- Agrochemicals

- Phosphate Rocks Market

Phosphate Rocks Market Size, Share, and Growth Forecast 2026 - 2033

Phosphate Rocks Market by Source (Marine, Igneous, Metamorphic, Biogenic, Weathered), End-User (Fertilizers, Food Additives, Animal Feed Supplements, Pharmaceuticals, Electronics, Chemicals, LFP Battery, Others), and Regional Analysis for 2026 - 2033

Phosphate Rocks Market Size and Trend Analysis

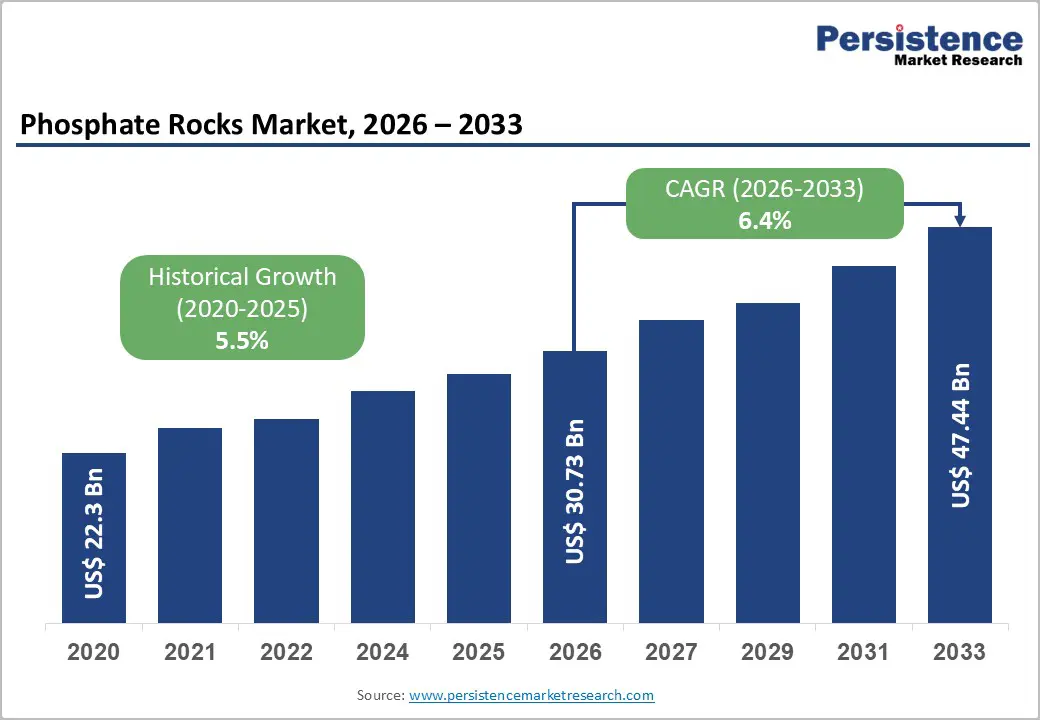

The global phosphate rocks market size is supposed to be valued at US$ 30.7 Bn in 2026 and is projected to reach US$ 47.4 Bn by 2033, growing at a CAGR of 6.4% between 2026 and 2033.

Market expansion is fundamentally driven by escalating global food demand and intensifying agricultural production across emerging economies. According to the United States Geological Survey, global phosphate rock production reached approximately 240 million metric tons in 2024, reflecting consistent demand from the fertilizer sector. Population growth and rising per capita meat consumption create immediate pressure on agricultural productivity, necessitating increased phosphorus inputs through phosphate-based fertilizers. Additionally, the rapid transition toward electric vehicles and lithium iron phosphate (LFP) battery technology represents a significant emerging demand stream. Phosphate rock is a critical feedstock for producing cathode active materials in next-generation energy storage systems, which are anticipated to command substantial market share during the forecast period.

