- Home Care & Utilities

- Pet Safe Cleaners Market

Pet Safe Cleaners Market Size, Share, and Growth Forecast, 2026 - 2033

Pet Safe Cleaners Market by Animal Type (Dog-specific, Cat-specific, Multi-pet), Product Form (Liquid, Sprays, Others), Solution Type (Enzymatic, Plant-based, Synthetic), Application Area (Floor Cleaners, Carpets, Bedding), and Regional Analysis 2026 - 2033

Pet Safe Cleaners Market Size and Trends Analysis

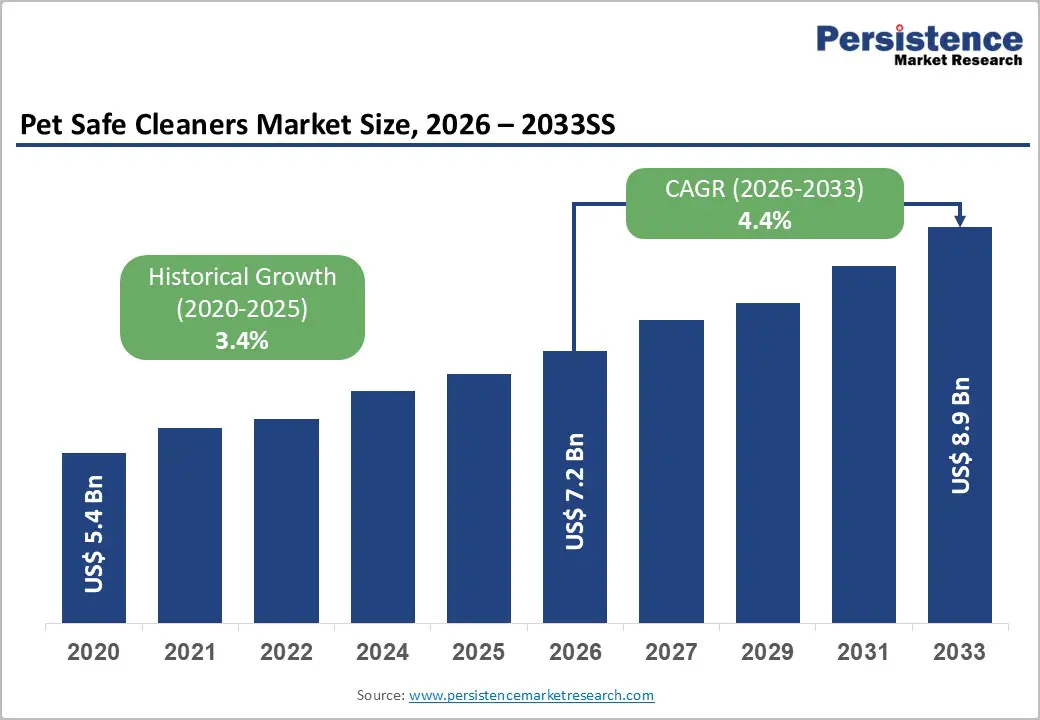

