- Medical Devices

- Personal Mobility Devices Market

Personal Mobility Devices Market Size, Share, and Growth Forecast, 2026-2033

Personal Mobility Devices Market by Product Type (Wheelchairs, Mobility Scooters, Walking Aids, Patient Lifts, Stair Lifts), Technology (Manual Mobility Devices, Powered Mobility Devices, Smart Mobility Devices), End-User (Homecare Settings, Hospitals, Rehabilitation Centers, Long-Term Care Facilities), and Regional Analysis for 2026-2033

Personal Mobility Devices Market Share and Trends Analysis

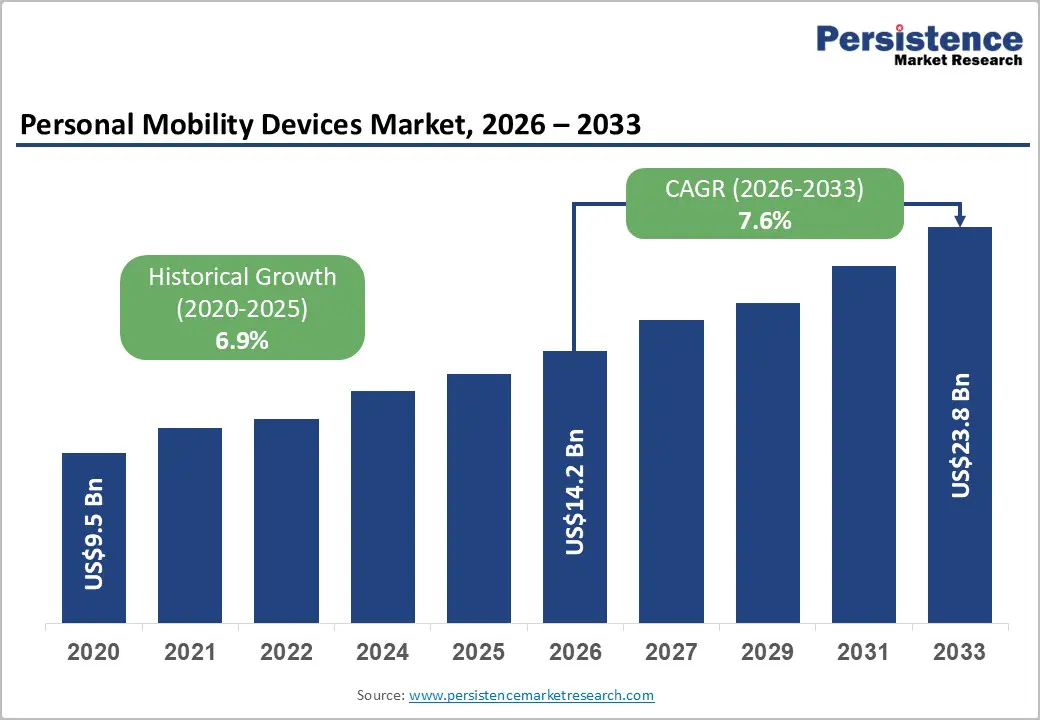

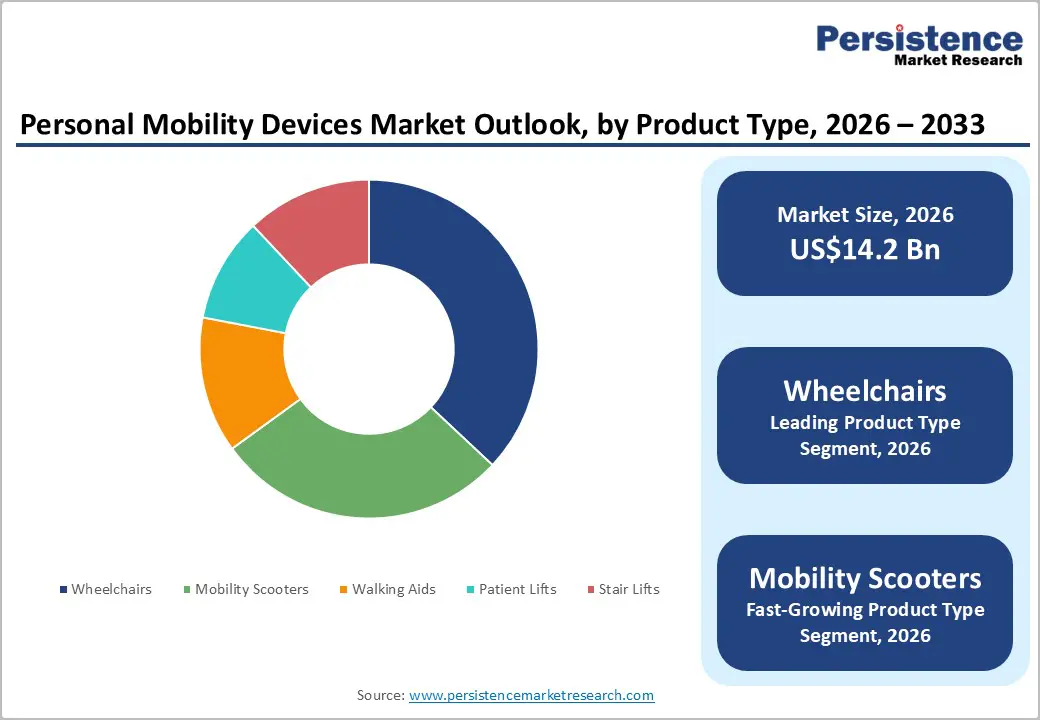

The global personal mobility devices market size is likely to be valued at US$ 14.2 billion in 2026, and is projected to reach US$ 23.8 billion by 2033, growing at a CAGR of 7.6% during the forecast period 2026–2033.

Market expansion is primarily driven by the rapidly rising global geriatric population and the increasing prevalence of mobility-limiting conditions such as arthritis, stroke, and neurological disorders. Older adults frequently require assistive technologies to maintain daily independence, which significantly increases demand for wheelchairs, mobility scooters, and walking aids. The healthcare systems are promoting independent living and aging-in-place models, encouraging the use of powered mobility devices within homecare settings. Technological advancements, including smart mobility devices with digital monitoring, navigation assistance, and connectivity features, further enhance usability. Supportive reimbursement programs and disability assistance policies across developed healthcare markets continue improving accessibility to assistive mobility devices, strengthening long-term market growth.

Key Industry Highlights

- Dominant Product Type: Wheelchairs are set to command around 37% revenue share in 2026, while mobility scooters are likely to grow the fastest at about 8.9% CAGR through 2033, fueled by increasing demand for independent mobility among elderly users.

- Leading Technology: Manual mobility devices are expected to lead with nearly 52% share in 2026, while smart mobility devices are projected to be the fastest-growing during 2026–2033, driven by IoT integration and digital health monitoring capabilities.

- Dominant End-User: Homecare settings are anticipated to account for approximately 42% revenue share in 2026, while rehabilitation centers are likely to grow the fastest through 2033, reflecting expanding rehabilitation programs worldwide.