Key Industry Highlights:

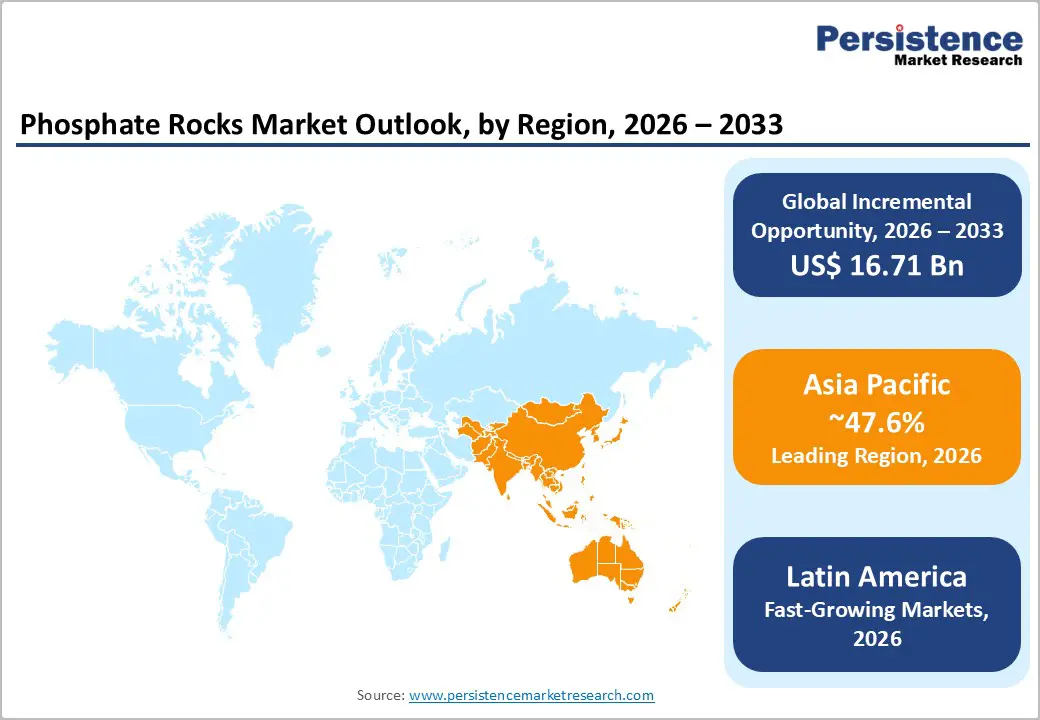

- Leading Region: Asia-Pacific dominates the global phosphate rocks market with 47.6% market share, driven by China's overwhelming production and consumption dominance at 110 million metric tons annually, combined with expanding agricultural sectors in India and ASEAN nations pursuing food security and precision farming objectives.

- Fastest-Growing Region: Latin America demonstrates accelerating phosphate demand growth driven by record agricultural harvests in Brazil and Argentina, expanded livestock production for export markets, and adoption of advanced farming technologies, with Brazil alone consuming 34.1% of regional feed phosphate demand and driving regional market expansion.

