eastman Chemical and Huntsman Corporation dominate, leveraging advanced R&D, robust distribution networks, and strong industry partnerships. They focus on enhancing flame-retardant performance, cleaner production, and high-purity grades for pharmaceuticals and electronics.

In Asia, major manufacturers such as Mitsubishi Chemical drive rapid growth through localized production, cost-efficient technologies, and integrated supply chains. The market is increasingly shaped by sustainable chemistry and bio-based innovations to meet stringent environmental regulations. Strategic collaborations, mergers, acquisitions, and capacity expansions are critical for capturing rising demand across agrochemicals, plasticizers, and specialty chemicals.

Key Industry Developments

- In March 2025, Eastman announced a price increase for its ester products, which likely impacts its TEP-related portfolio.

Companies Covered in Triethyl Phosphate Market

- Eastman Chemical Company

- Huntsman Corporation

- BASF SE

- Solvay SA

- Lanxess AG

- Kraton Corporation

- Perstorp Holding AB

- Mitsubishi Chemical Corporation

Frequently Asked Questions

The global triethyl phosphate market is projected to reach US$1.8 billion in 2025.

The primary drivers are the rising demand for flame retardants in polymers and electronics, increasing use of plasticizers and antifoaming agents, and growing applications as pharmaceutical excipients and food additives.

The triethyl phosphate market is expected to grow at a CAGR of 4.9% from 2025 to 2032.

Major opportunities lie in the development of bio-based and multi-functional phosphate esters, expanding applications in green flame retardants, and rising demand for high-purity pharmaceutical-grade triethyl phosphate.

Leading companies include Eastman Chemical Company, Huntsman Corporation, BASF SE, Solvay SA, Lanxess AG, Kraton Corporation, Perstorp Holding AB, and Mitsubishi Chemical Corporation.