- Plastics, Polymers & Resins

- Polyethylene Terephthalate Market

Polyethylene Terephthalate Market Size, Share, and Growth Forecast 2025 - 2032

Polyethylene Terephthalate Market by Grade (Food Grade, Non-Food Grade), by Application (Beverage Packaging, Food Packaging, Non-Food Packaging, Textiles & Fibers, Automotive Components, Electrical Components, Industrial Equipment), by Production Method (Direct Esterification Method, Transesterification Method, Ethylene Oxide Addition Method), by Regional Analysis, 2025-2032

Polyethylene Terephthalate Market Size and Trend Analysis

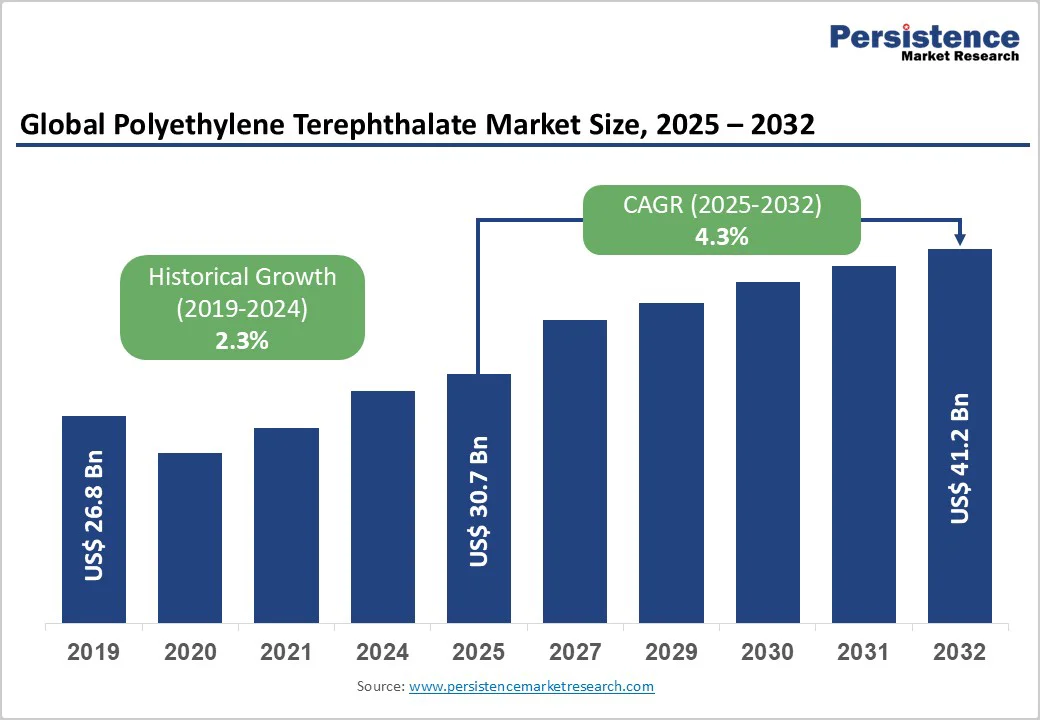

