- Metals & Minerals

- Calcined Pet Coke (CPC) Market

Calcined Pet Coke (CPC) Market Size, Share, and Growth Forecast, 2026 - 2033

Calcined Pet Coke Market by Product Type (Needle Coke, Shot Coke, Sponge Coke, Honeycomb Coke), Application (Fuel, Aluminum, Bricks & Glasses, Paints & Coatings, Titanium Dioxide, Steel, Fertilizer, Others), and Regional Analysis for 2026 - 2033

Calcined Pet Coke Market Share and Trends Analysis

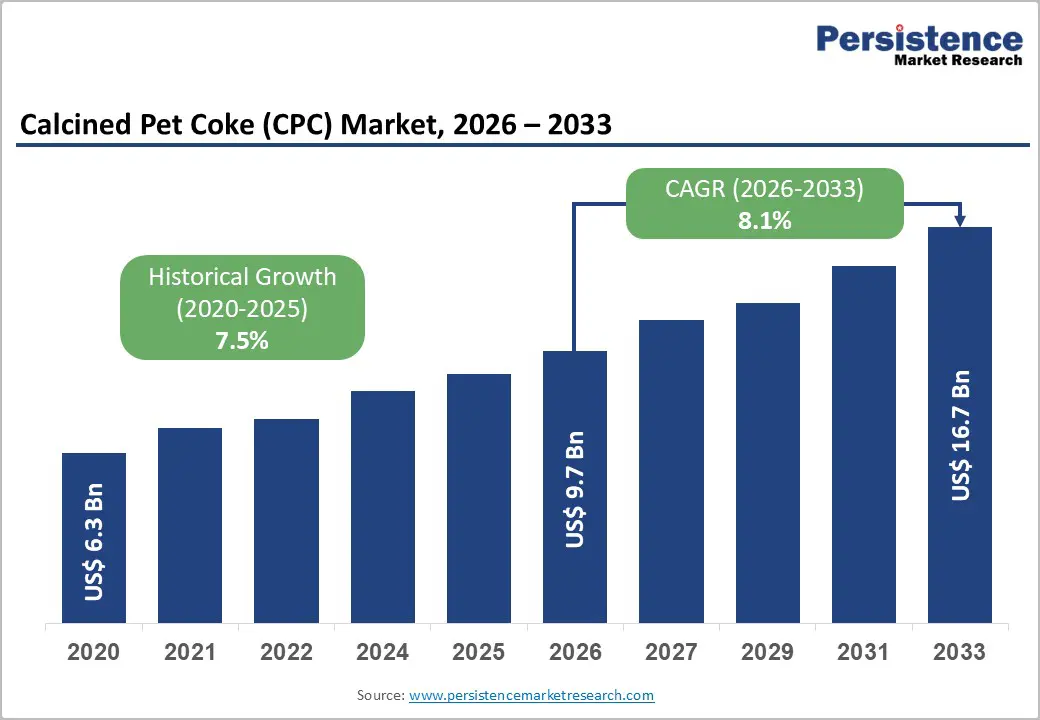

The global calcined pet coke market size is likely to be valued at US$ 9.7 billion in 2026, and is projected to reach US$ 16.7 billion by 2033, growing at a CAGR of 8.1% during the forecast period of 2026 - 2033. This growth trajectory is being driven by a steady demand for CPC from aluminum smelting operations, steelmaking facilities, and titanium dioxide (TiO2) production processes. Expanding infrastructure investment and ongoing downstream industrial recovery have been reinforcing market fundamentals and creating predictable revenue streams for suppliers.

The market expansion reflects structural economic trends that will continue to support robust demand across major consuming sectors. Quality specifications and technical requirements have been becoming increasingly stringent, with metallurgical industries prioritizing higher-purity carbon materials to optimize production efficiency and product performance. Capacity additions across developing economies have been accelerating, creating fresh demand drivers and extending the geographic reach of consumption patterns. These structural shifts have been creating sustained visibility into long-term demand, enabling producers and investors to plan with greater confidence. The combination of quality upgrades, geographic expansion, and industrial modernization will have positioned the CPC market for consistent growth, with supply-demand dynamics increasingly favoring suppliers who can meet advanced specifications and deliver consistent availability across multiple regions.

