- Baby Care & Accessories

- Pet Carriers Market

Pet Carriers Market Size, Share, and Growth Forecast, 2026 - 2033

Pet Carriers Market by Pet Type (Cats, Dogs, Guinea Pigs), Product Type (Soft Sided Carriers, Hard Shell Carriers, Backpack Carriers), Distribution Channel (Pet Store, Online), and Regional Analysis for 2026-2033

Pet Carriers Market Share and Trends Analysis

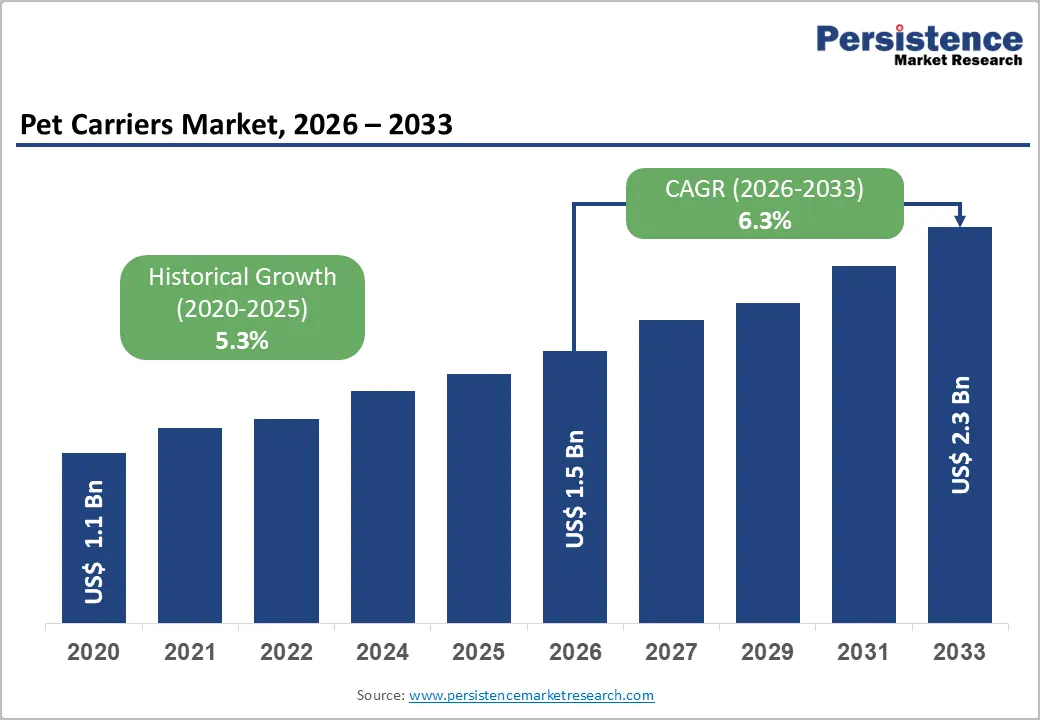

The global pet carriers market size is likely to be valued at US$ 1.5 billion in 2026, and is projected to reach US$ 2.3 billion by 2033, growing at a CAGR of 6.3% during the forecast period of 2026 - 2033. The market is expanding due to rising global pet ownership, increased spending on pet mobility products, and strengthening regulatory requirements for safe pet transportation. According to the American Pet Products Association (APPA), nearly two-thirds of U.S. households own at least one pet, while FEDIAF reports over 90 million pet-owning households across Europe, indicating a broad and stable consumer base. Urbanization and smaller household sizes are also contributing to higher companion animal adoption, particularly cats and small-breed dogs that require portable carriers for travel and veterinary visits. In parallel, e-commerce penetration has improved product accessibility and price transparency, while innovation in lightweight, ventilated, and airline-compliant carrier designs continues to enhance consumer adoption rates globally.

Key Industry Highlights

- Dominant Pet Type: Dogs are set to command approximately 62% revenue share in 2026, while cats are likely to grow the fastest through 2033, supported by increasing preference for compact travel solutions.