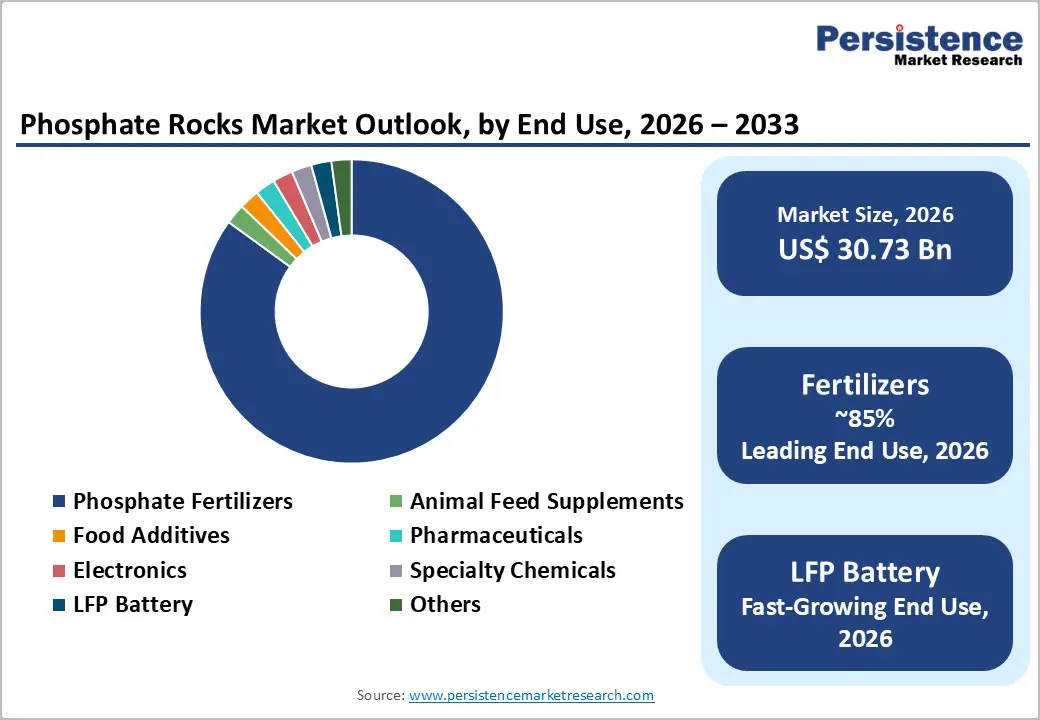

- Dominant Segment: Phosphate fertilizers command overwhelming market dominance, consuming approximately 85% of globally mined phosphate rock, reflecting the irreplaceable role of phosphorus in supporting agricultural productivity and feeding the world's expanding population through cereal, oilseed, vegetable, and specialty crop production systems.

- Fastest Growing: The LFP battery market, growing at 17.2% CAGR through 2034, requires an additional 2.5 million tons of phosphoric acid annually, creating premium-priced specialized demand opportunities beyond traditional commodity fertilizer segments for producers capable of supplying ultra-high-purity materials.

- Key Market Opportunity: Phosphogypsum recycling and circular economy technology development offer substantial commercial opportunities for market participants capable of converting 200-250 million metric tons of annually generated phosphogypsum waste into valuable secondary products, including recovered sulfuric acid, quicklime for construction applications, and recovered phosphate compounds, while simultaneously addressing environmental regulatory mandates.

| Key Insights | Details |

|---|---|

| Phosphate Rocks Market Size (2026E) | US$ 30.7 Bn |

| Market Value Forecast (2033F) | US$ 47.4 Bn |

| Projected Growth CAGR (2026-2033) | 6.4% |

| Historical Market Growth (2020-2025) | 5.5% |

Market Dynamics

Drivers

Agricultural Intensification and Precision Farming Adoption

Global phosphate fertilizer consumption closely aligns with the intensification of global food production and the growing dependence on phosphorus across agricultural systems. According to the FAO, agricultural phosphorus use reached nearly 42 million metric tons in 2022, with continued growth across developing regions. Approximately 30% of the world’s agricultural soils exhibit phosphorus deficiency, particularly within heavily cultivated areas of Asia and Africa, sustaining demand for high-grade phosphate rock.

Advancements in precision agriculture, such as variable-rate application and controlled-release fertilizers, have reduced phosphate overuse by up to 40% while improving nutrient efficiency by 25%. With 22% of global farmland adopting precision techniques and genetically modified crops occupying over 13% of agricultural land, demand for high-purity phosphate rock continues to strengthen as modern farming requires increasingly sophisticated fertilizer formulations.

Emerging Demand from Electric Vehicle Battery Production

Lithium iron phosphate (LFP) batteries have become the fastest-growing segment of the global battery industry, accounting for roughly 38% of total lithium-ion battery production in 2024. Their rapid expansion is driven by superior cost efficiency, longer cycle life, and enhanced safety relative to conventional battery chemistries. Phosphate rock plays a pivotal role as a primary raw material for producing cathode active materials used in LFP systems, creating a distinct and growing demand channel beyond traditional fertilizer applications.

Major industry participants are investing heavily to capitalize on this emerging battery materials market. By 2050, projected global production of more than 200 million light electric vehicles per year could require more than 3 million metric tons of phosphorus, equivalent to approximately 5% of current global phosphate mining capacity. This accelerating demand is expected to generate substantial revenue opportunities, intensifying competition for premium-grade phosphate rock suitable for advanced battery applications.

Restraints

Geographic Concentration and Supply Chain Vulnerability

Global phosphate rock reserves are heavily concentrated in a few countries: Morocco and Western Sahara together control more than 70% of the world’s known reserves, while China, the United States, and Russia account for most of the remaining economically accessible deposits. This high geographical concentration creates significant supply-chain vulnerability and elevates geopolitical risk. Morocco alone produces approximately 30.5 million metric tons of beneficiated phosphate rock annually and exerts considerable influence over global pricing for high-grade phosphate supplies.