Key Industry Highlights

- Dominant Application: Aluminum is expected to account for around 65% share in 2026, due to its essential role in anode production for primary aluminum smelting.

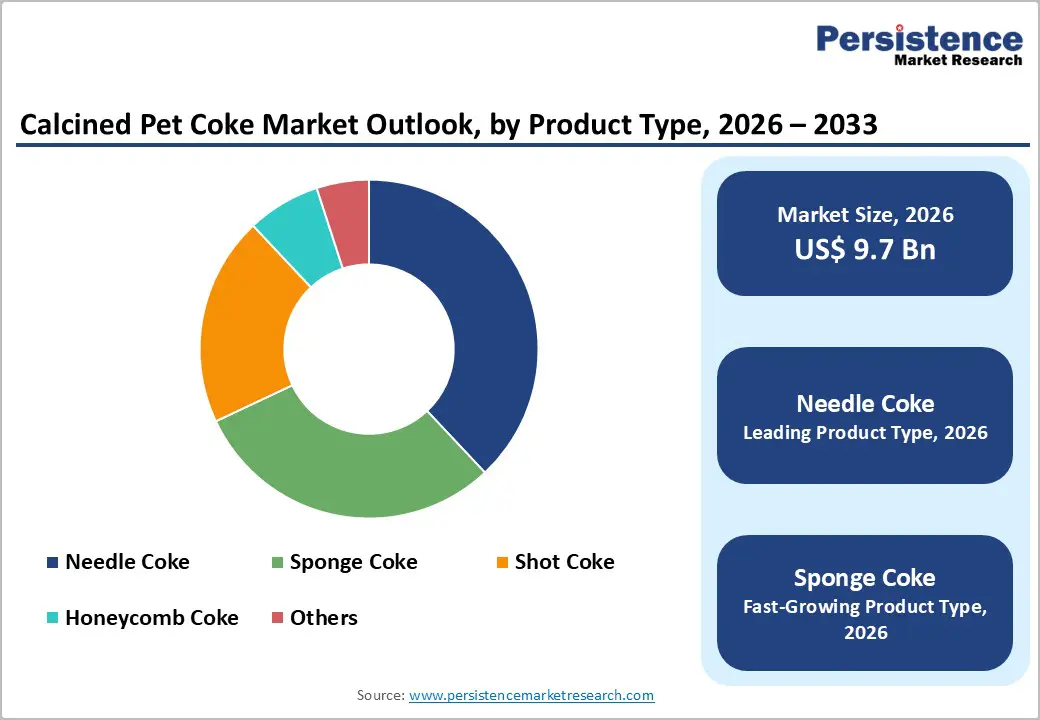

- Leading Product Type: Needle coke is anticipated to lead with an estimated 38% revenue share in 2026, while sponge coke is likely to be fastest-growing through 2033, reflecting its superior crystalline structure and low impurity profile.