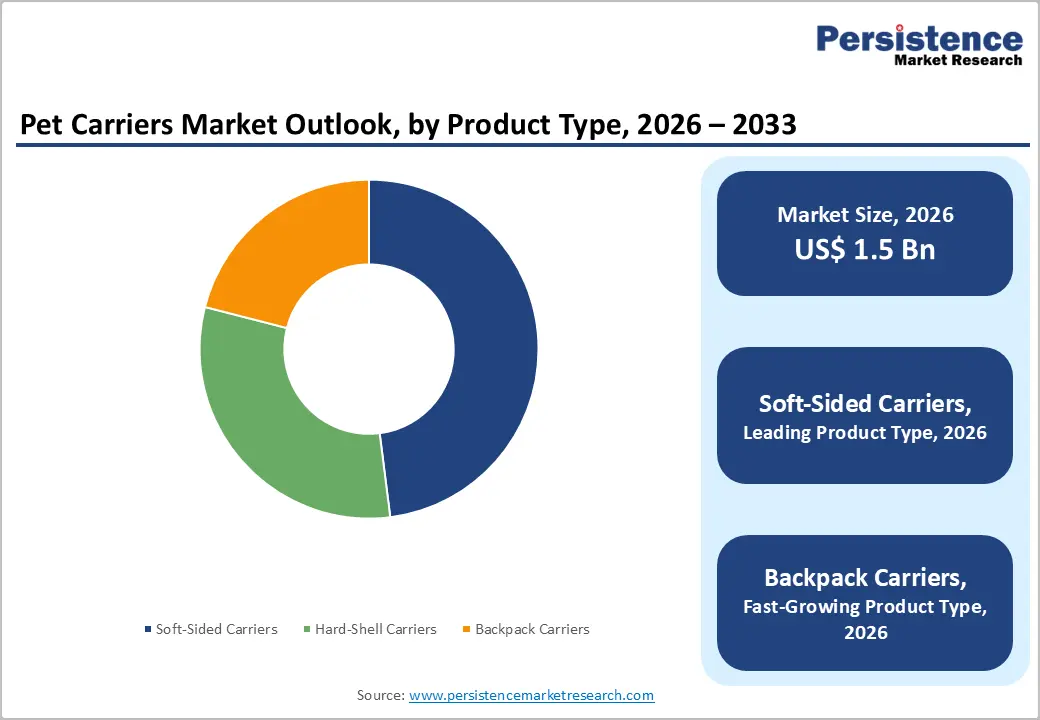

- Leading Product Type: Soft-sided carriers are projected to account for nearly 48% share in 2026, whereas backpack carriers are expected to expand at the fastest pace of 8.4% CAGR during 2026–2033, driven by ergonomic and hands-free mobility trends.

- Dominant Distribution Channel: Pet stores are anticipated to hold about 55% of total revenue in 2026, while online platforms are poised to grow the fastest through 2033, reflecting accelerating e-commerce penetration.

