- Specialty & Fine Chemicals

- Catalysts in Petroleum Refining Market

Catalysts in Petroleum Refining Market Size, Share, and Growth Forecast 2026 - 2033

Catalysts in Petroleum Refining Market by Ingredients (Zeolites, Metals, Chemical Compounds), Metal Component (Transition Metals, Others), Physical Form (Powder, Extrudates, Spheres & Beads), Applications, and Regional Analysis 2026 - 2033

Catalysts In Petroleum Refining Market Share and Trends Analysis

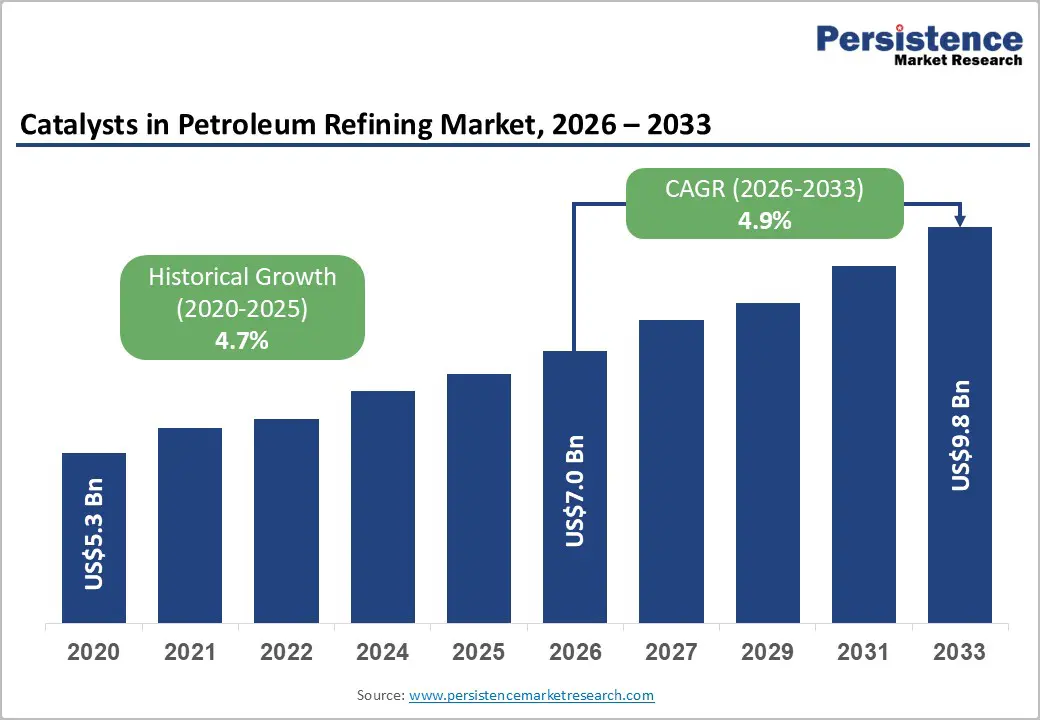

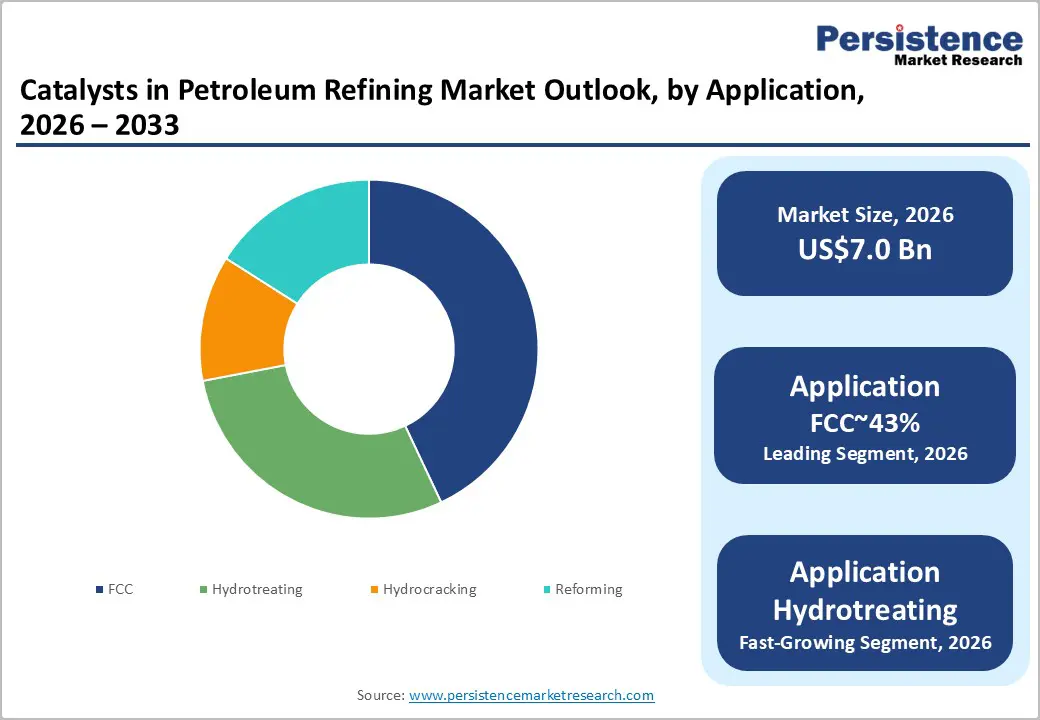

The global catalysts in the petroleum refining market size is likely to be valued at US$ 7.0 billion in 2026 and is expected to reach US$ 9.8 billion by 2033, growing at a CAGR of 4.9% during the forecast period from 2026 to 2033, driven by the escalating demand for high-octane fuels and the transition toward ultra-low sulfur diesel (ULSD) across major transportation sectors. The increasing complexity of crude oil slates, characterized by heavier and high-sulfur feedstocks, necessitates advanced hydro-processing and Fluid Catalytic Cracking (FCC) catalyst technologies to maintain refinery margins.