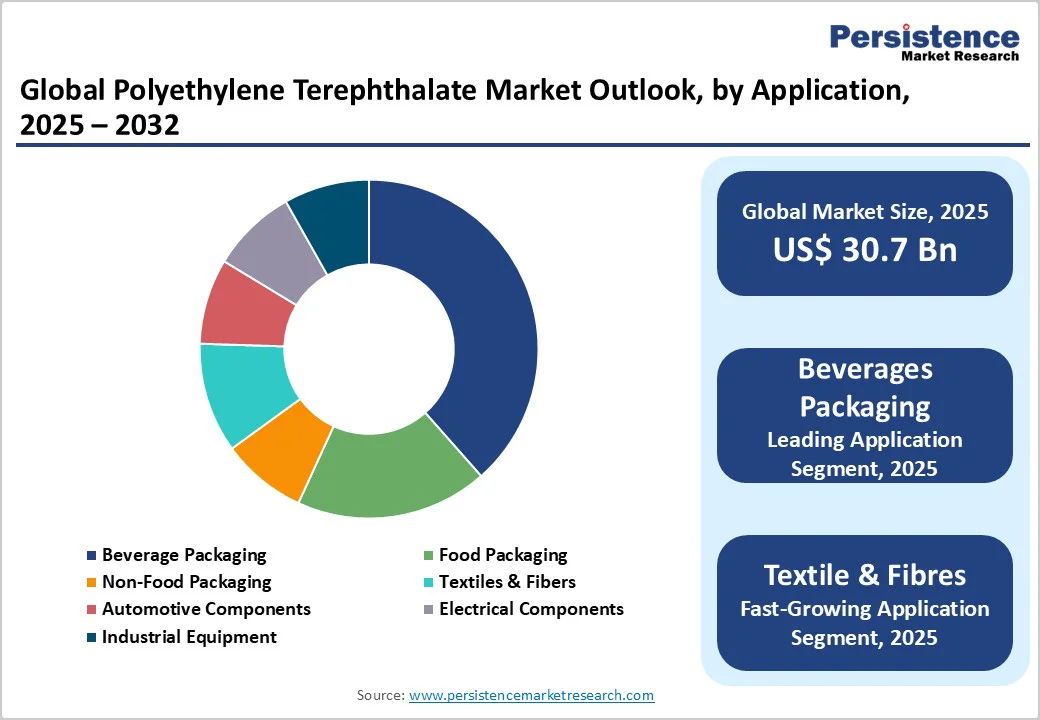

The global Polyethylene Terephthalate market size is likely to value at US$ 30.7 billion in 2025 and is projected to reach US$ 41.2 billion, growing at a CAGR of 4.3% between 2025 and 2032. The market’s robust expansion is primarily driven by escalating demand from the beverage packaging industry, where PET’s superior barrier properties, lightweight characteristics, and recyclability make it the preferred choice for carbonated soft drinks and water bottles. Rising consumer preference for convenient, safe, and sustainable packaging solutions continues to propel adoption across food and beverage sectors.

