- Animal Feed & Additives

- Pet Snacks and Treats Market

Pet Snacks and Treats Market Size, Share, Growth, and Regional Forecast, 2026 - 2033

Pet Snacks and Treats Market by Product Type (Eatables, Chewables), Form (Organic, Conventional), Pet Type (Dogs, Cats, Others), Distribution Channel (Supermarkets and Hypermarkets, Specialty Pet Stores, Online, Others), and Regional Analysis from 2026 - 2033

Pet Snacks and Treats Market Share and Trends Analysis

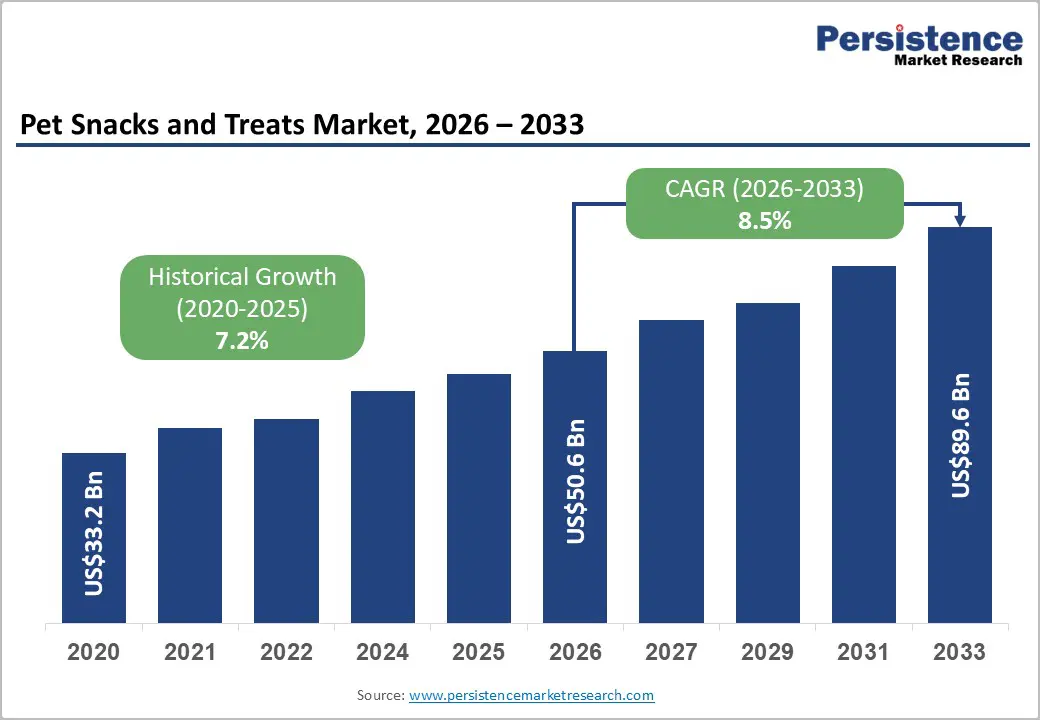

The global pet snacks and treats market size is estimated to grow from US$ 50.6 billion in 2026 to US$ 89.6 billion by 2033 growing at a CAGR of 8.5% during the forecast period from 2026 to 2033.