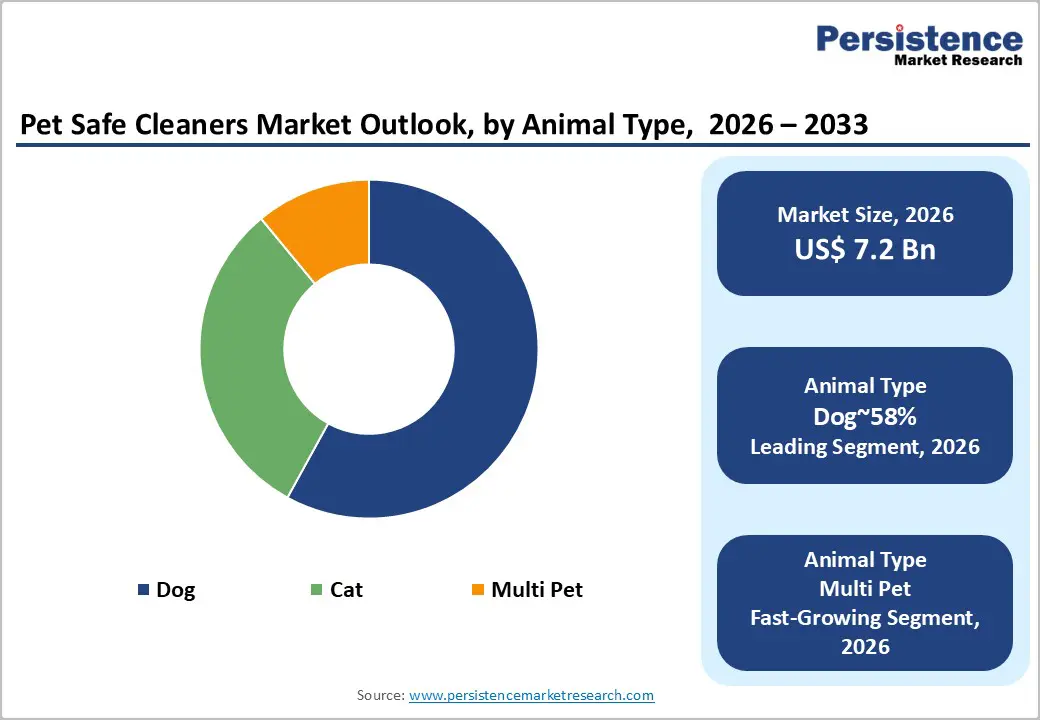

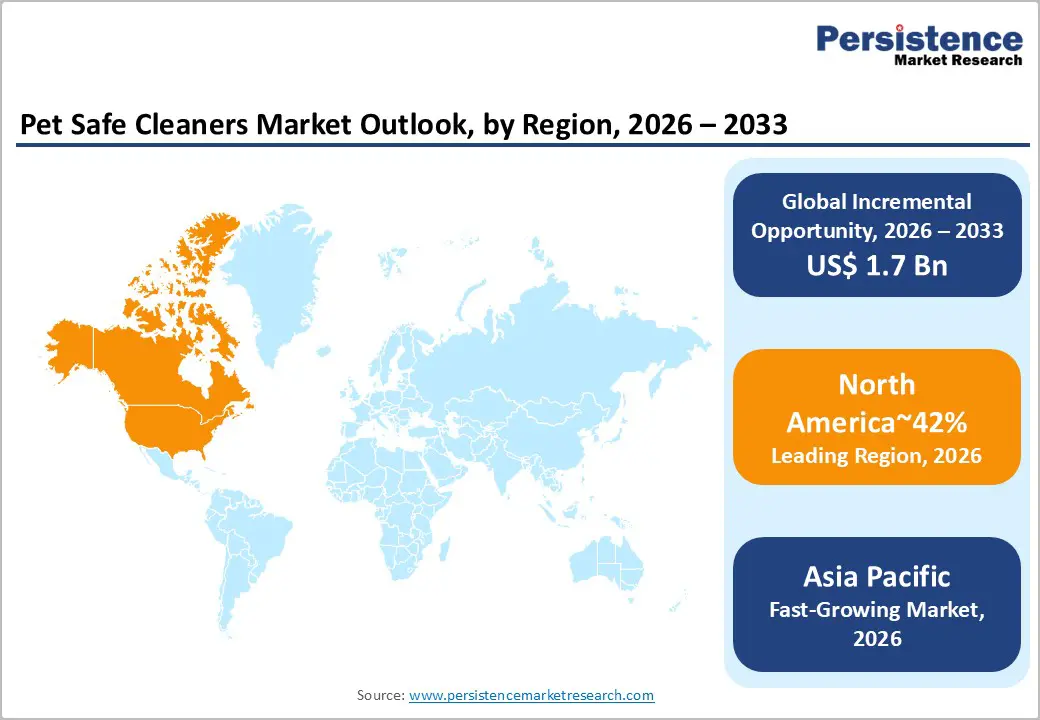

The global pet safe cleaners market size is likely to be valued at US$7.2 billion in 2026 and is expected to reach US$8.9 billion by 2033, growing at a CAGR of 4.4% during the forecast period from 2026 to 2033, driven by the increasing humanization of pets, leading to higher spending on safe products, along with a growing preference for eco-friendly solutions, which is boosting the adoption of enzymatic and plant-based cleaners.

