- Animal Health

- U.K. Pet Insurance Market

U.K. Pet Insurance Market Size, Share and Growth Forecast, 2026 - 2033

U.K. Pet Insurance Market by Type of Coverage (Accident-only, Time-limited, Maximum Benefit, Lifetime), Type of Pet (Dogs, Cats), Distribution Channel (Direct Sales, Brokers and Agents, Veterinary Clinics, Retailers and Pet Stores), and Regional Analysis for 2026 - 2033

U.K. Pet Insurance Market Size and Trends Analysis

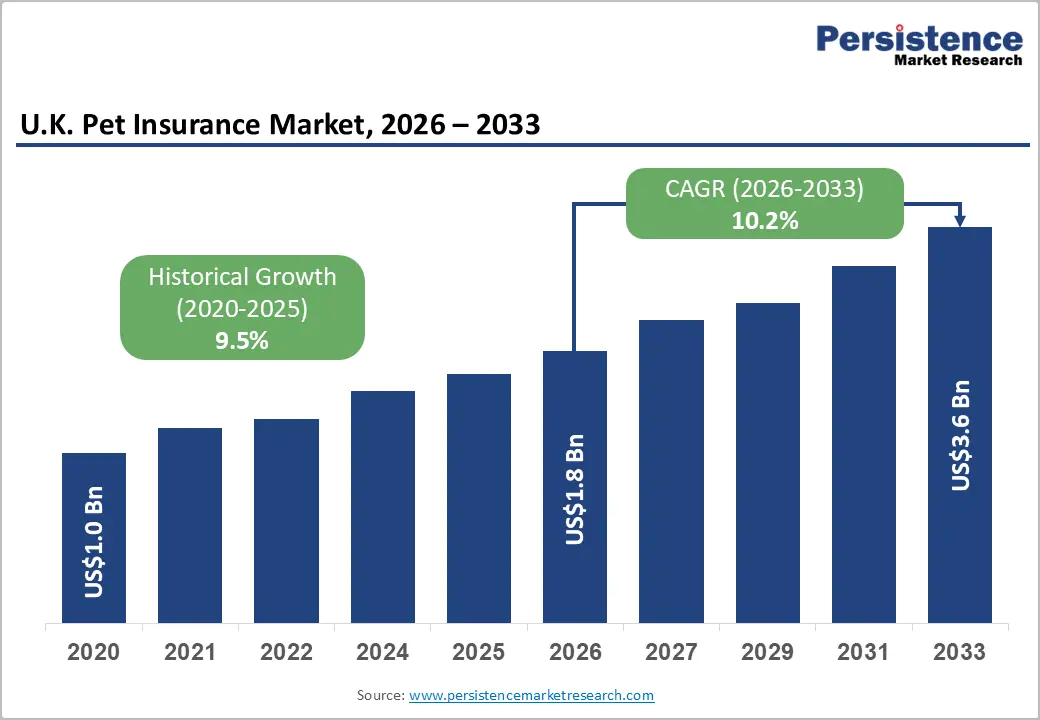

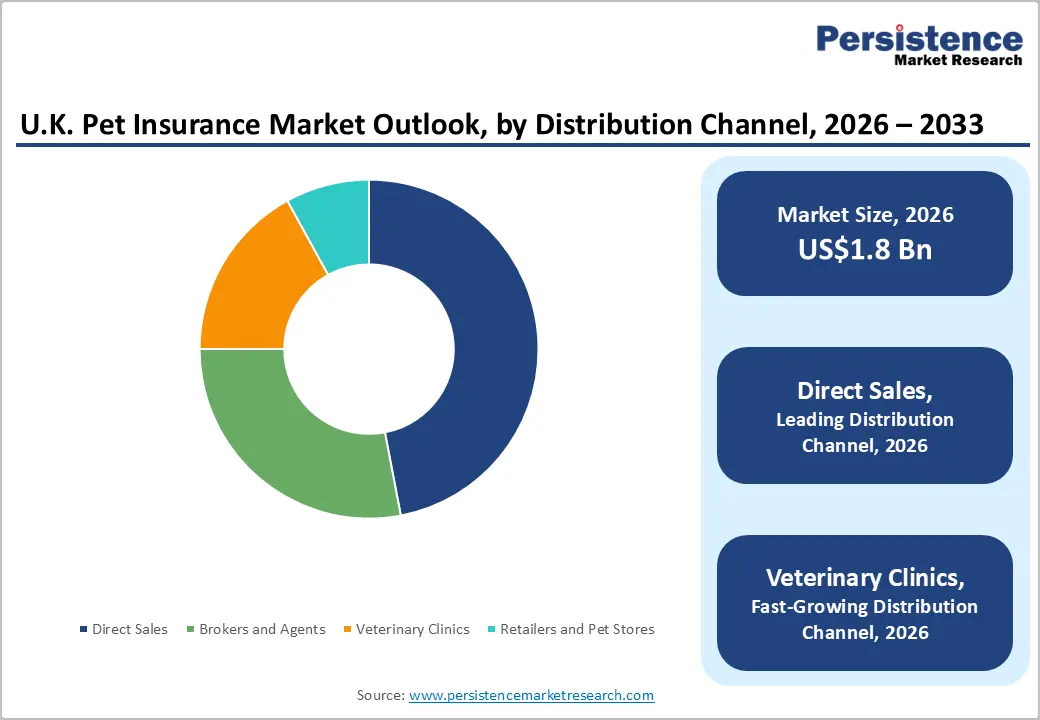

The U.K. pet insurance market size is likely to be valued at US$1.8 billion in 2026 and is projected to reach US$3.6 billion by 2033, growing at a CAGR of 10.2% during the forecast period from 2026 to 2033, driven by rising pet ownership, increasing veterinary treatment costs, and growing consumer awareness regarding financial protection for companion animals.

The U.K. remains one of the most mature pet insurance markets globally, supported by high insurance penetration among dog and cat owners. Growth is further reinforced by digital distribution channels, broader policy customization, and increasing demand for comprehensive lifetime pet insurance products. Rising expenditure on pet healthcare, preventive treatments, and advanced veterinary procedures continues to strengthen long-term market demand.

Key Industry Highlights:

- Dominant Coverage Type: Lifetime coverage is projected to account for approximately 52% of market revenue in 2026, while maximum benefit coverage is expected to be the fastest-growing coverage segment through 2033, driven by increasing demand for flexible and cost-effective protection plans.

- Leading Pet Type: Dogs are expected to account for approximately 61% of market revenue in 2026, driven by higher insurance penetration and veterinary spending per pet, while cats are projected to be the fastest-growing segment through 2033.

- Dominant Distribution Channel: Direct sales are expected to lead with around 47% of market revenue in 2026, while veterinary clinics are projected to emerge as the fastest-growing distribution channel through 2033, benefiting from stronger insurer-veterinarian partnerships and trusted point-of-care recommendations.

- Competitive Environment: Market competition is characterized by digital platform expansion, AI-enabled claims processing, veterinary partnership programs, and regulatory reforms promoting pricing transparency, all aimed at improving customer experience and accelerating long-term market growth.

DRO Analysis

Driver - Rising Pet Ownership and Escalating Veterinary Healthcare Costs Driving Insurance Adoption

The primary growth driver for the U.K. pet insurance market is the increasing financial burden associated with veterinary care, combined with a large and stable pet population. According to the PDSA Animal Wellbeing Report, the U.K. had approximately 10.6 million dogs and 10.8 million cats in 2024, while over half of U.K. adults owned at least one pet. The number of dog owners increased from 23% in 2011 to 28% in 2024, reflecting sustained demand for companion animal healthcare.

