- Specialty & Fine Chemicals

- Ammonium Polyphosphate (Phase II) Market

Ammonium Polyphosphate (Phase II) Market Size, Share, and Growth Forecast, 2026 - 2033

Ammonium Polyphosphate (Phase II) Market by Product Type (Melamine Coating, Silane Coating, Non-Coated), Form (Powder, Liquid, Granule), End-user Industry (Construction, Textiles, Electronics), Application (Flame Retardant, Others), and Regional Analysis 2026 – 2033.

Ammonium Polyphosphate (Phase II) Market Size and Trends Analysis

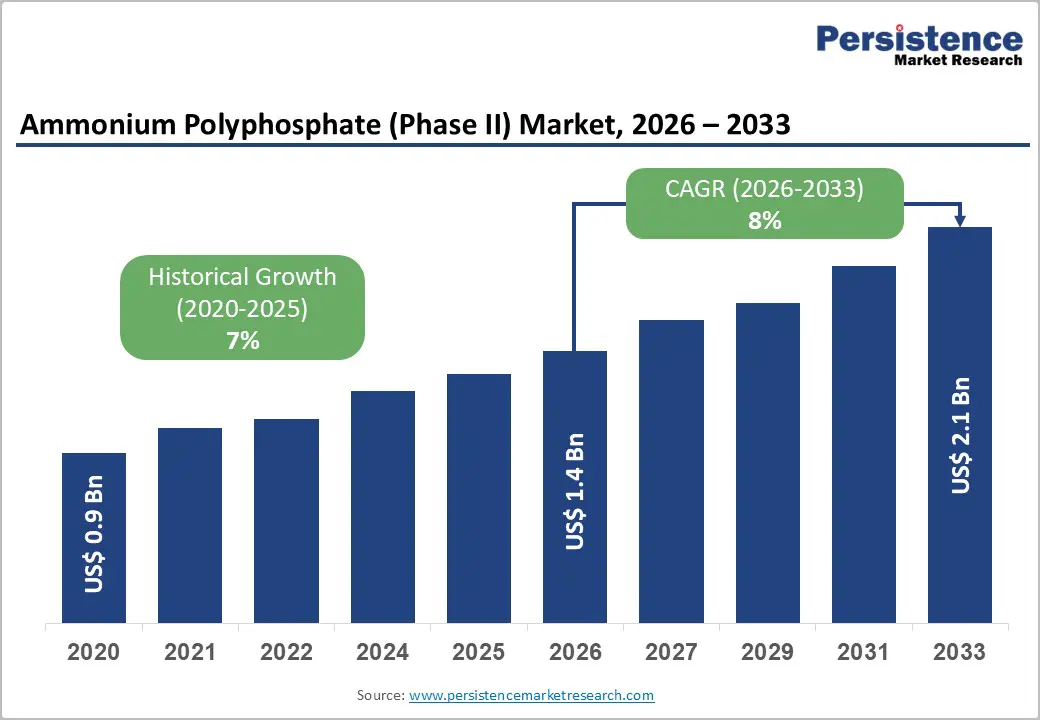

The global ammonium polyphosphate (Phase II) market size is projected to be valued at US$1.4 billion in 2026 and is projected to reach US$2.1 billion by 2033, growing at a CAGR of 8% during the forecast period from 2026 to 2033, driven by accelerating fire safety regulations across the construction, automotive, textiles, and electronics sectors.

The chemical's superior thermal stability, non-toxicity, and halogen-free properties position it as the preferred alternative to traditional brominated flame retardants. The burgeoning Electric Vehicle (EV) market is creating a specialized niche for high-purity ammonium polyphosphate (Phase II) in battery casing insulation, where traditional materials fail to meet stringent thermal runaway requirements.