The market is experiencing a significant shift, moving from a niche segment to a mainstream necessity within the broader home care industry. The rising consumer awareness of the carcinogenic risks associated with traditional cleaning agents (such as phenols, bleach, and ammonia) on small animals is further driving the transition to enzymatic and plant-based alternatives.

Key Industry Highlights:

- Leading Region: North America is projected to lead due to high pet ownership rates, strong consumer spending on pet hygiene products, and established retail and e-commerce channels, accounting for approximately 42% share.

- Fastest-growing Region: Asia Pacific is anticipated to grow the fastest, due to the rising pet adoption, increasing disposable incomes, and expanding awareness of pet hygiene.

- Leading Animal Type Segment: Dog-specific formulations are projected to dominate due to larger pet populations, higher usage frequency, and strong market familiarity, with approximately 58% share.

- Leading Solution Type Segment: Enzymatic cleaners are expected to lead through superior stain and odor removal efficacy, functional adoption, and residential preference, with approximately 48% share.

| Key Insights | Details |

|---|---|

|

Pet Safe Cleaners Market Size (2026E) |

US$7.2 Bn |

|

Market Value Forecast (2033F) |

US$8.9 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.4% |

|

Historical Market Growth (CAGR 2020 to 2025) |

3.4% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Growth Analysis - Pet Humanization and the Expansion of the Companion Animal Care Economy

The sustained expansion of the pet cleaners market is structurally anchored in the humanization of companion animals within household ecosystems. Sociological shifts increasingly position pets as integral family members, elevating expenditure resilience even amid broader inflationary pressures. As animals transition from outdoor to fully indoor living environments, exposure to household surfaces intensifies scrutiny over chemical residues and toxicological risk. This behavioral realignment reframes cleaning products from discretionary hygiene items to components of preventative animal healthcare infrastructure. Consequently, demand strengthens for liquid formulations and dog-specific cleaning solutions engineered for frequent surface contact and ingestion risk mitigation.

This humanization dynamic elevates formulation standards, ingredient transparency requirements, and compliance with emerging safety certifications. Retail assortments increasingly prioritize differentiated pet-safe claims supported by toxicology validation and regulatory alignment. Manufacturers respond through specialized product segmentation, higher-grade surfactant systems, and packaging innovations aligned with premium positioning strategies. These shifts recalibrate margin structures toward value-added formulations while embedding long-term demand stability within indoor pet-centric consumption patterns.

Rising Awareness of Chemical Toxicity in Companion Animal Environments

Veterinary oncology research increasingly associates environmental toxins with rising pet morbidity patterns. Conventional floor cleaners frequently contain phthalates and volatile organic compounds. These compounds accumulate at surface levels where animals breathe and rest. Heightened consumer vigilance is reshaping purchasing behavior across household cleaning categories. Health-oriented households increasingly scrutinize ingredient disclosures and toxicological certifications. This shift strengthens demand for plant-based and low-emission solution formats. Regulatory agencies, including the U.S. Environmental Protection Agency, reinforce safer formulation standards. Programs such as Safer Choice formalize compliance pathways for non-toxic positioning.

Compliance requirements elevate formulation and certification expenditures. Manufacturers must invest in alternative surfactants and biodegradable solvent systems. Reformulation processes alter procurement strategies and supplier qualification frameworks. Testing protocols intensify to validate reduced toxicity and emission profiles. Certification labeling reshapes retail merchandising and competitive differentiation dynamics. Retail channels increasingly privilege verified safe-claim products within premium segments. These shifts recalibrate cost structures toward higher input transparency burdens. Collectively, toxicity awareness embeds regulatory alignment into category growth fundamentals.

Barrier Analysis - Efficacy Misconceptions and Shelf Life Constraints in Natural Formulations

The transition toward pet-safe cleaners incorporating natural preservative systems introduces inherent stability constraints within formulation architectures. Compared with synthetic preservatives such as parabens, bio-derived alternatives often deliver reduced antimicrobial longevity under variable storage conditions. Shortened shelf stability compresses inventory turnover cycles and increases write-off risks across distribution networks. Retailers consequently face tighter replenishment planning and higher spoilage exposure within premium natural assortments. Concurrently, entrenched consumer heuristics equate strong chemical odors with validated disinfectant performance. This perception gap undermines confidence in low-odor or fragrance-free enzymatic cleaning systems designed for pet environments.