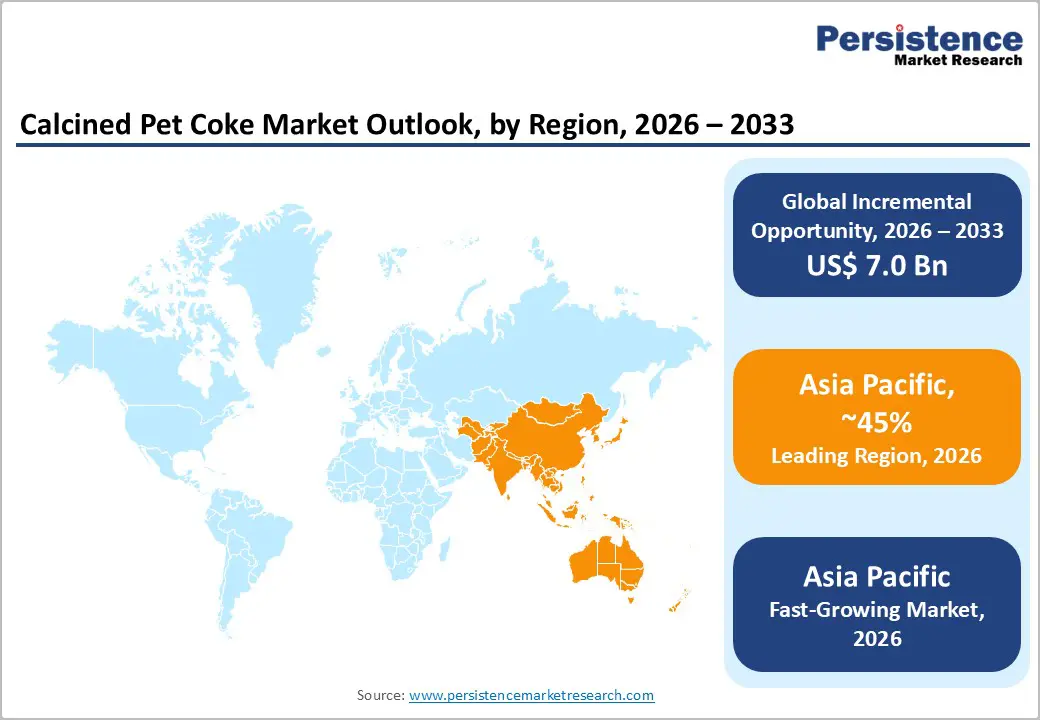

- Regional Growth Leadership: Asia Pacific is projected to represent approximately 45% of the market demand in 2026, driven by high refinery-linked calcination capacity and rapid aluminum and steel production growth.

- Competitive Environment: Competitive dynamics are shaped by environmental compliance and feedstock security, with leading producers investing in emission-control technologies and long-term green pet coke sourcing agreements.

- September 2025: ExxonMobil scaled the use of petroleum coke (petcoke) sourced from its own Canadian and Texas refineries as a proppant in Permian Basin wells, achieving 7–18% higher first-year production than sand-only fracturing.

| Key Insights | Details |

|---|---|

|

Calcined Pet Coke Market Size (2026E) |

US$ 9.7 Bn |

|

Market Value Forecast (2033F) |

US$ 16.7 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

8.1% |

|

Historical Market Growth (CAGR 2020 to 2025) |

7.5% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Industrial Output Expansion Driving CPC Demand

The demand for calcined petroleum coke in is being driven by rising industrial activity, particularly in aluminum production, steelmaking, and infrastructure development, as CPC is a critical raw material that directly impacts production efficiency. A concrete example is the May 2025 agreement between ADNOC Refining and Emirates Global Aluminium (EGA), under which ADNOC will supply up to 1.5 million tonnes of CPC over five years, valued at US$ 500 million. This contract aims to localize EGA’s supply chain, with ADNOC Refining providing at least 30% of EGA’s calcined pet coke requirements from the Ruwais Refinery, reducing reliance on imports. The supplied CPC is expected to support the production of approximately 3.75 million tonnes of aluminum over the agreement period, illustrating the direct link between calcined pet coke demand and industrial output expansion.

Steel production and broader infrastructure development further reinforce CPC consumption globally. The increased adoption of electric arc furnace (EAF) steelmaking raised calcined pet coke requirements for carbon electrodes, while refiners worldwide optimized calcination and desulfurization processes to produce low-sulfur grades for industrial end-users. Such agreements underscore the continued importance of industrial expansion as the primary driver of calcined pet coke demand, ensuring consistent volumes and supporting high-quality consumption across key sectors.

Regulatory and Feedstock Challenges Limiting Calcined Petroleum Coke Expansion

Stringent environmental regulations and evolving emission standards in have increasingly constrained CPC production and expansion. For example, new particulate matter and sulfur dioxide emission norms finalized in June 2025 by India’s Ministry of Environment, Forest and Climate Change (MOEF) require calcination facilities to meet tighter air quality standards, prompting producers to invest in upgraded pollution control systems within a stipulated compliance window. Such mandates raise capital and operational costs, especially for older plants that must retrofit technologies like flue gas desulfurization and advanced dust management systems. These compliance demands can delay capacity additions and increase unit costs, particularly in regions with rigorous air quality enforcement.