Key Industry Highlights:

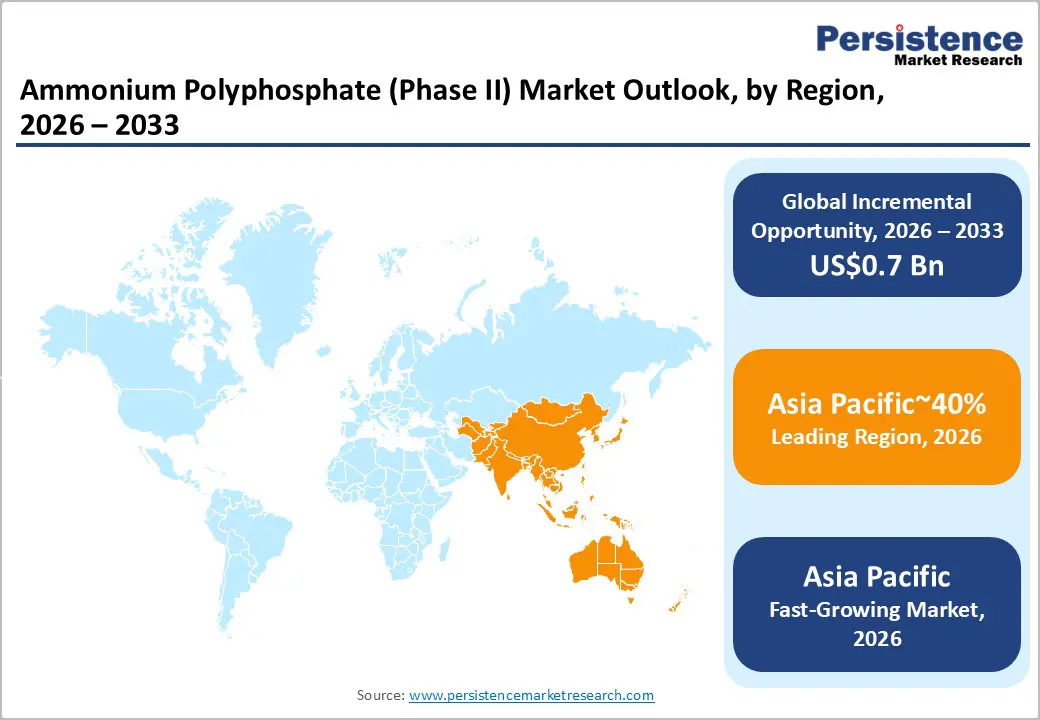

- Leading Region: Asia Pacific is projected to remain the leading region in the ammonium polyphosphate market, accounting for approximately 40% of the global demand.

- Leading Product Type: Melamine-coated ammonium polyphosphate is anticipated to lead with around 50% share, driven by superior thermal stability, low smoke emission, and compliance with halogen-free regulations in high-performance plastics and EV battery applications.