Key Market Highlights

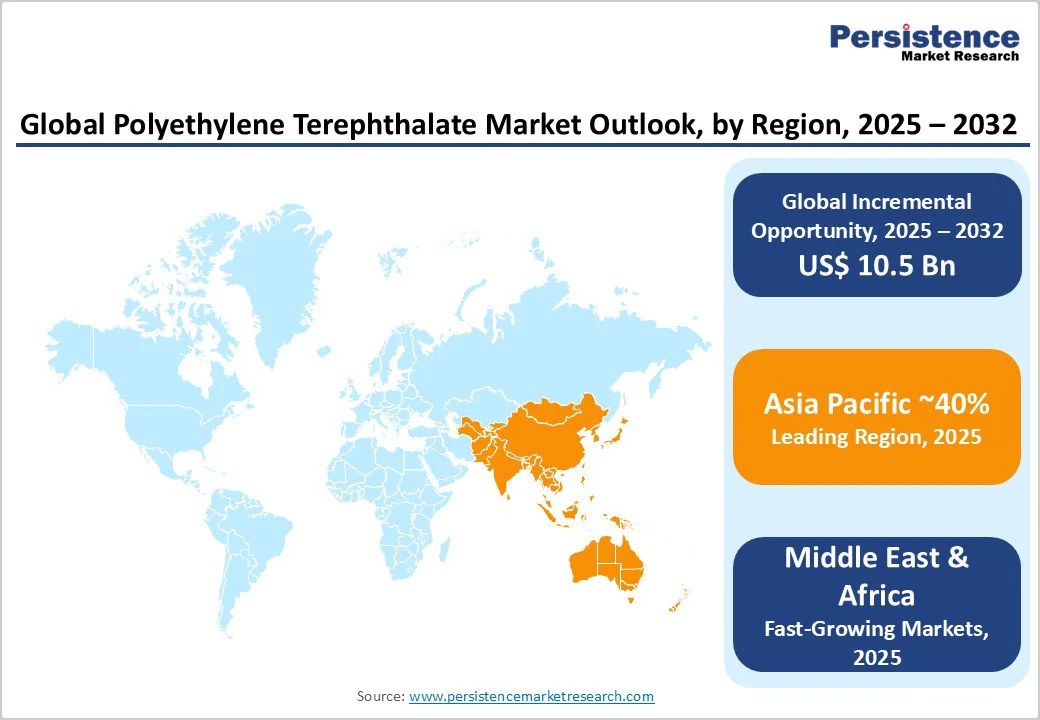

- Leading Region: Asia Pacific dominates the global Polyethylene Terephthalate market with approximately 40% market share in 2025, driven by China’s unmatched production capacity representing 38% of global supply, alongside India’s rapidly expanding consumption patterns.

- Fastest Growing Region: Middle East & Africa emerges as the fastest-growing regional market for Polyethylene Terephthalate, propelled by substantial petrochemical infrastructure investments in Saudi Arabia and UAE.

- Dominant Segment: Food grade PET commands the largest market share at approximately 61% in 2025, reflecting stringent regulatory requirements enforced by FDA and EFSA for food-contact applications.

- Fastest Growing Segment: Textiles & Fibers, particularly Polyester Staple Fiber (PSF), represents the fastest-growing application segment projected to expand at over 5% CAGR through 2032.

- Key Market Opportunity: The accelerating transition toward circular economy models presents substantial growth potential supported by mandatory recycled content regulations, brand owner sustainability commitments, and technological advancements in chemical recycling enabling virgin-quality rPET production.

| Key Insights | Details |

|---|---|

| Polyethylene Terephthalate Market Size (2025E) | US$ 30.7 Bn |

| Market Value Forecast (2032F) | US$ 41.2 Bn |

| Projected Growth CAGR (2025-2032) | 4.3% |

| Historical Market Growth (2019-2024) | 2.3% |

Market Dynamics

Drivers - Surging Demand from Beverage Packaging Sector Driving PET Consumption

The beverage packaging industry remains the dominant driver of PET market growth. According to industry data, global consumption of bottled beverages exceeded 13.5 billion liters in major markets, with PET bottles representing over 58% of beverage packaging formats due to their superior carbonation retention, transparency, and lightweight properties. The Food and Beverage Packaging Market continues to expand rapidly, with PET emerging as the material of choice for brands seeking to reduce transportation costs while maintaining product freshness.

Major beverage manufacturers including Coca-Cola and PepsiCo have implemented lightweighting initiatives, reducing bottle weights from 21 grams to 18.5 grams while preserving structural integrity, thereby saving approximately 3 million tons of PET annually. The shift toward single-serve and on-the-go consumption patterns, particularly in urbanizing regions, further accelerates demand for PET beverage bottles.

Expanding Textile Applications and Polyester Staple Fiber Production

The textiles and fibers segment is experiencing remarkable growth, with polyester staple fiber (PSF) emerging as the fastest-growing application for PET, projected to expand at over 5% CAGR through 2032. The cotton-to-polyester substitution trend, driven by cotton price volatility and PSF’s superior performance characteristics, is accelerating adoption across the textile value chain.

In 2024, cotton prices experienced significant fluctuations, prompting manufacturers to increase PSF blending ratios in fabrics to ensure cost predictability and supply stability. The automotive and construction industries are increasingly adopting PET-based non-woven materials for insulation and noise-vibration-harshness applications, creating new revenue streams. Government initiatives promoting sustainable textiles and circular economy practices, particularly in the European Union and United States, are incentivizing manufacturers to invest in PET recycling infrastructure, thereby supporting long-term market expansion.