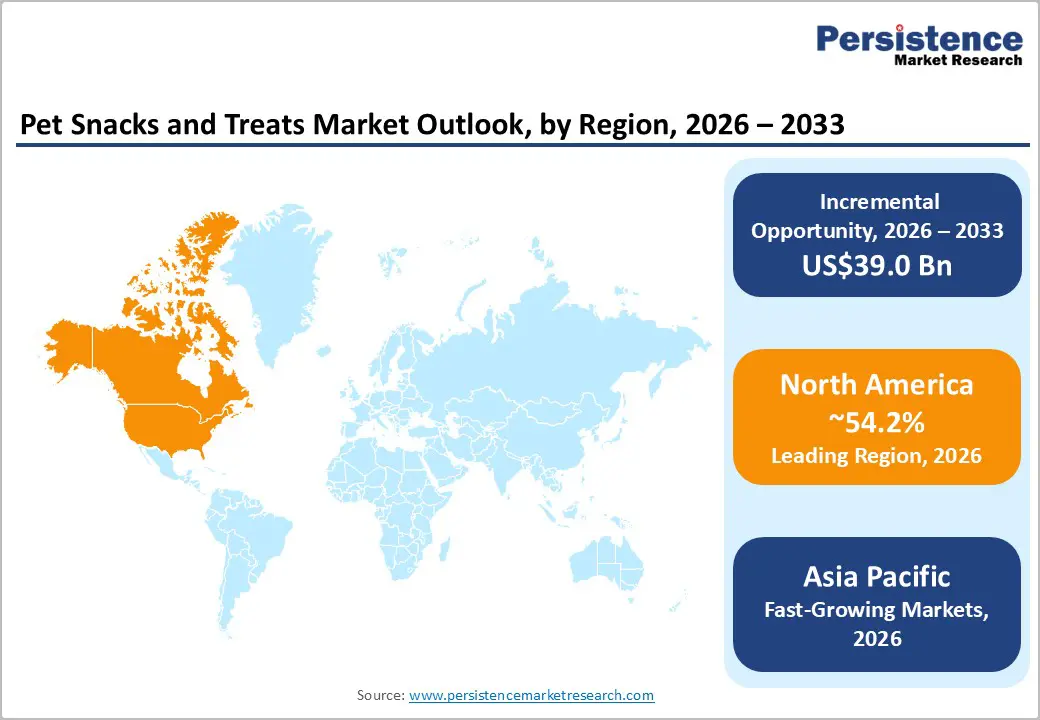

The market is expanding steadily, driven by rising pet humanization, health awareness, and demand for functional and natural treats. North America leads due to high pet ownership and robust distribution networks, whereas the Asia-Pacific region is the fastest-growing, supported by urbanization, e-commerce expansion, premiumization, and increasing adoption of innovative pet nutrition products.

Key Industry Highlights:

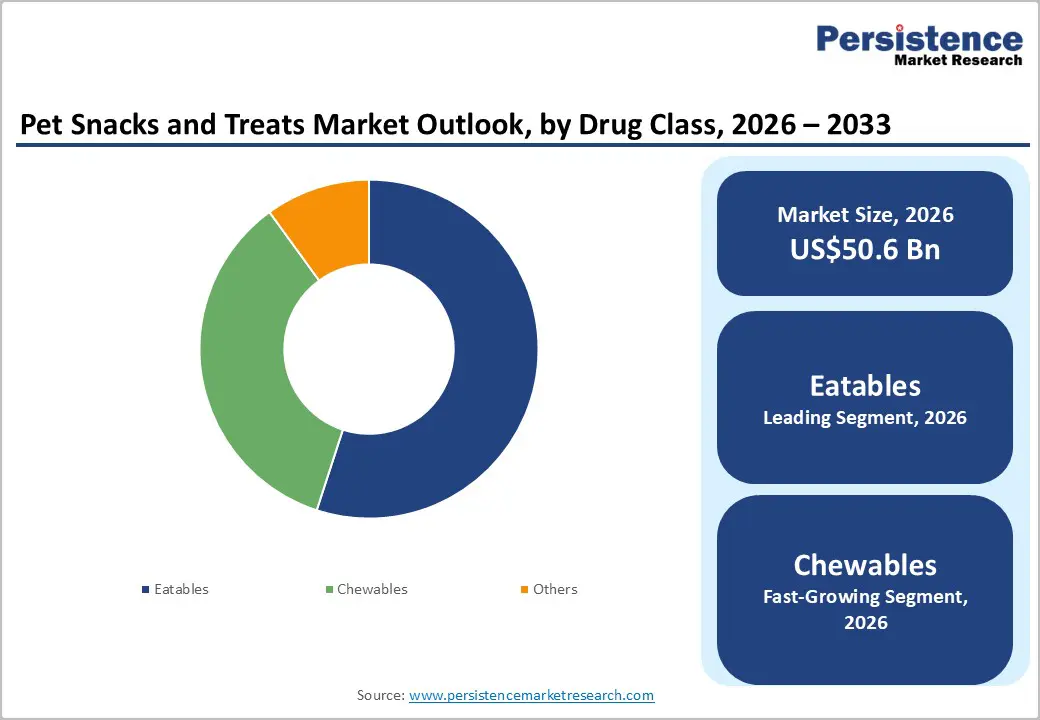

- Dominant Segment: Eatables account for 66.8% share of the Pet Snacks and Treats Market, driven by frequent consumption, palatability, and wide product availability. Chewables, particularly dental and functional chews, are the fastest-growing segment due to rising focus on oral health and behavioral benefits.

- Dominant Region: North America holds the largest market share, supported by high pet ownership, premiumization, and strong retail and e-commerce penetration. Europe follows, while Asia-Pacific is the fastest-growing region due to urbanization, rising disposable income, and increasing pet humanization.

- Market Drivers: Growth is driven by rising pet humanization, increasing awareness of pet health and nutrition, demand for functional and natural treats, and preference for convenient, value-added snack formats.

