- Baby Care & Accessories

- Pet Lodging Market

Pet Lodging Market Size, Share, and Growth Forecast 2026 - 2033

Pet Lodging Market by Pet Type (Dogs, Cats, Others), Service Type (Boarding, Daycare, Training, Luxury Pet Hotels), Booking Mode (Online, Offline), Regional Analysis, 2026 - 2033

Pet Lodging Market Size and Trend Analysis

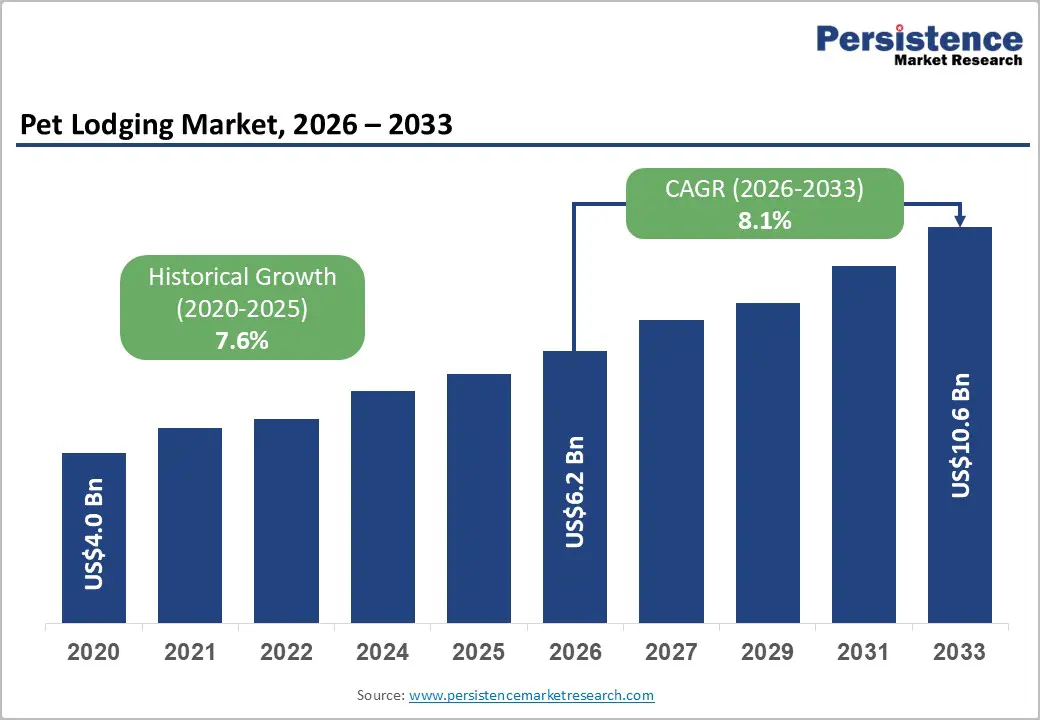

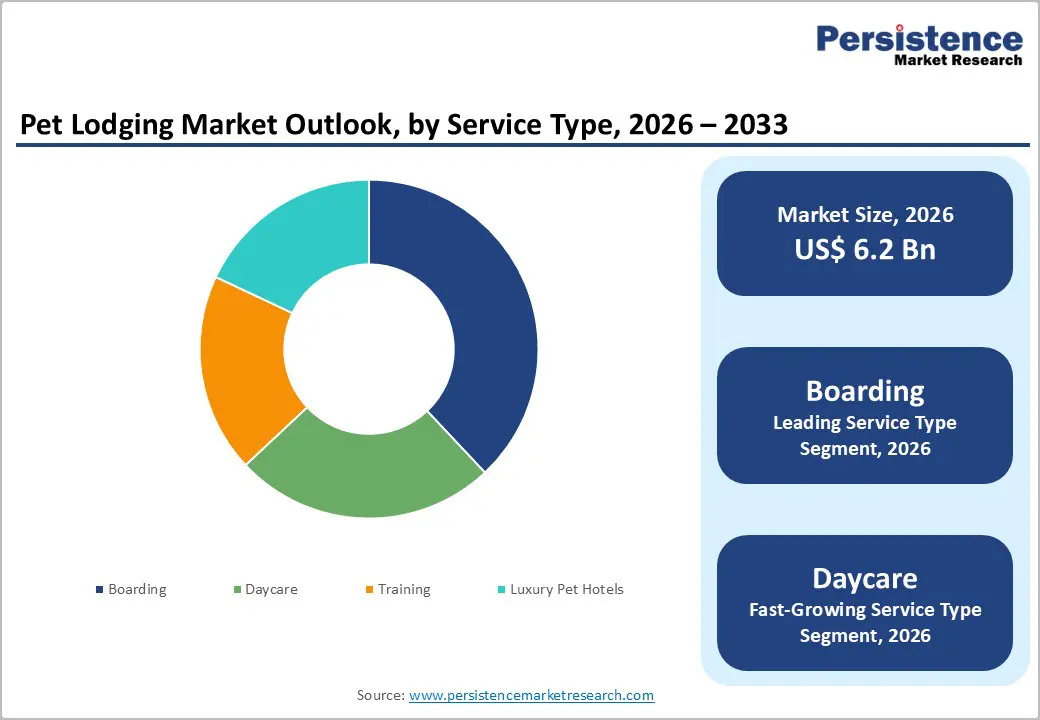

The global pet lodging market size is likely to reach US$ 6.20 billion in 2026 and US$ 10.69 billion by 2033, expanding at a CAGR of 8.1%. It is driven by accelerating pet ownership rates, deepening human-animal bonds, and rising consumer willingness to spend on premium care.