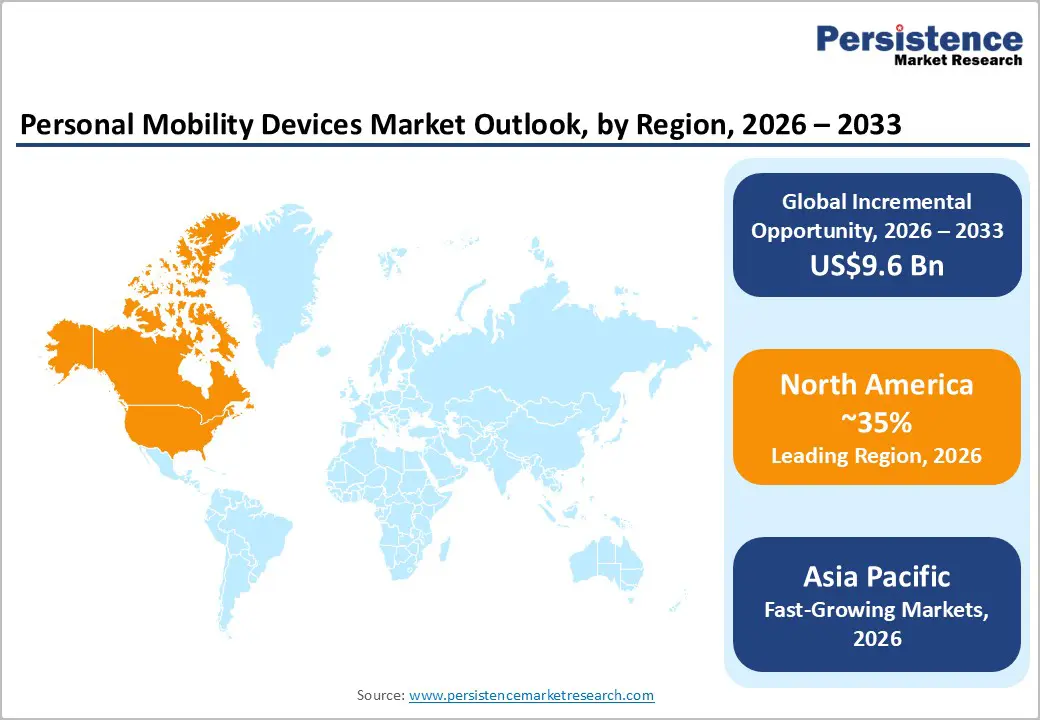

- Regional Leadership: North America is poised to dominate with an estimated 35% share in 2026, supported by strong reimbursement systems and advanced healthcare infrastructure.

- Fastest-Growing Market: Asia Pacific is expected to register the fastest growth at around 9.1% CAGR during 2026–2033, driven by rapidly aging populations and improving healthcare access.

- Innovation Trends: Innovations such as AI-assisted navigation, remote diagnostics, and enhanced battery efficiency are promoting the adoption of powered mobility devices and smart connected mobility solutions.

| Key Insights | Details |

|---|---|

| Personal Mobility Devices Market Size (2026E) | US$ 14.2 Bn |

| Market Value Forecast (2033F) | US$ 23.8 Bn |

| Projected Growth (CAGR 2026 to 2033) | 7.6% |

| Historical Market Growth (CAGR 2020 to 2025) | 6.9% |

Market Factors – Growth, Barriers, and Opportunity Analysis

Rising Global Aging Population and Mobility Impairment Prevalence

The rapid increase in the elderly population is a key structural driver for the personal mobility devices market. According to the World Health Organization (WHO), the global population aged 60 years and above will reach 2.1 billion by 2050, nearly doubling from 1 billion in 2020. Aging is strongly associated with mobility limitations such as osteoarthritis, muscle degeneration, and neurological disorders, which significantly increase demand for wheelchairs, walking aids, and mobility scooters. The United Nations Department of Economic and Social Affairs (UN DESA) also reports that one in six people worldwide will be over 65 by 2050. As healthcare providers focus on maintaining functional independence for elderly individuals, the demand for assistive mobility technology continues to grow across homecare and long-term care facilities.

Healthcare systems are increasingly emphasizing independent living and aging-in-place care models, which directly support the adoption of assistive mobility devices. Many elderly individuals prefer remaining in their homes rather than relocating to institutional care facilities, which has increased demand for home-friendly mobility products. Devices such as lightweight wheelchairs, ergonomic walking aids, and compact mobility scooters enable users to maintain daily activities with minimal assistance. Long-term care facilities and home healthcare providers are also integrating mobility technologies into patient support programs. This demographic shift is therefore creating a sustained and predictable demand base for personal mobility equipment worldwide.

Growing Prevalence of Chronic Diseases and Disabilities

Chronic diseases that impair mobility are increasing globally, driving consistent demand for personal mobility devices. The U.S. Centers for Disease Control and Prevention (CDC) reports that approximately 61 million adults in the United States live with a disability, many of which involve mobility limitations. Similarly, the Global Burden of Disease Study indicates that musculoskeletal disorders affect over 1.7 billion people worldwide, making them one of the largest contributors to disability. Conditions such as stroke, spinal cord injuries, and Parkinson’s disease require long-term mobility assistance through devices such as patient lifts, wheelchairs, and powered mobility scooters. As healthcare systems shift toward rehabilitation-focused care models, the need for advanced mobility support devices continues to expand.

Technological advancements are transforming the assistive mobility devices market, particularly with the emergence of powered mobility devices and smart mobility technologies. Innovations such as AI-assisted navigation, obstacle detection, remote health monitoring, and IoT-enabled mobility scooters are improving safety and usability. According to the International Society of Wheelchair Professionals (ISWP), powered wheelchairs now account for a growing share of device adoption in developed markets due to improved battery efficiency and ergonomic design. In addition, manufacturers are integrating smart sensors, telehealth connectivity, and remote diagnostics, making mobility devices more attractive to healthcare providers and rehabilitation centers. These technological enhancements significantly improve quality of life while expanding commercial opportunities for device manufacturers.

High Cost of Advanced Mobility Devices

Despite technological progress, the high cost of advanced powered mobility devices remains a major barrier to adoption, particularly in developing economies. Powered wheelchairs and smart mobility scooters can cost between US$ 2,000 and US$ 15,000, depending on customization and technology integration. Limited reimbursement coverage in many countries restricts accessibility, especially for low-income patients. According to WHO Assistive Technology reports, only one in ten individuals globally has access to assistive products they require, largely due to cost barriers. This affordability gap continues to slow adoption rates in emerging markets despite increasing demand.