Key Industry Highlights:

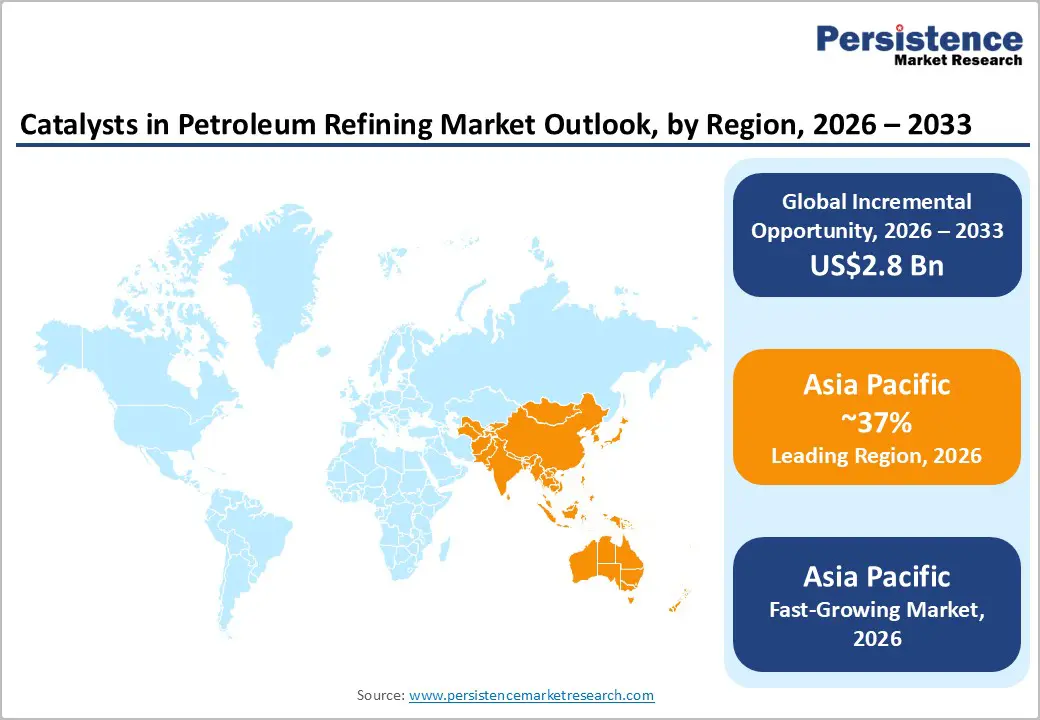

- Leading Region: Asia Pacific is projected to lead the catalysts in the petroleum refining market due to the world’s largest refining capacity, regulatory compliance mandates, and sustained capital deployment across China and India, accounting for approximately 37% share in 2026, supported by technology adoption, digital process integration, and a mature manufacturing ecosystem.

- Fastest-growing Region: Asia Pacific is anticipated to grow fastest due to new refinery investments, integrated refining–petrochemical complexes, policy support, and adoption across emerging ASEAN markets.

- Leading Ingredients: Zeolites are expected to lead accounting with approximately 41% share in 2026 through large-scale FCC adoption, throughput optimization, selectivity, and high-value petrochemical production.