Efficacy skepticism constrains penetration of enzymatic solution formats targeting organic bio-residue degradation. Consumers confronting persistent contaminants such as urine or vomit frequently default to high-intensity chemical cleaners. Overcoming the association between gentler formulations and weaker sanitation outcomes requires demonstrable performance validation. Certification testing, claims substantiation, and transparent ingredient disclosure elevate compliance and marketing expenditures. These additional verification burdens reshape cost structures and slow category transition toward bio-based cleaning chemistries.

Opportunity Analysis - Expansion into Exotic and Small Animal Care

The pet cleaners market presents an underpenetrated opportunity within exotic and small companion animal categories. While product development historically prioritizes dogs and cats, birds, reptiles, and small mammals exhibit distinct physiological sensitivities requiring tailored formulations. Avian respiratory systems, for instance, demonstrate acute vulnerability to aerosolized chemicals and non-stick coating fumes, elevating safety compliance thresholds. Standardized household cleaners often lack suitability for enclosed habitats such as cages, terrariums, and aviaries. This functional mismatch creates demand for low-residue sprays and wipes engineered for confined ecological systems.

Specialized habitat cleaners enable premium pricing through formulation differentiation and risk mitigation positioning. Limited competitive intensity within this niche reduces promotional pressure and supports margin resilience. Product development necessitates advanced toxicological screening and substrate compatibility testing for diverse enclosure materials. Regulatory scrutiny surrounding airborne particulates and volatile emissions further elevates compliance sophistication. As urban exotic pet ownership expands, habitat-specific cleaning solutions embed structural growth optionality within the broader pet-safe hygiene portfolio.

Subscription Models and Eco Refill System Integration

Technological convergence within digital commerce ecosystems enables scalable direct-to-consumer subscription architectures. Pet-safe cleaning products, particularly liquid formats, incur elevated logistics costs due to weight and volumetric inefficiencies. Concentrated tablets and refill pods materially reduce transportation burdens by shifting dilution to end users. This structural redesign lowers freight intensity, warehouse space requirements, and packaging material consumption across the value chain. Reducing shipping weight simultaneously decreases carbon exposure within increasingly scrutinized environmental reporting frameworks.

Refill-based sprays and concentrates align with sustainability-oriented purchasing behavior among pet-focused households. Subscription mechanisms stabilize demand visibility, smooth revenue cycles, and enhance customer lifetime value metrics. Recurring fulfillment models reduce retail intermediation margins while increasing direct brand control over pricing structures. Packaging redesign toward reusable dispensers embeds circular economy principles within product portfolios. Collectively, these dynamics recalibrate unit economics by compressing logistics expenditure while reinforcing environmentally aligned brand positioning.

Category-wise Analysis

Animal Type Insights

Dog-specific formulations are projected to lead, accounting for approximately 58% share in 2026, anchored in higher cleaning intensity associated with canine ownership. Larger body mass, outdoor exposure, and recurrent odor management needs structurally elevate product consumption per household. Enzymatic cleaners engineered to degrade protein-based residues and persistent organic stains reinforce category specialization. Brands such as Rocco & Roxie Supply Co., Nature's Miracle, and Simple Solution sustain dominance through targeted odor-neutralization platforms and veterinarian-informed formulations. High household penetration among dog owners strengthens replenishment frequency and retail shelf prioritization. This entrenched usage intensity supports predictable demand cycles and scale-driven manufacturing efficiencies across liquid enzymatic portfolios.

Multi-pet formulations are projected to be the fastest-growing segment, reflecting rising urban co-ownership of cats and dogs within shared living spaces. Consumers increasingly prefer unified solutions that reduce stock-keeping complexity and storage constraints. Universal formulations compatible with cross-species sensitivities enhance purchasing convenience and cost rationalization. Companies including BISSELL, Skout's Honor, and Angry Orange expand multi-surface, multi-species product lines to capture consolidated demand. Concentrated sprays and broad-spectrum enzymatic blends improve operational efficiency for households managing varied pet types. Portfolio versatility strengthens channel expansion across ecommerce and specialty retail ecosystems.