Dual-income households, increased business travel, and the premiumization wave have pushed the owners toward professional, facility-based solutions. The rising proportion of pet owners who consider their pets as "family members" across North America, Europe, and the Asia Pacific directly correlates with higher per-visit expenditure and increased repeat booking frequencies.

Key Industry Highlights:

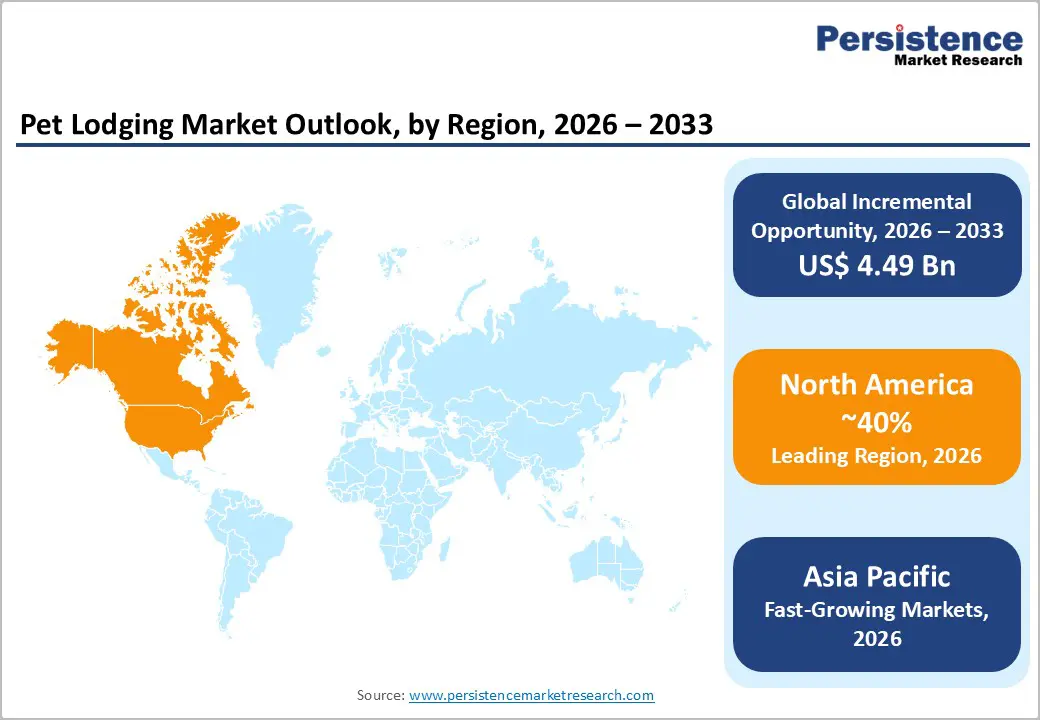

- Leading Region: North America commands approximately 40% of global revenue share, anchored by exceptional pet ownership density, mature franchise infrastructure, and high per-visit consumer spending.