- Leading Applications: The Fluid Catalytic Cracking (FCC) application is projected to dominate for operational flexibility, feedstock adaptability, efficiency, and functional use across high-volume refineries, holding approximately 43% share in 2026.

- Key Industry Developments: In November 2024, Ecovyst launched AlphaCat® advanced silica materials designed to enhance catalyst support performance in renewable fuel and bio-feedstock processing applications.

| Key Insights | Details |

|---|---|

|

Catalysts in Petroleum Refining Market Size (2026E) |

US$7.0 Bn |

|

Market Value Forecast (2033F) |

US$9.8 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

4.9% |

|

Historical Market Growth (CAGR 2020 to 2025) |

4.7% |

Market Factors - Growth, Barriers, and Opportunity Analysis

Increasing Demand for Light Distillates and Petrochemical Feedstocks

The global refining landscape is increasingly shaped by rising demand for light distillates and petrochemical feedstocks, reflecting structural shifts in downstream consumption. Transport fuels and chemical-grade intermediates are gaining priority as heavy fuel oil demand stabilizes, particularly across Asia Pacific refining hubs. This demand rebalancing is reinforcing the strategic importance of conversion intensity, positioning refineries to favor output flexibility and higher-value product slates aligned with petrochemical integration strategies.

Fluid catalytic cracking units sit at the center of this transition, as refiners seek to optimize yields from heavier feedstocks while protecting operating margins. Advanced zeolite-based catalyst systems are enabling higher selectivity toward light olefins and gasoline while suppressing coke formation and energy losses. These performance gains directly influence refinery economics by extending run lengths, stabilizing throughput, and supporting compliance with evolving fuel quality standards. As a result, catalyst efficiency is no longer a process-level consideration but a core determinant of competitive positioning within the global refining value chain.

Volatility in Raw Material Supply Chains

Volatility in catalyst raw material costs represents a structural restraint on market expansion, particularly for formulations dependent on platinum group metals and rare-earth inputs. Price instability is amplified by concentrated supply chains and recurring geopolitical disruptions in key producing regions, introducing procurement risk and budgeting uncertainty for refiners. These dynamics compress capital allocation flexibility, especially during margin-constrained operating cycles, and reduce willingness to commit to large-scale catalyst replacement programs.

Cost pressures are further intensified by the specialized and research-intensive nature of catalyst development. Continuous innovation is required to meet evolving feedstock complexity and regulatory thresholds, driving sustained investment in advanced materials science and process engineering. Smaller and mid-sized suppliers face disproportionate exposure, as limited scale restricts their ability to absorb input price swings or amortize development costs. Collectively, these factors reinforce industry consolidation trends and act as a moderating force on near-term adoption of next-generation catalyst systems.

Integration of Bio-refining and Renewable Diesel Production

The integration of bio-refining pathways is emerging as a structurally significant opportunity within the refining catalyst landscape, driven by regulatory pressure to decarbonize liquid fuel portfolios. Refiners are increasingly adopting co-processing strategies and repurposing legacy hydrotreating assets to accommodate renewable feedstocks, positioning renewable diesel and sustainable aviation fuel as scalable complements to conventional outputs. This transition is reinforced by policy frameworks targeting lifecycle emissions reduction and long-term fuel diversification.

Catalyst demand is evolving accordingly, with heightened emphasis on formulations capable of managing high oxygen content, variable acidity, and distinct contaminant profiles associated with biological oils. Performance differentiation in this segment is increasingly linked to tolerance, stability, and yield preservation under non-traditional operating conditions. As technology platforms converge across fossil and renewable systems, catalyst suppliers with cross-domain capabilities are positioned to capture incremental value. This shift is expected to unlock a sizable addressable opportunity as refiners accelerate compliance-driven capital redeployment toward low-carbon fuel production.

Category–wise Analysis

Ingredients Insights

Zeolites are projected to dominate the petroleum refining catalyst market, accounting for approximately 41% share in 2026, underpinned by their entrenched role in Fluid Catalytic Cracking (FCC) across large-scale refineries and petrochemical plants. The adoption remains anchored by their high thermal stability, molecular sieve selectivity, and feedstock flexibility, with refiners prioritizing throughput optimization and consistent light olefin yields in high-volume operations. Ongoing platform evolution, including AI-enabled catalyst design, digital twin simulations for pore structure optimization, and enhanced coke resistance, continues to reinforce replacement cycles and utilization intensity. Companies such as W. R. Grace, Honeywell UOP, and BASF are expanding portfolios with hierarchical and rare-earth-modified zeolite formulations to integrate into refinery operations and long-term service contracts. This combination of mature infrastructure, predictable feedstock processing requirements, and technological lock-in sustains zeolites’ dominance within structured catalytic workflows.