The Mosaic Company experienced a production loss of around 700,000 metric tons in 2024 due to weather events and maintenance issues, demonstrating how localized challenges can trigger broader global repercussions. Historically, such supply limitations have led to extreme price volatility, with spikes exceeding 800% during periods of acute shortages, creating substantial uncertainty for downstream fertilizer producers and other end-users reliant on stable input costs.

Environmental Regulations and Reserve Depletion Concerns

Phosphate rock mining produces significant environmental externalities, including habitat disruption, water pollution, and air quality degradation, which have led to increasingly stringent regulatory measures across developed regions. In 2020, the European Union classified phosphate rock as a critical raw material, implementing reduction targets and promoting alternative sourcing strategies.

Phosphogypsum, a byproduct of phosphoric acid production, generates an estimated 200-250 million metric tons of waste annually, of which only about 15% is currently recycled, creating escalating disposal and environmental liability concerns. Reserve depletion assessments indicate that economically extractable global phosphate rock reserves total approximately 74 billion metric tons, compared with current annual production of around 240 million metric tons. Furthermore, research published in Nature reports that only about 30% of applied phosphorus is absorbed by plants, highlighting substantial inefficiencies that increase pressure on finite reserves and intensify environmental risks associated with nutrient runoff and eutrophication.

Opportunities

Phosphogypsum Recycling and Circular Economy Innovation

The phosphogypsum recycling sector offers a significant opportunity for companies aiming to address environmental challenges while generating value from previously discarded byproducts. Advanced recycling technologies, including microbial-based treatment systems and innovative calcination methods, can recover phosphorus from phosphogypsum with efficiencies of up to 95%, while producing secondary outputs such as quicklime and sulfuric acid for reuse in phosphoric acid production.

Ma'aden Phosphate in Saudi Arabia is developing a dedicated recycling facility in partnership with thyssenkrupp Uhde and Metso Outotec to recover sulfuric acid and convert phosphogypsum into construction-grade limestone while capturing carbon emissions. With 200-250 million metric tons of phosphogypsum generated annually, substantial global potential exists. Companies that deploy cost-effective, compliant technologies will benefit as regulations increasingly shift from disposal to the mandatory utilization of waste.

Rapid Agricultural Expansion in Emerging Economies and Feed Phosphate Growth

India and Brazil are the fastest-growing centers of phosphate rock demand globally, driven by expanding agricultural sectors focused on achieving food security and by rising livestock production to meet domestic protein requirements. India, which relies heavily on phosphate rock imports due to limited domestic reserves, issued a tender for 44,000 metric tons of high-grade phosphate rock in 2025, indicating sustained procurement demand to support fertilizer production and animal feed supplement manufacturing. Brazil's phosphate consumption increased from just over 3.5 million metric tons of P-O- in 2010 to approximately 7.5 million metric tons in 2021, reflecting sustained agricultural expansion.

Agricultural policy initiatives in India and Brazil that emphasize productivity gains, coupled with rising per capita meat consumption, are expected to drive sustained double-digit growth in phosphate rock imports over the forecast period. Industry participants developing reliable supply partnerships and establishing downstream processing capacity in these emerging economies will benefit from growing demand density and first-mover advantages in capturing market share within rapidly expanding agricultural sectors.

Category-wise Analysis

Source Insights

Marine phosphorite deposits account for nearly 75% of global phosphate rock production, supported by their wide geographic distribution and favorable beneficiation characteristics. These sedimentary deposits form through paleoceanographic processes involving biological productivity and phosphatization of calcium carbonate sediments, typically containing 4-20% P-O- before processing. Their accessibility and suitability for surface mining in regions such as Morocco, Jordan, Peru, and Australia reinforce their dominant position, with beneficiated ores reaching 28-35% P-O- through screening, washing, deliming, magnetic separation, and flotation.

Igneous apatite deposits, found mainly in Russia, China, and Brazil, account for approximately 25% of the supply and offer higher ore grades, although their limited distribution and complex genesis constrain output. Metamorphic, biogenic, and weathered deposits contribute minimally, having been surpassed by large-scale marine and igneous operations.

End-user Insights

Phosphate fertilizers constitute the dominant end-use segment, consuming nearly 85% of globally mined phosphate rock and underscoring phosphorus’s essential role in sustaining agricultural productivity and global food security. Phosphate rock is converted into phosphoric acid through wet-process and thermal methods, and subsequently used to produce key fertilizers such as monoammonium phosphate (MAP) and diammonium phosphate (DAP), which support major cereal, oilseed, and vegetable production systems.