- Fastest Growing Region: Asia Pacific is projected to expand at a CAGR of 8.7% through 2033, driven by accelerating pet ownership, urban middle-class expansion, and digital platform scaling across China, India, Japan, and Southeast Asia.

- Leading Category: Dogs dominate pet type segmentation with approximately 46% market share, underpinned by the structural necessity of professional supervision and higher boarding frequency requirements relative to all other pet types.

- Fastest Growing Service Segment: Daycare is the fastest growing service type, accelerating as return-to-office mandates across North America and Europe drive structured weekday care demand from working pet owners.

- Key Market Opportunity: Online booking penetration at 78% creates a compounding advantage for digital-first operators leveraging loyalty integration, AI-driven personalization, and real-time monitoring to capture disproportionate market share.

Market Dynamics

Drivers - Surging Pet Humanization Trend Elevating Service Standards and Spending

The deepening humanisation of pets is the most powerful demand driver across the global Pet Lodging Market, directly translating into higher discretionary spending on professional lodging services. Over 67% of US households own at least one pet, with a growing majority selecting facilities based on welfare standards and staff expertise rather than price. This behavioral shift compels operators to invest in higher-quality infrastructure and certified personnel to remain competitive.

The consequence is a structurally elevated average revenue per booking and a widening addressable base. Millennial and Gen Z pet owners who treat companion animals as full household members are disproportionately driving this premiumization wave, reinforcing long-term demand for enriched service packages, specialized care programs, and experiential lodging environments that mirror domestic comfort standards.

Expansion of Dual-Income and Remote-Transitioning Households Increasing Boarding Demand

The persistent rise in dual-income households and the partial reversal of pandemic-era remote working arrangements represent a second structural force reshaping market demand. As corporate return-to-office mandates expanded through 2023-2024, millions of pet owners who had previously provided at-home daytime care became reliant on external professional services. Boarding and daycare bookings in urban markets registered volume growth of approximately 12-15% year-on-year during this transitional period.

This dynamic is expected to sustain elevated demand across the forecast window, particularly across metropolitan markets in North America and Europe, where office occupancy rates continue recovering. The structural permanence of hybrid work schedules further ensures that professional pet lodging remains an essential, recurring household expenditure rather than an occasional discretionary purchase.

Restraints - High Operational Costs Creating Barriers for Independent and Small-Scale Operators

High capital and operational cost burdens represent one of the most consequential restraints shaping the Pet Lodging Market. Staffing ratios mandated by animal welfare regulations, combined with facility maintenance, veterinary partnerships, and insurance premiums, generate cost structures that are difficult for independent operators to absorb without passing increases directly onto consumers. Price-sensitive pet owners facing fee increases often revert to informal arrangements, limiting the addressable market for professional services.

This pressure is particularly acute in high-cost urban markets across Western Europe and the United States, where labor costs represent upward of 50% of total operating expenditure. Independent operators unable to achieve economies of scale face sustained margin compression, accelerating consolidation toward larger franchise-backed and corporate-owned facility networks.

Regulatory Heterogeneity and Licensing Complexity Impeding Market Scalability

The pet lodging sector operates within a fragmented and inconsistent regulatory environment, creating meaningful barriers for operators attempting to scale across multiple jurisdictions. Licensing requirements, staff-to-animal ratios, facility standards, and health inspection protocols vary substantially between countries and even between municipalities within the same country. Operators pursuing franchise or multi-site expansion models must invest disproportionately in regulatory navigation, slowing growth timelines and deterring otherwise well-capitalized market entrants.

This complexity is particularly pronounced across Asia Pacific markets, where national-level regulatory frameworks governing commercial pet care are still in the early stages of maturity. Until greater harmonization emerges, compliance asymmetry will continue imposing unequal cost burdens across operators, structurally disadvantaging smaller participants while reinforcing the competitive positioning of established, compliance-experienced industry leaders.