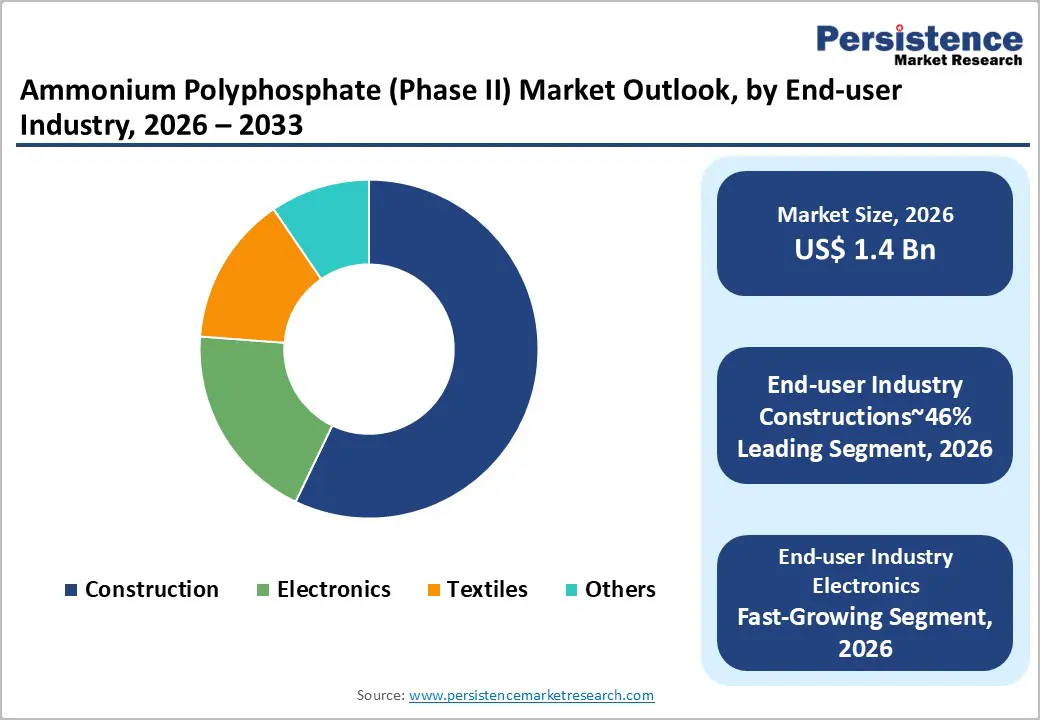

- Leading End-user: Construction is expected to remain the leading end-user with approximately 60% share, anchored by non-halogenated fire safety solutions, mass timber adoption, and integration in insulation panels and coatings.

- Key Industry Developments: In October 2025, Ahlstrom introduced its Flame-Gard™ technology for high-performance industrial flame-retardant papers, expanding the use of liquid Ammonium Polyphosphate (Phase II) into the paper and packaging sectors with a focus on its non-toxic and eco-friendly benefits.

| Key Insights | Details |

|---|---|

| Ammonium Polyphosphate (Phase II) Market Size (2026E) | US$ 1.4 Bn |

| Market Value Forecast (2033F) | US$ 2.1 Bn |

| Projected Growth (CAGR 2026 to 2033) | 8% |

| Historical Market Growth (CAGR 2020 to 2025) | 7% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rapid Industrialization and Construction Expansion in Emerging Markets

Asia Pacific’s accelerated industrialization and urban expansion are structurally intensifying demand for flame-retardant materials, with construction and infrastructure investment acting as the primary volume drivers. China, India, and Southeast Asia are scaling residential, commercial, and industrial builds in parallel with manufacturing localization agendas, reinforcing baseline consumption of fire-resistant coatings, insulation, and adhesive systems. Construction-linked demand is further amplified by the region’s concentration of electronics and automotive manufacturing, where component-level fire protection is increasingly non-negotiable. This convergence positions ammonium polyphosphate as a cost-efficient, regulation-aligned solution within high-throughput applications, translating infrastructure activity directly into sustained material offtake.

Regulatory tightening and performance standardization are reinforcing this demand trajectory by elevating compliance thresholds across emerging markets. National fire codes, urban safety mandates, and export-oriented manufacturing requirements are compressing substitution flexibility and favoring phosphorus-based, halogen-free formulations. While price sensitivity remains a structural constraint, scale advantages and localized production are mitigating margin pressure for established suppliers. As a result, construction-led growth in emerging economies is evolving from cyclical expansion into a multi-decade demand foundation, with technology-qualified ammonium polyphosphate formulations increasingly embedded across regional value chains.

Raw Material Price Volatility and Supply Chain Constraints

Volatility in phosphoric acid and ammonia pricing represents a persistent structural headwind for ammonium polyphosphate producers, directly compressing margins and complicating cost pass-through mechanisms. Feedstock exposure to polyphosphate rock supply disruptions, amplified by fertilizer-sector policy interventions and export controls, transmits instability across the flame-retardant value chain. These dynamics disproportionately affect small and mid-scale manufacturers with limited hedging capacity, while also elevating procurement risk for downstream formulators operating under fixed-price contracts.

Supply chain fragmentation is further intensifying these pressures by undermining operational efficiency and capital discipline. Geopolitical tensions, tariff realignments, and regional trade restrictions are forcing manufacturers to rebalance sourcing strategies and maintain higher safety inventories, increasing working capital intensity. In price-sensitive developing markets, this cost inflation constrains the adoption of ammonium polyphosphate formulations where substitute materials remain available. Collectively, raw material volatility and logistics uncertainty are reinforcing scale advantages for integrated suppliers, while structurally raising entry barriers and limiting flexibility across the broader competitive landscape.