- Market Opportunity: Key opportunities include organic and clean-label treats, functional snacks (dental, joint, digestive health), plant-based formulations, premium and customized products, and rapid expansion of online and direct-to-consumer channels in emerging markets.

| Key Insights | Details |

|---|---|

|

Pet Snacks and Treats Market Size (2026E) |

US$ 50.6 Bn |

|

Market Value Forecast (2033F) |

US$ 89.6 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.5% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.2% |

Market Dynamics

Driver - Rising pet humanization and willingness to spend on premium pet nutrition

The increasing humanization of pets has become a key driver of the pet snacks and treats market, as owners increasingly view pets as family members and prioritize their health and nutrition. In the United States, 97% of pet owners consider their animals part of the family, a mindset that is associated with higher spending on quality nutrition, including treats and supplements. Pet ownership is substantial, with approximately 66% of U.S. households owning pets as of 2024, indicating continued market expansion.

This humanization trend is reflected in spending behavior: U.S. pet owners spent 4.1% more on pet products in 2024, with pet treats purchased by 78% of online buyers, highlighting robust adoption of premium nutrition products. Moreover, nearly half of pet owners purchase premium pet food, and subscription models for nutrition products are rapidly gaining traction, indicating consumer willingness to invest in ongoing quality feeding options. Pet owners’ preference for high-quality, nutritious snacks parallels broader wellness trends in human food consumption, driving product innovation and premium pricing in the pet treats segment.

Restraints - High cost of premium, organic, and functional pet treats

A key restraint in the pet snacks and treats market is the high cost of premium, organic, and functional products, which can discourage regular purchases by many pet owners. USDA data indicate that organic ingredient costs for food products are consistently higher than those of conventional counterparts due to certification, compliance, and supply constraints. For example, organic grains and meats—common in premium pet treats—routinely command 20%–40% higher retail prices than non-organic products. This pricing gap influences consumer choice, as households with budget constraints often opt for lower-priced conventional snacks, reducing overall penetration of high-end treat formulations.

Household expenditure patterns reflect sensitivity to higher-cost items: U.S. Bureau of Labor Statistics data indicate that when food prices rise, consumers shift toward lower-cost goods, prioritizing essentials over premium alternatives. In the pet category, premium treats containing specialty ingredients such as probiotics or organic components can command a significant premium over standard treats, leading some pet owners to purchase conventional options or reduce treat frequency. This cost barrier is particularly impactful in markets outside major urban centers or among middle-income households, where discretionary spending on pets competes with other financial priorities.

Opportunity - Rapid adoption of functional and therapeutic snacks (dental, immunity, calming)

The pet snacks and treats market presents a growing opportunity for functional and therapeutic snacks—such as dental chews, immunity-support treats, and calming formulations — as pet health awareness increases. According to the American Veterinary Medical Association (AVMA), more than 67% of U.S. households owned a pet in 2024, and dental disease is among the most common chronic conditions in dogs and cats, affecting more than 80% of pets by age 3. This high prevalence drives demand for dental-focused treats that help reduce plaque and tartar, presenting manufacturers with an avenue to develop value-added products that align with veterinary health concerns.

Public health data further supports the demand for functional pet snacks. The Centers for Disease Control and Prevention (CDC) recognizes oral and chronic diseases as significant pet health issues and recommends daily oral care and nutrition that support overall wellness. Additionally, the USDA reports increasing consumer preference for animal products with health attributes, which extends to pet feeding choices. Given the prevalence of stress-related behaviors in pets due to urban lifestyles and changes in household routines, calming and immunity-support treats offer tangible benefits. These real health needs observed in pet populations create a clear opportunity for innovation in functional snacks that deliver measurable wellness outcomes.

Category-wise Analysis

By Product Type, Eatables Dominates the Pet Snacks and Treats Market

Eatables account for 66.8% of the global market in 2025 because they align with everyday feeding habits, offer versatility in formulation, and meet broad pet owner preferences for palatability and convenience. U.S. pet ownership data from the American Veterinary Medical Association (AVMA) indicate that more than 67% of households owned a pet in 2024, creating a substantial base for frequent treat consumption. Government food expenditure trends from the U.S. Bureau of Labor Statistics indicate that households consistently allocate a significant share of discretionary spending to pet food and treats, with basic snacks fitting more easily into regular budgets than specialized chews. Additionally, the USDA highlights rising interest in quality ingredients that eatables can incorporate in diverse forms (soft, baked, freeze-dried), broadening their appeal and reinforcing their market dominance.

By Form, Conventional is gaining traction due to affordability, availability, familiar ingredients, and stable pricing for most pet owners

Conventional products dominate the pet snacks and treats market because they are more affordable, widely available, and familiar to most pet owners, consistent with spending patterns documented by government sources. Data from the U.S. Bureau of Labor Statistics shows that average household expenditures on pet food and treats increased steadily, but price remains a key factor influencing purchase decisions; when food costs rise, consumers shift toward lower-cost alternatives.