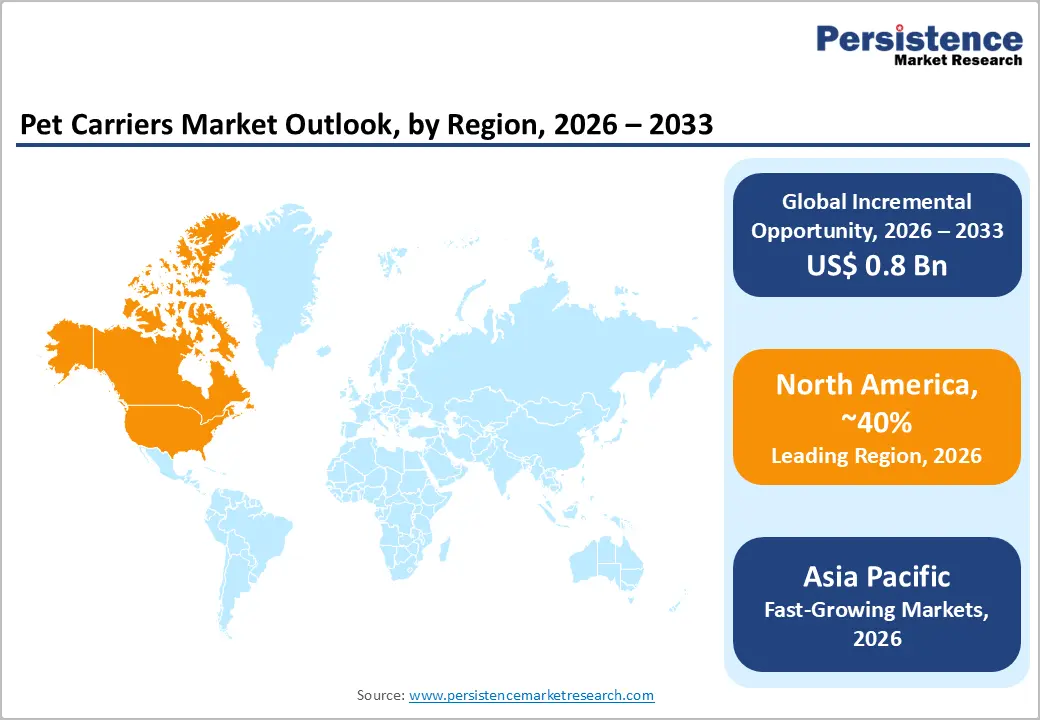

- Regional Dynamics: North America is estimated to secure around 40% market share in 2026, while Asia Pacific is forecast to register the highest growth at roughly 7.6% CAGR through 2033, led by expanding pet ownership.

| Key Insights | Details |

|---|---|

|

Pet Carriers Market Size (2026E) |

US$ 1.5 Bn |

|

Market Value Forecast (2033F) |

US$ 2.3 Bn |

|

Projected Growth (CAGR 2026 to 2033) |

6.3% |

|

Historical Market Growth (CAGR 2020 to 2025) |

5.3% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Pet Ownership and Lifestyle Integration

Global pet ownership continues to increase, driving structural demand for transport solutions. The American Veterinary Medical Association (AVMA) reports that approximately 66% of U.S. households own a pet, while over 90 million European households have companion animals. China’s urban pet population has surpassed 100 million animals in major cities. This expanding ownership base directly strengthens demand for carriers used in travel, veterinary visits, and relocation. Urban living patterns and smaller households further reinforce sustained adoption across developed and emerging markets.

The humanization trend, where pets are treated as family members, has translated into higher discretionary spending on safety and mobility products. U.S. pet industry expenditures exceeded US$ 140 billion in 2024, with accessories forming a meaningful component of non-food spending. In 2025, major hospitality chains and travel platforms reported significant growth in pet-inclusive bookings, reflecting lifestyle integration of companion animals. Increased participation in leisure travel and outdoor activities is elevating carriers from basic transport tools to essential lifestyle accessories. This behavioral shift provides durable revenue visibility for manufacturers.

Regulatory Standardization and Expansion of Pet Travel Services

The International Air Transport Association (IATA) continues to refine its Live Animals Regulations (LAR), strengthening global standards for animal transportation. In 2025, IATA introduced a dedicated digital portal to improve compliance transparency and safety validation for live animal transport. Airlines worldwide enforce carrier dimension and ventilation standards, particularly for cabin travel. As global passenger traffic recovery exceeded 90% of pre-pandemic levels, pet travel volumes have correspondingly increased. Regulatory alignment enhances demand for certified hard-shell and airline-approved soft-sided carriers.

Airline policy updates in 2025–2026 further support this structural driver. Several international carriers revised in-cabin pet policies, mandating soft-sided, under-seat compliant carriers to enhance onboard safety. In India, domestic airlines expanded pet travel services in response to rising passenger demand, increasing allowable pet weight limits and cabin allowances. These developments normalize pet air travel and reinforce compliance-driven purchasing behavior. As mobility becomes more integrated into pet ownership, standardized carriers remain a non-negotiable requirement for consumers.

Barrier Analysis - Raw Material Cost Volatility and Supply Chain Pressures

Pet carriers rely heavily on plastics, metal frames, and synthetic fabrics. Global petrochemical price fluctuations in 2025, driven by geopolitical supply disruptions and freight cost increases, elevated manufacturing costs. World Bank commodity reports indicate resin price variability exceeding 10–15% annually. Price instability in key feedstock such as benzene and derivative intermediates, which feed plastics production, has continued through late 2025, affecting price predictability for producers across sectors. These shifts make procurement planning more complex and impact short-term budgeting for carriers built with resin-based components.