Emergence of Bio-based and Sustainable Flame Retardant Solutions

The accelerating green chemistry transition is creating a structurally attractive opportunity for ammonium polyphosphate Phase II manufacturers as regulators systematically eliminate organ-halogen flame retardants from high-risk applications. Regulatory actions by the U.S. EPA and ECHA are reshaping procurement standards across consumer goods, electronics, and medical devices, opening a clearly defined market gap for certified low-toxicity alternatives. Demand is increasingly concentrated in bio-compatible and low-leaching formulations, where compliance capability and materials science differentiation determine supplier eligibility. Advances in micro-encapsulation technologies, particularly eco-resin coatings, are reinforcing ammonium polyphosphate’s moisture resistance and polymer compatibility, translating regulatory alignment directly into higher-value end-market access.

In May 2025, Fraunhofer WKI and Clariant Unveil "Scaleup" Bio-Based Ammonium Phytate Retardants as Plant-Derived Alternatives to Synthetic Halogenated Additives. This development directly addresses the US$ 450 million market gap created by the phase-out of organ halogens; by utilizing plant-derived phytic acid (ScaleAmP) and melamine-free ammonium polyphosphate phase II (Exolit AP 422), manufacturers can now offer low-leaching, bio-compatible certifications essential for securing contracts in the high-end medical device and sustainable consumer electronics sectors.

Category–wise Analysis

Product Insights

Melamine-coated ammonium polyphosphate is projected to dominate the global ammonium polyphosphate market with approximately 50% share, driven by its superior thermal stability, low toxicity, and minimal smoke emission. Recent industrial updates include BASF’s €100 million expansion to increase melamine output by 50,000 metric tons per year and the introduction of PFAS-free “Total Green” additives by Clariant AG and Eurotecnica, reducing carbon footprints at significant levels. Key drivers include global halogen-free regulations, the performance stability offered by melamine coatings at temperatures up to 300°C, and surging demand from EV battery packs and high-performance plastics. Industrial trends involve hybrid synergist systems combining ammonium polyphosphate with zinc borate or expandable graphite, nanocomposite integration for mechanical toughness and UV stability, and dominance of solid forms for transport and automation compatibility.

Silane-coated ammonium polyphosphate (SAPP) is anticipated to be the fastest-growing segment, leveraging silane coupling agents to chemically bond ammonium polyphosphate to organic polymers, improving mechanical and thermal performance. Recent updates include nano-scale SAPP products by Sanwa Flame Retardant Technology with higher thermal stability, and bio-composite integrations with PLA/rice husk, achieving UL 94 V-0 ratings. Key growth drivers are interfacial bonding that restores tensile strength, hydrophobicity enhancing outdoor durability, and compliance with LSZH requirements for cables and wiring. Factors influencing adoption include superior dispersion, viscosity control for coatings, and denser char formation for fire protection. Industrial trends involve hybrid synergists, sol-gel coating techniques for uniform layers, and eco-label compliance (TCO Certified, Blue Angel). Leading suppliers include Clariant AG (Exolit®), Sanwa Flame Retardant Technology, g, JLS Chemical, and high-volume Chinese producers such as Shifang Changfeng Chemical and Kingssun Group.

End-user Insights

The construction sector is anticipated to remain the leading end-user of ammonium polyphosphate, commanding around 60% share of global demand. This dominance is supported by the rising adoption of non-halogenated fire safety solutions in modern infrastructure. Recent updates include mass timber construction driving a 15% increase in liquid and powder ammonium polyphosphate usage, nano-ammonium polyphosphate coatings for structural steel reducing required coating thickness by 30%, and pre-integrated ammonium polyphosphate in insulation panels for combined thermal and fire performance. Clariant AG (Exolit® AP series), Budenheim, Hubei Xingfa Chemicals, and Perimeter Solutions are expected to continue supplying both high-purity powders and masterbatch pellets. Emerging trends include lignin-based bio-synergists, dust-free masterbatches, and multi-functional coatings offering fire, UV, and anti-corrosion protection. Ammonium polyphosphate is also increasingly applied in HVAC duct insulation and acoustic foams, enhancing sound dampening. Phosphate price volatility remains a key consideration, as an increase in raw phosphorus can raise total construction material costs by around 5%.