Recent industry developments continue to highlight the scale of this affordability challenge. Reports in 2025 indicated that more than one billion people globally still lack access to essential assistive products, including mobility aids, largely due to pricing barriers and limited healthcare coverage. In many low- and middle-income countries, import duties, limited local manufacturing, and inadequate subsidy programs further increase device costs. As a result, many healthcare systems prioritize basic walking aids over advanced powered mobility devices. Without broader insurance coverage and government procurement programs, the cost structure of advanced devices remains a structural restraint for large-scale market adoption.

Regulatory and Reimbursement Complexity

Medical device regulations and reimbursement frameworks vary significantly across regions, creating barriers for manufacturers entering new markets. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) impose strict product safety, certification, and clinical evaluation requirements. These compliance processes often increase product development costs and delay commercialization timelines. Additionally, reimbursement coverage for mobility devices is inconsistent across healthcare systems, creating uncertainties in procurement for hospitals and rehabilitation centers.

Recent policy developments illustrate how reimbursement differences across countries can influence market accessibility. For example, policy reforms announced in France in 2025 introduced full public reimbursement for standard wheelchairs under national health insurance, highlighting how regulatory and funding frameworks can significantly affect device affordability and adoption. However, similar coverage policies remain absent in emerging regional markets, creating fragmented global reimbursement environments. Manufacturers must therefore navigate diverse approval processes, procurement standards, and funding mechanisms, which increases administrative complexity and slows the international expansion of assistive mobility devices.

Expansion of Home Healthcare and Independent Living Solutions

The shift toward home healthcare services is creating significant opportunities for the personal mobility devices market. According to the WHO, community-based healthcare and homecare models are expected to serve an increasing proportion of elderly patients due to healthcare cost pressures and patient preference for independent living. Mobility devices such as walking aids, mobility scooters, and portable patient lifts are increasingly used in home environments to reduce hospital visits and support daily mobility. As healthcare providers encourage patients to remain in familiar living environments, demand for reliable assistive mobility solutions is expanding steadily.

Global health organizations are increasingly prioritizing assistive technology access as part of universal healthcare frameworks. The World Health Organization estimates that more than 2.5 billion people worldwide require at least one assistive product, including mobility aids such as wheelchairs and walkers, highlighting the scale of unmet demand in the market. Governments and healthcare systems are therefore expanding home-based care programs and assistive device distribution initiatives to reduce institutional healthcare costs while improving patient independence. This shift toward decentralized healthcare delivery is expected to create sustained demand for portable, lightweight, and home-compatible mobility devices.

Emerging Market Expansion and Smart Mobility Device Integration

Developing regions present substantial growth potential for assistive mobility devices manufacturers. Countries such as China, India, and Brazil are experiencing rapid demographic shifts toward aging populations while simultaneously expanding healthcare infrastructure. According to the World Bank, healthcare expenditure in emerging economies has increased significantly over the past decade, improving access to assistive technologies. Additionally, government programs focused on disability inclusion and elder care are increasing procurement of wheelchairs, walking aids, and rehabilitation mobility equipment. These trends create favorable conditions for manufacturers offering cost-efficient mobility solutions tailored to high-population emerging markets.

The convergence of digital health technologies with mobility solutions is generating new commercial opportunities. Research institutions and technology developers are increasingly designing smart mobility devices that integrate sensors, automated navigation, and health monitoring features. For example, next-generation powered wheelchairs are now being developed with multi-modal control systems and real-time health monitoring capabilities, allowing caregivers to track vital signs and mobility activity remotely. In parallel, organizations such as the Royal Society have emphasized the importance of collaborative innovation in assistive technologies to accelerate the development of inclusive digital mobility tools. These developments highlight the growing market opportunity for connected and AI-enabled mobility devices that support remote healthcare and patient independence.

Category-wise Analysis

Product Type Insights

Wheelchairs are expected to hold approximately 37% of the personal mobility devices market revenue share in 2026. These devices serve as essential mobility solutions for individuals with long-term or severe mobility impairments, including spinal cord injuries, neurological conditions, and advanced age-related disabilities. Hospitals, rehabilitation centers, and long-term care facilities continue to depend on both manual and powered wheelchairs to support patient mobility and independence. Continuous innovation is also enhancing product capabilities through improved ergonomics, motorized systems, and terrain adaptability. For instance, Permobil launched upgraded F-series front-wheel drive powered wheelchairs featuring enhanced seating ergonomics, advanced suspension, and improved digital control systems designed to improve posture support and user maneuverability.