Zeolites are anticipated to be the fastest-growing segment also, within the petroleum refining catalyst market, driven by the shift from fuel-focused operations to high-value petrochemical production. Growth is being catalyzed by innovations such as rare-earth-minimized formulations, in-situ crystallized zeolites, and digital twin-assisted batch optimization, which materially improve olefin yields, catalyst lifespan, and energy efficiency. Accelerating adoption is supported by automation and AI-guided process integration, lowering operational friction for refiners adopting advanced catalysts for Crude-to-Chemicals and bio-feed co-processing. Companies including Ketjen, W. R. Grace, and BASF are scaling new zeolite frameworks and service models to capture early-cycle demand and embed refinery switching costs. As industrial validation, regulatory compliance, and workforce familiarity increase, this segment is expected to outpace overall market growth over the forecast period.

Applications Insights

Fluid Catalytic Cracking (FCC) is projected to remain the leading application in the petroleum refining catalyst market, accounting for approximately 43% share in 2026, underpinned by its entrenched role in converting heavy crude fractions into high-value gasoline and light olefins across large-scale refineries. Adoption is anchored by throughput efficiency, catalyst longevity, and the ability to flex between fuel and petrochemical production, with refiners prioritizing operational flexibility and swing capacity in high-volume units. Ongoing platform evolution, including AI-optimized regenerator heat balance, short-contact-time reactors, and co-processing of bio-oils, reinforces utilization intensity and replacement cycles. Vendors such as W. R. Grace, Ketjen (Albemarle), and BASF are expanding offerings with high-propylene FCC catalysts and distributed-pore technologies to lock in refinery workflows and long-term service contracts. This combination of mature infrastructure, integration capability, and adaptable feedstock handling sustains FCC’s dominance in modern refining operations.

Hydrotreating is expected to be the fastest-growing application within the petroleum refining catalyst market, driven by strict sulfur regulations and the rise of renewable diesel production. Growth is catalyzed by high-pressure NiMo and CoMo catalysts, multi-layer “active grading” beds, and coke-resistant nano-catalysts, which materially improve desulfurization efficiency, hydrogen utilization, and operational uptime. Accelerating adoption is supported by digital monitoring, predictive maintenance tools, and circular catalyst recovery programs, lowering operational friction for first-time adopters. Companies including Haldor Topsoe, ART, and Axens are scaling advanced hydroprocessing platforms and renewable diesel-ready catalyst systems to capture early-cycle demand and embed switching costs. As industrial validation, regulatory enforcement, and renewable fuel integration increase, hydrotreating is expected to outpace overall market growth over the forecast period.

Regional Insights

Asia Pacific Catalysts in Petroleum Refining Market Trends

Asia Pacific is expected to remain the leading regional market, accounting for 37% of global demand, underpinned by the world’s largest refining capacity and sustained capital deployment across China and India. Regulatory frameworks such as China’s Double Carbon objectives and India’s BS-VI emission standards are intensifying demand for hydrotreating and fluid catalytic cracking catalysts, reinforcing compliance-driven adoption. The region’s cost-advantaged manufacturing base and expanding downstream integration continue to support its position as a global refining hub, with policy alignment accelerating technology upgrades across both private and state-owned assets.

Asia Pacific is also projected to be the fastest-growing region, driven by new refinery investments and the emergence of large-scale integrated refining–petrochemical complexes. ASEAN economies, including Vietnam and Indonesia, are increasing refining self-sufficiency and expanding addressable demand beyond traditional major markets. Concurrent investment in modernization and energy-efficiency retrofits is strengthening infrastructure maturity, while integrated catalyst solutions are gaining relevance to support higher conversion severity. Collectively, these dynamics position Asia Pacific ahead of more mature regions, where growth is constrained by replacement demand and tighter capital discipline.

North America Catalysts in Petroleum Refining Market Trends

North America is expected to maintain a strong position in the global catalyst market, supported by a highly sophisticated and complex refining infrastructure. The U.S. anchors regional performance, benefiting from abundant domestic tight oil resources that necessitate tailored catalyst formulations for efficient conversion. Regulatory oversight led by the Environmental Protection Agency, particularly under Tier 3 gasoline standards, continues to drive sustained investment in hydrotreating capacity, reinforcing compliance-led demand rather than volume expansion.