Animal feed supplements, including monocalcium phosphate (MCP) and dicalcium phosphate (DCP), account for about 10% of consumption, driven largely by expanding livestock and poultry production across Asia-Pacific and Latin America. The remaining 5% serves diverse industrial applications, including food additives, pharmaceuticals, electronics, and specialty chemicals. Emerging demand for lithium iron phosphate (LFP) batteries is expected to gradually expand consumption in specialty segments over the forecast period.

Regional Insights

North America Phosphate Rocks Market Trends

The North American phosphate rock market remains mature and stable, supported by integrated mining and processing operations that dominate the U.S. industry. The Mosaic Company, operating nine mines across Florida, North Carolina, Idaho, and Utah, is the leading producer, generating about 20 million metric tons of marketable phosphate rock annually, with 6.4–7.6 million metric tons of phosphate products expected in 2025–2026. The Florida region, contributing roughly 63% of domestic capacity, benefits from fully integrated mining, phosphoric acid, and fertilizer production facilities, ensuring value-chain efficiency and supply security.

Regional demand reflects a mature agricultural sector, in which growth primarily stems from crop intensification and the adoption of precision farming. CF Industries is advancing carbon-capture initiatives in Louisiana and Mississippi, while rising demand for lithium iron phosphate battery materials creates new opportunities for premium-grade phosphate supply.

Europe Phosphate Rocks Market Trends

The European phosphate rock market is characterized by high import dependence and a strong regulatory focus on circular-economy principles and critical-mineral security. Following the European Union's designation of phosphate rock as a critical raw material in 2020, the region has accelerated strategic sourcing efforts and the development of alternative phosphorus recovery technologies. Despite substantial fertilizer consumption across Germany, France, Spain, and the U.K., Europe possesses limited domestic reserves and relies heavily on imports from Morocco, Jordan, Egypt, and other North African and Middle Eastern suppliers.

Increasing regulatory restrictions on phosphorus use in detergents and wastewater treatment, combined with requirements for enhanced phosphorus removal and the adoption of precision agriculture, reinforce this shift. Emerging recycling innovations, such as PhosCycle’s recovery of phosphate fertilizer from expired fire extinguisher powder, and the introduction of the Carbon Border Adjustment Mechanism (CBAM) are expected to influence production costs, trade dynamics, and investment in low-carbon, circular phosphorus solutions.

Asia Pacific Phosphate Rocks Trends

Asia-Pacific is the leading region for phosphate rock production and consumption, accounting for approximately 47.6% of global demand, owing to extensive agricultural activity and the need to support food security for over 4.6 billion people. China dominates regional output, producing 110 million metric tons in 2024, around 98% of the region’s total, and consuming 94% domestically to sustain large-scale cereal, oilseed, and vegetable cultivation. Its focus on agricultural modernization has driven continuous investment in integrated mining-to-fertilizer operations operated by major producers.

India is the second-largest market, using 9-10 million tons of phosphate fertilizers annually, supported by policy reforms promoting balanced NPK use. Import-dependent countries such as Japan, South Korea, and Southeast Asian nations continue securing long-term supply contracts. The region is expected to remain the fastest-growing through 2033.

Competitive Landscape

The global phosphate rocks market is moderately consolidated, led by a small group of integrated producers with substantial reserve bases and advanced value-chain capabilities. China and Morocco dominate global supply, with China producing nearly 110 million metric tons annually and Morocco controlling over 70% of global reserves through OCP. The Mosaic Company, PhosAgro, Yara International, OCP, and ICL Group collectively hold significant market share through backward-integrated mining operations and sophisticated downstream processing assets. Competition centers on reserve quality, beneficiation technology, production efficiency, sustainability performance, and emerging opportunities in lithium iron phosphate battery materials. Key industry trends include investments in phosphogypsum recycling, development of low-carbon phosphate production incorporating carbon-capture technologies, expansion into LFP cathode materials, and geographic growth in high-demand emerging markets such as India and Brazil.

Key Developments:

- February 2025: PhosAgro announced a record agrochemical production of 11.8 million tonnes in 2024, a 4.3% increase from 2023 and a new company production record, driven by capacity expansions at the Cherepovets, Volkhov, and Balakovo facilities, with continued investment momentum and expansion plans extending through 2026.