Mobility scooters are anticipated to register the highest 2026-2033 CAGR of around 8.9%. Growth is strongly associated with increasing demand from aging populations seeking independent outdoor mobility and improved lifestyle convenience. Mobility scooters offer greater range and comfort compared with traditional wheelchairs, making them suitable for daily commuting, shopping, and recreational activities. Advances in lithium-ion battery systems, lightweight frames, and foldable designs are also expanding their usability in urban environments. Manufacturers are increasingly focusing on compact and travel-friendly scooter models to address portability needs. In 2026, Pride Mobility Products introduced updated versions of its Go-Go travel scooter series, integrating longer-range batteries, modular disassembly systems, and improved suspension aimed at enhancing outdoor mobility for elderly users.

Technology Insights

Manual mobility devices are expected to dominate by accounting for approximately 52% of the market share in 2026. Products such as manual wheelchairs, walkers, rollators, and crutches remain widely used due to their affordability, mechanical simplicity, and minimal maintenance requirements. Healthcare systems in developing and cost-sensitive markets frequently prioritize manual devices for large-scale distribution through public health and disability assistance programs. Their reliability and ease of use also make them common in hospitals and rehabilitation centers where basic mobility support is required. Government procurement initiatives continue to play an important role in expanding access to these devices. Supporting the momentum, National Health Services (NHS) England expanded procurement frameworks for essential assistive equipment, including manual wheelchairs and walking aids to strengthen accessibility for patients with long-term disabilities across community healthcare settings.

Smart mobility devices are forecast to grow the fastest through 2033. These advanced devices incorporate technologies such as IoT sensors, GPS navigation, obstacle detection systems, and remote health monitoring capabilities. Intelligent mobility solutions are designed to enhance user independence while improving safety through automated navigation assistance and fall detection features. Healthcare providers are increasingly recognizing the value of connected mobility devices for remote patient monitoring and digital health integration. The convergence of robotics, artificial intelligence, and assistive mobility technology is expected to accelerate innovation in this field. In 2025, WHILL launched the Model R mobility scooter, designed with smart control systems, tight turning radius capability, and enhanced suspension to support urban navigation and connected mobility applications.

Regional Insights

North America Personal Mobility Devices Market Trends

North America is anticipated to secure roughly 35% of the personal mobility devices market share in 2026. The United States represents the largest contributor, supported by its advanced healthcare infrastructure and rapidly expanding elderly population. According to the U.S. Census Bureau, adults aged 65 and older are projected to represent nearly 22% of the U.S. population by 2040, significantly increasing the need for assistive mobility devices, including wheelchairs, mobility scooters, and walking aids. Strong reimbursement frameworks also strengthen adoption across healthcare systems. Programs administered by Centers for Medicare & Medicaid Services provide coverage for medically necessary mobility equipment when prescribed by healthcare professionals. These policies ensure accessibility to mobility solutions for millions of patients requiring long-term assistance.

The region also benefits from a strong innovation ecosystem that supports development of advanced powered mobility devices and smart mobility technologies. Medical device manufacturers across the United States and Canada continue investing in ergonomic design improvements, digital connectivity features, and battery performance enhancements. Regulatory oversight from the U.S. FDA ensures strict product safety and performance standards, reinforcing user trust in assistive technologies. In addition, partnerships between healthcare providers and device manufacturers are accelerating adoption of digitally connected mobility solutions. Continuous investments in rehabilitation infrastructure, homecare services, and disability support programs further reinforce North America’s leadership in the personal mobility devices market.

Europe Personal Mobility Devices Market Trends

Europe represents a well-established regional market for personal mobility devices. Germany, the United Kingdom, France, and Spain contribute significantly to regional demand due to well-developed healthcare systems and comprehensive disability support policies. According to the European Commission (EC), more than 20% of the European population is aged 65 or older, creating sustained demand for assistive mobility devices such as wheelchairs, walking aids, and stair lifts. Public healthcare coverage programs across several European nations provide partial or full reimbursement for essential mobility devices, which helps maintain steady market penetration. These policies support accessibility for elderly populations and individuals living with long-term mobility impairments.