The American Veterinary Medical Association (AVMA) reports that over two-thirds of U.S. households owned a pet in 2024, a population that includes many middle and lower-income families for whom conventional treats represent the most accessible option. Additionally, USDA agricultural pricing data indicate that conventional ingredient costs remain lower and more stable than certified organic equivalents, reinforcing conventional formulations as the default choice for mass consumption.

Regional Insights

North America Pet Snacks and Treats Market Trends

North America dominates the pet snacks and treats market with 54.2% share in 2025, because it has exceptionally high pet ownership and strong consumer spending on pet nutrition, creating a large and engaged customer base. In the United States alone, about 94 million households own at least one pet, reflecting widespread cultural embrace of pets as family members and driving consistent demand for treats as part of pet care and feeding routines. U.S. pet industry expenditures reached approximately USD 152 billion in 2024, with pet food and treats accounting for a substantial share, indicating that owners prioritize nutrition and supplementary snacks for their animals. This robust demand is echoed in Canada, where pet food retail sales exceeded Can$6.7 billion in 2024, supported by significant dog and cat populations and growing consumer preferences for quality ingredients. These ownership and spending patterns in North America create a favourable environment for premium and diverse pet snack products, reinforcing the region’s leadership in the global market.

Europe Pet Snacks and Treats Market Trends

Europe is an important region in thepet snacks and treats market because it has a large and growing pet population and substantial consumer spending on pet nutrition. Recent data from the European Pet Food Industry Federation (FEDIAF) shows that approximately 139 million European households own at least one pet, representing nearly half of all homes across the continent, with dogs and cats prevalent in about 25–26 % of households. This widespread ownership drives consistent demand for pet food and treats, contributing to a €29.3 billion pet food market that includes significant treat segments.

European consumers place increasing emphasis on quality, innovation, and tailored nutrition, reinforcing the region’s role as a major contributor to global consumption of pet food and snacks.

Asia-Pacific Pet Snacks and Treats Market Trends

Asia-Pacific is the fastest-growing region in the pet snacks and treats market because pet ownership and spending are rising rapidly amid socioeconomic shifts. Urbanisation, rising disposable incomes, and changing lifestyles have led to significant growth in pet populations, with approximately 32% of households in the region owning a dog and 26% owning a cat, reflecting expanding demand for pet nutrition and treats. Urban centres in China, India, Japan, and Southeast Asia are experiencing a rise in pet companionship, particularly among younger and middle-class consumers who treat pets as family.

E-commerce channels are also proliferating, with online pet food sales accounting for a large share of total transactions and facilitating access to premium snacks. These demographic and consumer behaviour changes are driving accelerated growth in functional and specialty pet treats across the Asia-Pacific region.

Competitive Landscape

Leading pet snacks and treats businesses prioritize innovation, safety, and consumer-friendly products, with a focus on flavor, texture, and functional benefits. R&D ensures palatability, nutrient stability, and convenience, while collaborations with veterinary and nutrition experts enhance credibility. These strategies boost consumer adoption, satisfaction, and daily supplement compliance, driving growth and innovation in the global pet treats market.

Key Industry Developments:

- In October 2025, Mars highlighted its focus on American-made brands and strategic investments across the United States. The company emphasized initiatives to support local manufacturing, strengthen supply chains, and enhance production capacity for its pet food and treat portfolio.

- In September 2025, Mars announced a $2 billion investment to expand its manufacturing capabilities across the United States. The initiative aimed to modernize production facilities, enhance efficiency, and support growing demand for pet food and treats.

- In September 2025, Mars Snacking, in collaboration with the Unreasonable Group, welcomed fourteen new ventures into its Unreasonable Food™ program. The initiative aimed to support innovative food startups by providing mentorship, resources, and strategic guidance.

Companies Covered in Pet Snacks and Treats Market

- Mars, Incorporated and its Affiliates

- Nestlé

- SCHELL & KAMPETER, INC.

- The J.M. Smucker Company

- Hill's Pet Nutrition, Inc.

- Addiction Foods

- Wellness Pet Company

- Spectrum Brands, Inc.

- Unicharm Corporation

- Blue Buffalo Co., Ltd

- Others

Frequently Asked Questions

The global Pet Snacks and Treats Market is projected to be valued at US$ 50.6 Bn in 2026.

Rising pet humanization, health awareness, functional treats demand, premiumization, e-commerce growth, and innovative product offerings.

The global Pet Snacks and Treats Market is poised to witness a CAGR of 8.5% between 2026 and 2033.

Organic, clean-label, functional, plant-based, CBD/CBN, customized treats, emerging markets, online retail, flavor and packaging innovation.

Mars, Incorporated and its Affiliates, Nestlé, SCHELL & KAMPETER, INC., The J.M. Smucker Company, Hill's Pet Nutrition, Inc., Addiction Foods.