Smaller manufacturers face margin compression due to limited procurement leverage. Logistics bottlenecks in Asia-based production hubs also contribute to inventory risks. Compounding these pressures, broader manufacturing activity in key regions slowed in mid-2025 as supplier deliveries lengthened and inventories built up, according to industry production indices. Delays in inbound shipments of key parts and raw materials continue to strain lead times and working capital requirements. Together, these dynamics challenge manufacturers’ ability to stabilize costs and pass consistent pricing through to distributors and retailers.

Regulatory Variability and Airline-Specific Compliance Complexity

While IATA provides global standards, airlines maintain individual carrier dimension and design requirements, creating product customization challenges. Non-compliance can result in denied boarding, undermining consumer trust and brand reputation. In mid-2025, Air Canada updated its pet travel policy to mandate soft-sided carriers only for in-cabin travel, tightening size and design requirements, which can exclude many previously compliant carrier models and increase return rates for manufacturers. This airline-specific rigidity underscores the complexity of serving global travel markets with one standard product.

Further illustrating fragmentation, multiple carriers have modified or expanded their pet travel services through 2025–2026, for example, Air India now permits cats and dogs up to 10 kg (including the carrier) in-cabin on select flights, with specific soft-carrier dimensions required, and Virgin Australia received regulatory approval to allow small pets in cabin under national safety rules. These differentiated policies require manufacturers to produce a broader range of SKU variations to meet evolving criteria. For global brands, this regulatory patchwork increases design, testing, and inventory costs, slowing product innovation and complicating cross-border distribution planning.

Premiumization and Ergonomic Product Innovation

Consumer preference is shifting toward ergonomic, lightweight, and aesthetically differentiated carriers. Demand for memory-foam bases, breathable mesh panels, and expandable compartments is rising, particularly among urban pet owners. Backpack and hybrid stroller-carrier products represent high-margin subcategories, appealing to consumers who combine daily commuting, outdoor recreation, and travel. Premium designs that prioritize comfort, safety, and style are increasingly influencing purchasing decisions, moving carriers beyond basic utility products. Emerging embedded features such as modular compartments and accessory integration further enhance consumer appeal.

Industry developments in 2025 reflect this trend toward differentiated products. The Global Pet Expo 2025 showcased hundreds of new pet accessories, including ergonomic travel solutions and innovative carrier designs that emphasize comfort and mobility, highlighting industry focus on functional premiumization. Moreover, broader travel trends in 2026 are projected to emphasize pet-inclusive policies among airlines and tourism platforms, signaling continued integration of pet travel into mainstream mobility and supporting demand for advanced carrier solutions. These shifts indicate that carriers with premium and ergonomic features will capture increasing share as pet owners seek design and performance excellence.

Geographic Expansion and Sustainable Product Development

Urbanization and rising disposable income across India, Southeast Asia, and Latin America are generating new demand corridors for pet mobility solutions. The World Bank notes sustained GDP growth above global averages in several ASEAN economies during 2024–2025. Pet adoption rates in India have grown strongly on a double-digit basis, while domestic travel bookings that include pets increased significantly, indicating expanded demand for mobility products, lodging, and transport accessories. Distribution expansion into Tier-2 cities and beyond presents scalable opportunities for organized retail and e-commerce platforms.

Sustainability is also shaping product development strategies. Major pet utility segments are increasingly adopting recycled, reusable, and biodegradable materials in manufacturing, in response to both regulatory momentum and consumer demand for circular economy products. Recent industry reporting highlights the accelerated adoption of eco-responsible materials across pet care goods, reinforcing product differentiation. In parallel, airline and transport sectors are focusing on pet travel service enhancements, further signaling broader market opportunities for carriers that align with sustainability and mobility trends. This alignment of geographic expansion and sustainable innovation unlocks significant opportunity for differentiated carrier solutions in both established and emerging markets.