Regulatory harmonization has further strengthened the regional market environment. The European Union (EU) Medical Device Regulation (MDR) has standardized product approval and safety requirements across the region, ensuring high-quality mobility equipment while improving market transparency for manufacturers. Innovation within Europe also focuses on lightweight materials, ergonomic device design, and energy-efficient mobility technologies. Many manufacturers are prioritizing sustainable production practices and recyclable materials in response to environmental regulations. Additionally, partnerships between rehabilitation centers and mobility device suppliers are expanding patient access to customized assistive equipment.

Asia Pacific Personal Mobility Devices Market Trends

Asia Pacific is projected to be the fastest-growing market, expected to expand at a CAGR of approximately 9.1% between 2026 and 2033. Rapid demographic transitions across countries such as China, Japan, and India are significantly increasing the demand for personal mobility devices. According to Japan Ministry of Internal Affairs and Communications, nearly 30% of Japan’s population is already aged 65 or older, making it one of the world’s most rapidly aging societies. China is also witnessing strong demographic shifts, with the National Bureau of Statistics of China reporting steady expansion of the elderly population. These demographic patterns are increasing the need for mobility aids, rehabilitation equipment, and homecare mobility solutions across the region.

Asia Pacific also benefits from strong manufacturing capabilities that support cost-efficient production of wheelchairs, walking aids, and powered mobility devices. Many global medical device manufacturers operate production facilities across China and Southeast Asia to leverage established supply chains and competitive manufacturing costs. This manufacturing advantage enables companies to deliver affordable assistive technologies to emerging markets while supporting export demand. Governments across the region are also expanding disability support programs and elderly care initiatives to address the needs of aging populations. Investments in healthcare infrastructure and rehabilitation services are further strengthening regional demand for assistive mobility technologies, reinforcing Asia Pacific’s position as the fastest-growing market globally.

Competitive Landscape

The global personal mobility devices market structure remains moderately fragmented, with major manufacturers such as Invacare Corporation, Permobil, Sunrise Medical, and Pride Mobility Products holding significant revenue shares. These companies maintain strong market positions through extensive distribution networks and long-standing partnerships with hospitals and rehabilitation centers. Their product portfolios span wheelchairs, mobility scooters, and walking aids across manual and powered categories. Steady R&D investment supports innovation in powered mobility devices and smart assistive technologies, ensuring competitive differentiation and supporting premium product positioning.

Regional and specialized mobility device manufacturers also play an important role in shaping the competitive landscape. Companies such as Drive DeVilbiss Healthcare and WHILL are focusing on compact and technologically advanced mobility solutions. However, digital health integration and IoT-enabled mobility solutions are enabling new technology partnerships. Strategic collaborations, product innovation, and expansion into emerging healthcare markets are expected to intensify competition in the assistive mobility devices market.

Key Industry Developments

- In December 2025, ALIMCO launched a three-wheeler electric scooter and a clip-on motorized wheelchair add-on, aimed at improving mobility and independence for persons with disabilities. The wheelchair attachment converts manual chairs into battery-powered units, marking a shift toward smart, accessible assistive technologies in India.

- In September 2025, Decon Mobility signed an agreement to acquire Spain-based Batec Mobility, a manufacturer of premium electric add-on handbikes. The acquisition aims to strengthen Decon’s power-assist mobility portfolio and expand its global distribution network.

- In July 2025, Sunrise Medical announced the acquisition of Norway-based Made for Movement, a developer of neurorehabilitation therapeutic devices. The deal expands Sunrise Medical’s rehabilitation technology portfolio, adding clinically validated solutions such as Innowalk and NF-Walker.

Companies Covered in Personal Mobility Devices Market

- Invacare Corporation

- Sunrise Medical

- Ottobock SE & Co. KGaA

- Pride Mobility Products Corp.

- Permobil AB

- Drive DeVilbiss Healthcare

- GF Health Products Inc.

- Karma Medical Products Co. Ltd.

- Medline Industries LP

- Kaye Products Inc.

- Arjo AB

- Hill-Rom Holdings

- Etac AB

- Hoveround Corporation

Frequently Asked Questions

The global personal mobility devices market is projected to reach US$ 14.2 billion in 2026.

Rising aging population, increasing prevalence of mobility impairments, and growing demand for assistive mobility devices in home care settings are driving market growth.

The market is poised to witness a CAGR of 7.6% from 2026 to 2033.

Expansion of home healthcare services, growth in emerging economies, and innovation in smart mobility devices are creating strong market opportunities.

Key companies in the market include Invacare Corporation, Permobil, Sunrise Medical, and Pride Mobility Products.