Feedstock availability and quality variability further limit market flexibility and growth. The quality of raw petroleum coke feedstock is directly tied to crude oil types and refinery coking processes, making CPC supply sensitive to upstream refiners’ feedstock choices and crude market shifts. The volatility in crude slates with some refiners reducing heavy crude processing due to cost and environmental pressures tightened availability of suitable low-sulfur green petroleum coke, complicating downstream calcination schedules and pricing. This unpredictability impacts contract stability, production planning, and long-term supply reliability, highlighting how regulatory and feedstock challenges continue to act as structural restraints on market growth.

Premium Product Development and Strategic Capacity Expansion

The calcined petroleum coke market is witnessing the birth novel opportunities in premium product development and capacity expansion that align with evolving industrial demand profiles. Marathon Petroleum launched a new low-sulfur calcined petroleum coke grade in 2025, designed to reduce emissions in aluminum smelting and improve anode performance, illustrating the growing importance of advanced CPC products in cleaner and higher-efficiency industrial processes. Such product innovations cater to stricter environmental and performance requirements in aluminum and metallurgical applications, creating higher-value market segments and supporting differentiated pricing relative to legacy calcined petroleum coke grades. These developments signify a clear shift toward diversified, quality-driven market demand.

Strategic expansion of calcination capacity also presents considerable opportunity for long-term growth. Between 2023 and 2025, global calcined capacity expanded significantly, adding approximately 1.6–1.9 million tons and lifting utilization rates, including the commissioning of multiple large rotary-kiln and fluidized-bed units. This incremental capacity reflects industry confidence in future CPC demand across key sectors such as aluminum, steel, and specialty carbon applications. Expanding capacity improves geographic supply distribution and enhances supply-chain responsiveness for downstream industries, underscoring why strategic scaling of CPC production is a significant growth opportunity in the global market.

Category-wise Analysis

Product Type Insights

Needle coke is anticipated to lead in 2026, accounting for an estimated 38% of the CPC market revenue share, owing to its low thermal expansion and high crystallinity required for premium aluminum anodes. The aluminum producers globally prioritized anode efficiency and operational stability amid higher energy and compliance costs, reinforcing demand for higher-quality CPC grades. Procurement strategies increasingly favored long-term, quality-assured supply to reduce performance variability and exposure to spot market volatility. These structural demand drivers continue to anchor needle coke’s dominant position in the calcined pet coke market.

Sponge coke is slated to be the fastest-growing product type, projected to expand at a CAGR of 16% through 2033, driven by its suitability for steelmaking, cement, and industrial fuel applications. In 2025, for example, Tata Steel UK advanced its electric arc furnace transition, increasing the demand for flexible and cost-efficient carbon inputs in scrap-based steel production. The balanced sulfur profile and broad metallurgical usability of sponge coke is supported its adoption beyond premium anode applications. Faster qualification cycles and lower cost sensitivity compared with needle coke further accelerated its uptake, reinforcing sponge coke’s position as the primary growth engine within the CPC product mix.

Application Insights

Aluminum is set to remain the dominant application segment, representing approximately 65% of the calcined pet coke market revenue share in 2026, as CPC is indispensable for anode manufacturing in electrolytic smelting. Emirates Global Aluminium has continued to rely on long-term CPC supply agreements to support stable smelter operations, highlighting the importance of feedstock security in aluminum production. Another example is Norsk Hydro, which sustained full anode production at its European smelters despite energy market volatility, prioritizing secured CPC sourcing to avoid operational disruptions. These developments reinforce aluminum’s role as the largest and most structurally stable demand center, anchoring global CPC consumption with long-term volume reliability for suppliers.