The electronics segment is projected to be the fastest-growing end-user, driven by the global shift to halogen-free flame retardants for consumer electronics and EV components. Nano-ammonium polyphosphate products from Sanwa Flame Retardant Technology improve thermal stability, while Ampacet and Clariant provide HFFR masterbatches and melamine-free grades such as Exolit® AP 422 A. The key drivers include 5G infrastructure, high-voltage EV systems, and miniaturized electronics requiring UL 94 V-0 compliance in sub-millimetre housings. AI-based formulation tools, microencapsulation for hydrolysis protection, and upstream phosphate integration by Nutrien are expected to accelerate adoption. Leading suppliers for high-purity and technical-grade ammonium polyphosphate include Clariant, Sanwa Flame Retardant, Budenheim, and ICL Group, addressing applications across cables, adhesives, foams, and circuit board laminates in Asia, Europe, and North America.

Regional Insights

Asia Pacific Ammonium Polyphosphate (Phase II) Market Trends

Asia Pacific is expected to remain the leading and fastest-growing regional market, accounting for roughly 40% of global demand, supported by scale-driven consumption and accelerating industrial activity. China anchors regional volume through construction intensity, manufacturing concentration, and electronics production, while Japan contributes stable, high-value demand from automotive and advanced electronics supply chains. India represents the fastest-growing submarket, with infrastructure expansion, smart city programs, and evolving building codes reinforcing structural demand. Collectively, these dynamics position the region ahead of North America and Europe on growth velocity, while maintaining cost and capacity advantages across the value chain.

Regulatory evolution and industrial policy are progressively shaping competitive outcomes across Asia Pacific. Fire safety standards are tightening through ISO alignment and national code upgrades, although enforcement remains uneven, creating a bifurcated market between cost-competitive local suppliers and compliance-driven premium offerings. Manufacturing localization initiatives, including China’s industrial upgrading and India’s Make in India agenda, are strengthening regional supply capability. Rising electric vehicle production further concentrates demand for battery-safety materials, reinforcing Asia Pacific’s role as both the primary consumption base and the most strategically attractive investment destination.

North America Ammonium Polyphosphate (Phase II) Market Trends

North America is expected to account for roughly 20% of global demand, reflecting a mature market characterized by established regulatory frameworks, high safety standards, and advanced supply chain infrastructure. The U.S. anchors regional consumption, supported by post-2020 construction recovery, strict residential building codes, and industrial safety mandates, while Canada contributes incremental demand from energy infrastructure and resource-linked construction. Market growth is steady rather than rapid, with scale constrained by maturity but supported by a large, regulation-driven addressable base and consistent replacement demand across construction and industrial applications.

Regulatory and risk-management considerations remain the primary demand drivers, reinforced by state-level fire safety codes, energy efficiency standards, and insurance-led specification requirements favoring halogen-free solutions. Electrification of the automotive sector within the USMCA zone is emerging as a secondary growth lever, increasing demand for high-performance flame-retardant polymers. Competitive positioning emphasizes technical service, regulatory documentation, and distributor reach, enabling margin stability. Investment activity is selectively focused on specialty platforms, digital manufacturing upgrades, and e-mobility-related flame-retardant systems rather than capacity-led expansion.

Europe Ammonium Polyphosphate (Phase II) Market Trends

Europe is expected to remain a mature, regulation-led market, accounting for approximately 25% of global demand, underpinned by stringent compliance frameworks and high-value application intensity. The region’s market structure is shaped by EU-wide REACH requirements, national fire safety codes, and Green Deal sustainability mandates, which collectively elevate technical thresholds for material adoption. Germany anchors regional consumption and production, supported by established chemical manufacturing infrastructure and advanced construction standards, while France, the U.K., Italy, and Spain contribute steady demand through renovation-led construction and infrastructure modernization. Growth is incremental rather than volume-driven, reflecting market maturity and rigorous qualification cycles.