- March 2025: The Mosaic Company restored phosphate production guidance to 7.4-7.6 million tonnes for 2025 following completion of maintenance activities at its Florida and Louisiana facilities, addressing operational disruptions from 2024 weather events and sulfuric acid turnaround maintenance.

- January 2024: Ma'aden Phosphate (Saudi Arabia) initiated joint development of an innovative phosphogypsum recycling plant with thyssenkrupp Uhde and Metso Outotec, incorporating advanced calcination technology to convert phosphogypsum waste into valuable quicklime and sulfuric acid while capturing carbon dioxide.

Top Companies in the Phosphate Rocks Market

The Mosaic Company (Tampa, U.S.) represents the largest integrated phosphate producer and processor in North America, operating nine phosphate mines and advanced processing facilities across Florida, North Carolina, Idaho, and Utah. The company commands vertically integrated operations from mine extraction through finished fertilizer production, ensuring supply chain control and customer service capabilities for agricultural and industrial markets across North America.

PhosAgro (Moscow, Russia) operates as one of the world's largest integrated phosphate-based fertilizer producers and phosphate rock processors, achieving record 11.8 million metric tons of agrochemical product output in 2024 through operations at multiple production complexes including Kirovsk, Cherepovets, Volkhov, and Balakovo. The company maintains extensive phosphate reserve bases from apatite-nepheline ores and is advancing aggressive capacity expansion programs supported by record capital investments exceeding RUB 75 billion annually, positioning itself as a global supply source of fertilizer products to emerging market regions.

Yara International ASA (Oslo, Norway) operates as a leading global crop nutrients and specialty fertilizer producer with substantial phosphate rock processing capacity and integrated operations across Europe, North America, and Africa. The company maintains significant competitive capabilities in phosphate fertilizer manufacturing, specialty nutrient formulations, and sustainable agricultural solutions, servicing diverse customer segments across developed and emerging markets with comprehensive phosphate-based product portfolios.

Companies Covered in Phosphate Rocks Market

- The Mosaic Company

- PhosAgro

- Yara International ASA

- BASF SE

- CF Industries Holdings, Inc.

- Guizhou Kailin Holdings Co., Ltd.

- Hubei Xingfa Chemicals Group Co., Ltd.

- Wengfu Group Co., Ltd.

- Misr Phosphate Company

- ICL Group

- Phosphates Marocaines (OCP)

- Jordan Phosphate Mines Company

- Saudi Ma'aden Phosphate

Frequently Asked Questions

The global phosphate rocks market is projected to reach US$ 47.4 billion by 2033, growing at a 6.4% CAGR from 2026 to 2033, driven by sustained agricultural intensification, emerging lithium iron phosphate battery demand, and livestock production expansion across emerging economies, including India, Brazil, and China.

The primary demand drivers include escalating global food production requirements driven by population growth and agricultural intensification, expanding livestock farming operations, particularly in Asia-Pacific and Latin America, requiring animal feed phosphate supplements, and the adoption of precision agriculture practices emphasizing optimized nutrient management for enhanced crop productivity and resource efficiency.

Phosphate fertilizers represent the overwhelmingly dominant end-use segment, consuming approximately 85% of globally mined phosphate rock supplies, essential for supporting agricultural productivity across cereal, oilseed, vegetable, and specialty crop production systems critical to sustaining global food security and feeding the world's expanding population exceeding 8 billion people.

The Asia-Pacific region commands market leadership with over 47.6% market share, dominated by China's overwhelming production capacity of 110 million metric tons annually and expanding domestic consumption, combined with rapidly growing phosphate demand from India and ASEAN nations pursuing agricultural modernization and food security objectives aligned with population growth requirements.

Phosphogypsum recycling and circular economy innovation represents the most significant emerging growth opportunity, enabling market participants to convert 200-250 million metric tons of annually generated phosphogypsum waste into recovered sulfuric acid, quicklime, and recovered phosphate compounds, while simultaneously addressing environmental regulatory mandates, reducing dependence on finite phosphate rock reserves, and creating incremental revenue streams through waste valorization and closed-loop production systems.

The key market players include The Mosaic Company, PhosAgro, Yara International ASA, BASF SE, CF Industries Holdings, Guizhou Kailin Holdings, Hubei Xingfa Chemicals, Wengfu Group, and Phosphates Marocaines (OCP), alongside emerging producers including Ma'aden Phosphate and ICL Group, positioning for lithium iron phosphate battery material supply.