Opportunities - Digital Platform Integration and Direct-to-Consumer Booking Models Unlocking Scalable Growth

The accelerating shift toward app-based and online booking represents one of the most monetizable opportunities in the Pet Lodging Market through 2033. Operators investing in proprietary digital infrastructure for real-time availability management, AI-driven personalization, webcam access, and loyalty program integration can command premium pricing while simultaneously reducing customer acquisition costs. Online booking penetration already stands at approximately 78% in leading markets, yet interface sophistication among independent operators remains comparatively underdeveloped.

This gap presents a decisive first-mover advantage. Operators who prioritize mobile-first booking experiences and CRM-integrated communication systems as a primary competitive differentiator will be best positioned to capture disproportionate market share as digital expectations among millennial and Gen Z pet owners continue escalating throughout the forecast period.

Luxury and Wellness-Oriented Pet Lodging Capturing the Premiumization Wave

Luxury pet lodging encompassing spa treatments, breed-specific nutrition programmes, hydrotherapy, and individual suite accommodation represents a high-margin growth frontier the market is only beginning to fully exploit. Consumer research consistently demonstrates that high-income pet owners across North America and Western Europe are willing to pay a 30-50% premium for luxury facilities over standard boarding alternatives, creating structurally attractive opportunities for tiered service models that maximize revenue per visit without proportional cost increases.

The window for first-mover positioning in this sub-segment remains open but is narrowing. Franchise networks and premium hospitality brands considering adjacency plays into luxury pet lodging stand to benefit substantially from brand trust transfer and significant demographic overlap with their existing high-net-worth consumer bases.

Category-wise Analysis

Pet Type Insights

Dogs represent the dominant segment, commanding nearly 46% of the share in 2026. This reflects the higher frequency of boarding and daycare requirements relative to other pet types. Dogs need consistent external supervision and socialization in the absence of owners, making professional lodging a near-necessity. This behavioral dependency ensures sustained, predictable demand regardless of broader macroeconomic conditions.

The cats segment is the fastest-growing category within pet type segmentation, reflecting rising ownership rates in urban markets across Asia Pacific and Europe, where apartment living favours lower-maintenance companions. Operators historically focused on canine services are now investing in dedicated feline accommodation spaces, with specialized quiet zones and vertical enrichment features becoming standard differentiators in leading facilities responding to this emerging demand.

Service Type Analysis

Boarding leads the pet lodging market's service type segmentation with approximately 38% of total revenue share, driven by the fundamental requirement for overnight and multi-day supervision during owner travel a need no alternative service category can substitute. Boarding generates the highest average transaction value per visit and benefits from repeat booking patterns tied to predictable travel calendars, making it the most reliable revenue anchor for operators across all geographies.

Daycare is the fast-growing service type segment, accelerating as return-to-office trends drive weekday demand from working pet owners seeking structured, supervised daytime care. The Luxury Pet Hotels sub-segment is simultaneously attracting significant investor attention, as premiumization dynamics push a meaningful share of high-income consumers away from commodity boarding toward experience-driven, hospitality-grade alternatives.

Booking Mode Analysis

Online booking dominates the Pet Lodging Market's booking mode segmentation with an estimated 78% share, reflecting the broader digitalization of consumer service purchasing and the convenience premium pet owners place on instant confirmation, webcam access, and digital record management. Platform-based and app-first operators have consistently outperformed traditional walk-in facilities on customer acquisition efficiency and repeat booking rates, reinforcing the structural advantage of digital channels across established markets.

The Offline booking channel is identified as the fast-growing mode within this segmentation, not because digital growth is decelerating, but because independent and rural operators are formalizing in-person service offerings across previously underserved geographies. This reflects a market expanding into communities with lower digital infrastructure penetration, making offline channels the marginal growth driver at the expanding edges of the addressable market.

Regional Insights

North America Pet Lodging Market Trends and Insights

North America leads the global pet lodging market with approximately 40% of total revenue share, a position sustained by the region's exceptionally high pet ownership density, mature consumer spending culture, and well-developed franchise-based lodging infrastructure. The United States remains the single largest national market globally, supported by a robust ecosystem of specialist operators, pet-focused insurance products, and digital booking platforms. Canada is emerging as a secondary growth engine, particularly in urban centres where dual-income households and premium pet care spending are expanding rapidly.