Steel is the fastest-growing application segment, projected to expand at a CAGR of 16% from 2026 to 2033, driven by rising EAF adoption and scrap-based steel production. ArcelorMittal increased EAF operations in Poland and Spain, directly raising the requirement for calcined petroleum coke as a recarburizer to maintain melt quality. Simultaneously, U.S. steelmakers responding to Infrastructure Investment projects increased EAF-based output, creating higher CPC demand for carbon input control. These operational shifts show that as EAF utilization scales globally, calcined petroleum coke consumption in steel applications is accelerating, making it the fastest-growing CPC segment.

Regional Insight

North America Calcined Pet Coke (CPC) Market Trends

North America boasts a mature CPC market, with the United States leading regional demand. The regional market has been benefiting from well-established refining infrastructure and consistent aluminum and steel consumption patterns. The U.S. Environmental Protection Agency (EPA) regulations have been driving significant investments in cleaner calcination processes and advanced dust control technologies. These regulatory pressures have been supporting operational efficiency upgrades rather than prompting large-scale capacity expansions. Market practices have been revolving around long-term supply agreements, which have been reducing price volatility and ensuring stable revenue streams for producers. Technologically advanced smelters and steel manufacturing facilities have been reinforcing predictable consumption patterns, creating a fundamentally sound market environment with high barriers to entry for new participants.

A notable example is Alcoa Corporation that has been implementing comprehensive smelter efficiency improvements across its North American operations, focusing on optimized anode performance and reliable CPC utilization. The company has been concentrating on regulatory compliance, enhanced energy efficiency, and strategic long-term sourcing arrangements to strengthen operational stability. These strategic measures have been positioning North America as a structurally stable and technologically sophisticated CPC market. Industry stakeholders will have achieved greater resilience by continuing to prioritize sustainable practices and efficiency optimization. The combination of regulatory compliance, technological advancement, and established supply chain relationships has been creating a competitive advantage that newer entrants will find challenging to replicate, ensuring the region maintains its leadership position in the global CPC landscape.

Europe Calcined Pet Coke (CPC) Market Trends

Europe operates as a regulated and value-driven market for calcined petroleum coke, with Germany, the United Kingdom, France, and Spain serving as the primary contributors. The region’s regulatory environment, shaped by harmonized European Union (EU) environmental policies, has been favoring producers with advanced compliance capabilities. Demand for CPC is concentrated in aluminum recycling, specialty steel manufacturing, and chemical processing, where feedstock quality is prioritized above volume. Price stability and technical differentiation have been supporting revenue retention for established suppliers. Infrastructure improvements and ongoing process upgrades have been driving moderate market growth, with a strong emphasis on sustainability and efficiency.

Producers across the region have been making focused investments in compliance and efficiency, enabling them to meet stringent EU standards. These initiatives have been reinforcing Europe’s strategic importance in the global CPC landscape. Regional market growth is anticipated to remain moderate, but quality-driven consumption patterns will continue to ensure long-term stability for suppliers. The combination of regulatory alignment, technological advancement, and process optimization has been positioning Europe as a resilient and strategically relevant market for high-quality CPC.

Asia Pacific Calcined Pet Coke (CPC) Market Trends

Asia Pacific has been projected to remain the largest and fastest-expanding calcined petroleum coke market, driven by China, India, and the ASEAN economies. The region is forecasted to secure about 45% of the calcined pet coke market share and is expected to register an estimated 2026-2033 CAGR of roughly 9%. Large-scale manufacturing activity has been increasing demand, while refinery integration has been improving cost control and feedstock access. Proximity to major aluminum and steel hubs has been shortening supply routes and supporting more predictable delivery performance. Government-backed industrial policies and ongoing infrastructure buildouts have been strengthening competitiveness, and new calciners plus refinery-linked investments have been adding volume in a disciplined way. For suppliers and buyers, strategic sourcing has been reducing exposure to raw material disruptions and has been supporting consistent quality for high-throughput operations.

In China, refinery-linked CPC expansion projects have been improving supply availability and have been tightening coordination between refiners and end users. In India, on the other hand, National Aluminium Company Limited (NALCO) has been upgrading its supply chain, which has been strengthening feedstock security and improving operating efficiency for aluminum and steel producers. These actions have been reinforcing regional momentum because rapid industrialization is still expanding downstream capacity and raising technical expectations for coke quality. Investors and operators are continuing to prioritize projects that secure long-term feedstock, integrate logistics, and meet tightening emissions expectations, since those capabilities have been separating leaders from price-only competitors. If current execution continues, Asia Pacific will have solidified its position as the most strategically important CPC market globally, with scale advantages that will be difficult for other regions to replicate.