Simultaneously, veterinary treatment costs have risen significantly due to advanced diagnostics, specialty treatments, imaging technologies, and chronic disease management. The Competition and Markets Authority (CMA) reported that veterinary service prices increased by approximately 63% between 2016 and 2023. As pet owners increasingly view pets as family members, demand for financial protection through pet insurance policies continues to rise. This trend supports premium growth, encourages insurers to launch broader coverage options, and strengthens long-term market expansion.

Restraint - Premium Inflation and Affordability Concerns Limiting Market Penetration

Despite favorable market fundamentals, affordability remains a significant challenge. Rising claims severity, increasing veterinary costs, and inflationary pressures have led many insurers to adjust premium structures. Pet owners often experience substantial annual premium increases, particularly for aging pets or those with pre-existing conditions. Consumer feedback across the market highlights concerns regarding policy renewals and escalating insurance costs.

Despite favorable market fundamentals, affordability remains a key barrier to wider insurance adoption. According to a recent pet owner survey published in 2026, nearly one-third of U.K. pet owners do not have pet insurance. Among uninsured owners, 46% cited high premium costs as the main reason for not purchasing coverage, while 29% stated that their household budget does not allow for additional insurance expenses. Rising veterinary treatment costs have contributed to premium increases, particularly for older pets and comprehensive policies. As a result, cost sensitivity continues to limit policy uptake among lower-income households, younger pet owners, and multi-pet families, potentially constraining overall market penetration.

Opportunity - Digital Distribution and Personalized Pet Healthcare Solutions Expanding Market Potential

A significant opportunity for the U.K. pet insurance market lies in increasing coverage among uninsured pet owners through digital-first distribution models. According to the PDSA Animal Wellbeing Report, the U.K. has approximately 10.6 million dogs and 10.8 million cats, while a substantial share of pet owners remain uninsured. Online policy purchases, mobile claims processing, instant quotations, and tele-veterinary services are improving accessibility and helping insurers reach younger, digitally engaged consumers more efficiently.

Another growth avenue is the development of personalized coverage and preventive healthcare solutions. Around 38% of pet owners are first-time owners of their chosen species, creating strong demand for guidance, wellness services, and financial protection products. Additionally, GlobalData's 2025 survey found that approximately 40% of pet owners would consider using smart pet-health monitoring technologies, highlighting growing interest in integrated pet healthcare. Insurers that combine wellness benefits, tele-veterinary support, and veterinary partnerships can strengthen customer engagement and accelerate policy adoption through 2033.