- United States Pet Lodging Market Size

The United States accounts for approximately 85% of North America's total pet lodging revenue, equivalent to roughly US$ 2.11 billion in 2026, based on the region's 40% global share. Demand drivers include a pet ownership rate exceeding 67% of households, strong cultural normalisation of professional pet care, and a well-capitalised operator base spanning national franchises and premium independents. The U.S. market is expected to sustain mid-single-digit growth through 2033, with premium service tiers and digital platform investment representing the primary vectors of incremental revenue expansion.

Europe Pet Lodging Market Trends and Insights

Europe represents the second-largest regional market in the global pet lodging market, with structural demand supported by high pet ownership rates across Western Europe and a regulatory environment that enforces rigorous animal welfare standards, effectively raising the quality floor for commercial pet lodging facilities.

Germany, the United Kingdom, and France collectively account for the majority of European revenue, driven by urban professional demographics and growing cultural alignment between European and North American pet ownership attitudes. The EU Animal Welfare Strategy and national-level licensing frameworks continue to shape competitive dynamics by favouring well-capitalised, compliant operators over informal alternatives. Looking ahead, Eastern European markets represent a nascent but accelerating growth frontier for the European pet lodging sector as pet ownership rates and disposable incomes converge toward Western norms.

- Germany Pet Lodging Market Size

Germany commands an estimated 22-25% of the European pet lodging market, making it the region's largest national market. Strong demand drivers include Germany's approximately 16.7 million pet-owning households, rigorous regulatory standards that reinforce consumer confidence in professional facilities, and an affluent urban demographic with high discretionary spending capacity. Forward-looking dynamics suggest that luxury boarding and wellness-integrated service concepts will generate above-average growth in German metropolitan markets through 2033.

- United Kingdom Pet Lodging Market Size

The United Kingdom accounts for approximately 18-20% of total European pet lodging revenue, supported by one of Europe's highest pet ownership densities with an estimated 12 million dogs and 12 million cats registered across UK households, according to the industry data. Post-pandemic behavioral shifts have increased demand for professional boarding, as the partial reversal of remote work arrangements re-established weekday and holiday care requirements. The UK market is expected to see accelerated platform consolidation through 2033 as digital-first booking operators acquire independent facilities.

- France Pet Lodging Market Size

France represents approximately 16% of Europe's pet lodging market share, driven by an estimated 7.5 million dog-owning households and a cultural tradition of high-quality animal care that aligns well with premium service positioning. The French market has historically been characterised by a higher proportion of independent boutique operators relative to franchise chains, creating a differentiated competitive landscape compared to Germany and the UK. This fragmentation creates meaningful consolidation and franchise expansion opportunities for well-capitalized operators targeting France as a strategic growth market through 2033.

Asia Pacific Pet Lodging Market Trends and Insights

Asia Pacific is the fastest growing market for pet lodging, projected to expand at a CAGR of 8.7% by 2033, outpacing all other geographies as structural acceleration forces compound simultaneously. Rapidly rising pet ownership in China, Japan, India, and Southeast Asia is converging with an expanding urban middle class, rising disposable incomes, and a generational shift toward treating pets as family members. Digital booking infrastructure is scaling faster in the Asia Pacific than in any other region, enabling operators to reach pet owners efficiently at lower acquisition costs.

The region is expected to capture a materially larger share of global pet lodging revenue by 2033, driven by greenfield market development rather than market share redistribution from incumbents.

- Japan Pet Lodging Market Size

Japan accounts for approximately 30% of the Asia Pacific's pet lodging revenue, reflecting its status as one of the region's most mature and premium-oriented markets. The country's urbanized, aging population and strong cultural emphasis on pet welfare support above-average per-visit spending, with luxury and wellness-integrated lodging concepts already well-established in Tokyo and Osaka. Going forward, Japan is expected to serve as a benchmark reference market for premium pet lodging concepts expanding elsewhere across the Asia Pacific.

- India Pet Lodging Market Size

India currently represents approximately 10% of Asia Pacific pet lodging revenue but is expanding at one of the fastest rates within the region, driven by a rapidly growing urban middle class, rising pet adoption rates among younger demographics, and accelerating normalization of professional pet care services in Tier 1 cities, including Mumbai, Delhi, and Bengaluru. According to industry data, pet ownership in India grew by approximately 20% between 2020 and 2023, establishing a durable structural foundation for the pet lodging market's expansion. India's market is expected to at least double in absolute revenue terms between 2026 and 2033, making it one of the most compelling growth opportunities in the global pet lodging space.