The region also benefits from a mature innovation ecosystem, with advanced research capabilities supporting continuous improvement in fluid catalytic cracking and hydrocracking technologies. Capital allocation is increasingly directed toward green refining initiatives, including the conversion of conventional refining assets to renewable diesel production. This shift reflects a strategic response to decarbonization pressures rather than capacity growth, positioning North America as a technology-led and regulation-driven market. Compared with Asia Pacific’s scale-led expansion, regional growth is expected to remain measured, anchored by asset optimization, emissions compliance, and technology upgrading priorities.

Europe Catalysts in Petroleum Refining Market Trends

Europe is expected to remain a structurally mature but strategically significant market, shaped by early adoption of stringent environmental standards and deep regulatory harmonization. Euro VI requirements and the anticipated transition toward Euro VII are reinforcing demand for high-efficiency catalyst systems, while elevating compliance thresholds and barriers to entry. Countries such as Germany, the U.K., and France continue to lead in catalyst performance optimization and recycling frameworks, aligning with broader circular economy objectives embedded within EU industrial policy.

Despite these strengths, Europe faces structural headwinds from limited capacity expansion and the risk of selective refinery closures. In response, refiners are reallocating capital toward bio-feedstock processing, advanced hydrotreating, and carbon capture integration to preserve asset relevance under tightening emissions constraints. This strategic pivot favors specialized, high-margin catalyst formulations over volume-driven demand. As a result, the regional competitive landscape remains highly consolidated, with growth prospects tied more closely to technology intensity and regulatory alignment than to incremental throughput expansion.

Competitive Analysis

The global catalysts in petroleum refining market is highly consolidated, with the top five players controlling over 60% of the total market share. W.R. Grace, Albemarle, BASF, and Honeywell UOP lead through deep process chemistry expertise, proprietary formulations, and long-term supply agreements with refiners. Entry barriers remain high due to sustained R&D intensity, qualification cycles, and the need for on-site technical services. Market concentration is strongest in FCC and hydro processing catalysts, where performance guarantees and continuous optimization create durable supplier relationships.

Recent strategies reinforce this structure. Honeywell UOP launched an advanced hydrotreating catalyst in 2024 to strengthen ultra-low sulfur diesel compliance, targeting growth in Asia. BASF secured upstream integration by acquiring a minority stake in a Chinese zeolite producer to stabilize FCC supply economics. Albemarle partnered with ExxonMobil on regenerative catalyst technology, aligning efficiency gains with tightening emissions regulations and long-term decarbonization goals.

Key Industry Developments:

- In August 2024, BASF launched the Fourtiva fluidized catalytic cracking catalyst to boost high-octane gasoline yields. The catalyst enhanced butylene selectivity by 5–10%, enabling refineries to increase profitable gasoline blending components and improve FCC unit economics amid rising demand for premium fuels.

- In July 2024, Ecovyst announced an equity investment in Pajarito Powder to advance hydrogen catalyst technologies. The investment strengthened catalyst portfolios for hydrogen integration in refining and helped accelerate blue hydrogen adoption while potentially reducing emissions by up to 30% in hydrocracking applications.

Companies Covered in Catalysts in Petroleum Refining Market

- W.R. Grace & Co.

- Albemarle Corporation

- Ecovyst

- BASF SE

- Honeywell International Inc.

- Axens

- Clariant AG

- Haldor Topsoe A/S

- Sinopec Catalyst Co.

- ExxonMobil Catalysts

- Shell Catalysts & Technologies

- Johnson Matthey

- Chevron Lummus Global

- Arkema S.A.

- Evonik Industries AG

- Criterion Catalysts & Technologies

- JGC Holdings Corporation

Frequently Asked Questions

The global catalysts in petroleum refining market is projected to be valued at US$7.0 bn in 2026 and are expected to reach US$9.8 bn by 2033, reflecting steady demand from complex refining operations.

Demand is increasing due to the shift toward ultra-low sulfur fuels, rising processing of heavy and high-sulfur crude oil, and the need to maintain refinery margins through advanced hydrotreating and FCC catalyst technologies.

The catalysts in petroleum refining market are expected to grow at a CAGR of 4.9% between 2026 and 2033, supported by refinery upgrades and tightening environmental regulations.

The fastest growth opportunities are emerging in Asia Pacific, led by expanding refining capacity in China and India, modernization of existing refineries, and rising fuel demand across the industrial and transportation sectors.

Key players in the catalysts in petroleum refining market include W.R. Grace & Co., Albemarle Corporation, BASF SE, Honeywell International, Axens, Clariant AG, Haldor Topsoe A/S, Johnson Matthey, Sinopec Catalyst, ExxonMobil Catalysts, Shell Catalysts & Technologies, Evonik Industries, and Criterion Catalysts & Technologies.