Competitive Landscape

The global calcined petroleum coke market structure is moderately consolidated, with leading players being Rain Carbon Inc., Oxbow Corporation, Tata Group, Phillips 66, and PetroCoque. These organizations have been leveraging refinery-linked production capabilities, long-term supply agreements, and advanced calcination technologies to deliver high-quality CPC for aluminum, steel, and TiO2 industries. Investment in low-sulfur grades and specialty carbon products has been supporting compliance with environmental standards while meeting end-user specifications. Integrated supply chains have been providing operational reliability and reinforcing market stability, which allows these incumbents to command pricing power and maintain customer loyalty across economic cycles.

Regional and niche producers such as Indian Oil Corporation, GOA Carbon, and Sinoway Carbon have been focusing on localized supply and specialty grades, carving out defensible positions in their respective markets. High capital intensity, feedstock availability, and regulatory compliance requirements have been functioning as formidable entry barriers that protect incumbents and limit competitive pressure. Growing demand for premium CPC has been encouraging innovation and process improvements across the industry. Market consolidation will continue through capacity expansions, long-term supply arrangements, and strategic partnerships designed to strengthen geographic reach and technical capabilities. Technology collaborations have been enhancing product differentiation and competitive positioning across regions, ensuring that suppliers who combine operational scale with innovation will capture disproportionate value in the years ahead.

Key Industry Developments

- In July 2025, U.S.–Brazil trade tensions destabilized global petroleum coke markets, with Brazil threatening retaliatory tariffs on American petcoke after U.S. taxes on Brazilian exports. Price volatility spread unevenly across regions, with Europe experiencing modest increases driven by stable steel demand, while China faced oversupply and price declines and India saw demand rebound with price increases.

- In April 2025, India’s Directorate General of Foreign Trade (DGFT) allocated a total of 775,000 tons of CPC import quota for the fiscal year April 2025–March 2026. The quota was shared among Vedanta, Hindalco, Bharat Aluminium, and Nalco, providing critical feedstock for domestic aluminum smelting operations. Rain CII Carbon secured the largest share of the related RPC quota (462,589 tons) for CPC manufacture, underscoring its market prominence.

- In February 2025, Texas A&M University and the U.S. Department of Energy Advanced Research Projects Agency-Energy (ARPA-E) began developing a US$3 million, three-year project to convert petroleum coke into synthetic graphite for lithium-ion batteries using catalytic graphitization. The process dramatically reduces processing temperatures from 5,000°F and significantly cuts energy consumption and carbon emissions compared to traditional synthetic graphite production methods.

Companies Covered in Calcined Pet Coke (CPC) Market

- Rain Carbon Inc.

- Oxbow Corporation

- BP plc

- Phillips 66

- Shandong KeYu Energy Co., Ltd.

- Aluminium Bahrain B.S.C. (Alba)

- PetroCoque S.A.

- GOA Carbon

- Sinoway Carbon Co., Ltd.

- Atha Group / Petro Carbon & Chemicals Ltd.

- Indian Oil Corporation

- Petrobras

- ExxonMobil Corporation

Frequently Asked Questions

The global CPC market is projected to reach US$ 9.7 billion in 2026.

The rising demand from aluminum production, steel manufacturing, and industrial carbon applications, along with refinery-linked supply chain expansion, drives the market.

The market is poised to witness a CAGR of 16.7% between 2026 and 2033.

The growth in needle-grade CPC for specialty carbon applications, capacity expansions in emerging markets, and investments in low-sulfur and high-purity grades are key opportunities.

Rain Carbon Inc., Oxbow Corporation, Tata Group, Phillips 66, Shandong KeYu Energy, Aluminium Bahrain (Alba), PetroCoque S.A., GOA Carbon, are some of the leading market participants.