- Southeast Asia Pet Lodging Market Size

Southeast Asia accounts for approximately 14% of the Asia Pacific's pet lodging revenue, with Thailand, Singapore, Indonesia, and Vietnam emerging as the most commercially significant national markets within the sub-region. Singapore punches above its population weight due to extremely high per-capita pet spending and a wealthy, internationally influenced consumer base that readily adopts premium service concepts. Platform-based and app-first operators are scaling rapidly across Southeast Asia, and the sub-region is expected to see the highest new facility opening rates in the global pet lodging market through 2028.

Competitive Landscape

The Pet Lodging Market operates within a moderately fragmented competitive landscape characterised by a dual-track structure. Large national franchise systems and corporate-backed chains compete for scale-driven cost advantages, while a vast long tail of independent and boutique operators differentiates on specialisation, personalisation, and community trust. The primary basis of competition is shifting decisively from price and location toward digital experience and demonstrable animal welfare credentials.

Consolidation activity is accelerating, with private equity-backed platforms acquiring independent operators in high-density urban markets to build regional density ahead of further roll-up activity. Premium independents and luxury operators continue to differentiate through bespoke service design and facility investment, sustaining a viable counterposition against scale-oriented competitors throughout the forecast period.

Key Developments:

- In January 2025, Dogtopia announced the expansion of its franchise network to exceed 350 locations across North America, with a stated target of 400 open facilities by the end of 2025, reflecting aggressive franchise-driven growth in the urban daycare and boarding segment.

- In March 2024, Mars Petcare deepened its investment in technology-enabled pet services by integrating AI-powered health monitoring tools into partner boarding facilities, positioning wellness data as a differentiator in the premium lodging segment and extending its ecosystem beyond nutrition products.

- In September 2024, K9 Resorts completed a strategic capital raise to fund the acceleration of its luxury boarding franchise model, targeting 25 new site openings across the Eastern United States through 2026, signalling strong investor confidence in the premium end of the pet lodging competitive landscape.

Pet Lodging Market Report - Key Insights & Details

| Key Insights | Details |

|---|---|

| Historical Market Value (2020) | US$ 4.00 Billion |

| Current Market Value (2026) | US$ 6.20 Billion |

| Projected Market Value (2033) | US$ 10.69 Billion |

| CAGR (2026 - 2033) | 8.1% |

| Leading Region | North America (40%) |

| Dominant Pet Type | Dogs (46%) |

| Top-ranking Service Type | Boarding (38%) |

| Top-ranking Booking Mode | Online (78%) |

| Incremental Opportunity (2026 - 2033) | US$ 4.49 Billion |

Companies Covered in Pet Lodging Market

- Mars Petcare

- PetSmart

- Dogtopia

- Camp Bow Wow

- Wag Hotels

- Best Friends Pet Care

- PetBacker

- Paradise 4 Paws

- K9 Resorts

- Barkefellers

- Urban Tails

- Paws Pet Resort

- Pet Palace

- PetsHotel

- Swifto

- Rover Group

- VCA Animal Hospitals

- Hound Haven

- The Kennel Club, Petbarn

Frequently Asked Questions

The market is valued at US$ 6.20 Billion in 2026, projected to reach US$ 10.69 Billion by 2033, growing at a CAGR of 8.1%.

Pet humanisation, dual-income household expansion, and return-to-office mandates driving professional boarding and daycare demand are the primary growth catalysts.

Dogs dominate with approximately 46% share, driven by higher boarding frequency requirements and the structural necessity of professional supervision during owner absences.

North America leads with approximately 40% revenue share, supported by high pet ownership density, mature franchise infrastructure, and elevated per-visit consumer spending.

Luxury and wellness-integrated lodging represents the highest-margin opportunity, with high-income owners willing to pay 30-50% premiums over standard boarding alternatives.

Leading players include Mars Petcare, PetSmart, Dogtopia, Camp Bow Wow, and Rover Group.