Restraints - Raw Material Price Volatility Impacting Production Economics

PET production costs are highly sensitive to fluctuations in petrochemical feedstock prices, particularly purified terephthalic acid (PTA) and monoethylene glycol (MEG), both derived from crude oil. In post COVID era, crude oil price volatility resulting from geopolitical tensions and supply chain disruptions in key producing regions has created margin pressures for PET manufacturers.

Since PTA and MEG account for approximately 70% of PET production costs, price swings directly impact profitability and competitiveness. Small and medium-sized producers lacking backward integration capabilities face particular challenges in managing input cost variability. The reliance on fossil-based feedstocks also exposes manufacturers to long-term transition risks as carbon pricing mechanisms and environmental regulations become more stringent. These economic pressures may constrain capacity expansion plans and limit market entry for new players.

Regulatory Pressures and Plastic Waste Management Challenges

Increasing regulatory scrutiny on single-use plastics and packaging waste management is creating compliance burdens for PET producers and converters. The European Union’s Single Use Plastics Directive mandates 25% recycled content in PET beverage bottles by 2025, rising to 30% by 2030 for all plastic beverage bottles, alongside 77% collection targets by 2025 and 90% by 2029.

Similar mandates are emerging in North America, with states including California, Washington, and New Jersey implementing 15-25% recycled content requirements. While PET boasts relatively high recyclability compared to other plastics, infrastructure gaps in collection, sorting, and processing limit actual recycling rates. The absence of standardized collection systems in many developing markets and contamination issues in mixed waste streams further impede recycling efficiency.

Opportunities - Accelerating Adoption of Recycled PET (rPET) Creating New Value Chains

The transition toward circular economy models presents significant growth opportunities for the Recycled PET (rPET) Market, which is projected to expand from US$ 13.1 Bn in 2025 to US$ 23.8 Bn by 2032 at a CAGR of 8.9%. Leading global brands including Coca-Cola, PepsiCo, Nestlé, and Unilever have committed to incorporating minimum 25-50% recycled content in their packaging by 2030, creating guaranteed demand for high-quality rPET.

In October 2024, Indorama Ventures, the world’s largest PET producer with over 5.9 million tons’ annual capacity, announced it had recycled 150 billion PET bottles since 2011, with the company now processing 789 bottles per second across 20 recycling facilities in 11 countries. The company has formed strategic partnerships with Suntory, ENEOS Corporation, and Neste to develop the world’s first commercial-scale bio-PET bottles from used cooking oil. Regulatory incentives, including extended producer responsibility schemes, deposit return systems, and tax benefits for recycled content utilization are improving rPET economics.

Category-wise Insights

Grade Analysis

Food grade PET dominates the market with approximately 61% share in 2025, driven by its widespread application in beverage and food contact packaging where safety, regulatory compliance, and barrier properties are paramount. Food grade PET undergoes rigorous decontamination processes to eliminate potential contaminants, with manufacturers employing advanced solid-state polycondensation technologies to achieve intrinsic viscosity levels exceeding 0.80 dl/g. The material’s chemical inertness ensures minimal migration of polymer constituents into food products, maintaining taste integrity while meeting specific migration limit values established by regulatory authorities.

Global beverage giants including Coca-Cola, Danone, and Nestlé Waters exclusively utilize food grade PET for their bottled products, with quality specifications requiring acetaldehyde content below 1 ppm and benzene levels within stringent safety thresholds. Major producers including Indorama Ventures, Alpek, and Reliance Industries maintain dedicated food grade production lines with enhanced quality control systems to meet brand owner requirements and regulatory standards, reinforcing the segment’s dominant market position.

Application Analysis

Beverage packaging maintains the largest application share at approximately 44% in 2025, reflecting PET’s unmatched performance characteristics for carbonated soft drinks, water bottles, and non-carbonated beverages. Within this segment, carbonated soft drinks represent a substantial portion, with PET bottles preferred over glass and aluminum due to their exceptional carbonation retention properties, transparency allowing product visibility, and superior strength-to-weight ratio, reducing transportation costs.