Category-wise Analysis

Pet Type Insights

Dogs are likely to account for approximately 62% of the pet carriers market revenue share in 2026. High ownership levels across North America and Europe continue to anchor volume sales, particularly among small and medium breeds that require compliant travel solutions. Dog owners demonstrate higher travel frequency for leisure, relocation, and veterinary visits, directly increasing carrier utilization rates. Airline-compliant hard-shell and structured soft-sided carriers dominate this segment due to safety and regulatory compatibility. Urban apartment living has further accelerated demand for compact travel carriers suited to small-breed dogs. Product durability and reinforced locking systems remain key purchasing considerations.

Cats are likely to represent the fastest growing segment, projected to expand at approximately 7.1% CAGR from 2026 to 2033, outpacing the overall market. Urban households increasingly prefer cats due to space efficiency and lower maintenance requirements. This demographic shift supports rising demand for lightweight, foldable, and soft-sided carriers optimized for short-distance mobility. Backpack and expandable designs are gaining popularity among cat owners for veterinary visits and public transport usage. In densely populated markets such as Japan and Western Europe, compact living environments are reinforcing demand for space-saving carrier solutions. As adoption rates climb, cat-focused product innovation is expected to capture incremental share.

Product Type Insights

Soft-sided carriers are projected to hold the highest revenue share, accounting for approximately 48% of the pet carriers market sales in 2026. Their dominance stems from affordability, lightweight construction, and compatibility with airline cabin requirements. Consumers favor collapsible designs for ease of storage, particularly in urban households with limited space. Expandable mesh panels and reinforced stitching introduced post-2023 have strengthened safety perception and comfort appeal. Online platforms drive substantial sales due to easy product comparison and size filtering. The segment benefits from balanced pricing and functional versatility across both dog and cat categories.

Backpack carriers are poised to represent the fastest growing product category, projected to showcase an estimated 2026-2033 CAGR of 8.4%. Rising urban commuting patterns and outdoor recreation trends support adoption of hands-free transport solutions. Younger consumers, particularly Millennials and Gen Z, demonstrate strong preference for ergonomic and aesthetically distinctive designs. Social media visibility and influencer-led demonstrations have amplified consumer awareness of backpack formats. Lightweight frame support and ventilation enhancements further improve product acceptance. As lifestyle mobility increases, backpack carriers are expected to gain incremental market share from traditional formats.

Regional Analysis

North America Pet Carriers Market Trends

North America is likely to capture an estimated 40% of the pet carriers market share in 2026, underpinned by high pet ownership rates and significant consumer spending. The United States leads regional demand, supported by strong retail infrastructure, widespread e-commerce adoption, and cultural acceptance of pets as family members. Urbanization and frequent domestic mobility further stimulate demand for airline-compliant and travel-ready carriers. Canada mirrors U.S. trends, with continued urban pet travel interest and demand for portable carriers ensuring balanced growth across North America.

Recent industry movements reinforce this vitality. In late 2025, RetrievAir, a U.S.-based airline catering specifically to pets, expanded routes where dogs and cats can travel in the cabin with owners, demonstrating rising travel inclusivity for companion animals and signaling broader acceptance of pet mobility services. Passengers booked seats quickly, showing pet owners’ willingness to invest in convenient transport services for larger pets. This evolution in pet-centric travel strengthens carrier demand, particularly for ergonomic and regulation-compliant designs that support diverse travel formats.

Europe Pet Carriers Market Trends

Europe represents a significant market for pet carrier products, with Germany, the U.K., France, and Spain as dominant demand centers supported by large pet populations and structured consumer cultures. Harmonized safety regulations across the EU simplify cross-border trade and distribution, enabling manufacturers to serve multiple markets with consistent standards. Sustainability preferences shape material selection and product design, particularly in Western European nations where eco-certified carriers and recyclable components resonate with environmental values. Digital retail platforms also play a growing role in product accessibility and consumer education.

A notable 2025 development supporting this regional dynamic was the launch of a luxury dog hotel at Rome’s Fiumicino International Airport, offering premium care and travel services for canine companions directly at the terminal. This initiative, combined with regulatory changes allowing larger dogs in certain domestic cabin flights, underscores expanding pet travel amenities in Europe. Such service enhancements not only benefit pet owners directly but also elevate expectations for carrier quality, convenience, and comfort, especially for long-distance and airport-linked journeys.