Solution Type Insights

Enzymatic solutions are projected to lead, accounting for approximately 48% share in 2026, reflecting their functional superiority in bio-waste degradation applications. These formulations deploy proteases, amylases, and ureases to biologically decompose uric acid crystals rather than masking odors. This biochemical mechanism effectively targets remarketing behavior, encouraging repeat usage and increasing consumer dependence. Leading brands such as Nature's Miracle, Rocco & Roxie Supply Co., and Simple Solution anchor portfolios around enzyme-based stain and odor platforms. Functional credibility, veterinarian endorsement, and demonstrated odor elimination efficacy sustain premium positioning. Established manufacturing capabilities for stabilized enzyme blends further entrench this segment within high-performance cleaning workflows.

Plant-based solutions are projected to be the fastest-growing segment, propelled by expanding demand for ingredient transparency and environmentally aligned formulations. These cleaners utilize surfactants derived from corn, coconut, and citrus inputs, aligning with vegan and clean-label preferences. Consumers increasingly scrutinize chemical disclosures, favoring recognizable components and biodegradable claims. Companies such as Skout's Honor, Burt's Bees, and Better Life extend plant-derived product lines to capture sustainability-oriented demand. Advancements in bio-based surfactant chemistry enhance foaming performance and residue safety. This convergence of performance parity and ethical positioning accelerates adoption across specialty retail and ecommerce channels.

Regional Insights

North America Pet Safe Cleaners Market Trends

North America is expected to remain the leading region, accounting for approximately 42% share in 2026, supported by high consumer spending intensity and entrenched pet humanization behaviors. The region is positioned to sustain structural dominance through mature retail penetration, advanced e-commerce infrastructure, and premium product acceptance across urban households. Demand is anticipated to remain anchored in the U.S., where regulatory benchmarking through the U.S. Environmental Protection Agency Safer Choice framework standardizes safety claims and reinforces consumer trust. Large specialty chains and digital platforms are expected to continue expanding eco-labeled assortments, strengthening visibility for certified formulations. Innovation ecosystems across enzymatic and probiotic cleaning technologies are projected to reinforce premiumization dynamics and accelerate replacement cycles.

The U.S. is expected to function as the regional anchor, shaping product standards, labeling norms, and retail merchandising strategies. Concentrated brand presence, including The Clorox Company and its pet-focused portfolios, is anticipated to sustain competitive intensity while driving formulation upgrades. Regulatory alignment with non-toxic benchmarks is projected to elevate compliance thresholds and reinforce differentiation around veterinarian-endorsed positioning. Investment flows are expected to prioritize probiotic-based cleaners and advanced odor-neutralization chemistries, embedding technology-led value capture within established distribution ecosystems.

Europe Pet Safe Cleaners Market Trends

Europe is expected to remain a structurally significant region, shaped by harmonized chemical governance and sustainability-led consumption standards. The region is positioned to advance through stringent compliance frameworks under European Chemicals Agency REACH regulations, which restrict harsh surfactants and elevate safety documentation requirements. This regulatory architecture is anticipated to structurally favor plant-based, biodegradable, and low-toxicity formulations across retail channels. Demand is projected to remain anchored in environmentally conscious households, where product legitimacy is linked to both ingredient safety and lifecycle transparency. Sustainable packaging integration, including recycled and plastic-free formats, is expected to remain central to procurement decisions and retailer shelf allocation strategies.

Germany is expected to function as the regional anchor, shaping sustainability benchmarks and eco-certification alignment across the bloc. National emphasis on circular economy compliance is projected to reinforce the adoption of concentrates and refill-compatible systems. Vendors such as Seventh Generation are anticipated to expand plant-based portfolios tailored to European labeling expectations. Investment flows are expected to prioritize biodegradable surfactant chemistry and recyclable material engineering, embedding sustainability within competitive differentiation.

Asia Pacific Pet Safe Cleaners Market Trends

Asia Pacific is expected to be the fastest-growing region, supported by rapid urbanization and expanding middle-class consumption. Dense metropolitan living environments are projected to intensify demand for daily odor management and surface hygiene solutions within compact residential spaces. China and India are anticipated to accelerate category expansion as first-time pet ownership rises among digitally engaged households. Japan is positioned to reinforce regional value through advanced odor-neutralization technologies and premium product engineering. Expanding e-commerce ecosystems and social media influence are expected to amplify awareness around pet health, ingredient transparency, and routine cleaning frequency across urban clusters.