Water bottles constitute another major category, with global bottled water consumption exceeding billions of liters annually, particularly in regions with limited access to potable tap water. India’s Packaged Drinking Water Market is projected to reach US$ 6.5 Bn by 2032 with PET bottles holding 78% of the market share. The segment’s dominance is reinforced by continuous innovation in bottle design, with manufacturers implementing lightweighting initiatives that reduce material consumption while maintaining structural integrity.

Production Method Analysis

The direct esterification method, commonly known as the PTA Method, accounts for approximately 67% of global PET production share in 2025, reflecting its superior cost-effectiveness, simplified process flow, and higher product quality compared to alternative routes. The process offers significant advantages, including fewer intermediate steps, lower energy consumption, and reduced environmental emissions compared to the Transesterification Method using dimethyl terephthalate (DMT).

China operates the world’s largest concentration of PTA-based PET plants, with producers such as Sanfame, Yisheng Petrochemical, and Wankai New Materials collectively operating over 10 million tons per year capacity. Modern facilities incorporate closed-loop MEG recovery systems and heat integration schemes to maximize energy efficiency while minimizing operational costs, reinforcing the method’s competitive advantage in global PET production.

Regional Insights

North America Polyethylene Terephthalate Market Trends

North America maintains a significant position in the global PET market, with the United States leading regional consumption driven by strong beverage industry presence and stringent packaging quality standards. The region has witnessed substantial regulatory developments, with the U.S. Environmental Protection Agency (EPA) implementing enhanced oversight of plastic waste management. State-level initiatives are also accelerating sustainability transitions, with California, Washington, and New Jersey mandating 15-25% recycled content in PET bottles by 2025, creating guaranteed demand for rPET and incentivizing investment in advanced recycling infrastructure.

The region’s established PET producers, including Alpek DAK Americas and Indorama Ventures’ North American operations, are investing in both virgin and recycled PET capacity, with a focus on food-grade applications meeting FDA approval standards. The National Association for PET Container Resources (NAPCOR) provides industry leadership through technical guidance and sustainability advocacy, having demonstrated that PET packaging delivers superior environmental performance compared to glass and aluminum alternatives, potentially saving 4.4 billion liters of water annually.

Europe Polyethylene Terephthalate Market Trends

Europe represents a technologically advanced and highly regulated PET market, with Germany, United Kingdom, France, and Spain driving regional consumption patterns. The European Union’s comprehensive regulatory framework, particularly the Single Use Plastics Directive and Packaging and Packaging Waste Regulation (PPWR), establishes among the world’s most ambitious circularity targets. European beverage consumption patterns show a strong preference for premium and sustainable packaging, with bottled beverage sales in the UK exceeding 13.5 billion liters in 2020, predominantly utilizing PET containers.

Germany leads European innovation in deposit return systems and closed-loop recycling, achieving among the highest collection rates globally, while providing model infrastructure for other member states. SABIC’s advanced recycling joint venture with Plastic Energy in Geleen, Netherlands, processing 20,000 tons of plastic waste annually into certified circular polymers, exemplifies regional commitment to chemical recycling technologies complementing mechanical processes.

Asia Pacific Polyethylene Terephthalate Market Trends

Asia Pacific dominates global PET production and consumption with approximately 40% market share in 2025, anchored by China’s unmatched manufacturing scale and India’s rapid demand growth. China alone operates over 13.2 million tons per year PET capacity, representing 38% of global production, with major integrated facilities operated by Sanfame Group, Yisheng Petrochemical, Wankai New Materials, and Zhejiang Hengyi. Chinese producers benefit from extensive backward integration into PX, PTA, and MEG production, with companies like Rongsheng Petrochemical, Hengyi Industries, and Tongkun Group operating integrated refinery-to-polyester complexes, enabling superior cost competitiveness.