Category-wise Analysis

Type of Coverage Insights

Lifetime coverage is expected to account for approximately 52% of market revenue in 2026, making it the dominant coverage type. Its leadership is supported by the increasing demand for protection against chronic and recurring conditions, which account for a significant share of veterinary claims. According to the U.K. Competition and Markets Authority (CMA), pet owners are increasingly facing higher treatment costs for specialist and referral services, thereby strengthening demand for policies that provide continuous annual coverage and long-term reimbursement.

Maximum benefit coverage is projected to be the fastest-growing segment, registering an estimated 10.4% CAGR through 2033. The segment benefits from growing consumer preference for cost-controlled insurance products that still provide substantial claim limits. As insurers expand flexible policy offerings and tiered pricing structures, maximum benefit plans are increasingly attracting middle-income households seeking broader protection without the premium commitments of lifetime coverage.

Type of Pet Insights

Dogs are anticipated to contribute approximately 61% of market revenue in 2026, maintaining their position as the leading insured pet category. According to claims data published by major insurers, dogs typically generate higher average claim values than cats due to a greater incidence of musculoskeletal disorders, cruciate ligament injuries, and breed-specific hereditary conditions. This results in stronger insurance penetration and higher premium expenditure across the canine segment.

Cats are expected to be the fastest-growing segment, expanding at an estimated 10.8% CAGR through 2033. Growth is being supported by increasing diagnosis rates of chronic feline conditions such as kidney disease and hyperthyroidism, particularly among aging pets. Data from veterinary associations indicate that preventive health screenings and routine wellness visits for cats have increased in recent years, encouraging greater awareness of insurance as a tool for managing long-term healthcare costs.

Distribution Channel Insights

Direct sales are projected to lead the market with approximately 47% of revenue share in 2026. The segment is benefiting from the rapid adoption of digital insurance services across the U.K., where the majority of insurance consumers now research and compare policies online before purchasing. Investments in digital onboarding, automated claims handling, and customer self-service platforms continue to strengthen the competitiveness of direct distribution models.

Veterinary clinics are forecast to be the fastest-growing distribution channel, advancing at an estimated 10.6% CAGR through 2033. Growth is supported by the increasing role of veterinary professionals in educating pet owners about healthcare financing options. Industry trends show a rising number of partnerships between insurers and veterinary practices, enabling insurance discussions to occur during consultations and improving policy conversion rates at the point of care.

Competitive Landscape

The U.K. pet insurance market is moderately consolidated, with leading providers such as Petplan, Agria Pet Insurance, ManyPets, Animal Friends, Direct Line Group, and Admiral Group accounting for a significant share of total premiums. These established insurers leverage strong brand recognition, extensive veterinary partnerships, and broad policy portfolios to maintain competitive positions. Market leaders continue investing in digital platforms, automated claims processing, and personalized coverage options to enhance customer experience and improve policy retention in an increasingly competitive environment.

Meanwhile, challenger brands and digital-first insurers are gaining traction by offering simplified online purchasing, flexible policy structures, and technology-enabled customer engagement models. While regulatory requirements, underwriting expertise, and claims management capabilities create barriers to entry, ongoing digitalization is enabling newer participants to compete effectively through innovation rather than scale. The market is expected to witness continued partnership activity between insurers, veterinary networks, and pet wellness providers, while established players increasingly focus on product differentiation, preventive healthcare benefits, and AI-driven service capabilities to strengthen long-term growth.

Key Industry Developments:

- In December 2025, the Association of British Insurers analyzed the CMA's provisional findings, highlighting implications for pet insurers as over 60% of veterinary practices are now controlled by six large corporate groups.

- In October 2025, the U.K. Competition and Markets Authority (CMA) proposed 21 measures to improve transparency in the £6.3 billion veterinary services market, including mandatory price disclosures, prescription fee caps, and a national price-comparison platform. These reforms are expected to influence pet insurance pricing and claims management.

Companies Covered in U.K. Pet Insurance Market

- Petplan

- Agria Pet Insurance

- ManyPets

- Animal Friends Insurance

- Direct Line Group

- Admiral Group

- RSA Insurance

- Tesco Bank Pet Insurance

- Sainsbury's Bank Pet Insurance

- AXA Pet Insurance

- Allianz Pet Insurance

- Napo

- Petgevity

Frequently Asked Questions

The U.K. pet insurance market is projected to reach US$1.8 billion in 2026.

Rising pet ownership, increasing veterinary treatment costs, and growing demand for financial protection drive market growth.

The market is expected to grow at a CAGR of 10.2% from 2026 to 2033.

Insurers can capitalize on digital distribution, tele-veterinary services, and personalized pet healthcare solutions.

Petplan, Agria Pet Insurance, ManyPets, Animal Friends, Direct Line Group, and Admiral Group are among the leading market participants.