Asia Pacific Pet Carriers Market Trends

Asia Pacific is expected to be the fastest growing regional market, likely to register an approximate CAGR of 7% between 2026 and 2033, driven by rising disposable incomes, rapid urbanization, and expanding pet ownership across major markets like China, Japan, India, and ASEAN nations. China and Japan dominate in value terms, with urban lifestyles fostering demand for innovative and space-efficient carriers. Manufacturing advantages in China and Vietnam also offer export competitiveness, supporting both regional consumption and international distribution. In developing markets such as India, price-sensitive demand for soft-sided carriers remains strong, particularly among first-time pet owners.

Virgin Australia trialed a “Pets in Cabin” service on select domestic flights, requiring soft-sided carriers that fit under passenger seats, reflecting evolving pet travel norms in Asia Pacific regions connected to Australia. This move aligns with broader regional efforts to accommodate pet mobility in travel and hospitality sectors. Additionally, Indian domestic airlines such as Akasa have updated their pet travel guidelines in early 2026, providing clearer cabin carrier specifications and demonstrating responsiveness to pet owners’ needs in expanding air travel markets. These trends support continued expansion of pet carrier demand across the Asia Pacific landscape.

Competitive Landscape

The global pet carriers market structure is moderately fragmented, with leading brands such as Petmate, Sherpa, Sleepypod, and Ferplast collectively accounting for around 40–50% of total revenue. These companies benefit from strong brand recognition, diversified product portfolios, and wide retail and e-commerce distribution. Innovation focuses on airline compliance, lightweight materials, and ergonomic design. Premium players emphasize safety certifications and aesthetic appeal to target urban consumers. Continuous product upgrades help maintain competitive positioning.

Regional manufacturers and emerging direct-to-consumer (D2C) brands intensify competition through price competitiveness and niche design offerings. Asian producers support global supply through cost-efficient manufacturing and private-label production. Sustainability-driven materials and compact, multifunctional designs are gaining traction. Entry barriers remain moderate due to regulatory compliance and brand loyalty in premium segments. Overall, competition is driven by innovation, omnichannel reach, and evolving consumer lifestyle trends.

Key Industry Developments

- In February 2026, Indian petcare platform Supertails secured US$ 30 million in a Series B round led by Venturi Partners, with participation from Nippon India Alternative Investments and Titan Capital. The funding will support expansion of 24-hour veterinary clinics, strengthen logistics infrastructure, and launch rapid quick-commerce delivery for pet products.

- In March 2025, PetScreening raised US$ 80 million in a funding round led by Volition Capital and Guidepost Growth Equity to expand operations and enhance compliance-focused product offerings. The company plans to extend its presence into adjacent markets such as short-term rentals and hotels.

- In February 2025, Sleepypod’s full line of pet carriers became the first to earn top safety ratings under the Center for Pet Safety’s new crash-test standard aligned with updated U.S. child restraint guidelines, validating their protective design and restraint performance.

Companies Covered in Pet Carriers Market

- ABB Ltd.

- Siemens AG

- Alstom Grid

- Eaton Corporation

- Schneider Electric SE

- Hitachi Energy

- Mitsubishi Electric Corporation

- GE Grid Solutions

- Parker Hannifin Corporation

- Schweitzer Engineering Laboratories, Inc.

- NARI Technology Co., Ltd.

- Guodian Electric Co., Ltd.

- Nozomi Networks, Inc.

- Cisco Systems, Inc.

- Ericsson

Frequently Asked Questions

The global pet carriers market is projected to reach US$ 1.5 billion in 2026.

Rising pet ownership, increasing pet travel frequency, urbanization, and growing demand for airline-compliant and portable solutions are key growth drivers.

The market is poised to witness a CAGR of around 6.3% from 2026 to 2033.

Premiumization trends, sustainable materials adoption, and expansion of e-commerce distribution channels present major growth opportunities.

Leading players in the market include Petmate, Sherpa (Worldwise), Sleepypod, Ferplast, and Karlie Group.