Regulation functions as the primary market-shaping force across Europe, systematically restricting brominated and high-risk chemistries while favouring halogen-free phosphorus-based solutions. EN fire classification standards and the SVHC designation process are accelerating reformulation activity, reinforcing demand for compliant ammonium polyphosphate formulations in construction, transportation electrification, and advanced composites. Competitive differentiation is concentrated on regulatory expertise, technical service depth, and sustainability credentials, sustaining premium pricing and positioning Europe as a value-driven, compliance-intensive market rather than a scale-led growth region.

Competitive Landscape

The global ammonium polyphosphate (phase II) market exhibits moderate to high concentration, with the top five players controlling roughly 45–50% of total revenue, led by Clariant AG, Budenheim KG, and Thor Group through integrated manufacturing, long-standing production expertise, and established customer relationships across coatings, foams, and thermoset applications. High-purity technical grades remain highly concentrated, while standard industrial grades are more fragmented, particularly across China and India, where regional suppliers leverage cost-competitive offerings to capture volume-driven segments. Competitive advantage is increasingly determined by technological differentiation, including proprietary coating methods, application-specific formulation expertise, and compliance with regulatory frameworks such as REACH, which collectively reinforce market positioning and limit meaningful substitution risks.

Market structure is characterized by substantial entry barriers, encompassing capital-intensive manufacturing infrastructure, technical expertise requirements, and comprehensive safety and regulatory documentation. Emerging regional competitors and gradual consolidation among smaller players indicate incremental structural shifts, yet established suppliers maintain a durable competitive moat. Forward dynamics suggest sustained demand for high-performance flame retardants, technology-led differentiation, and selective adoption of industrial-grade AP products in cost-sensitive regions.

Key Industry Developments:

- In April 2025, Clariant celebrated 50 years of Exolit® AP and made a strategic pivot toward Melamine-Free ammonium polyphosphate Phase II Solutions. This marked a major shift in the ammonium polyphosphate Phase II market toward "Substances of Very High Concern" (SVHC)-free alternatives, directly addressing the growing demand for safer, non-leaching intumescent coatings in the construction and EV sectors.

- In November 2024, Budenheim achieved UL 94 V-0 certification for recycled polypropylene using specialized Melamine-Phosphorus ammonium polyphosphate compounds. This proved the viability of ammonium polyphosphate Phase II in high-performance recycled materials and opened a new revenue stream in the "Circular Economy" segment, where traditional flame retardants often failed to maintain performance.

- In November 2024, the British Standards Institution (BSI) fully revamped the residential fire safety code BS 9991:2024. This regulatory update acted as a massive market driver for intumescent coatings containing ammonium polyphosphate Phase II, as it mandated higher fire resistance durations for residential high-rises and care homes.

- In April 2024, Trinseo introduced High-Performance PFAS-Free Flame Retardant Polycarbonate Resins for consumer electronics. It demonstrated the industry-wide move away from fluorinated "forever chemicals," creating a vacuum that phosphorus-based additives such as ammonium polyphosphate Phase II increasingly filled in the $11B electronics sector.

Companies Covered in Ammonium Polyphosphate (Phase II) Market

- Clariant AG

- Budenheim

- Ahlstrom

- Innophos

- Nabaltec

- Albemarle Corporation

- Fraunhofer WKL

- Shifang Changfeng Chemical

- BASF SE

- Trinseo

- Zhejiang Longyou Shenghe

- Aquaspersions

- Shandong Taixing Fine Chemical

- Bisley International

- ICL Group

- Lanxess AG

Frequently Asked Questions

The global ammonium polyphosphate (phase II) market is projected to be valued at US$1.4 billion in 2026 and is expected to reach US$2.1 billion by 2033.

Demand is accelerating due to tightening fire safety regulations, the shift toward non-halogenated flame retardants, and rising adoption in construction, electronics, textiles, and electric vehicle battery insulation applications.

The ammonium polyphosphate (phase II) market is expected to grow at a CAGR of 8.0% between 2026 and 2033, supported by regulatory compliance requirements and high-performance material demand.

The strongest growth opportunities are emerging in Asia Pacific, led by China’s construction and manufacturing scale.

The leading players in the ammonium polyphosphate (phase II) market include Clariant AG, Budenheim, Nabaltec AG, BASF SE, ICL Group, Lanxess AG, Shandong Taixing Fine Chemical, and other regional specialty manufacturers.