India presents the region’s fastest-growing market, with PET demand expanding at 7.1% CAGR between 2025-2032, driven by surging packaged food and beverage consumption, expanding middle class, and rapid urbanization. Southeast Asian nations including Indonesia, Vietnam, Thailand, and Malaysia are witnessing rapid market expansion driven by favorable demographics, rising disposable incomes, and manufacturing sector growth, with producers establishing integrated facilities to serve regional and export markets. Government initiatives promoting domestic manufacturing and sustainability are accelerating investment in PET production and recycling infrastructure across the region.

Competitive Landscape

The global polyethylene terephthalate market exhibits a moderately consolidated structure with the top 10 producers controlling over 60% of global production capacity in 2024, creating significant barriers to entry through economies of scale and integrated supply chains. Indorama Ventures maintains clear market leadership as the world’s largest PET producer with combined capacity exceeding 5.9 million tons annually across 63 manufacturing and recycling facilities in 26 countries spanning Asia Pacific, North America, Europe, and Middle East & Africa.

Alpek S.A.B. de C.V, Sanfangxiang Group, Yisheng Petrochemical, and Wankai New Materials follows the market leadership with increasing focus on recycled PET. Mid-tier regional specialists differentiate through specialized grade offerings, technical service capabilities, and strategic positioning near key end-markets, enabling responsive supply and customized resin properties.

Competitive dynamics emphasize technology advancement, sustainability credentials, and vertical integration as key differentiation factors, with companies investing in bio-based feedstock development, chemical recycling infrastructure, and advanced lightweighting innovations to capture growing demand from brand owners committed to circular economy principles.

Key Market Developments

- September 2024: Indorama Ventures entered into a joint venture with Varun Beverages Limited and Dhunseri Group to establish multiple cutting-edge PET recycling facilities across India, targeting expansion of food-grade rPET production capacity to serve the rapidly growing Indian beverage market and support brand owner sustainability commitments.

- August 2025: Indorama Ventures announced reaching 150 billion PET bottles recycled since 2011, collectively processing 789 bottles per second across its global network of 20 recycling facilities in 11 countries, representing estimated avoidance of 3.8 million tons of CO? emissions and reinforcing leadership in circular economy practices.

- October 2024: Indorama Ventures, in collaboration with Suntory, ENEOS Corporation, Mitsubishi Corporation, Iwatani, and Neste, launched the world’s first commercial-scale bio-PET bottle derived from used cooking oil, marking a significant breakthrough in sustainable packaging and demonstrating viability of alternative feedstock pathways for PET production.

Companies Covered in Polyethylene Terephthalate Market

- Indorama Ventures

- BASF SE

- Far Eastern New Century Corp

- Zhejiang Wankai New Materials Co Ltd

- Reliance Industries Ltd.

- The Dow Chemicals Company

- Nan Ya Plastics Corporation

- DAK Americas

- SABIC

- SK Chemicals

- Neo Group

- Alpek S.A.B. de C.V.

- Lotte Chemical Corporation

- Selenis

- Zhejiang Hengyi Group Co., Ltd.

Frequently Asked Questions

The global Polyethylene Terephthalate market is projected to reach US$ 41.2 Bn by 2032, growing from US$ 30.7 Bn in 2025 at a compound annual growth rate of 4.3% during the forecast period.

The market is primarily driven by escalating demand from the beverage packaging industry where PET’s superior barrier properties, lightweight characteristics, and recyclability make it preferred for carbonated soft drinks and water bottles.

Food grade PET dominates the market with approximately 61% share in 2025, driven by stringent regulatory requirements from FDA and EFSA for food-contact applications.

Asia Pacific leads the global Polyethylene Terephthalate market with approximately 40% market share in 2025, anchored by China’s dominant production capacity of over 13.2 million tons per year.

The accelerating transition toward circular economy models presents the most significant growth opportunity, with the Recycled PET (rPET) Market projected to expand from US$ 13.1 Bn in 2025 to US$ 23.8 Bn by 2032 at 8.9% CAGR.