China is expected to function as the regional anchor, shaping manufacturing scale, cost efficiency, and local brand emergence. Integrated supply chains for plant-based surfactants derived from coconut and related inputs are projected to compress production costs and enhance price competitiveness. Domestic vendors are anticipated to scale affordable liquid and enzymatic formats tailored to multi-pet urban households. Investment flows into automated production and formulation optimization are expected to strengthen regional self-sufficiency while accelerating product diversification.

Competitive Landscape

The global pet safe cleaners market is moderately fragmented, with leadership gradually concentrating among diversified consumer goods suppliers and established pet care platforms. Dominant players such as Spectrum Brands, Bissell, and The Clorox Company anchor distribution through mass retail, specialty pet chains, and direct-to-consumer channels. Portfolio breadth across adjacent homecare categories strengthens procurement leverage and retailer negotiations, reinforcing scale advantages. Despite this concentration, relatively accessible entry barriers for plant-based and “natural” positioning sustain a long tail of boutique brands competing on ingredient transparency and ethical claims.

Competitive positioning reflects a bifurcated structure between horizontally diversified multinationals and vertically specialized niche formulators. Brands such as Puracy, Better Life, and Skout's Honor differentiate through cruelty-free certifications, organic inputs, and concentrated refill systems. Private label expansion by platforms including Chewy and Amazon Basics is expected to intensify margin pressure and accelerate ecosystem consolidation. Industry dynamics are likely to favor players integrating formulation science, digital merchandising, and supply-chain optimization within scalable brand portfolios.

Key Industry Developments:

- In January 2026, Church & Dwight Co., Inc. reshaped its portfolio by exiting non-core businesses such as spin-brushes and reallocating resources to premium "Power Brands" in pet and home hygiene to combat high input costs.

- In May 2025, Bissell Inc. launched the Pet Hair Eraser Allergen Lift-Off vacuum, designed to capture fine pet dander and allergens, offering major wellness benefits for multi-pet households with allergies.

- In October 2024, Bissell Inc. re-entered the Indian market with a pet-focused vacuum range, including the "Little Green" and "CrossWave" series, targeting the growing Indian vacuum market with "Pet Proven" tools for hair and odor removal.

- In February 2024, Koparo Clean (India) expanded its pet range, launching pet-safe hygiene products such as floor cleaners and laundry liquids to cater to the rising Indian middle class.

Companies Covered in Pet Safe Cleaners Market

- Spectrum Brands Holdings, Inc.

- The Clorox Company

- Bissell Inc.

- Church & Dwight Co., Inc.

- The Honest Company

- Seventh Generation

- Method Products, PBC

- Manna Pro Products, LLC

- Puracy

- Skout's Honor

- Better Life

- ECOS

- Rocco & Roxie Supply Co.

- Aunt Fannie's

- Bio-Kleen

- Koparo Clean

Frequently Asked Questions

The global pet safe cleaners market is projected to be valued at US$7.2 billion in 2026 and is expected to reach US$8.9 billion by 2033, driven by the structural shift of pet humanization and rising consumer awareness regarding the toxicity of conventional cleaning agents.

As pets are increasingly treated as family members living indoors, scrutiny over chemical residues and ingestion risks intensifies. This reframes cleaning products from discretionary items to components of preventative animal healthcare, creating resilient demand for formulations with ingredient transparency and toxicological validation, even during inflationary periods.

The pet safe cleaners market is forecast to grow at a CAGR of 4.4% from 2026 to 2033, reflecting steady adoption driven by premiumization and the displacement of conventional chemical cleaners in pet-owning households.

North America is the leading regional market, accounting for approximately 42% share, supported by high pet ownership rates and strong consumer spending. Asia Pacific is the fastest-growing region, driven by rising pet adoption, increasing disposable incomes, and expanding awareness in countries, including China, Japan, and India.

The market is moderately fragmented, with leadership concentrated among diversified suppliers such as Spectrum Brands, The Clorox Company, and Church & Dwight Co., Inc. Established pet care platforms such as Bissell Inc. and niche formulators such as Rocco & Roxie Supply Co., Skout's Honor, and Puracy compete through specialized enzymatic technologies and plant-based, cruelty-certified formulations.